Exploring Accounting System of Non-profit

Organizations in Indonesia : An Organizational

Ethnography Study

学位名

博士 (先端マネジメント)

学位授与機関

関西学院大学

学位授与番号

34504甲第647号

i

Doctoral Dissertation

For Doctoral Degree

Kwansei Gakuin University

Exploring Accounting System of Non-profit Organizations in Indonesia:

An Organizational Ethnography Study

Doctoral research advisor: Professor Noriaki Yamaji

June, 2017

Graduate Department of Advanced Management (Ph.D)

Institute of Business and Accounting

ii 第 23 章 1主はわたしの牧者であって、わたしには乏しいことがない。 2主はわたしを緑の牧場に伏させ、いこいのみぎわに伴われる。 3主はわたしの魂をいきかえらせ、み名のためにわたしを正しい道に導かれる。 4たといわたしは死の陰の谷を歩むとも、わざわいを恐れません。 あなたがわたしと共におられるからです。 あなたのむちと、あなたのつえはわたしを慰めます。 5あなたはわたしの敵の前で、わたしの前に宴を設け、わたしのこうべに油をそそがれる。 わたしの杯はあふれます。 6わたしの生きているかぎりは必ず恵みといつくしみとが伴うでしょう。 わたしはとこしえに主の宮に住むでしょう。 Psalm 23 A psalm of David. 1 The L

ORD is my shepherd, I lack nothing. 2 He makes me lie down in green pastures, he leads me beside quiet waters,

3

he refreshes my soul.

He guides me along the right paths for his name’s sake.

4 Even though I walk through the darkest valley, I will fear no evil,

for you are with me; your rod and your staff, they comfort me.

5 You prepare a table before me in the presence of my enemies. You anoint my head with oil; my cup overflows.

6 Surely your goodness and love will follow me all the days of my life,

and I will dwell in the house of the LORD

forever.

iii

Abstract

Non-Profit Organizations (NPOs) in Indonesia as a part of civil societies have a very long history. NPOs are commonly referred to Society Self-Supporting Institutions (Lembaga Swadaya Masyarakat/LSM) which have rapidly grown in the last decades. At the same time, they have been facing many obstacles. Financial reporting is one of the essential issues. This concern has been leading them to another challenge which is accountability and transparency. However, the root problem of financial reporting issue is not noticeably solved. The accounting system is an infrastructure in the organizations, both profit-oriented and non-profit organizations. Two different types of organizations have different characteristics, such as goals and business process. Therefore, this research gap has been urging to initiate a study about accounting systems for NPOs in Indonesia which is supposed to view NPOs with broader infrastructure needs and analysis the necessity of accounting systems in fundamental point of view.

The main objective of the research is to thoroughly explore the accounting system for NPOs in Indonesia and fulfill the research gaps between the need of financial reporting and the challenge of accountability and transparency. This study has employed qualitative methodology under the organizational ethnography in the chosen NPOs, Child Development Centers (CDCs), with supporting of the archival and action methods. The research attempts to view the facts of NPOs in Indonesia, to understand two basic frameworks in the financial reporting: the financial accounting standards and the accounting basis, and then to provide a general accounting system model as a benchmark, also to propose an NPO accountability system as a point of reference.

The result of the study has shown thatNPOs in Indonesia, a part of CSOs, have been built by restrictions and crisis. After a long history and under the influence of Indonesia politics, they have been growing in numbers and a variety of services and functions. Dealing with crisis and poverty is the main motivation. Building a better young generation through education is the best service option for most NPOs. Even though it still needs improvement to deal with some weaknesses, Indonesian government recognizes NPOs’ important role in society. The government itself needs to improve and equip their assistance to NPOs, but it has shown that there is a good willingness from the government to enhance NPOs’ capacity and position.

iv

Regarding financial reporting, the establishment of financial accounting standards for NPOs in Indonesia, PSAK 45, did not have strong background history and process. Most content of the standard is a translation from SFAS 117 of the US GAAP. Even though PSAK 45 is not sufficient enough for NPOs in Indonesia, SAK-ETAP and SAK accompanying PSAK 45 has been creating flexibility in financial reporting. The facts, however, NPOs in Indonesia seem quite difficult to apply PSAK on their financial reporting process. In addition, the standard do not suggest applying any accounting basis. However, the provided example in the statement seems using accrual basis. The fact is that not all NPOs apply it in their financial reporting process to publish their financial statements. The study in CDCs, the result has shown that in a broader organization, where CDCs are part of Compassion International (CI), different accounting basis is applied for different level of organization: the accrual accounting in CI, the modified cash basis in CIF, and the cash basis in CDCs. Hence, choosing an accounting basis is not about the best basis, but which basis is the most appropriate to the nature and business process of the NPO.

Finally, the study has resulted a general model of accounting system. The accounting system of CDCs is a part of the larger systems of CI. It consists of transaction cycles and accounting cycles. It has five cycles: the revenue cycle, the expenditure cycle, the payroll cycle, the operation cycle, and the financing cycle, as well as a general ledger and reporting system. All five cycles interface with the reporting system, which consists of all activities related to the preparation of financial statements and other managerial reports. Because of budget-based transactions, setting the budget is the key success of running the accounting systems in NPOs. Therefore, an accounting cycle model of NPOs should be different from that of POs. In NPOs, it is called as the budget-based accounting cycle. Along with the proposed accounting cycle, the study also suggests a different definition of adjustments. Furthermore, the proposed accounting system includes the internal control systems. The internal control serves a part of accountability. The non-profit accountability system is collaborative efforts and controls of an NPO. It is not only about efforts what NPOs do, but also controls what NPOs not do. Accountability requires a relational principle among the actors. This principle leads the accountability to the trusting attitude among the actors. To maintain the trust, there should be mechanisms to follow. In other words, accountability is about trust. NPOs tend to reach a certain level of trust to convince themselves first, then stakeholders, about their mission and operation. For NPOs, being accountable organization is already legitimacy.

v

Table of Contents

Abstract ... iii Table of Contents ... v Chapter 1 Introduction ... 1 1.1 Background ... 1 1.2 Objectives ... 6 1.3 Research Questions ... 6 1.4 Research Significances ... 6 1.5 Research Methodology ... 7 1.6 Scope ... 9 1.7 Research Structure ... 9Chapter 2 Introducing Non-Profit Organizations in Indonesia... 12

2.1 Background ... 12

2.2 Non-Profit Organizations: Definition and Characteristics ... 13

2.3 Categories of NPOs... 16

2.3.1 International Classification of Non-Profit Organizations (ICNPO) ... 16

2.3.2 Indonesian Classification of Non-Profit Organizations ... 17

2.4 Non-Profit Organizations in Indonesia ... 19

2.4.1 Indonesia Facts and Figures ... 19

2.4.2 Historical Background ... 20

2.4.3 Numbers ... 23

2.4.4 Research on NPOs in Indonesia ... 25

2.5 Non-profit Organizational Behavior ... 28

2.5.1 Alternatives Terminology of Non-profit ... 28

2.5.2 Non-profit’s Structure ... 29

2.5.3 NPOs in Indonesia: Analysis and Representatives ... 31

2.6 NPO in the Research: Child Development Centers ... 34

2.7 Conclusion ... 37

Chapter 3 Criticizing Accounting Standards for Non-Profit Organizations in Indonesia ... 39

3.1 Background ... 39

3.2 Indonesian Financial Accounting Standards ... 41

3.2.1 Historical Background ... 41

3.2.2 Financial Accounting Standard for NPOs ... 42

3.3 Referred Accounting Standards ... 44

3.3.1 Statement of Financial Accounting Concepts No. 4 ... 44

3.3.2 Statement of Financial Accounting Standards No. 116 ... 45

3.3.3 Statement of Financial Accounting Standards No. 117 ... 47

3.4 Findings and Analysis ... 50

3.4.1 Comparison Facts ... 50

3.4.2 Discussion ... 54

3.4.3 Application ... 57

3.5 Conclusions ... 60

Chapter 4 Analyzing Applied Accounting Basis for Non-profit Organizations in Indonesia ... 62

4.1 Introduction ... 62

4.2 Literature Review... 64

4.3 Findings and Discussion ... 73

vi

Chapter 5 Reviewing Non-profit Accounting Systems Design for Non-profit Organizations in

Indonesia ... 81

5.1 Background ... 81

5.2 Literature Review... 83

5.3 Research Methodology ... 92

5.4 Findings and Analysis ... 93

5.4.1 Ethnographic Case Study: Child Development Centers ... 93

5.4.2 General Model of Transaction Cycles ... 105

5.4.3 Proposed Accounting Cycle Model ... 124

5.5 Discussion ... 125

5.6 Conclusion ... 130

Chapter 6 Developing Accountability Systems for Non-profit Organizations in Indonesia ... 132

6.1 Background ... 132

6.2 Literature Review... 133

6.3 Research Methodology ... 140

6.4 Findings and Analysis ... 141

6.4.1 Ethnographic Case Study: Child Development Centers ... 141

6.5 Conclusion ... 147 Chapter 7 Conclusion ... 148 7.1 Findings ... 148 7.2 Further Research ... 155 Bibliography ... 156 Appendix 1 ... 166 Appendix 2 ... 167 Appendix 3 ... 168 Appendix 4 ... 169 Appendix 5 ... 170 Appendix 6 ... 171 Appendix 7 Strength in Numbers: Annual Report of Compassion International 2015-2016

Appendix 8 Compassion International, Incorporated and Affiliates: Consolidated Financial Statements June 30, 2016 and 2015

vii

Abbreviations

AICPA The American Institute of Certified Public Accountants

CBO Community Based Organization

CDC Child Development Center

CI Compassion International

CIF Compassion Indonesia Foundation

CS Child Sponsor

CSO Civil Society Organization

DFAT Department of Foreign Affairs and Trade

DFD Data Flow Diagram

FASB Financial Accounting Standard Board

GAAP Generally Accepted Accounting Principles

GDP Gross Domestic Product

IAI Ikatan Akuntan Indonesia (Institute of Indonesia Chartered Accountants)

ICNPO International Classification of Non-profit Organizations

IDR Indonesia Rupiahs

INGO International Non-Governmental Organization

IO Indonesia (Code for Indonesia Office)

IPSAK Interpretasi Pernyataan Standar Akuntansi Keuangan (Interpretation of SFAS)

IT Information Technology

KKB Koalisi Kebebasan Berserikat (Coalition for the Freedom of Association)

NPO Non-Profit Organization

NGO Non-Governmental Organization

PAI Prinsip Akuntansi Indonesia (Indonesian Accounting Principles)

PC Partner Church

PO Profit-oriented Organization

PSAK Pernyataan Standar Akuntansi Keuangan (Statement of Financial Accounting

Standard)

viii

SAK-ETAP SAK –Entitas Tanpa Akuntabilitas Publik (Financial Accounting Standards for

Non-Publicly-Accountable Entities)

SFAC Statement of Financial Accounting Concept

SFAS Statement of Financial Accounting Standard

SNA System of National Accounts

UN United Nations

YBK Yayasan Bantuan Kasih (Registered name of Compassion Indonesia Foundation)

YCAB Yayasan Cinta Anak Bangsa

ix

List of Tables

Table 2.1 Comparison Two NPO Satellite Account Definitions

Table 2.2. ICNPO: groups and subgroups

Table 2.3 Milestones History of Indonesian CSOs

Table 2.4 Legal Form of NPOs

Table 2.5 NPOs based on ICNPO

Table 2.6 Profile CDCs in Salatiga Cluster

Table 3.1 History of SAK 45

Table 3.2 Referred Facts of PSAK 45 to American Accounting Standards

Table 3.3 Suggested Terminologies in PSAK 45

Table 3.4 Compilation of the Audited Financial Statements of NPOs in Indonesia

Table 4.1 Applied Accounting Basis of NPOs in Indonesia

Table 4.2 Accrual Financial Reporting by Budget Funded Agencies

Table 5.1 Threats and Controls in the Revenue Cycle

Table 5.2 Threats and Controls in the Expenditure Cycle

Table 5.3 Threats and controls in the Payroll Cycle

Table 5.4 Threats and Controls in the Operation Cycle

Table 5.5 Threats and Controls in the Financing Cycle

Table 5.6 Threats and Controls in the General Ledger and Reporting System

Table 6.1 Characteristics of Accountability Mechanisms

x

List of Figures

Figure 1.1 Porter’s Value Chain Concept

Figure 2.1 Overview the Child Development Model

Figure 2.2 Cities in Indonesia where there are CDCs

Figure 3.1 Flow of Reporting in Compassion

Figure 4.1 Modified Give and Take Exchanges in CDCs

Figure 4.2 Modified Transaction cycles

Figure 4.3 Different Accounting Basis for Different Level of Organization

Figure 5.1 Accounting System Function

Figure 5.2 Factors Influencing Design of the Accounting Systems

Figure 5.3 General Accounting Cycle

Figure 5.4 Gray’s Model of Culture, Societal Values and the Accounting Sub-culture

Figure 5.5 Give and Take Exchanges in CDCs

Figure 5.6 Accounting Systems and Its Subsystems in CDCs

Figure 5.7 Revenue Cycle in CDCs

Figure 5.8 Expenditure Cycle in CDCs

Figure 5.9 Payroll Cycle in CDCs

Figure 5.10 Operation Cycle in CDCs

Figure 5.11 Financing Cycle in CDCs

Figure 5.12 General Ledger and Reporting Systems in CDCs

Figure 5.13 Accounting Cycle in CDCs

Figure 5.14 General Give and Take Exchanges

Figure 5.15 General Model of Revenue Cycle

Figure 5.16 General Model of Expenditure Cycle

Figure 5.17 General Model of Payroll Cycle

Figure 5.18 General Model of Operation Cycle

Figure 5.19 General Model of Financing Cycle

Figure 5.20 General Model of General Ledger and Reporting System

xi

Figure 5.22 Types of Information for Stakeholders

Figure 6.1 Accountability System Framework of CDCs

xii

Acknowledgements

It is not about the destination, it is about the journey.

First and foremost, praise and thanks goes to my savior Jesus Christ for the many blessings undeservingly bestowed upon me. I am very grateful to experience this amazing excitement and priceless process.

This work would not have been possible without the scholarship of the Directorate General for Science & Technology Institution and Higher Education, Indonesia. I also thank the Faculty of Information Technology - Satya Wacana Christian University for the top-up financial support. I feel extremely privileged and grateful to all members of Child Development Centers for their support and services.

I would like to express the deepest appreciation to my advisor, Professor Noriaki Yamaji for his guidance and persistent helps. I would also like to thank Professor Koji Ueda and Professor Koji Kojima for their inspiring critiques and valuable suggestions.

Nobody has been more important to me in the pursuit of this study than my family. I would like to thank my eternal cheerleaders, my beloved mother - Maryani and two wonderful sisters - Wiwik and Ayu. Their presence, love, encouragement and pray are always with me.

My experience at the Kwansei Gakuin University particularly and in Japan generally was greatly enhanced by the interaction with faculty members and staff, other students, fellow doctoral students, church members, and friends from Indonesia and around the world. Thank you.

1

Chapter 1 Introduction

1.1 Background

Non-Profit Organizations (NPOs) in Indonesia as a part of civil societies have a very long history. In general, an NPO is usually associated with Non-Governmental Organization (NGO). However, in Indonesia, NPOs are commonly referred to Society Self-Supporting Institutions (Lembaga Swadaya Masyarakat/LSM) which have rapidly grown in the last decades. In the New Order era from 1965 until 1998, numbers of NPOs were very limited, since the repression of political expression and engagement, and laws limiting the right to associate were enforced during the period. Then, the start of decentralization in the early 2000s furthered this proliferation. In 2010, the official number of NPOs that have been registered in the Ministry of Law and Human Rights of Indonesia was 21,569. However, this sector has to overcome several issues, which are legal, financial, and human resources and organization (World Bank, 2010, p. 41).

Related to the financial issues, many NPOs are not transparent to publish their financial reporting and program implementation (World Bank, 2010, p.42). It has been reported that the Indonesia government has not even been able to monitor the complete NPO profiles and management, financial reporting, and activities (World Bank, 2010, p.121). It is indeed difficult to discover NPOs information on the website. The financial reports of foreign-based NPOs, however, are relatively easy to access. As nonprofits are asked to show greater transparency and accountability in their financial operations, the need to improve accounting and reporting systems becomes more pressing (De Vita and Flemming, 2001, p.20).

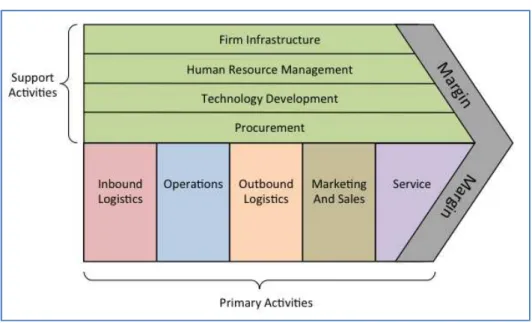

According to Porter’s value chain concept in Figure 1.1, to provide value to their customers, an NPO as an organization should perform some different activities. Different kind of organizations will have different purposes and customers. The purpose of profit organization establishment is to gain profit. Primary activities in the profit-oriented organizations (POs) are generally to transform the resource into products or services to be sold. The selling price is formed of the cost of product or service added to profit margin. In order to run the business, POs have a loan from creditor or investment from the investor. Creditors and investors both also have profit orientation. Contradictory, NPOs have no profit goal. The prime focus in the organizations is to accomplish

2

programs that confirm the organization mission. NPOs perform on its programs provided rather than on improving profit. This kind of performance is not easily conceptualized or rendered calculable, especially when programs are often intangible and the demands of stakeholders so variant (Hoque and Parker, 2015, p.15). The programs are funded by donors who would like to grant their asset to the organizations. This purpose drives NPOs to have different main activities. To allow primary activities to be performed efficiently and effectively, NPOs need support activities, which are infrastructure, human resources, technology, and procurement. On the other side, similar to profit organizations, a business process in NPOs will also be accounted by the management through financial reports. In other words, financial reports have a main function as a form of management’s accountability to stakeholders or accountability is the cornerstone of all financial reporting.

Figure 1.1 Porter’s Value Chain Concept

Source: Romney and Steinbart, 2015

In order to produce financial reports, organizations need the main infrastructure which is part of support activities. It is called as accounting systems. The fact is that most of the accounting systems literature studied about the systems of POs. While in Indonesia, in terms of NGOs, the public sector is widely discussed, instead of NPOs. Hence, NPOs have been standing in the confusing position. However, the study of accounting is, as it were, decentered. As a result, the suggested way to understand accounting practice includes accounting systems, is through an understanding of the organizational reality which is the context of accounting, and which is the

3

reality that the accounting systems are designed to account for (Roberts and Scapens, 1985, p.444). Regarding the organizational reality, the Global Journal, an online media with headquarter in Geneva, Switzerland focuses on social and developmental issues, had published The Top 100 NGOs 2013 from 450 selected NGOs in the world. They employed a questionnaire approach to evaluatingtwo aims: how NGOs demonstrate accountability and transparency and also how they tease out information linked to what the journal term their “pillars of interest” which are an impact, innovation, and governance. Yayasan Cinta Anak Bangsa (YCAB Foundation) was the only one NGO from Indonesia which listed as one of 100 Top NGOs in the world, at number 74. The 1st position is BRAC (Bangladesh), while the 100th is Akilah Institute for Women (Rwanda). This fact notes that only one Indonesia NGO meets the accountability requirements. The rest of NGOs needs assistance to deal with this issue.

Besides the ranking report, two main types of research on Indonesian’s NPOs, in general, have been conducted in the last few years: World Bank research in 2010 and Department of Foreign Affairs and Trade (DFAT), Government of Australia in 2014-2015. World Bank research stated that one of the main problems in NPO is accountability and transparent. It has been argued that NPOs have initiated to develop self-regulation method in the form of a code of ethics of NPO sector. The development of the code of ethics is to enhance the accountability and transparency of the NPO itself. However, the effort on the development of the code of ethics has experienced stagnation in the last couple of years. In additional, the study has also found misleading perception in society that accountability and transparency are only needed for the report to the donors or only valid for large-funded NPOs. A large NPO reveals its perception that accountability and transparency have not been an important issue for small NPOs. Besides, only relatively large NPOs that have been able to publish the audited financial statements through websites, and other mass media as an effort to increase accountability and response to Law Number 14 the year 2008 about the Openness of Public Information. The research mentioned in the discussion with Indonesian Financial Transaction Reports and Analysis Center/INTRAC. In order to improve NPOs, the first supervision is to apply the principle of good governance, namely transparency, and accountability of NPOs.

Besides World Bank research, DFAT also researched about NPOs in Indonesia. DFAT’s field research covered the theme of NGO accountability and governance structures and processes. The

4

study concluded that accountability toward beneficiaries and the public is uneven. According to the survey of NGOs conducted for the NSSC (NGO Service and Study Centre) design. Almost all local and national NGOs reported having a mechanism or way to collect information on progress and outcomes, but only a third of local NGOs and less than half of national NGOs use the information to support their advocacy work, and less than two-thirds use the information to improve organizations and to develop annual program planning. NGO personnel themselves identify lack of clear measurement to evaluate progress and impacts as a weakness. National NGOs shared their financial report and outcomes more often to the public than sub-national organizations. Of the NGOs that conducted audits, national NGOs were much more likely to report doing so for intrinsic rather than donor-driven reasons than the few sub-national NGOs that did so. Sub-national NGOs were much more likely to do so because donors required it. While audits are not an ideal way to gauge transparency or accountability because they are expensive and they are unlikely to be appropriate for organizations operating on tiny budgets. However, hard data on different proxies for accountability is notoriously difficult to find. Moreover, it has been argued that legal status is not a workable indicator of accountability in the Indonesian context. According to the NGO Sector Review, the registration system is rarely if ever enforced and has little effect on organizations’ operations (though there are more recent reports of the UU Ormas law governing community organizations being used to limit organizations’ ability to put pressure or conduct activities with the government.). According to a 2009 survey and in the field surveys conducted as part of the 2012NGO Sector review, even though a majority of NGOs had ‘registered with the notary public, many never finalized their registration with the relevant government bodies.'

Another research on NGOs in Indonesia is conducted by Antlov, Ibrahim, and Tuijl. The research summarized that one of NGO weaknesses is a lack of accountability (Anlov et al., 2005, p.10).The study found that in 2002, LP3ES (the Agency for Research, Education, Economic and Social Development) a national NGO, has taken the initiative to prepare a code of ethics and to establish an NGO association or umbrella organization, particularly for NGOs that are working in community-based social and economic development. However, there is no further information of accomplishment about this initiative. The code contains matters related to integrity, accountability and transparency, independence, anti-violence, gender equality, and financial management, including accountability to external parties such as beneficiaries, government, donors, other NGOs

5

and the public at large. One of four points in the code of ethics that may be considered important to improve NGOs’ accountability and transparency as non-profit organizations is about utilizing bookkeeping and financial systems that are in accordance with. The financial reporting needs the basic foundation to manage a bookkeeping. In Indonesia, the only accounting standard for NPOs is PSAK 45 (Pernyataan Standar Akuntansi Keuangan 45) which is Statement of Financial Accounting Standards about financial statement reporting of NPOs.

Regarding accounting systems and accountability, Ijiri (1983, p.75) explained that in an accountability-based framework, the objective of accounting is to provide a fair system of information flow between the accountor (the supplier of accounting information) and the accountee(the recipient of accounting information). It has been said that accounting is, in fact, like a diary you keep for someone else’s use. This situation does not mean that the diary you keep for others is not useful for yourself. Nor does it imply that you may not benefit indirectly from keeping it for others. Accounting is not just for the recipient of accounting information, nor just for the supplier. The point is that existing accounting systems would just not make any sense at all if they were to be treated like a diary you keep for yourself. The accounting system can be highly useful to the supplier and the recipient even if no one reads the accounting reports. If thesupplier behaves more accountable and the recipient increases the trust onthe supplier because of the existence of records and reports, that benefit ofthe accounting system is of fundamental importance even if neither party reads the records or reports (Ijiri, 1983, p.78).In the accountability-based framework, the stability of the accounting system is often of crucial importance. If an accounting system is unstable, the supplier and the recipient sense the risk of relying upon it in developing their agreement and look for other means that are more stable (Ijiri, 1983, p.79).

The aforementioned background has shown that NPOs in Indonesia have significantly increased, but at the same time, they have been facing many obstacles. Financial reporting is one of the essential impediments. This issue has been leading them to another challenge, which is accountability and transparency. While several types of research have been engaged in dealing with the matter, the root problem of financial reporting issue is not noticeably solved. An implicit concern of accounting research focuses rather narrowly on particular elements of accounting systems, but there is no framework within which to integrate an understanding of the technical and

6

actual practice of accounting systems (Roberts and Scapens, 1985, p.443). Therefore, this research gap has been urging to initiate a study about accounting systems for NPOs in Indonesia which is supposed to view NPOs with broader infrastructure needs and analysis the necessity of accounting systems in fundamental point of view.

1.2 Objectives

The main objective of the research is to thoroughly explore the accounting system for NPOs in Indonesia and fulfill the research gaps between the need of financial reporting and the challenge of accountability and transparency. Following this objective, the research attempts:

1. to view the facts of NPOs in Indonesia,

2. to understand two basic frameworks in the financial reporting: the financial accounting standards and the accounting basis,

3. to provide a general accounting system model as a benchmark,

4. to propose an NPO accountability system as a point of reference.

1.3 Research Questions

1. How is the nature of NPOs in Indonesia?

2. Is the PSAK 45 sufficient in the purpose of NPOs’ financial reporting? 3. Is the accrual accounting the best basis for NPOs in Indonesia?

4. What kind of improvement should be proposed for NPOs’ accounting systems design?

5. What are the NPO’s needs to develop adequate non-profit accountability systems?

1.4 Research Significances

It has been developed important significances of the current research, as follow:

1. Theoretical significances

• Critiques on the PSAK 45 are supposed to be considered inputs for the Institute of Indonesia Chartered Accountants as the standard setter in Indonesia to make improvements and reform the standard in order to assist NPOs a better foundation in the financial reporting.

• The proposed general accounting systems and NPO accountability systems are supposed

7

• In broad-spectrum, findings of the study are supposed to be a contribution to the theory of accounting systems specifically and generally in the theory of accounting and NPOs’ literature.

2. Practical Significances

• For NPOs in Indonesia, the proposed general accounting systems and NPO accountability

systems are supposed to be a groundwork model for NPOs to equip their organizational infrastructure through building their own systems in order to present adequate financial reports and achieve the organizational accountability.

• For Indonesian Government, the proposed systems are supposed to be notable academic

aids to set related regulations for NPOs to provide a better service and monitoring for NPOs’ enhancements.

• In general, findings of the study are supposed to be a practical guidance for NPOs to overcome challenges and issues in their day-by-day transactions and activities, especially for workforces who do not have an accounting background and have lacks of accounting skills.

1.5 Research Methodology

This study has employed qualitative methodology under different research approaches and analyses. The main approach is the organizational ethnography. Supporting this methodology, the archival and action research are conducted.

1. Organizational ethnography research

This study is a qualitative research which has employed the organizational ethnography method. It involves the observation of, and participation in, particular groupings (Neyland, 2008, p.1). Data consists of primary and secondary data. Primary data is the result of participation in and observation of the ethnography process. Documentation study gathers secondary data such as the center financial report.

The key rationale selecting this research method can reveal NPO’s perspectives and values towards accounting basis. It may prevent information manipulation, since people may mask their weaknesses and exaggerate their strengths. Most people in all sites of NPO do not understand the terminologies in an accounting context, but they can understand what supposed to do with those.

8

The research relies on participation and observation, to answer questions about how NPOs operate. Participation took place through participating in office interaction, following their daily conversation about processes and issues in bookkeeping. The observation was achieved through reviewing NPOs’ archives, especially financial report and meeting notes.

The organizational ethnography research was conducted two times: 12 – 25 February 2015 and 23 December 2015 – 13 January 2016. There was a focus group discussion to confirm the research findings on 10 - 14 October 2016. The research on 12 – 25 February 2015 was arranged during work hour (08.00 – 17.00 WIB), according to the following schedule:

Date Name of CDC Participation as

12 February Agape Internal Auditor

13 February Efrata Treasurer

14 February Andreas Secretary

16 February Eklesia Mentor

16 February Maranatha Mentor

17 February Immanuel Treasurer

17 February Samuel Treasurer

18 February Yohanes Secretary

18 February Musa Secretary

19 February Yosua Treasurer

20 February Nehemia Secretary

21 February Daniel Treasurer

23 February Victory Secretary

24 February Eben Haezer Internal Auditor

25 February Anugerah Mentor

2. Archival research

The archival research embraces the sources used to generate research based on historical documents, texts, journal articles, corporate annual reports, company disclosures, and so on (Smith, 2015, p.160). Sources can usually be classified as primary, secondary, and tertiary. Primary sources are original research results published for the first time. Information that has been disclosed by third parties, like that in corporate reports and the press release is categorized as secondary sources. The last source is tertiary. It is for data which has been aggregated, categorized and/or reworked in databases.

9

In the current research, sources are mainly secondary, which are financial accounting standards, NPOs’ financial statements, NPO’s case study documents, such as financial reports, transaction documents and meeting notes.

3. Action research

The action research is highly related to participant observation approach where the researchers interact with the members of the organization in a collaborative venture (Smith, 2015, p.148). The participant is usually active on both sides and is more than either a consultancy project or an in-organization problem-solving exercise. The research is guided by theory in examining the change process, allowing the anticipation of consequences and outcomes. The process should have external validity in that it should produce.

1.6 Scope

While a variety of the term NPOs have been suggested, this study will keep using the term NPOs. Throughout this dissertation, NPOs have narrow characteristics as follow:

1. Legal organizations, especially foundation (Yayasan) and a parent NPO that has multisite-operation offices

2. Private/Non-government based organizations

3. Not-profitable purposed organizations

4. Non-political party

5. Absence of defined ownership interests

1.7 Research Structure

The research consists of seven chapters, as follow:

Chapter Title

1 Introduction

2 Introducing Non-profit Organizations in Indonesia

3 Criticizing Accounting Standards for Non-profit Organizations in Indonesia

4 Analyzing Applied Accounting Basis for Non-profit Organizations in Indonesia

10

6 Developing Accountability Systems for Non-profit Organizations in Indonesia

7 Conclusion

Chapter 1 highlights the introductory information of the research. It includes the background, the research gap, the problems, the objectives, the research questions, the significances for theory and practice, the research methodology, the scope, and the structure of the dissertation contents.

Chapter 2 introduces NPOs in Indonesia in general. It explains the background of the chapter, several definitions and characteristics of NPOs, categories of NPOs, overview of NPOs in Indonesia, and discussions about non-profit organizational behavior. The general description explains about several definitions and characteristics of NPO, also categories of NPOs. Overview of NPOs in Indonesia illustrates the history, the growth, research about NPOs’ challenges. In non-profit organizational behavior part, it gives details how NPOs manage their organization generally and how far NPOs in Indonesia perform.

Chapter 3 criticizes accounting standards for NPOs in Indonesia. It portrays two statements of PSAK 45 and SFAS 117, a comparison among them, and sufficiency evaluation of PSAK 45 in terms of its application on NPOs in Indonesia. Before comparing two standards, the sub chapter of Indonesia Financial Accounting Standards explains the detail of PSAK 45. PSAK 45 referred to American accounting standards. The next sub chapter overviews the detail of SFAC 4, SFAS 116, and SFAS 117.

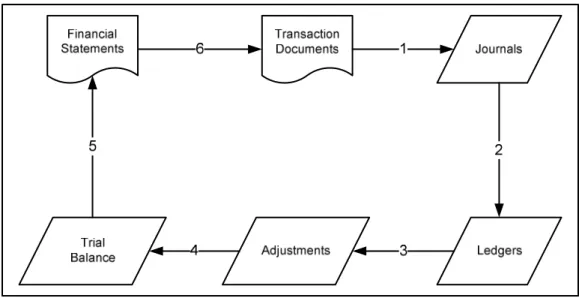

Chapter 4 analyses the applied accounting basis in NPOs. It gives an overview of general accounting basis in accounting systems. Then, it discusses the applied accounting basis in the chosen NPO. It describes the flow of transactions and transaction records in journals and ledgers, based on the principle of accounting basis.

Chapter 5 reviews the non-profit accounting system design. It pictures the accounting system design in CDCs by Data Flow Diagram (DFD) documentation technique and proposes an accounting system, includes a general model of transaction cycles and a budget-based-transaction accounting cycle. Portraying the transaction cycles followed a system presentation by Romney and Steinbart.

Chapter 6 develops the NPO accountability systems. It proposes an NPO accountability system in CDCs which is based on four accountabilities by Ebrahim. It explains the detail of the accountability to whom, the accountability for what, and the accountability how.

11

Chapter 7 contains a summary of the research. It concludes the study based on the findings and the results, also proposes recommendations for further study based on the research limitations.

There are five main studies which related each other and their mind mapping is described as follows:

12

Chapter 2 Introducing Non-Profit Organizations in Indonesia

2.1 Background

Non-profit Organizations (NPOs) throughout the world provide important roles anda variety of service and humanitarian functions. Since the mid-1970s, this sector in both developed and developing countries has significantly grown. However, to generalize about what NPOs are, what they do, and how they do it is not easy and simple. They differ vastly in scope and scale, ranging from informal organizations with no assets and no employees through multibillion-dollar foundations and other forms of organizations complexes with thousands of employees or members. Sources of revenue diverge. Many NPOs are supported by donations, others depend on income from sales of goods and services, and some receive their revenues from government.

Because of the complexity and diversity of NPOs, the term non-profit itself has a variety of meanings. Several researchers distinguished NPOs and Non-Governmental Organizations (NGOs). Hence, it is necessary here to exactly clarify what is meant by NPOs. Several organizations employ different terms of NPOs. The United Nations (UN) makes use of Non-Profit Institutions, while Financial Accounting Standards Board (FASB) applies Nonbusiness Organizations. Other organizations such as Department of Foreign Affairs and Trade (DFAT) of Australian Government and World Bank use Non-Governmental Organizations (NGOs). Less of literature mentioned NPOs as Non-profit Corporations. In Indonesia, NPOs are known as Lembaga Swadaya

Masyarakat (LSM) which means “self-reliant community development institutions.”

Besides, NPOs in every country in the world have their specific characteristics. It is because of every country has different nature and history of NPOs. For example, in United States of America organizations such as charitable, educational, and religious organizations were founded in the colonial era. In fact, over 90 percent of NPOs in the USA currently in existence were established since 1950. However, the concept of NPOs was mentioned as a unified and coherent sector dates back only to the 1970s.

For this reason, nonprofits pose particular difficulties for scholars trying to explain their history. At best, in trying to understand the history of nonprofits, it is important to identify the various ideas and institutions that make up today’s Indonesian nonprofits domain and show how

13

they have evolved over time. Since NPOs in Indonesia also have a long history and background, and before discussing NPOs’ infrastructure in the following chapter, it is necessary to understand how the nature of NPOs in Indonesia is.

The discussion of this chapter follows the following mind-mapping.

2.2 Non-Profit Organizations: Definition and Characteristics

(a) Ikatan Akuntan Indonesia/IAI (Institute of Indonesia Chartered Accountants)

IAI stated NPO as a non-profit entity which has the following characteristics (2011, p. 45.2):

1. Entity’s resources are from resource givers who do not expect an equal amount of return or

economic benefit as they gave.

2. The entity provides goods and/or services with no purpose to generate profit. Even if they have profit, it will not be shared with founders or owners of the entity.

3. There is ownership such in profit organizations, which means ownership in the entity cannot

be sold, transferred, redeemed, or it does not represent shared proportion of resources when it is in liquidation or dissolution.

(b) United Nation

According to the1993 System of National Accounts (SNA) in the Handbook of National Accounting, UN defines NPOs as (United Nations, 2003, p. 12):

14

Legal or social entities created for the purpose of producing goods and services whose status does not permit them to be a source of income, profit, or other financial gain for the units that establish, control or finance them.

Table 2.1 Comparison Two NPO Satellite Account Definitions

Structural-Operational Definition (United Nations, 2003, p. 16) Working Definition (United Nations, 2003, p. 18) 1. Organizations 2. Private 3. Non-profit distributing 4. Self-governing 5. Voluntary 1. Organizations

2. Not-for-profit and non-profit distributing

3. Institutionally separate from government

4. Self-governing

5. Non-compulsory

The term NPOs encompasses structural-operational and working. Structural-operational definition follows the basic SNA definition quite closely. On the other hand, working definition clarifies some ambiguities of SNA definition in practice. The satellite accounts on NPOs are explained in Table 2.1 above.

(c) Financial Accounting Standards Board

FASB uses the term Nonbusiness Organizations in the Statement of Financial Accounting Concepts No. 4(FASB, 1980, p 11) to refer to:

Organizations that have predominantly nonbusiness characteristics that heavily influence the operations of the organizations.

Non-Profit Organizations have three major distinguishing characteristics which include (FASB, 1980, p 11):

1. The organizations receive significant amounts of resources from resource providers who do

not expect to receive either repayment or economic benefits proportionate to resources provided

2. The organizations operates for purposes that are other than to provide goods or services at a profit or profit equivalent

15

3. The organizations have an absence of defined ownership interests that canbe sold, transferred, or redeemed, or that convey entitlement to a share of a residual distribution of resources in the event of liquidation of the organization

(d) Department of Foreign Affairs and Trade of Australian Government

DFAT explains NPOs are part of civil society. Civil society refers to a wide and growing range of non-government and non-market organizations through which people organize themselves to pursue shared interests or values in the public domain (DFAT, 2015, p. 4). NPOs membership in civil society organizations is voluntary, while NPOs themselves are self-governing with any profits turned back into the organization rather than intothe hands of private individuals (Scanlon and Alawiyah, 2014, p. iv).

(e) World Bank

World Bank defines NPOs as (2006, p. 1754):

Private organizations that pursue activities to relieve the suffering, promote the interests of the poor, protect the environment, provide basic social services, or undertake community development.

The term “ NPOs” is thus very broad and encompasses many different types of organizations. It would, therefore, include NGOs, Voluntary Agencies, charitable trusts and institutions and any such organizations that do not distribute profits for their activities.

(f) Definition Compilation from Researchers

Several researchers and authors have a different point of views about NPOs. Hansmann (Jegers, 2008, p.7) was using the term ‘NPOs’ to refer to particular an organization whose founders are not entitled to the organization’s profit (non-distribution constraint). For Oleck (1956, p. 1-2), non-profit is related to a compound of many motives. In NPOs, the motive is the test. When ethical, moral, or social motives are the dominant ones in an enterprise, that enterprise is non-profit. If an enterprise is to be viewed as non-profit, it is not enough that it merely subordinate the profit motive. It must eliminateprofit-making from its basic purposes. Therefore, Non-Profit Organizations mean a corporation organized for a purpose not involving pecuniary profit or gain to its shareholders or members, and not paying dividends or other pecuniary remuneration to its shareholders or members, provided that corporation may pay reasonable compensation or salaries

16

for services rendered. Also, Non-Profit Organizations are classified as a corporation, no part of the income of which is distributable to its members, directors, or officers.

Keating and Frumkin (Singh and Mirchandani, 2006, p. 1754) explained the fundamental features of NPOs are: (1) they exist to fulfill a charitable purpose, (2) they function without the use of coercion, (3) they operate without distributing profits to stakeholders, and (4) they exist without simple and clear lines of ownership and accountability. Worth (2012, p. 55) identified six characteristics of NPOs: (1) organized entities, (2) private, (3) non-profit distributing, (4) self-governing, (5) voluntary, and (6) of public benefit.

In Indonesia, NPOs are a part of Civil Society Organizations (CSOs). NPO encompasses not-government based organizations and not-profitable purposed organizations (Bastian, 2007, p.10).

2.3 Categories of NPOs

2.3.1 International Classification of Non-Profit Organizations (ICNPO) Table 2.2. ICNPO: groups and subgroups

Groups Subgroups

1. Culture and recreation 1 100 Culture and arts

1 200 Sports

1 300 Other recreation and social clubs

2. Education and research 2 100 Primary and secondary education

2 200 Higher education 2 300 Other education 2 400 Research

3. Health 3 100 Hospitals and rehabilitation

3 200 Nursing homes

3 300 Mental health and crisis intervention 3 400 Other health services

4. Social services 4 100 Social services

4 200 Emergency and relief

4 300 Income support and maintenance

17

5 200 Animal protection

6. Development and housing 6 100 Economic, social and community development

6 200 Housing

6 300 Employment and training

7. Law, advocacy, and politics 7 100 Civic and advocacy organizations

7 200 Law and legal services 7 300 Political organizations 8. Philanthropic intermediaries and

voluntarism promotion

8 100 Grant-making Foundations

8 200 Other philanthropic intermediaries and voluntarism promotion

9. International 9 100 International activities

10. Religion 10 100 Religious congregations and associations

11. Business and professional associations, unions

11 100 Business associations 11 200 Professional associations 11 300 Labour unions

12. Not elsewhere classified 12 100 Not elsewhere classified

Source: United Nations, 2003

2.3.2 Indonesian Classification of Non-Profit Organizations

In Indonesia, NPOs are part of CSOs. The right to freedom of opinion and assemble in Indonesia is protected by the Constitution as stated in the Article 28 of the 1945 Constitution of the Republic of Indonesia. There are three laws regulating the legal status of NPO, (1) the Law No.16 of 2001 regarding Yayasan (Foundations) and the Law No.28 of 2004 regarding the amendment of Law No.16 of 2001, (2) Staatblad 1870 regarding Perkumpulan (Associations), and (3) the Law the Law No.8 of 1985 regarding Social Organization. Comprehensively there are 15 laws, 4 Government Regulation, and seven ministerial decrees related to NPO.

Law No. 17 of 2013 regarding Organisasi Kemasyarakatan (Societal Organizations) regulates civil society organizations in general. The Law provides that there are two types of CSOs, namely (1) the ones with a legal entity, which consist of Foundations and Associations; and (2) societal organizations without legal entity status. The implication of the law is a procedure a procedure of

18

registration divided into three steps which are basically can be divided into two steps only. The first step is a requirement to achieve a legal status from the Minister of Law and Human Right. The next step is to register to the Minister of Home Affairs to obtain Registered Letter (Surat

Keterangan Terdaftar or SKT). The last step is to register to the relevant ministries. For instance,

if an NPO runs social services, the registration is filed with the Ministry of Social Affairs. If an NPO focuses on religion, the registration is filed with the Ministry of Religious Affairs, and so on. The function of supervision is under each of the ministries. For instance, religious-type NPO issupervised by the Ministry of Religious Affairs; a social-service NPO is supervised by the Ministry of Social Affairs, labor union NPO is supervised by the Ministry of Manpower and Transmigration, and so on.

Therefore, there are three primary forms of NPOs in Indonesia: 1. Yayasan (Foundations)

Foundations are regulated by Law No. 16 of 2001, as amended by Law No. 28 of 2004 (Law on Foundation). A foundationis defined as a non-membership legal entity, established based on the separation of assets, and intended as a vehicle for attaining certain purposes in the social, religious, or humanitarian fields. The law stipulates that the organizational structure of a foundation must consist of three bodies: Badan Pembina (the Governing Board), Badan

Pengawas (Supervisory Board), and Badan Pengurus (Executive Board).

There are three types of such foundations:

a. foreign foundations

b. Indonesian foundations founded by foreign nationals or by foreign nationals together with Indonesian citizens

c. Indonesian foundations founded by a foreign legal entity 2. Perkumpulan(Associations)

Associations are governed by the Dutch Colonial Government inherited law that is still valid, namely Staatsblad 1870-64 (Dutch Colonial State Gazette) on Associations with Legal Person Status. An association is a member-based organization.

19

Societal organizations without legal entity status include any organizations set up by civil society. It is possible for an NPO generally categorized as small-scale, only operates in a limited area and does not operate in other regions.

2.4 Non-Profit Organizations in Indonesia

2.4.1 Indonesia Facts and Figures

Indonesia is located in Southeastern Asia, archipelago between the Indian Ocean and the Pacific Ocean. The country lies between latitudes 11°S and 6°N, and longitudes 95°E and 141°E. It is the largest archipelagic country in the world, extending 5,120 kilometers from east to west and 1,760 kilometers from north to south.

The Dutch began to colonize Indonesia in the early 17th century; Japan occupied the islands from 1942 to 1945. Indonesia declared its independence shortly before Japan's surrender, but it required four years of sometimes brutal fighting, intermittent negotiations, and UN mediation before the Netherlands agreed to transfer sovereignty in 1949. A period of sometimes unruly parliamentary democracy ended in 1957 when President Soekarno declared martial law and instituted "Guided Democracy." After an abortive coup in 1965 by alleged communist sympathizers, Soekarno was gradually eased from power. From 1967 until 1988, President Suharto ruled Indonesia with his "New Order" government. After rioting toppled Suharto in 1998, free and fair legislative elections took place in 1999.

Indonesia is now the world's third most populous democracy, the world's largest archipelagic country, and the world's largest Muslim-majority nation. Current issues include: alleviating poverty, improving education, preventing terrorism, consolidating democracy after four decades of authoritarianism, implementing economic and financial reforms, stemming corruption, reforming the criminal justice system, holding the military and police accountable for human rights violations, addressing climate change, and controlling infectious diseases, particularly those of global and regional importance.

After experiencing two periods of crisis, in 2015 World Bank reported that Indonesia had reached GDP of USD 861.9 billion with GDP growth of 4.8%. Recovery from the Asian Financial Crisis of 1997-98 has seen steady economic growth, a growing shift of labor from agriculture to

20

services, and solid job creation in cities. These trends have contributed to a halving of the poverty rate, from 24% in 1999 to 11.4% by early 2013. However, the rate of poverty reduction has been slowing. In 2012 and 2013, poverty declined by only 0.5 percentage points each year which is the smallest declines in the last decade. Many Indonesians who have climbed out of poverty remain just above the line. In 2013, around 28 million Indonesians lived with less than IDR 293,000 (roughly $25) a month. An additional 68 million made do with not much more. Small shocks can drive them into poverty, and indeed many families fall in and out of poverty. Based on 2010 data, over half of the poor, each year was not poor the year before. A quarter of Indonesians suffers from poverty at least once in a three-year period.

Following the economic crisis at the end of the 1990s, funded by foreign donors, a consortium consisting of 27 NPOs established the Community Recovery Program (CRP) as part of the efforts to overcome the crisis and help the poor to climb out of poverty. The civil society was very enthusiastic in responding to the program. It was reported that many local NPOs or community-based organizations (CBOs) were established in almost all regions of Indonesia. They were engaged in community development for overcoming the economic crisis (Suharko, 2003).

2.4.2 Historical Background

Civil society has been playing an important role in Indonesian NPOs’ history. However, it did not run smoothly, especially when laws were enforced to limit the right to associate during the New Order era from 1965 until 1998. Under the brutal transition to the New Order regime under President Soeharto, the state limited CSOs’ political expression and engagement. The regime saw CSOs as in opposition to the state and co-opted or repressed them including a number of regulations that aimed to minimize their influence. Into the 1970s, globally and in Indonesia CSOs were limited in number and mainly charity or relief-focused. In the mid-1950s, three prominent International Non-Governmental Organizations(INGOs), the Asia Foundation, the Ford Foundation and Oxfam began working in Indonesia by providing direct service to communities, scholarships for Indonesian students to study abroad, or expert advice to government mostly at the time and into the 1970s. By the mid-1980s, due to the advancement of the role of civil society in transitions todemocracy, international donor agencies and INGOs funded and supported for Indonesian CSOs. At the end of the 1990s, the transition to democracy led to a proliferation of and expansion in the diversity of CSOs. The start of decentralization furthered this proliferationin the

21

early 2000s. Decentralization rose to a new generation of CSOs with a local focus on governance and public service. This process built up to 2014’s Village Law (No.6 of 2014), which resulted in a higher development budget for thousands of villages, with the support of civil society. Moreover, there is an area for the CSOs’ involvement assisting villages to identify needs and also manage and spend the funds.

For the last ten years, Indonesia has been considered an emerging middle-income country and has experienced economic growth since the economic crises in 1998. From 2010–2015, Indonesia's gross domestic product (GDP) growth rate was 5-6%. This increases substantial opportunities and challenges for the CSO sector. Meanwhile globally, as in Indonesia, CSOs are facing restrictions on international donor agency funding where many donors are more likely to connect their aid budget to their strategic foreign policy and trade agendas (to defend their spending for foreign aid while they are cutting their domestic spending).

Recently, while the role of civil society sector has been acknowledged and their support helped electthe current President Joko Widodo (Jokowi), the relationship between civil society and government continues to be wary. Many civil society organizations and volunteers were involved and supported President Jokowi to be elected in 2014. The election represented an important shift away from the ‘New Order’ establishment to a new generation of leaders who came from outside that power structure. As mayor of Solo and subsequently as Governor in Jakarta, Jokowi was explicitly anti-corruption. He also closely consulted with CSOs’ leaders during his presidential campaign and pre-inaugural transition period. However,many CSOs are disillusioned with Jokowi as of mid-2015 as he has made several decisions that appear to contradict commitments made during the campaign on anti-corruption and human rights issues. Additionally, the new law governing community organizations (UU Ormas, No. 17 of 2013), was passed to great concern from prominent civil society organizations. Those concerns were based on vague wording in several of the articles and the potential for the law to be used to diminish freedom of association. Muhammadiyah (Indonesia’s second largest mass-based religious organization) and the Koalisi

Kebebasan Berserikat (KKB; Coalition for the Freedom of Association, consisting of 14

prominent national CSOs) both filed separate judicial review applications to the Constitutional Court challenging dozens of articles in the law. In December 2014, the Court accepted the objections of these organizations, deciding that more than ten articles were unconstitutional,

22

including the regulation on the objectives of establishing a CSO, the regulation on boards and executives, and the regulation on memberships. The KKB has called on the government to terminate all government regulation derived from the law. The longer-term impact of the law and the Constitutional Court’s decision remain to be seen as of mid-2015. It is worth noting as an update since 2012 that the KKB also requested that the draft law for associations be prioritized for the national legislative agenda in for 2015–2019. The existing regulation for associations (Government Gazette 1870 No 64) does not align with the relatively complex structures of organizations in the modern era compared to when the regulation was enacted.

Table 2.3 Milestones History of Indonesian CSOs

Year Milestones

Mid 1950s Three prominent INGOs, the Asia Foundation, the Ford Foundation and Oxfam

began working in Indonesia

1965 – 1998 New order era: Laws limiting the right to associate

1966 Indonesia re-joined the Bretton Woods system made up of the International

Monetary Fund and World Bank

Mid 1980s International donor agencies and INGOs provided some funding and support for

Indonesian CSOs

1990s The transitionto democracy led to a proliferation of and expansion in the

diversity of CSOs

2000s The start of decentralization furthered the proliferation

2013 2013’s Community Organizations law (No 17 of 2013): Vague wording in

several of the articles and the potential for the law to be used to diminish freedom of association

2014 2014’s Village law (No 6 of 2014): Development budget for villages, with

support of civil society

2014 The Constitutional Court accepted the objections of Coalition for Freedom of

Association (Consisting 14 prominent national CSOs): 10 articles were unconstitutional

2010 – 2015 Indonesia’s GDP rate of 5-6% has led the opportunities and challenges of CSO

sector

23

Indonesia’s NPO sector has a relatively weak intermediary support infrastructure; that is, there is inadequate support available to small and local NPOs from organizations that provide strategic capacity development and assistance. This is reflective of larger global trends as well. The strength of the intermediary support infrastructure in an NPO sector is closely linked to the evolution of the civil society of which they are a part. An NPO sector that is still maturing will have fewer intermediary support organizations. Additionally, countries with traditionally strong democratic contexts such as the Philippines, Brazil, and Peru will have stronger civil society support organizations than countries with less democratic context.

2.4.3 Numbers

Research by Scanlon and Alawiyah (2014) stated that there were an estimated 2,293 active and viable NPOs throughout Indonesia as of 2012. The NPO sector overall in Indonesia had estimated revenues of AU$340 million(IDR 3,415,520,323,162) in 2013.The most important source of funding by far for national NPOs is international donor agencies or INGOs (73%). An additional 6.67% NPOs report that their most important source of funding is another national NPO, which in practice means their funding almost certainly originates from an international donor agency, albeit indirectly.

Table 2.4 Legal Form of NPOs

No Type of Legal Entity Number

(Percentage)

Type of NPO

1 Foundation 21,301 (99%) Orphanage, Tithe, Social Organization,

NGO, etc

2 Association 268 (1%) Religious community, labor/worker union,

student assembly, farmer union, etc

3 Societal Organization

(Non-legal Entity)

- Congregation group, hobby group, etc

Total 21,569

Source: World Bank, 2010

There are some stages to get formal legality from the state. An NPO has to have an Incorporation Deed from Notary. After that, the NPO should submit a request for registering its organization to the Ministry of Law and Human Rights of Indonesia and subsequently it will acquire a certification which is mentioned in the Ministerial Decision Letter Concerning Certificate of Incorporation. However, it is also stated that not all NPOs that already have

24

incorporation deed from the notary proceed to submit request registering its corporation to the Ministry. The government does not compel the registration. Therefore, the related Ministry is not able to estimate the official number of NPOs in Indonesia. Research by World Banking 2010 reported that the sum of NPOs that have been registering in the Ministry is 21,569 NPOs (p. 25). The team stated that it is difficult to acquire an accurate number of NPOs because the data set management system is carried out separately and not integrated. Because of NPOs that are legal entities (normally foundation or Yayasan) need to report their existence to the authorities, so it is impossible to estimate the exact number of NPOs in Indonesia (Antlov et al., 2005, p.2).

There are 131 foreign NPOs listed in the Ministry of Foreign Affairs. However, it is presumably a large amount of unlisted foreign NPOs conducting activities in Indonesia. Supervision and partnership with foreign NPO still is required to be developed as an effort to develop accountability and transparency,as well as increasing the reward to the supremacy and independency of the Indonesia Society (World Bank, 2010, p.7).

Table 2.5 NPOs based on ICNPO

No ICNPO’s group Number

1 Culture and Art 1

2 Education and Research 83

3 Health 10

4 Social Service 32,474

5 Environment 34

6 Community Development 131

7 Law, Advocacy, and Politic 60

8 Philanthropy and Voluntarism 4

9 Gender and Development 24

10 Religious Affairs 5

11 Profession Association 278

12 Faith in God Almighty 8

Total 33,112