Pr

ef

ace

About50 yearsago,the Japanese governmentadopted a“universalhealth insurance”system Public

health insurance transformed comprehensive and universalcompulsory health insurance forallresidents,

regardlessofoccupation,age,sex,and area.Nevertheless,more “uninsured”are emerging in the 21st

century.However,the Japanese government’spublicstance isthatthere can be no uninsured in Japan,and

more employeesare facing accessibility problemsforemployment-based health insurance by diversification

ofwork arrangementsand increasing mobility ofemployment.More insured people face problemsof

insurance premium affordability.

The presentstudy discusseshow the publichealth insurance system worksassafety netin Japan,

based on the characteristicsofthe publichealth insurance system.

Ⅰ.

Char

act

er

i

st

i

cs

of

Japan’

s

publ

i

c

heal

t

h

i

nsur

ance

syst

em

1.Universalhealth insurance using a socialinsurance schemeUniversalcompulsory publichealth insurance forallisadistinctive feature ofJapan’s“welfare state.”

I

s

t

he

saf

et

y

net

f

or

heal

t

hcar

e

i

n

J

apan

f

r

ayi

ng?

:

Empl

oyment

,

heal

t

h

i

nsur

ance,

and

publ

i

c

assi

st

ance

HASEGAWA

Chi

ha

r

u

ⅰAbstract:Thisstudy discusseshow the publichealth insurance system worksasasafety netin Japan,

based on the characteristicsofthe publichealth insurance system.Japan’suniversalhealth insurance

system isoperated using asocialinsurance scheme.The twin pillarsofthissystem are employment

-based health insurance (Kyokai-kempo,Kumiai-kempo,and Kyosai)and area-based health insurance

(NationalHealth Insurance and the medicalcare system forthe latter-stage elderly).However,unstable

employmentand persistentunemploymentcould increase the numberofemployeeswithoutemployment

-based health insurance (most are non-regular workers). Those who cannot participate in public

employment-based health insurance could find alternative publichealth insurance,namely,National

Health Insurance,asasafety net.However,more NHIinsured lose theirpremium payments,because

the ratio ofpremiumsto income isrising and the burden isexcessive forlow-income earners.The state

needsto improve accessibility foremployment-based health insurance,and improve affordability for

NationalHealth Insurance.

Keywords : Universalhealth insurance system,Employment-based health insurance,NationalHealth

Insurance,Non-regular(non-traditional)employee,Uninsured,Accessibility,Affordability

Thisuniversalhealth insurance system isoperated using asocialinsurance scheme.The twin pillarsof

Japan’suniversalhealth insurance system are employment-based health insurance and area-based health

insurance.

The history ofthe health insurance system (intended forblue-collarworkers)datesfrom 1922.The

NationalHealth Insurance Act(intended forfarmers)wasenacted in 1938,butmunicipalitieswere not

required to setup the foundationsofNationalHealth Insurance (NHI).By amending the NationalHealth

Insurance Actin 1958,the Japanese governmenthasextended coverage ofNHIto allJapanese people,

eliminating only those who are covered by employment-based health insurance,to be managed by local

governments,thereby realizing universalhealth insurance coverage (exceptforwelfare recipients).

From the startofthe universalhealth insurance system,the nationalgovernmenthasprovided

subsidiesand contributionsto ensure thatNHIfinancesremain healthy.

2.Distinctive features ofJapan’s health insurance systems

The Japanese universalhealth insurance system hasthree characteristics.First,itisclassified into

employment-based health insurance and area-based health insurance.Second,multiple insurersoperate

independently.Third,the type ofpublicinsurance coverdependson employmentpatternsand age.

Dependentfamiliesare covered by the insurance thatappliesto the household head.

With regard to the characteristicsofthe insured groups’contributions,the majority ofpeople (about

60%)are enrolled in employment-based health insurance (Figure 1).

Japan hasthree primary employment-based health insurance programs:health insurance administered

by the Japan Health Insurance Association (JHIA)(Kyokai-kempo,agovernmentagency established in

Figure1:Composition ratio ofpublic health insurances in Japan,2013

October2008)foremployeesofsmalland medium-sized enterprises;asociety-managed,employment-based

health insurance (Kumiai-kempo,employee health insurance managementsocietiesestablished by alarge

company orgroup ofcompanies)foremployeesoflarge enterprises;and health insurance managed by a

mutualaid association (Kyosai)fornationaland localpublicofficialsand private schoolstaff.Employees’

family membersare able to receive employment-based health insurance asnon-working dependents.

There were 1,443 insurersofKumiai-kempoatthe end ofMarch 2012,and 1 insurerofKyokai-kempo

(47 branchesin each prefecture).Ifcompaniesdo notestablish societies,employeesare enrolled in JHI

A-administered health insurance.Thus,JHIA-administered health insurance actsasthe safety netin Japan’s

employment-based health insurance.

Every individualbelow the age of75 yearswho cannotjoin one ofthese employment-based health

insurance programssubscribesto the area-based health insurance (NHImanaged by localgovernments).

Specifically,farmers,the self-employed,non-workers(e.g.,pensioners),and employeesand theirfamiliesnot

covered by employment-based health insurance are enrolled in NHI.There are 1,717 insurers,the same

numberasthe numberofmunicipalitiesin Japan.

A medicalcare system forthose aged 75 yearsand overhasbeen operating since April2008.The

insurerhasextended associationsforlatter-stage elderly health insurance in each prefecture.

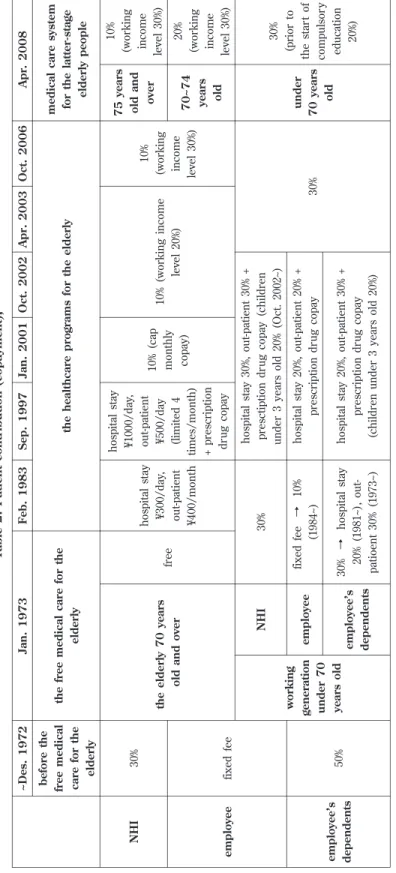

3.Health insurance benefits and patientcontribution (copayment)

Multiple publichealth insurance associationsshare common health insurance benefitpayments(Table

1).Health insurance benefitpaymentsare classified into healthcare payments(in-kind benefits)and cash

payments.When insured patientsvisitmedicalservice providersunderNHI,they pay 30% oftheirmedical

costsforservices.Through the claimsofthese providers,NHIpaysthe remaining 70% ofthe medicalcosts

to providers.However,health insurance paymentsvary by age bracketasfollows:up to primary school

entry (80%),those aged 70–74 years(80%),those aged 75 yearsand over(90%),and those whose taxable

income ismore than the average taxable income ofthe workforce of1,450,000 yen peryearsince April2008

(70%).

Historically,patientpaymentshave been 30% ofmedicalcostsforNHIinsured,with fixed feesfor

employeesenrolled in employment-based health insurance,and 50% ofmedicalcostsforemployees’

dependentsuntil1972 (Table 2).By welfare reform in 1973 (the firstyearofwelfare),free medicalcare for

the elderly started.However,thisended after10 years,and afixed fee forthe elderly wasadopted (hospital

stay:300 yen/day;outpatient:400 yen/month).In 1997,thatfee wasincreased (hospitalstay:1,000 yen/day;

outpatient:500yen/day,fourtimesamonth + prescription drug copayment).In 2001,the patientcopayment

forthe elderly waschanged to 10% ofmedicalcost,and 1 yearlater,the copaymentforthe elderly whose

income wasthatofworking income levelwasincreased to 20% ofmedicalcost.In 2006,thisincreased to

30%).Since 2008,the patientcopaymentforthose aged 70–74 yearshasbeen 20% ofmedicalcost,and that

forthose aged 75 yearsand overhasbeen 10%.

In 1973,ahigh-costmedicalcare expense program,with individuallimits,wasintroduced,and the

patientcopaymentforthe working generation underthe age of70 yearswasreduced (10% foremployees

enrolled in occupationalhealth insurance,and 30% foremployees’family members).In 2003,the patient

copaymentforthe working generation was30% ofmedicalcostacrossthe board.

There are fourcategoriesofcash payments:lump-sum allowancesforchildbirth;lump-sum allowances

forburialcosts;invalid benefits;and maternity allowances.Invalid benefitsand maternity allowancesare

S o u rc e : Mi n is tr y o f He al th , L ab o u r, a n d We lf ar e , A n o u tl in e of t h e Ja p a n es e Me d ic a l S ys te m ( E n g li sh ) < h tt p :/ / w w w .mh lw .g o .j p / b u n y a/ ir y o u h o k e n / ir y o u h o k e n 0 1 / d l/ 0 1 _ e n g .p d f> . A cc es se d 2 01 5 Ja n 6 . T a b le 1 : He a lt h i n su ra n c e b e n e fi ts ( h e a lt h c a re p a yme n t a n d c a sh p a yme n t)

T a b le 2 : P a ti e n t c o n tr ib u ti o n ( c o p a yme n t) , A p r. 2 0 0 8 Oc t. 2 0 0 6 A p r. 2 0 0 3 Oc t. 2 0 0 2 Ja n . 2 0 0 1 S e p . 1 9 9 7 F e b . 1 9 8 3 Ja n . 1 9 7 3 ~ De s. 1 9 7 2 me d ic a l c a re s ys te m fo r th e l a tt e r-st a g e e ld e rl y p e o p le th e h e a lt h c a re p ro g ra ms f o r th e e ld e rl y th e f re e me d ic a l c a re f o r th e e ld e rl y b e fo re t h e fr e e me d ic a l c a re f o r th e e ld e rl y 10 % (w o rk in g in co me le ve l 30 % ) 7 5 y e a rs o ld a n d o ve r 10 % (w o rk in g in co me le ve l 30 % ) 10 % ( w o rk in g i n co me le ve l 20 % ) 10 % ( ca p mo n th ly co p ay ) h o sp it al s ta y ¥1 00 0/ d ay , o u t-p at ie n t ¥5 00 / d ay (l imi te d 4 ti me s/ mo n th ) + p re sc ri p ti o n d ru g c o p ay h o sp it al s ta y ¥3 00 / d ay , o u t-p at ie n t ¥4 00 / mo n th fr ee th e e ld e rl y 7 0 y e a rs o ld a n d o ve r 30 % NH I 20 % (w o rk in g in co me le ve l 30 % ) 7 0 ~ 7 4 ye a rs o ld fi x ed f ee e mp lo ye e 30 % (p ri o r to th e st ar t o f co mp u ls o ry ed u ca ti o n 20 % ) u n d e r 7 0 y e a rs o ld 30 % h o sp it al s ta y 30 % , o u t-p at ie n t 30 % + p re sc ti p ti o n d ru g c o p ay ( ch il d re n u n d er 3 y ea rs o ld 2 0% ( Oc t. 2 00 2~ ) 30 % NH I w o rk in g g e n e ra ti o n u n d e r 7 0 ye a rs o ld h o sp it al s ta y 20 % , o u t-p at ie n t 20 % + p re sc ri p ti o n d ru g c o p ay fi x ed f ee → 10 % (1 98 4~ ) e mp lo ye e 50 % e mp lo ye e ’s d e p e n d e n ts h o sp it al s ta y 20 % , o u t-p at ie n t 30 % + p re sc ri p ti o n d ru g c o p ay (c h il d re n u n d er 3 y ea rs o ld 2 0% ) 30 % → h o sp it al s ta y 20 % ( 19 81 ~) , o u t-p at io en t 30 % ( 19 73 ~) e mp lo ye e ’s d e p e n d e n ts S o u rc e: Mi n is tr y o f He al th , L ab o u r, a n d We lf ar e, A n o u tl in e of t h e Ja pa n es e Me di ca l S ys te m ( E n g li sh ) <h tt p :/ / w w w .mh lw .g o .jp / b u n ya / ir yo u h o k en / ir yo u h o k en 01 / d l/ 01 _e n g .p d f> . A cc es se d 20 15 J an 6 .

employeesare enrolled in NHI,they have no economicsecurity ifthey become unable to work because of

accidentsorsicknessunrelated to theirjobs.

Ⅱ.

Funds

f

or

medi

cal

expendi

t

ur

e

1.Insurance premium and contributionEach publichealth insurerimplementsfiscalmanagementindependently.Calculation methodsfor

health insurance premiumsdifferforoccupationalinsurance,area-based insurance,and the medicalcare

system forlatter-stage elderly people.Majorsourcesofrevenue are premiums(paid by the insured and

employers), public expenditure for health benefits (state, prefectural governments, and municipal

governments),and copaymentsby patients.

In 2012FY,health insurance benefitswere about47% ofnationalhealth expenditure,health insurance

benefitsforthe latter-stage elderly were about32%,publicexpenditure forhealth benefitswasabout7%,and

copaymentsby patientswasabout13% (Figure 2).Forthe share ofnationalhealth expenditure by financial

resource, premiums were about 49%, public expenditure about 39% (state 26% and local 13%), and

copaymentsby patientsabout12%.

The calculation method ofoccupationalhealth insurance premiumsdependson the principle ofability

Figure 2:Nationalhealth expenditure (2012FY)

to pay (index monthly earning and bonus× premium rate).The average premium rate ofJHIA-managed

health insurance is10%,whereassociety-controlled insurance is8.9% (2014FY).Occupationalinsurance

premiumsconsistofthispremium and specificpremiumsforsupporting medicalcostsofthe elderly (4.07%

in the case ofthe JHIA,~March 2014).Insured employeesand theiremployersshare the costsofpremiums

50–50,and in the case ofsociety-controlled health insurance,mostemployersshouldermore burdens.

Occupationalhealth insurance isnotcalculated on the benefitprinciple and doesnotcharge family

premiums(Shimazaki2011).

Mostofthe insured enrolled in JHIA-managed health insurance are employeesofsmalland medium

enterprisesand theiraverage wagesare lowerthan those ofemployeesoflarge enterprises;thus,the JHIA

hasweak funding.Aslong ascompulsory participation preventsemployeesfrom choosing theirpreferred

occupationalhealth insurance,itisnecessary to narrow the funding gap between the JHIA and societies

(Kumiai-kempo)by state governmentsubsidy (Shimazaki2011).Therefore,the state subsidizesthe health

benefitexpenses(16.4%)forthe JHIA to controlthe growth ofthe JHIA’spremium rates.

The calculation method ofNHIpremium dependson both the principle ofability to pay and the benefit

principle.NHIpremiumsare determined by aformulabased on the insured’sability to pay (afixed

percentage oftotalhousehold income and property tax),and iscalculated foreach household according to

benefitsreceived (fixed amountpercapitaand fixed amountperhousehold).Levy calculation formulas,

premium rates,and fixed amountsdifferamong insurers.Forexample,in the case ofKyoto city,NHI

premium consistsofafixed percentage oftotalhousehold income,afixed amountpercapita,and afixed

amountperhousehold.

NHIhasweak funding because the average age ofthe insured and the levelofmedicalcare costsare

higherthan occupationalhealth insurance;moreover,the average income ofNHIinsured islower.Thus,

NHItakesnationalgovernmentsubsidiesamounting to 50% ofbenefits,afixed-rate state contribution of32%,

state adjusting subsidiesof9%,and prefecturaladjusting subsidiesof9%.The other50% ofbenefitsare

covered by premiums.To adjustthe gap ofpremium income and spending between municipalgovernments,

there are jointprojectsto strengthen the financialbasisofNHI.The state,prefectures,and municipalities

jointly take on the financialburdensofhigh-costmedicalreceiptsand low-income insured.Even so,most

NHIinsurershave fiscaldeficitsand many municipalitiestransferapartoftheirgeneralaccountexpenditure

to NHIspecialaccount.

2.Financialadjustments ofmedicalexpenditure forthe elderly

Aging population and the resulting expansion ofmedicalexpenditure are common issuesshared by

developed countries.In Japan,those who are enrolled in employment-based health insurance move to area

-based health insurance afterretirement,and so,there isuneven distribution ofthe elderly between insurers.

In particular,there are very big elderly populationsin NHImanaged by localgovernments,and NHIcovers

the financialburden of medicalexpenditure forthe elderly.To ease the burden of NHI,afinancial

adjustmentsystem isrequired formedicalexpenditure forthe elderly among allinsurers,including

occupationalhealth insurance.

By health insurance reform in 2006,the state introduced afinancialadjustmentsystem forthe earl

y-stage elderly and amedicalcare system forthe latter-stage elderly to achieve equitable sharing ofmedical

costsamong insurers,equitable premium burdensamong the elderly,and clarification ofthe ratio ofthe

premium amountsbetween aged and young generations.

insurersreceive grantsrelated to nationalaverage participation ratesofthe elderly aged 65–74 yearsto

adjustimbalance among insurersdue to the uneven distribution ofthe elderly aged 65–74 years.In fact,

insurersofemployment-based health insurance pay leviesand NHIinsurersreceive grants(Figure 3).

Underthe medicalcare system forthe latter-stage elderly,thiselderly group makesapremium

paymentequivalentto 10% ofinsurance benefitsforthe latter-stage elderly,young generationscontribute

40%,and generalpublicexpenditure makesup the remaining 50% (Figure 4).The latter-stage elderly pay a

Figure 4:Medicalcare system forthe latter-stage elderly

Source;Ministry ofHealth,Labour,and Welfare,An outlineoftheJapaneseMedicalSystem (English)<http://www.mhlw.go.

jp/bunya/iryouhoken/iryouhoken01/dl/01_eng.pdf>.Accessed 2015 Jan 6.

flatpremium rate in each prefecture,calculated asafixed percentage oftotalhousehold income and fixed

amountpercapita.

3.Gradualreduction systems ofpremium payments by low-income households

NHIand the medicalcare system forthe latter-stage elderly actassafety netsofpublichealth

insurance,and so,these comprise gradually reducing premium paymentsby low-income households.

NHIpremiumscalculated by the benefitprinciple (fixed amountpercapitaand fixed amountper

household)are discounted by 70%,50%,or20%,designated by nationallaw.Some municipalitieshave

originaldiscountsystemsin theirordinances.Ifhousehold income islessthan 330,000 yen,thathousehold

NHIpremium calculated by the benefitprinciple isdiscounted by 70%.Ifhousehold income islessthan

330,000 yen + (245,000 yen × numberofpeople perhousehold),itisdiscounted by 50%.Ifthe household’s

income islessthan 330,000 yen + (450 000 yen × numberofpeople perhousehold),itisdiscounted by 20%.

The medicalcare system forthe elderly aged 75 yearsand overhasapremium discountsystem forl

ow-income insured,whose premium paymentisonly afixed amountpercapitaand thatamountisdiscounted

gradually.In addition,aspecialreduction premium measure hasoperated since 2008.

Ⅲ.

St

r

uct

ur

al

f

act

or

s

cr

eat

i

ng

t

he

uni

nsur

ed

11.Employees withoutemployment-based health insurance

Employees(those employed by acompany with more than five employeesin aworkplace covered by

socialinsurance)and theirdependentfamiliesare enrolled mandatorily in employment-based health

insurance.However,more employees(non-regularworkers)are eliminated from applying foremployment

-based health insurance.

An “employee”isassumed by occupational

health insurance to be afull-time workerand

would have lifetime employment and a

seniority-based wage (Figure 5).A “regular

employee” is defined as a worker entering

into acontractofemploymentformore than 2

monthsorwithoutterm,and who worksmore

than three-quarters of scheduled working

hours on prescribed working days2. Thus,

short-term contract workers and part-time

workers do not apply to be employees, as

defined by employment-based health insurance,

asageneralrule.Thusnon-regularemployees

have been enrolled in NHI or employment

-based health insurance asfamily dependents.

Kurata (2004) offers two systemic reasons

why employment-based health insurance

essentially is available only to regular

employees.First,legalprovisionsdo notapply

to day workers, some contingent workers,

Figure 5:Classification between Regularemployee and Non-regularemployee

seasonalworkers,and temporary workersemployed forlessthan 6 months.Second,the pay base on which

insurance premiumsare calculated pertainsonly to regularemployees.

Figure 6 showsthe employmentcharacteristicsofJapanese workers.In 1984,84.7%,excluding board

members,were regularemployees.Thataverage percentage eased between 1994 and 2008 and declined to

63.3% in 2013.Conversely,Japan’s19.06 million non-traditionalemployeesnow comprise 36.7% ofthe

workforce.Since 1985,amendmentsto the ManpowerDispatching BusinessActand to the LaborStandard

Law have deregulated hiring practices,and the numberofnon-traditionalworkersisincreasing without

laborprotection,such asequaltreatmentwith full-time employees.

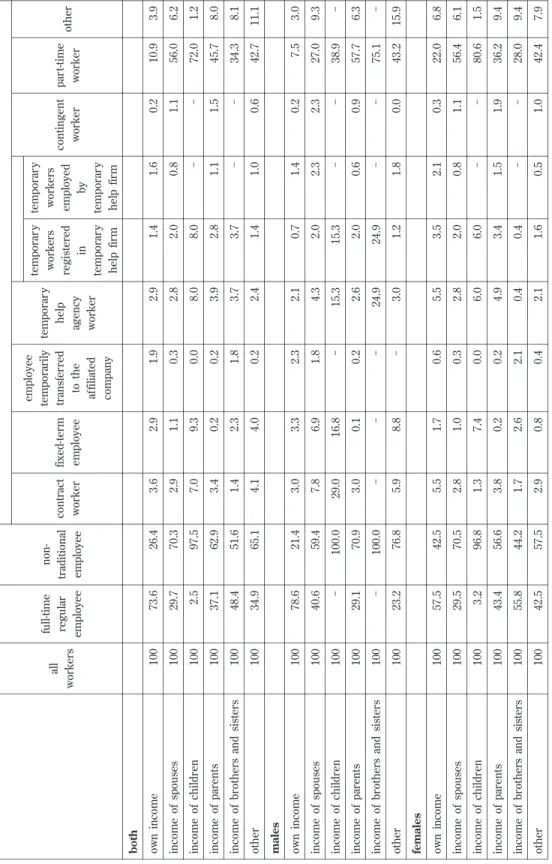

Table 3 showsthatallfull-time regularemployeeshave employment-based health insurance,butless

than half of non-traditional employees do. More specifically, about 95% of employees on temporary

assignmentapplied foremployment-based health insurance,butonly 88% ofcontractortemporary workers,

78% oftemporary help agency workers,35% ofpart-time workers,and 14% ofcontingentworkersapplied.

Temporary help agency workershave shortand intermittentemploymentagreementsand no accessto

occupationalhealth insurance from the company they are assigned to orfrom the personnelagency that

assigned them.Recognizing the growing numberoftemporary help agency workers,the Health Insurance

Society forTemporary Workers(Haken-Kempo)wasfounded in 2002 “in orderto strive forthe stability of

Figure 6:Annualchanges in the actualnumberofnon-traditionalemployees in Japan (Ten thousand persons),1985―2013

Note:“part-time”and “arbeit”are internalname,so both are part-time workers.

T a b le 3 : P e rc e n ta g e o f w o rk e rs w it h u n e mp lo yme n t, e mp lo ye e h e a lt h , a n d e mp lo ye e p e n si o n i n su ra n c e , in J a p a n , 2 0 1 0 w o me n me n T o ta l E mp lo ye e p en si o n in su ra n ce E mp lo ye e h ea lt h in su ra n ce U n emp lo y-me n t in su ra n ce E mp lo ye e p en si o n in su ra n ce E mp lo ye e h ea lt h in su ra n ce U n emp lo y-me n t in su ra n ce E mp lo ye e p en si o n in su ra n ce E mp lo ye e h ea lt h in su ra n ce U n emp lo y-me n t in su ra n ce 99 .8 % 99 .8 % 99 .8 % 99 .3 % 99 .3 % 99 .3 % 99 .5 % 99 .5 % 99 .5 % fu ll -t ime r eg u la r emp lo ye e 44 .9 46 .0 64 .7 61 .3 64 .4 66 .1 51 .0 52 .8 65 .2 n o n -t ra d it io n al e mp lo ye e 85 .8 88 .5 87 .3 85 .0 88 .6 83 .2 85 .4 88 .5 85 .1 co n tr ac t w o rk er 85 .3 87 .1 88 .6 85 .1 88 .0 82 .7 85 .2 87 .8 84 .0 te mp o ra ry w o rk er 89 .8 89 .7 90 .3 93 .0 95 .6 90 .3 92 .6 94 .9 90 .3 emp lo ye e te mp o ra ri ly t ra n sf er re d t o t h e af fi li at ed c o mp an y 74 .0 75 .3 84 .6 77 .8 81 .4 84 .7 75 .6 77 .9 84 .7 te mp o ra ry h el p a g en cy w o rk er 75 .6 77 .4 81 .5 66 .5 75 .1 79 .3 73 .0 76 .7 80 .9 te mp o ra ry w o rk er s re g is te re d i n t emp o ra ry h el p f ir m 70 .8 71 .1 90 .7 84 .1 85 .0 87 .7 78 .6 79 .3 89 .0 te mp o ra ry w o rk er s emp lo ye d b y te mp o ra ry h el p f ir m 10 .9 12 .5 10 .3 11 .2 15 .9 33 .4 11 .0 13 .5 16 .6 co n ti n g en t w o rk er 33 .2 34 .0 58 .8 35 .6 39 .1 45 .5 33 .8 35 .3 55 .3 p ar t-ti me w o rk er 67 .6 70 .2 76 .3 68 .4 69 .6 72 .2 67 .9 70 .0 74 .6 o th er S o u rc e: Mi n is tr y o f He al th , L ab o u r, a n d We lf ar e (2 01 0) .

T a b le 4 : Di st ri b u ti o n o f e mp lo ye e s’ ma in s o u rc e o f in c o me , b y w o rk s ta tu s, 2 0 1 0 n o n -tr ad it io n al emp lo ye e fu ll -t ime re g u la r emp lo ye e al l w o rk er s o th er p ar t-ti me w o rk er co n ti n g en t w o rk er te mp o ra ry h el p ag en cy w o rk er emp lo ye e te mp o ra ri ly tr an sf er re d to t h e af fi li at ed co mp an y fi x ed -t er m emp lo ye e co n tr ac t w o rk er te mp o ra ry w o rk er s emp lo ye d b y te mp o ra ry h el p f ir m te mp o ra ry w o rk er s re g is te re d in te mp o ra ry h el p f ir m b o th 3. 9 10 .9 0. 2 1. 6 1. 4 2. 9 1. 9 2. 9 3. 6 26 .4 73 .6 10 0 o w n i n co me 6. 2 56 .0 1. 1 0. 8 2. 0 2. 8 0. 3 1. 1 2. 9 70 .3 29 .7 10 0 in co me o f sp o u se s 1. 2 72 .0 ‐ ‐ 8. 0 8. 0 0. 0 9. 3 7. 0 97 .5 2. 5 10 0 in co me o f ch il d re n 8. 0 45 .7 1. 5 1. 1 2. 8 3. 9 0. 2 0. 2 3. 4 62 .9 37 .1 10 0 in co me o f p ar en ts 8. 1 34 .3 ‐ ‐ 3. 7 3. 7 1. 8 2. 3 1. 4 51 .6 48 .4 10 0 in co me o f b ro th er s an d s is te rs 11 .1 42 .7 0. 6 1. 0 1. 4 2. 4 0. 2 4. 0 4. 1 65 .1 34 .9 10 0 o th er ma le s 3. 0 7. 5 0. 2 1. 4 0. 7 2. 1 2. 3 3. 3 3. 0 21 .4 78 .6 10 0 o w n i n co me 9. 3 27 .0 2. 3 2. 3 2. 0 4. 3 1. 8 6. 9 7. 8 59 .4 40 .6 10 0 in co me o f sp o u se s ‐ 38 .9 ‐ ‐ 15 .3 15 .3 ‐ 16 .8 29 .0 10 0. 0 ‐ 10 0 in co me o f ch il d re n 6. 3 57 .7 0. 9 0. 6 2. 0 2. 6 0. 2 0. 1 3. 0 70 .9 29 .1 10 0 in co me o f p ar en ts ‐ 75 .1 ‐ ‐ 24 .9 24 .9 ‐ ‐ ‐ 10 0. 0 ‐ 10 0 in co me o f b ro th er s an d s is te rs 15 .9 43 .2 0. 0 1. 8 1. 2 3. 0 ‐ 8. 8 5. 9 76 .8 23 .2 10 0 o th er fe ma le s 6. 8 22 .0 0. 3 2. 1 3. 5 5. 5 0. 6 1. 7 5. 5 42 .5 57 .5 10 0 o w n i n co me 6. 1 56 .4 1. 1 0. 8 2. 0 2. 8 0. 3 1. 0 2. 8 70 .5 29 .5 10 0 in co me o f sp o u se s 1. 5 80 .6 ‐ ‐ 6. 0 6. 0 0. 0 7. 4 1. 3 96 .8 3. 2 10 0 in co me o f ch il d re n 9. 4 36 .2 1. 9 1. 5 3. 4 4. 9 0. 2 0. 2 3. 8 56 .6 43 .4 10 0 in co me o f p ar en ts 9. 4 28 .0 ‐ ‐ 0. 4 0. 4 2. 1 2. 6 1. 7 44 .2 55 .8 10 0 in co me o f b ro th er s an d s is te rs 7. 9 42 .4 1. 0 0. 5 1. 6 2. 1 0. 4 0. 8 2. 9 57 .5 42 .5 10 0 o th er S o u rc e: Mi n is tr y o f He al th , L ab o u r, a n d We lf ar e (2 01 0) .

life and the improvementofwelfare oftemporary employees...”Unlike Kumiai-Kempo,Haken-Kempoallows

the insured to retain coverage despite interruption in employmentifthey remain registered with the same

dispatching agency,have definitive employmentagreementsfor1 month orlonger,and startwork within 1

month aftertheirpreviousemploymentagreementsend.When switching to adifferentdispatching agency

orifthe intervalbetween assignmentsexceeds1 month,these insured are noteligible to continue coverage.

Itwould appearthatsome non-regularworkersdo notwanttheirown employment-based health

insurance because they are enrolled in theirspouses’employment-based health insurance asadependent

family member,with annualincome oflessthan 1,300,000 yen.Ifnon-regularemployeesare notthe family’s

primary breadwinner,these conditionsofemploymentmightpresentproblems.However,Table 4 showsthat

quite anumberofnon-regularworkersspecify theirown wagesastheirmain sourcesofincome.

Workersthatare noteligible foremployer-sponsored insurance can enrollin NHI,butvulnerability to

wage lossdiffersunderthese two programs.Workerswith employer-sponsored health insurance could

receive cash foratime ifthey misswork because ofillness,injury,orchildbirth.Workerswith NHIreceive

no such benefits,and they are endangered by losing allwage income through illness,injury,and childbirth.

Figure 7 showscertain characteristicsofhouseholdscovered by NHI.Among households,the percentage of

householdsin which family headsare employeeswas35.2% in 2012 compared to 23.8% in 1995.The sharp

increase isexplained by individualsaged 75 yearsand olderwho shifted from NHIto the latter-stage elderly

health care system in 2008.

2.Loss ofemployment-based health insurance through unemployment

Workerswho lose theirjobsalso lose theiremployment-based health insurance.Certain former

Figure 7:Composition rate ofhousehold with NHI,by work status offamily head,1994―2012

employees, retirees, spouses, and dependent children have the right to temporary continuation of

employment-based health insurance;ifthey have held the same employment-based coverage formore than 1

year,they can continue with itforup to 18 monthswith propernotification (voluntary continuation

program).The formeremployee mustpay the entire premium and losescoverage ifhe/she isin payment

arrearsforatleast1 month.

Workerswho do notchoose the voluntary continuation program mustnewly notify forNHI.Ifthey fail

to make the propernotification orto apply forNHIwithin aspecified time (within 14 daysafterlosing their

insurance card), they lose coverage from their previous employers. Thus, increased possibility of

unemploymentincreasesthe dangeroflosing health insurance.

AsFigure 8 indicates,Japan’sunemploymentrate remained at2% untilthe early 1990s,increased

gradually to 5% in the 2000s,and now standsaround 4%.The unemploymentrate was4.1% in the fourth

quarteroffiscal2008 and rose to 5.4% in the third quarteroffiscal2009.In July 2009,unemployment

reached arecord high of5.6%.Despite amodestdecline,unemploymentremainshigh,particularly among

workers age 34 years and younger. The risk of unemployment is acute for non-traditionalworkers.

According to the Ministry ofHealth,Labourand Welfare,contractexpirations,workforce adjustments,and

otherterminationsamounted to 4,262 Japanese businessesbetween October2008 and December2009,and

cost244,000 non-traditionalworkerstheirjobs.

Ifdisplaced from residencesprovided by formeremployers,the unemployed withoutotherfixed

addressescannotapply forNHIbecause they mustdeclare localaddresseswhen applying forNHI.Even if

the unemployed retain previousemployer-sponsored coverage orjoin NHI,they may have difficulties

affording premiums.Partofthe premium forNHIisbased on the previousyear’searnings,even forthose

Figure 8:Umemploymentrate in Japan,by age group,1973―2013

who losttheirjobsand have no income3.Because premiumsforNHIare rising,even those covered by NHI

are in dangerofbecoming uninsured through inability to pay premiums.

3.Uninsured risk forNHIinsured

Since people are covered by NHIwhen they cannotreceive employer-sponsored health insurance,the

Japanese government’spublicstance isthatthere can be no uninsured in Japan.However,since NHIisa

socialinsurance system,premium paymentsand benefitsare applied.Ifthe insured cannotpay premiums

foran extended time,theirhealth insurance ceasesand they could become uninsured.

In April2000,the governmentrequired municipalitiesto issue certificate cardsofNHIeligibility to the

insured who have defaulted on premiumsfor1 yearormore;ifthe insured are dispossessed ofinsurance

cards,they instead receive certificate cardsofNHIeligibility,butthen,they cannotreceive insurance

benefitsforhealthcare servicesorprescription drugs.Moreover,some individualschanged to NHIcards

with limited effective dates;these cardsexpire sooner(afterlessthan 6 months,mostly after1 month)than

the generalNHIinsurance card (more than 1 year).Those holding the NHIcard with limited effective dates

mustpay premium arrearscontinuously.Ifthe card isnotupdated,itexpires,and the insurance benefitis

forfeited.Thisisan instance ofbecoming uninsured by notpaying premiums.

Non-paymentofpremiumshasincreased since the 1990sand 2000s.The percentage ofpremiumspaid

forthe NHIhasfallen since the end ofthe 1990s.Nationally,the percentage ofpremiumspaid in fiscal2009

averaged 88.01%,down 2.48 percentage pointsfrom fiscal2007 and the lowestsince fiscal1961.

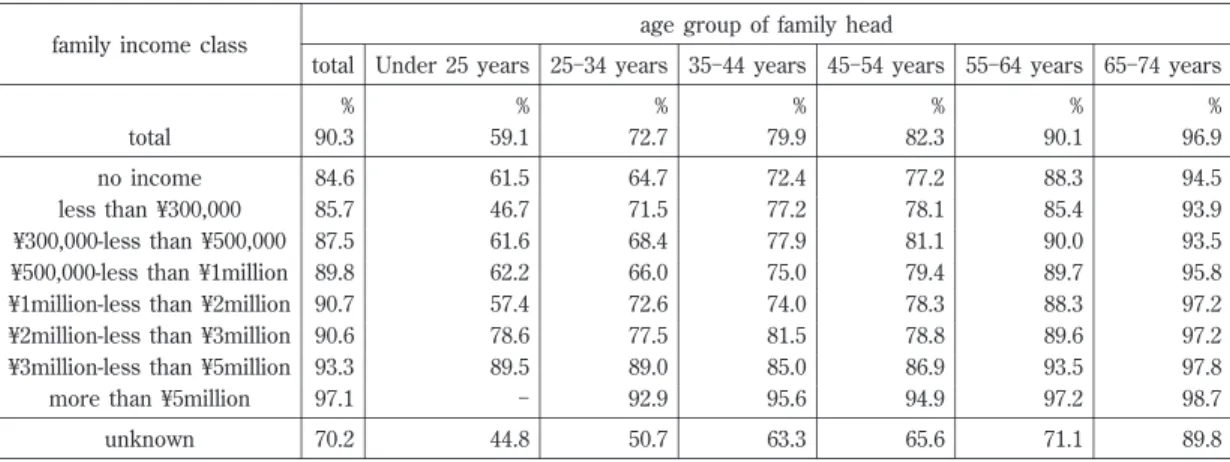

Table 5 itemizesthe percentage ofpaid premiumsoftotalcharged premiumsofNHI,by age group of

family head and family income.The percentage riseswith age,butasincome declines,the percentage of

premium paid islowerforallage groupsexceptforpeople aged youngerthan 25 years.

As Figure 9 shows, households that failed to pay premiums for NHI grew to 20.6% of all NHI

householdsbetween 2008 and 2010,butthereafterdeclined.In 2013,3,721,615 householdsfailed to pay

premiums(18.1% ofallNHIhouseholds).In addition,277,039 households(7.4% ofnon-paying households)

changed from the generalNHIcard to the certificate card ofNHIeligibility,and 1,169,533 households

changed to the NHIcard with limited effective term (31.4% ofnon-paying households).Compared with 2003,

Table 5:Percentage ofpayed premiums among totalcharged premiums ofNHI,by age group offamily head and family income class,2011

age group offamily head family income class 65―74 years 55―64 years 45―54 years 35―44 years 25―34 years Under25 years total % % % % % % % total 90.3 59.1 72.7 79.9 82.3 90.1 96.9 94.5 88.3 77.2 72.4 64.7 61.5 84.6 no income 93.9 85.4 78.1 77.2 71.5 46.7 85.7 lessthan ¥300,000 93.5 90.0 81.1 77.9 68.4 61.6 87.5 ¥300,000-lessthan ¥500,000 95.8 89.7 79.4 75.0 66.0 62.2 89.8 ¥500,000-lessthan ¥1million 97.2 88.3 78.3 74.0 72.6 57.4 90.7 ¥1million-lessthan ¥2million

97.2 89.6 78.8 81.5 77.5 78.6 90.6 ¥2million-lessthan ¥3million

97.8 93.5 86.9 85.0 89.0 89.5 93.3 ¥3million-lessthan ¥5million

98.7 97.2 94.9 95.6 92.9 ― 97.1 more than ¥5million 89.8 71.1 65.6 63.3 50.7 44.8 70.2 unknown

F ig u re 9 : Nu mb e r a n d t h e p e rc e n ta g e o f h o u se h o ld s w it h NH I th a t fa ll b e h in d o n t h e ir p re mi u ms , 2 0 0 3 ―2 0 1 3 20 13 20 12 20 11 20 10 20 09 20 08 20 07 20 06 20 05 20 04 20 03 20 ,5 83 ,6 82 20 ,6 37 ,3 60 20 ,7 11 ,3 75 21 ,1 36 ,7 52 21 ,4 46 ,4 73 21 ,7 17 ,8 37 25 ,5 08 ,2 46 25 ,3 02 ,1 12 24 ,8 97 ,2 26 24 ,4 36 ,6 13 23 ,7 13 ,3 39 to ta l h o u se h o ld w it h NHI ( A ) S o u rc e: Mi n is tr y o f He al th , L ab o u r, a n d We lf ar e (2 01 4d ).

the numberofhouseholdsthatfailed to pay premiumsand received the certificate card ofNHIeligibility

increased about2%,and householdsthatchanged to NHIwith limited effective termsincreased by 10%.

The increase ofhouseholdsthatfailed to pay premiumsisattributable to rising NHIpremiums.

According to Mainichinewspaper(June 8,2009),801 municipalities(44.6% ofallcities,towns,and villages)

raised NHIpremiumsin 2008FY,and 204 municipalitiesincreased premiumsby more than 50,000 yen fora

modelcase ofan insured household4.The ratio ofpremiumsto income isrising and the burden is

excessive forlow-income earners(Figure 10).Although the average fixed amountofthe premium is10.1%

ofincome,the percentage forhouseholdswith yearly income oflessthan 5 million yen exceedsthat.About

79% ofhouseholdswith NHIhave annualincome oflessthan 2 million yen,and theirpremium burden is

overloaded.

The socialaid system isleaving behind asubstantialnumberofimpoverished uninsured who cannot

pay premiumsforextended periods.The rapid increase in recipientsofpublicassistance since the end of

the 1990ssuggeststhatthe socialinsurance system inherited from the 20thcentury isceasing to function,

particularly asthe employmentstructure since the mid-1990shaschanged.

Although the numberofhouseholdsreceiving publicassistance (monthly average)decreased from the

mid-1980suntilthe mid-1990s,ithasrisen rapidly since the end ofthe 20thcentury (Figure 11),reaching

1,558,510 households,with acoverage rate of32.4‰ in fiscal2012.The numberofhouseholdsreceiving

publicassistance hasincreased since 1996.

By type,677,577 assisted householdswere “elderly households”(43.7%),defined asnon-working

households,and 475,106 (about30.6%)were “sick,injured,and disabled person households.”However,the

Figure 10:Calculated NHIpremiums perhousehold,and those as a percentage ofincome,by family income class (premiums forown health insurance and medicalcare system forthe latter-stage elderly people),2012

increase in fiscal2012 increase of“otherhouseholds”—those thatincluded aperson able to work—was

remarkable:284,902 households,an increase of31,162 (12.3%)overfiscal2011.

Ⅳ.

Di

scussi

on

The characteristicsofinsured groupsshow thatamajority ofpeople (60.3%)are enrolled in employment

-based health insurance.Unstable employmentand persistentunemploymentcould increase the numberof

employeeswithoutemployment-based health insurance.Thus,the state needsto improve accessibility for

employment-based health insurance.

Those who cannotparticipate in publicemployment-based health insurance could find alternative public

health insurance,NHI,asasafety net.

Howeverbecause the ratio ofpremiumsto income isrising and the burden isexcessive forlow-income

earners,more NHIinsured are losing theirpremium payments.Thiscould prove to be the breakdown of

NHIasmore Japanese could become “uninsured.”Thus,the state needsto improve the affordability ofthe

NHI.

Acknowledgements

Thispaperwassupported by the following projects:the Japan Society forthe Promotion ofScience (JSPS

KAKENHIGrantNumber:26285140)and the 50thAnniversary MemorialProjectofthe College ofSocialSciences,

Ritsumeikan University.

Notes

1 Thispaperisbased on Hasegawa(2011)updated by using new statisticaldata,altered,and refined.

2 “The three-quartersrequirement”wasmandated by the formerMinistry ofHealth and Welfare in 1980

(Shimazaki2011).

Figure 11:Actualnumberand percentage ofhouseholds receiving Public Assistance (monthly average), 1975―2012

3 Japan’snationalgovernmentestablished aprogram forworkerswho lefttheirjobsinvoluntarily (e.g.,through

company bankruptcy,dismissal,and non-renewed contracts).Underthisprogram,which came into force in

April2010,workerswho losttheirjobsand theiremployment-based health insurance could subscribe afresh to

NHIby paying lower-than-customary premiumsfrom the date ofunemploymentto the end ofthe following

year.

4 According to the Mainichisurvey,the modelcase ofan insured household isasfollows:annualhousehold

income is2 million yen and fixed assettax is50,000 yen forafamily offourwith ahusband and wife aged in

their40sand two children aged lessthan 20 years.

References

Kurata,S.(2004).“The jurisprudentialissue forthe increase ofatypicalemployeesin Japan.”TheQuarterlyof

SocialSecurityResearch 40(2):127-138(倉田聡「非正規就業の増加と社会保障法の課題」(『季刊・社会保障研

究』40巻2号).

Shimazaki,K.(2011).JapaneseHealthcare-System and Policy.Tokyo,University ofTokyo Press.(島崎謙治『日本の医

療─制度と政策』,東京大学出版会)

Hasegawa,C.(2010).“The universalhealth insurance system isfraying in Japan.”H.Shibuya,H.Higuchi,and J.

Sakurai,eds.Globalization,WelfareState,and Community.Tokyo,Gakubunsha:138-157.(長谷川千春「国民皆

保険システムのほころび」(渋谷博史・樋口均・櫻井潤編『グローバル化と福祉国家と地域』(21世紀の福祉国家

と地域2),学文社))

Hasegawa,C.(2011).“The uninsured in Japan and the United States:A comparison ofhealth insurance systems.”

Kokugakuin Keizaigaku 60(1/2):565-601.

Ministry ofHealth,Labour,and Welfare (2010).Diversification ofEmploymentPattern Survey2010.(厚生労働省『平

成22年度雇用形態の多様化に関する調査』).

Ministry ofHealth,Labour,and Welfare (2014a).AnnualHealth,Labor,and WelfareReport2014.(厚生労働省『平成

26年度厚生労働白書』).

Ministry ofHealth,Labour,and Welfare (2014b).NationalHealth CareExpenditure2012FY.(厚生労働省『平成24年

度国民医療費の概況』).

Ministry ofHealth,Labour,and Welfare (2014c).NationalSurveyofNationalHealth Insurance2012.(厚生労働省

『平成24年度国民健康保険実態調査』).

Ministry ofHealth,Labour,and Welfare (2014d).FiscalCondition ofNationalHealth InsuranceManaged by

MunicipalGovernments2012.(厚生労働省『平成24年度国民健康保険(市町村)の財政状況(速報)』).

Ministry ofHealth,Labour,and Welfare (2014e).Surveyon IndividualsReceivingPublicAssistance2012.(厚生労働

省『平成24年度被保護者調査』).

Ministry ofInternalAffairsand Communications(1984-2001).TheSpecialSurveyoftheLaborForceSurvey.(総務

省『労働力調査特別調査』)

Ministry ofInternalAffairs,and Communications(2002-2014).LaborForceSurvey(Detailed Tabulation).(総務省

『労働力調査詳細集計』).

Ministry ofInternalAffairs,and Communications(2014).LaborForceSurvey(BasicTabulation,HistoricalData).(総

務省『労働力調査基本集計・長期時系列データ』).

Ministry of Health, Labour, and Welfare (undated), An outline of the Japanese Medical System (English)

<http://www.mhlw.go.jp/bunya/iryouhoken/iryouhoken01/dl/01_eng.pdf>.Accessed 2015 Jan 6.(厚生労働省

本稿では,日本の医療保険制度の特徴を踏まえた上で,「無保険」を生み出す構造的要因について検討し, 公的医療保険のセイフティネットとしての機能について考察する。日本が国民皆保険の国として歩み始めて から,50年以上が経過した。それは,職業,年齢,性別,地域にかかわらず加入できるよう,公的医療保険 を包括化,一般化する道であった。しかし,21世紀に至り,日本において「無保険」問題が発生している。日 本における「無保険」問題とは,大きく二つの側面でとらえることができる。第1の側面とは,雇用形態の多 様化,失業を伴う雇用の流動化により職域保険から排除されることで,保険入手可能性に問題が生じている。 そして,第2の側面とは,医療費の増加に伴って保険料そのものが上昇しており,とくに公的医療保険の最後 のセイフティネットである市町村国民健康保険(以下,市町村国保)に加入する人の保険料負担可能性に問題 が生じ,実質的に保険診療が受けられない事態が生じている。国民皆保険とはすべての国民にいずれかの公 的医療保険に加入することを義務付け,被保険者とその被保険者を雇用する事業主に対し保険料の納付義務 を課すことを意味する。すなわち,社会保険方式に基づく医療保障システムは,社会保険料の拠出を給付の 根拠とする側面をもつ。公的医療保険を包括化,一般化することは,負担能力の低い被保険者や財政力が低 水準の保険者をも社会保険に包摂することを意味しており,保険料の負担可能性の追求と国家負担は不可欠 である。しかし,雇用構造が変化する中で職域保険から排除される被用者(主に非正規雇用の被用者)が増加 している。すなわち,非正規雇用(パート・アルバイト,派遣,契約,臨時など)とされる労働者は,同じ 被用者であっても雇用先で職域保険への加入資格が認められない現状がある。非正規雇用の職員・従業員の 割合は35.7%(20013年平均)を占める一方で,職域保険である健康保険の適用は半数に達しない。職域保険 に加入できない労働者は,被扶養者として健康保険に加入する人を除き,市町村国保に加入することになる が,両者で賃金喪失リスクへの対応が異なっている(「傷病手当金」「出産手当金」の有無)。また,失業の可 能性の高まりは,医療保険喪失の危険性を高めることにもつながっている。職域保険に加入できない場合, セイフティネットとしての市町村国保に加入することになるため,「無保険」という状況は生じないというの が建前である。しかし,市町村国保への加入は保険料納入の義務を伴うものであり,保険料を納付できない 状態が長期にわたれば,保険からの給付が停止され,保険医療を受けられない実質的な「無保険」状態が生じ うる。経済的困窮により保険料納付が困難ということになれば,被保険者証から短期被保険者証あるいは資 格証明書に切り替えられることとなり,その期間が長期にわたれば,ラストリゾートとして生活保護制度が残 されるだけとなる。公的医療保険のセイフティネットとしての機能を高めるためには,職域保険への加入可 能性(保険入手可能性)を高めること,そして市町村国保の保険料負担可能性を高めることが不可欠であろう。 キーワード:国民皆保険,職域保険,国民健康保険,非正規雇用,無保険,保険入手可能性,保険料負担可能性