Corporate Shareh01ding and Agency Cost

Katsura Nakano

Abstract

This paper incorporates the agency problenl with a risk_sharing argunl― ent for corporate shareholding. With a unilateral investrnent model,we find conditions for a pOsitive stock investment:(1)the manager is risk averse; 12)her managerial reward is linked with the value of the nrm she manages; and 13)the operating profits of investing and invested companies is negative― ly correlated. COrporate investrnent is larger if the invested company's operating prOnt is less v01atile and/or if the cOvariance in the operating profits of the companies is more strongly negative. If a manager is risk_ neutral, the manager becomes the residual clailnant and pays a high `竹

anchise fee"(1.e.negative wage)to the shareh01der.For managers with a medium degree of risk averslon, shareholders lower the rate of managerial reward which is linked tO the firnl's performance, and may have to pay a positive fixed wage to keep the managers in the cOmpany. If managers are highly risk averse, shareholders lower the link tO the performance further. The risk prernium remains high because the managers are highly risk averse,but is not so high because the managerial reward is linked weakly to the perfomance of the cOmpany. Hence the wage dOes not have to be so high tO keep the managers in the company. With such factors serving to lower incentive, the profit Of the company with highly risk averse managers is low.With a bilateral investlnent decision model, we find

一一一一in addition tO the above results― 一―一that COrporate investrnent tends *This paper is based on Chapter 3 of nly Ph.D.dissertation(Nakano,1999),

The Hikone Ronso No.330

to be larger if the investing company's operating pront is less v。 latile and /or if there is iess counter investment from the invested nrm to the invest― ing firm. We also find that shareholders' payoffs are lower than in the unilateral investrnent model, because the mutuality of investrnent reduces the risk reduction effect of stock investment in the bilateral investrnent model.

key words: intercorporate shareholding, risk sharing, agency costs JEL classiF■ cation:D81;G32;L10

1口 Introductiom

Today a substantial amount of corporate stocks are held by other

companies in many countries. Inter― corporate shareholdings are very corrlmon especially among JapaneSe firrns. For the last two decades, individual shareholders have owned only about 30% of shares of the companies which

were listed at the Tokyo Stock Exchange MIarket(Nihon Ginko,純 ぢ2aづ To乃θづハしγttο,various years).The remaining 70%has been owned by,most―

1 ) ly, private corporations.

There are three maior arguments for corporate shareholding;risk_shar― の

ing, market―power and control― rights arguments.

Aoki(1988,pp.225-234)introduces risk口

sharing argument.He arttues

1)The same statistics are available for some other countries such as Korea,Taiwan, and the United States. For example, in Korea, 50。 2% of stocks were owned by individuals in 1991 and this percentage has been fairly stable since early 1970s (Korea Statistical Yearbook,various years).According to Aoki(1988),individuals in the United States o、vned 51.1% of total shares outstanding in the United States in 1980,

2)There are some other arguments as well.For example,Tanigawa(1986)shows that

cross shareholding could benefit individual shareholders under the then」 apan's tax system that companies need not pay corporate tax for received dividend, while dividend tax is ievied on net dividend payment.

that a nrnl which is exposed to ldiosyncratic shocks can reduce rlsk by investing in other companies.Suppose that there are two nrms(ゥ ェ 1,2) and their operating profits are subiect tO tWO independent states(ブ ==1,2). The operating profits for each irm at each state are given byィ such that irm l performs better in state l and firm 2 does better in state 2;

πi > イ a n d π2 > π ら, I f b o t h i r l n s c o u l d i s s u e s o m e n e w s h a r e s a n d s w a p them each other, nrrns' profits, after dividend pattents and receipts, become

less volatile,According to Aokl, those who most benent frorn this type of inter―corporate stock investments are nOn_saleable stakeholders of companies such as employees. Individual shareholders, 、 vho are saleable stakeholders, can reduce their risk through corporate stock investrnent,but they do not necessarily rely on this mechanism to diversify their portfollo.Workers in a company, on the other hand, accumulate their wealth in the company

and a part of the wealth is paid out as a separation payment, which usual― ly is neither portable nor marketable. In most」 apanese firms, where quasi― life―tirne and senlority―payment systems prevail, workers bear human capital investrnent costs and receive low wages in the nrst years of their career, 、vhile they are compensated in later years. The wealth retained in a company in these forms depends on the performance of the company and there is no way for employees to diversify these holdingse Since managerial compensation is usually linked to the performance of the company, rnanag―

3)

ers also hold non―saleable stakes in the company. For this reason employees and/or managers want the firrn to hold the shares of other companies to reduce the volatility of the company's performance.

Market‐ power argument was originally introduced by Reynolds and Snapp (1986)and further developed by Flath (1991)and Reitrnan(1994). Reynolds and Snapp argue that, under a Cournot model, a firnl with

134 The Hikone Ronso No.330

shareholding in its rival reduces product market competition because the irnl's total profit is linked to that of the rival through dividend payments. As a consequence of this horizontal shareholding, the equllibrium price(or

quantityl is higher Qowerl than the competitive price lquantit,.For example,

if there are tt identical firms in a market and if each firm owns 1/物

frac―

tion of shares of every other firnl, then the industry will produce the monopoly level of output in equllibrium. According to their model, as the amount of corporate shareholding increases form O to 1/?み , the industry moves frorn 4り firms' oligopoly to monopoly. It is interesting to note that conventional market concentration ratios such as Herfindahl index do not

4) prOperly reflect the true state of market competition.

Flath and Reitrnan question the Reynolds― Snapp's argument in light of individual rationality, although they agree to the argument that firms in the same industry rnight want to invest each other in order to reduce the market competition.

Flath creates a two― nrrn tw。 _stage Nash duopoly model, where each firm decides the amount of stock investrnent in the other irrn in the irst

5) stage and the firrns compete in product market in the second stage.Accord― ing to the model, a irm actually invests into the other irms only if the irm knows that investrnent results in an increase of its own proits rath―

er than the joint pronts of the investing and invested irms. The first st―

age necessary condition can be decomposed into two effects; ``strategic 4)An example shown by them is as follows.If each of ten irms,with no shareholding

ties,had a ten percent market share, a four― firm concentration ratio would be 40%. However, if each had a ten percent interest in each of the other irms, then their model suggests that the industry 、 vould produce the monopoly level of output. 5)Flath (1989)looks at the vertical shareholding ties, instead of horizontal ones. He

shows that more stock investments by upstream firms in downstream firms will lower the consumer price,but imore investIIlents by downstream arms in upStream firms does not lower and may even raise the price. According to Flath, the reason for this asymmetry is because upstream firms are the irst movers.

︱ ︲

ettect" and “direct effect''. The strategic effect is the effect on the invest― ing firnlPs profit of the stock investment through the change in the invested firnl's choices in the product market. The direct effect is the change in the investing nrrn's pront by the stock investrnent through the change in its own choices in the product market. Flath says that, for both Cournot and Bertrand competition in the product rnarket, the direct effect is negative because the im has to give up a part of its own Operating profit to obtain a partial ownership in the other firms. Since the investment into the oth― er irms makes the investing firm react softly, for the fir■ l to make a positive investment, the choice variables in the product market have to be strategic complements Cat cat ploy;Tirole,1988).In other words,for the existence of a subgame perfect equllibriunl, the product market competition cannot be Cournot competition, but could be Bertrand. Flath shOws that, under Bertrand duopoly, there can be a Nash equllibrium with cross― shareholding, if the products of rivals are ilnperfect substitutes. If the products are perfect substitutes, it would not be rational to acquire the shares of the other firm.

Using a conieCtural variation model,Reitman shOws that all of the firms in the industry do not necessarily agree to participate in a cross shareholding relationship at a Nash equllibrium. It may be rational for sOme firms to stay outside the cross shareholding arrangement because there is a positive externality for the firms which decide not to participate in the arrangement. Reitman finds that it is not rational for any firrn to participate in any cross shareholding relation, if the number of irms in the industry is three and if they are competing in Cournot or less rivalrous way. On the other hand, if the irms are competing in more rivalrous than Cournot, such as Bertrand, there exists an individually rational cross shareholding arrangement.

The Hikone Ronso No。 330

Despite some variations, the market― power arguments corrlmonly predict that inter―corporate shareholdings, if any, should reduce the rnarket competi― tion and increase the profits of the nrms.

The risk―sharing and market… power arguments are based on a function of common stocks as profit clairns.Control口 rights arg_ent,On the oth― er hand, focuses on the other characteristic of conllnon stocks as control― rights. Resolutions regarding management of a firm such as appointrnents of board mettbers are deterrnined at shareholders' rneetingso With corporate shareholdings, Inanagers of an investing company represent the company and exercise the voting rights on behalf of the company they manage.

Based on this characteristic of coHllnon stocks, t、 vo types of arguments have been made in order to explain corporate shareholdings.

Perotti(1992)and Berg16f and Perotti(1994)say that cross sharehold一 ing(CSH)is a sort bf hostage exchange to support collaboration among managers. In their model, managers make two decisionsi collaborate or

not;and exert effort or not,A rnanager's effort,say R&D effort,increases the proit, not only of her irrn, but also of the other firms if those firms

c o l l a b o r a t e w i t h e a c h o t h e r i n a R & D p r o i e C t . T h i s e x t e r n a l i t y d o e s n o t exist if they do not collaborate. There is a certain range of payoffs for

which the managers fall in a prisoneris dilernlna when a cross sharehold― ing arrangement does not exist. In a one― shot game, they do not collaborate but exert effort for their own sake. In a repeated― game setting, a punishm ent for deviation is to end collaboration if there is no cross shareholding arrangement. The punishment, however, may mot be strong enough to force the managers to collaborate. With a cross shareholding arrangement, a manager who deviates will be ousted by the other managers, and this threat

of job loss,which is a more sever punishment,can induce every manager to comply with the agreement. Hence profits are higher for the firms

which participate in the cross shareholding arrangement.

The other type of argument in this category says that cross sharehold― ing arrangement prevents any member firln from being taken over by outsid一 ers.Osano(1996)claims that eliminadon of takeover threat makes tt possi― ble for the managers in the cross shareholding arrangement to invest a

(state_depended)high―

risk high―

return project rather than a risk―

free low―

return proieCt.Without a CSH arrangernent,there is a threat that manag― ers may be evicted if the outcome of a high― risk project is very bad. If the possibility of eviction is high, the managers are scared to invest in the high―risk ptteCt even though the expected retuHl of the proieCt iS high― er than that of a risk―free proiect.A CSH arrangement,however,can ensure that mettber irrns support each other whatever the outcome is, and remove the threat of takeover. With a CSH arrangement, the managers can safely invest in a high―risk high―retuHl prdect.BOth types of control―rights argurn― ents state that companies should exhibit higher proits、vith cross_sharehold― lngs.

This paper explores Aoki's risk― sharing argument in light of manager's incentive for stock investrnent. First, this paper introduces the principalぃag― ent issue. Shareholders and managers are in a principal― agent relation. Second, this paper assumes that each manager non― cooperatively decides on stock investrnent.

MIodels presented in this paper incorporate the principal_agent issue, explicitly,with the risk― sharing argument as followso Suppose that a risk_ neutral shareholder is the principal and a risk― averse manager the agent. Non― observable managerial effort is the prilnary input for a company. Managerial payment scheme consists of a performance― based reward and a nxed wage, where the performance of a company is measured by the

The Hikone Ronso No。 330

the managers non― saleable stakeholders of the company. A stronger link between the company's performance and the managerial re、 vard works in two different directions. First, it increases the risk that the managers have to face, as is discussed in Aoki(1988). Secondly, it increases the manager's incentive to exert effort, as in any standard principalhagent model. Given the contract, managers try to maxirnize their expected utility by choosing the level of their effort and the amOunt of corporate stock investments. Shareholders, on the other hand, try to extract all the rents frorn the managers by choosing a payment scheme which will keep the managers in the company.

One of the purpose of this study is to see if our model, a risk― shar― ing model with agency cost, can provide a consistent explanation for the

stylized facts that, in」 apan, COmpanies which are more involved in inter― corporate shareholding exhibit lower but less volatile profit rates measured by return on assets.See for example,Caves and Uekusa(1976),Hoshi and lto(1992),and Lincoln,Gerlach,and Ahmadiian(1996).The above AokiPs

risk sharing argument consistently explains the lower volatility of proits, but not the lower level of profitso None of other arguments discussed in this introduction do not seem to successfully provide a complete explana― tion for the stylized facts, either. The market―power argument predicts that the profits of the firms should rise with reduced competition, which

contradicts the observations that profit rates are lower amo4g cOmpanies which are more involved in inter― corporate shareholding. The control_rights argument states that companies should exhibit higher(average)prOnts with cross―shareholding,which also contradicts the findings of empirical studies. MIoreover,the choice of risky proieCtS in Osanors rnodel should cause rnore volatility in the companies' c寛 ‐pοsけ profits.

of unllateral stock investrnent under a standard principal― agent model will be considered. A silnple model explains when and how a manager can

reduce risk by investing in another company. In this model, the invested company is an entrepreneurial company and does not hold any shares in the investing company. The third section extends the model to a bllateral investrnent model, by assurning that the invested company also has the same principal―agent problemo This adds llew tiers to the model― magい ers(and shareholders)of the two companies interact strategically when

they choose their variables. The fourth section draws concluslons from the second and third sections.

2日 PoA Model Mれ th lUttateral Stock lnvestIElent(Dpportl回 問ity Let us start with a standard principal― agent model. A firnl, say firm l, is owned by a risk― neutral individual shareholder and run by a risk―

averse manage?. The firIIl's prOfit, π

l, iS generated by a manager's non―

observable effort, θl, with a disturbance, ε l: πl = θl + εl

where

ε

l ∼N ( 0 , σ

そ

) 。

Thereお a cost of effort to the manager,whch為 歩θ?・The manageゴ s net income is denoted by 71 and the manager's utility function is ― ―exp (一 γ171)where γl is the manageゴs degree of absolute risk averslon.

The tirning of the game is as follows. In the first stage, the sharehold― 6)Individual shareholders are assumed to be risk neutral, due to mainly a technical

reason, If individual shareholders are risk averse, deterllination of stock price becomes extremely complicated because individual shareholders intervene the managers' investment decisions by affecting the stock priceo Since the focus of this study is on the risk sharing behavlor of non― saleable stakeholders(i.ee rnanagers), individual shareholders,who can diversify their portfolio directly,are assumed to behave as if they were risk‐neutral in this model.

︱

,

The Hikone Ronso No。 330

er wtttes a contract. Since Httnagenal erort is non― observable, the sharehold― er has to write a contract on observable variables. 小 ブ【anagerial reward can be linked lto either the operating pront or the value of the company. The shareholder can also pay a wage. If the wage is negative, it is a transfer payment fronl manager to shareholder. The manageris expected utility must be non― negative so that the manager will participate in the contract. In theisecond stage, given the contract, the manager decides on her effort. If opportunities to invest in other firms exist, the manager also decides on the nrnl's investrnent. Since firms in this model do not have any fund

7)

at this stage yet, only the decislon is made in the this stage. Finally, the manager exerts effort, and the stochastic elements are revealed. Shares are transacted at the pre_deterrnined price and quantity as decided in the second stage, Pronts are distributed to the manager and the shareholder according to the manatterial contract and the ownership stttcture.

What follows shows that;(1)operating― pront―based and value― of_the―nrrn_ based payment schemes in the incentive contract are equivalent for both individual shareholder and manager if there is no investrnent opportunity;

12)with the Operating― pront―based payment scheme,a manager can never reduce risk in her income by investing in another company and;(3)with the irrn―value―based payment scheme, a manager can reduce risk by invest― ing in another company, which eventually beneits the shareholder.

(1‐1)Operating口 ProFlt‐based Pa7ynent Scheme wtth No lnvestIIlent Opportunity

Suppose that the managerial reward is a fractiOn 九 l of the operating profit plus a wage切 1.Then the manageゴ s net income,り 1,is九 l πl+物

1-7)Bond financing could be included in nature of our argument as iong as the

the model. It, however, does not change the possibility of bankrupcy is not considered.

イ/2.Given that the manageゴ

s utility function is一

exp(下γ

lク

1),the

certainty equivalent income for the manager, ″ 1, ls

触=朋[夕

]―

考施γ

[勢

]

=如a十例一歩イー歩相 ・ (1)

The last ternl is the risk prernium.

In the second stage, the manager maxilnizes the certainty equivalent income, β l, with respect to her own effort, θ l. Hence the optilnal level of effort is θi=九 1.The manager exerts more effort when the managerial

reward is more strongly linked to the operating profit of the nrrn‐ As you see in the above equation, a higher ttl increases not only managerial effort but also the degree of risk that the manager is exposed to.

Shareholder's net income,物 1,is(1-九 1)πl― 切1.Being risk neutral, the shareholder is concerned with his expected income,ゴ [物1]=(1-九 1) θl 紀妙1. In the first stage, the shareholder maxirnizes his expected income SubieCt tO the manageris participation constrainti

m a x ( 1 - 九

1 ) ゴ

[ π

l ] ―

切1 = 城

紡

( 1 九

1 ) 九

1 - 切

1 ( 2 )

九1,り1

subject to

イ十

例一

号だ一

歩イぱ対

Assunling that the participation constraint is binding, the solution is

拭 = 杭 2 伸 )

1

and

Ⅲ γl σ

そ

T l

( 4 )切1= 2(1+γ

l σ

?)2 ・

‖

142 The Hikone Ronso No.330

ing pront(i.e.larger九 1)assigns more risk to the manager.Although the shareholder himself is risk neutral, a large risk preHliuHl for the manager means that less can be extracted froHl the manager while keeping the

manager in the firm. Hence the shareholder has to set 九 l small at the expense of manager's incentive so that the risk prernium for the manager will be small. See Figure l.Note that σ l is assumed to be one in all of the figures in this paper.

Figure l:九i as Function of γl:Model(1-1)

Figure 2 shows that as the manager's degree of risk aversion rises, 8)

the wage increases, initially, and then decreases. The increasing part is associated with the gradual weight shift from a perforrnance― based reward towards a ixed wage. As is shown above, when the manager's degree of

risk averslon is sHlall, the shareholder gives higher incentive to the manag―

えi

3

例

er. With the higher incentive, the expё cted profit of the company is large, and the shareholder asks the manager to pay a higher “ franchise'' fee(1.e. negative wage).The middle part of the function shows the case where,if the manager is moderately risk averse, the shareholder has to provide a

positive wage to keep the manager in the company. If the manager is high― ly risk averse, the risk prenliunl ls high, but not so high because the managerial payment is weakly linked to the performance of the company by a lower 九 l value. The、 vage can be lowered accordingly. This is shown in the decreasing part of the function.

In equilibrium, the shareholderis expected payoff is

H 凋

=

切 ]

Figure 2:切 i as Function of γ l:Model(1-1)

Figure 3 depicts the shareholder's expected income, which decreases the manageris degree of risk aversion lncreases.

144 The Hikone Ronso No.330

This lnakes a benchmark case for the following arguElent.

E[ul]

Figure 3:Shareholder's Expected lncolne as Function of γ l:コ班odel(1-1)

(1‐2)ValuC‐ Of‐the o FirIIL口BaSed Payllent Scheme Ⅵ 成th No lnvest白 ment Opportllnity

Suppose that everything is the same as in model l-1, except that the manatterial reward is a fraction九 l of the value of the irm plus a wage, 欲九.The value of the irln,υ l,is deined after wage payment.It is,therefore, 死1-―彼,1, if there is no outside investment opportunity. Then the manager's

i n c o m e , り

1 , i s 九

1 ( 死

1 - 切1 ) 十

切1 - 歩

θ

? , a n d t h e c e r t a i n t y e q u i v a l e n t i n c o m e

f o r t h e m a n a g e r , βl , i s 九l β[ πl ― 物1 ] 十 切1 - 歩 θ? 一号 イ σ? ・T h e c e r t a i n t y equivalent income is maximized,as before,when θ i=九 1.

T h e s h a r e h o l d e ゴs e x p e c t e d i n c o m e i s ( 1 - 九1 ) ゴ[ 死1 - 御 1 ] i n t h i s s e t u p . The shareholderis maxirnization problenl is

3

γ

Subiect to

九1 ( 九1 - 切 1 ) 十切]

一

歩イー

サイぱ≧

は

This forFnula appears different from the previOus rnodel.However, assunling the participatiOn cOnstraint to bind and manipulating the expres― slon to elinlinate the wage, the reduced form Of the maxirnization problem is the same in the twO models. Thus, the optilnal chOices Of九 1, and hence

the level of effort,is the same as in model l-1:九

i=1/(1+γl σ

?).The

wage,

ガ = ω

is direrent because the value of the irnl is denned by the operating pront minus fixed wage.Despite the change,物 i has the same property as in the prevlous model一 一一―it is increasing in γ l and o「l if bOth γl and σ l are

9) small, while decreasing if they are large.

Although復 尤is different,the shareh01deゴs expected payoff is the same as in model l-1.

H 州 = o

This is because the shareh01der payoff is the operating pront Hlinus the manager's cost of effort rninus the risk prerniunl, which are all the same as in model l-1.

This shOws that the twO payment schemes in models l_l and l_2 are equivalent. The following subsections shOw that the equivalency Of the twO payment schemes does not hold when there is an Outside investrnent opportunity.

9 ) M o r e p r e c i s e l y , 切i i s i n c r e a s i n g i n γ1 0 r σl i f γl σl < 1 + 7 7 , w h i l e d e c r e a s i n g i f

146 The Hikone Ronso No。 330

(2‐1)Operating o PrOrlt‐ Based Payment Scheme with lnvest】 ment Opportuttity

Suppose that there is an entrepreneurial company, firm 2, which generates

π2 = σ2 + ε2 ( 8 )

Where σ 2 iS a the arst_best effort level which is ixcd,while firln l's operat― 101

ing profit is the same, 死 ュ=二例 十 εl. εづ iS a random variable with

ε

∼

X は■

l a n d Σ

封& 1 翻.

From convention, σ づ stands for the standard deviatlon of shOcks. σ ″ is the covariance between ε づ and cブ . Firm l is Owned by an individual shareholder. The tOtal number of shares is one for each firm.

Under this circumstance, irm l has an opportunity to invest in firm 2. Suppose that, in the second stage, firm l asks firm 2Ps owner to sell sorne fraction αl of irrn 2's shares.The value of the shares is α l力2 While the cost is αlp2 Where p2 iS the share price. A risk_neutral owner, 、vho originally had 100%of arm 2,is entitled to(1-α l)π2after this transac― tion while receiving α lp2 in CaSh. The share price is deterrnined by an “

efficient market". In an efficient market, the price of a share is equal to ll)

i t s e x p e c t e d v a l u e ; p 2 = ゴ[ π2 ] .

What follows shows that nOthing changes by the existence of outside investment opportunity, as long as the rnanagerPs reward is based on operat― ing pronts. under an operating_proit― based payment scheme, the manager's

101θ2dOeS not have tO be the arst_best effort level for the following argument to h01d, 11)Obvlously this is a strong assumption because, for this to be true in general,

everybody in stock market has to be risk neutral with no tilne preference. This assumption, however, allows us tO single out the managerial risk sharing issue, which is the focus Of Our study.

net incOme, グ 1, and hence the certainty equivalent incOme, 21, is the same as in mOdel l_1(equatiOn l).TherefOre the manageゴ s chOice remains the same as well: θl=九 1. Since 21 ls independent Of αl, the arnOunt of investrn― ent is indifferent tO the manager.

Given the above, the payoff to firm l's shareh01der, 物 1, is denned by irm l's Operating pront plus dividend incOme from irm 2 ェ linus purchas― ing cOst Of firm 2's share nlinus managerial compensatiOns: 物 1=π l―十αl

″2 α l う2 九 l πl ―物1 . s i n c e β[ πl ] = θi a n d β[ π2 ] = 疹2 i n t h e e q u a t i o n , t h e e x p e c t e d p a y o f f t O t h e s h a r e h o l d e r i s β[ 物1 ] = ( 1 - 几) θ

i ―物1 , w h i c h is the same as in model l_1. Hence the shareh01der's maxirnization problem

is identical 、vith the one in mOdel l_1, as is the s01utiOn.

In sunl, the existence of an investment oppOrtunity does not change the equllibrium chOices Of bOth manager and shareholder if the managerial compensation is based on the operating prOfit Of the firm.

(2口2)Vallle口 Of‐the口 FirIBrl‐Based Payment Scheme with lnvestIIlent Opportllnity

The next shOws that, if the managerial re、 vard is paid based On the value Of the firrn, intrOductiOn Of Outside investrnent opportunity benefits the shareholder.

When firm l holds a fractiOn α 1 0f firm 2, the value of nrrn l is, o l = π t t αl υ2 - αl p 2 - 物

Where υ 2 is the value Of firm 2. The terms On the right hand side of the equation are; the Operating prOnt Of the firnl, the market value of the shares purchased from an individual shareh01der of nrm 2; the mOney that is prOnlised tO be paid to the individual sharehOlder; and the ixed wage paid to the manager. These four items denne the market value Of nrm l. Since nrm 2 does nOt Own any nrnl's shares, the value of irm 2 is sirnp―

148 The Hikone Ronso No.330

ly equal to its operating profiti υ 2=π 2.

With a value― of―the―firEl―baSed payment scheme, the manager's income

lS

勢 = 加 例 十 例 一 歩 家 .

W i t h t h e e t t c i e n t m a r k e t a s s u m p t i o n ( 1 . e . p 2 = β[ υ2 ] ) , t h e e x p e c t e d v a l u e of the irm is equal to the level of effort Hlinus wage paid to the manager,

β[ υl ] = β[ πl ―切1 ] = θl ―切1 .

Thus, certainty equivalent income for the manager, 21, is 触 = 九 〈例 一 似 ) 十似 一

号 イ

ー 望

セ1 生( 拭 + 2 σ1 2 a l 十梶 ぱ ) . ( 9 ) Given the payment scheme, the manager in the second stage maxilnizes

βl w i t h r e s p e c t t o θl a n d αl s u b j e c t t o O ≦αl ≦1 . T h e s o l u t i o n i s θi = 九1 and αi = 0 1 f O ≦ σ1 2 ≦1

= σ1 2 / σ

2 i f 一

σ2 ≦σ1 2 < 0

= ユif σ

12< σ2

What is found here is as follows.First,αi is independent of the nrst stage choices, 九l and 彼,1. Secondly, the covariance must be negative for the optilnal amount of investrnent to be positive. This is because cash, which is a risk_free asset, is pronllsed in exchange for a profit clailn in the outside proieCt,Which is a risky asset.A rarnification of the second finding is that firm l's standard deviation (σ l)has to be positive for the optimal amount investment to be positive,because the covariance(σ 12)iS always zero if the standard deviation(σ l)is zero.This means that only a manager of a risky irln invests in other companies.Thirdly,in its interior,

stock investment is larger if the covariance in operating profits is smaller

(1.e. mOre strongly negative)and/or if the target company's level of risk is smaller.The degree of risk that irm l originally faces(1.e.σl>0)does

12)

not affect the equllibriunl level of investment. Lastly, if the invested company is very safe, the optilnal level of investrnent reaches the bounda― r y , αi = 1 .

The managerts participation constraint, and therefore the maxilnization problern in the irst stage, depends on the managerial investment choice in the second stage.When there is no stock investrnent(i.e. α i=0), the maxirnization problenl, and the solution, is the same as in model l-2.With positive investrnent, the participation constraint is

ね ( 如 ― 例 ) 十例 一 歩 イ ー 学 σそ( 1 - 百ゴ景身葬つ ≧ 0 i f O < α i < 1 加 ( 如 一 似 ) 十例 ― チ イ ー 王 午す 生 < 拭 + 2 σセ 十 α ) ≧0 if α i=1

depending on the equllibriunl level of investrnent.

In order to further analyze these two cases, let us define a function such that

メ

1(γ

l,σ

l,σ

2,σ

12)=γ

lσ

?(1-σ物/σ

?σ

2)if ―σ2≦σ12<0

=γ

l(σ

?+2σ12+σ

2)if σ

12≦σ2

1t is straightforward to show thatメ

l iS increasing in γ

l, σ

l, σ

2,and

σ12,aS 10ng as σ

12<0,Since the risk premium is九

?/1/2,this means

that the risk prerniunl increases as either the manager's degree of risk12)The reasOn for this is,again,that cash is prornised in exchange of another company's stocks in our model and that investing irnゴs decis10n is made solely based on the marginal cost and beneit of such an exchange.

150 The Hikone Ronso No.330

averslon, the variances in investing or invested firnl's operating profit, or the covariance in operating profit increases. Note also that」 βl is positive

13) as long as the parameters, γ l, σl, σ2, and O「12, Stay in their feasible regions

Suppose that the participation constraint is binding. Then a reduced form of the shareholder's maxilnization problern is

臀 ( 1 如 ) 加 十 イ ー →井だ 一 ギ井だ ぬ 伍 , 例, σろσ姥) . Q D The solution is

︲

一 町

〓 九 and 率 / 1 - 1切1= 2(1+/1▼

1・

The shareholder's expected payoff is

β

[拭

]=2(1■

/1)=号

拭

(14)The functional forms of tti and tti in thiS model are the same as

those shown in model l-2.Replacing/1 in the above equations with γ

lσ

そ

reproduces the solutions for model l-2. Equation 12 shows that tti is

13)This can be easily shown, remembering the correlation coefficient, ρ, is always between minus one and one; -1≦ ρ=σ ヶブ/σづqブ≦ 1.

(1)γ

lσ

?(1-σ勉/σ

?σ

2)≧O since

γ

lσ

?(1-σわ/σ

?σ

2)=γ

lσ

?(1-ρ2)

and γl,σl≧ 0。12)γ

l(σ

?+2σ12+σ2≧O since

σ?+2σ12+σ2=(σl―σ2)2+2(1+σ12/σ

lσ

2)σ

lσ

2

=(σ l― σ2)2+2(1+ρ )σlσ2 and γl,σl,σ2≧ 0.Q.E.D.14)In modeis,1-2 and 2-2,the value― oユthe―nrm based payment scheme is employed. In model l-1, on the other hand, the operating_profit_based payment scheme is used. This is why the wage function in model l-l is not comparable to the ones in models l-2, 2-2 and the bilateral model in the next section.

Corporate Shareholding and Agency Cost 151 decreasing in/1,While equatlon 13 shows that tti is increasing for a small― er value of」rl and decreasing for a larger value. Applying the chain rule, we can study the comparative statics of γl,σl,σ2and σ 12 0n tti and切1. 九i iS decreasing in all of these variables.As we have discussed,marginal

effect of those variables on tti depends On the value of Jl:For a srnallメ1, 切i iS increasing in γl,てア1,(ア2 andてア12,While for a large jFl,it is decreas― lng.

An important fact is thatメ

l is alWays smaller than γ

lσ

?as long as

15)

the covariance is negative. This means that the shareholder would choose a larger 九 l than he would without outside investment opportunity as in model l-2. The high managerial incentive makes the shareholder better off as is shown in Figure 4. The upper line is with the investrnent opportuni― ty(mode1 2-2),and the 10wer one is without it(model l_2)when σ l=σ 2 a n d σ1 2 = - 0 . 5 .

This figure clearly shows that, with outside investrnent opportunity, the firrn―value―based payment scheme ilnproves the shareholderis expected income.

Up to this point, we only allowed one company to invest, unilaterally, in the other company. In the next section, we consider what happens if both companies can invest. It adds new layers to the model, representing strategic interactions of managers and shareholders in two companies.

15)The proof is as follows.

(1)γ

lσ

?(1-σわ/σ

?σ

2)=γ

lσ

?(1-ρ2)≦γ

lσ

?since-1≦ρ≦1.

12)γ

l(σ

?+2σ12+σ2)≦γ

lσ

?since

2σ

12+σ2<-2σ夕十σ2≦0

frOm σ

12<一σ2<0.Q.E.D.

The Hikone Ronso No.330

Top:Mode1 2-2 1with investment)

Middle t Bllateral Model lwith investment) Bottom:Models l-1,1-2,and 2-1(no investment)

E[ul]

0 1 2 3 4 5 6

γl

Figure 4 i Shareholder's Expected lncome as Function of γli Comparison

3.P口 A Modell胡 ith B工ateral Stock lnvestIIlent OpportHLmty 3.l The Model

Suppose that there are two firms, and one shareholder for each of the firms. In the first stage, each shareholder, independently, writes a managerial incentive contract. In measuring the performance of manager, the value― of_the_firrn is employed. In the second stage, Inanagers non… cooperatively decide on the amount of stock investrnent and the level of their ettorte Corporate stock investrnents can be mutual.

The remaining assumptions are the same as before: Initially, there is no corporate shareholder in the economy and none of the individual

shareholders holds the shares of more than one firln; the nuttber of shares for each firrn is equal to one; managers are risk― averse, while individual shareholders are risk― neutral.

︱ ︱

The operating pront of nrmづ (ぢ=1,2)is π = θを十 εづ

ε ∼ N ( 0 , Σ)

whereづ,ブ=1,2.

The mrket value of firrnづ after corporate shareholding and wage payEl―

ents is

υづ= 力 十 αづη― αぁp ゥー 物

where αづis a fraction of irmブ'S Shares held by irmめ and tt is nrmブ's share price. Solving the above equations for υら we obtain

1

υづ= 可

ず 液 万 ( πづ十 αづ殉 一 αづ勲 α t t p め一 αウ物 切 つ. ( 1 5 ) The value of the firm,υ め, is distributed among the residual clailnants; 九 ″づ

t o t h e m a n a g e r , 的υづt o t h e c o r p o r a t e s h a r e h o l d e r , a n d ( 1 - ん―釣) υめt o the individual shareholder of irrn づ.

U n d e r t h e e f f i c i e n t m a r k e t a s s u m p t i o n ( 1 . e . p づ= β [ υづ] ) , t h e e x p e c t e d value of the firnl is equal to the level of effort rninus the 、 vage,

β[ υぢ] = β [ πづ] 一物 = θゥー 物ぁ. ( 1 6 ) Hence managerめ 's certainty equivalent income, under the value―of―the― firm based payment scheme, is

角九7(σ

夕+2σ″αづ

+ σ?α7)

2 ( 1 - α づ釣 ) 2

(1の

The risk preEliunl is concave in the amount of the firrn's investrnent, αづ. It is also a function of counter― investrnent, oけ. The counter― investrnent increases the risk prenllum as long as at is positive. This is because, with

higher counter―investlment, rnore of nrHlゲs investrnent into firrllブ is re― invested in firHl あ, thereby reducing the effectiveness of firHl づ's investrn― ent in nrlrnブ.

勧 = ん ( a 一 物 ) 十 物 ― 七 井

:

The Hikone Ronso No。 330

3.2 The Solution The Second Stage

Managersぢ

's objeCtive is to maximize her certainty equivalent income,

勧, taken as given the strategy of managerブ

. The constraints on their

choices are O≦ αづ, 6り≦ l and α ゥ∽ +1. The last constraint excludes the case where α t and tt are both equal to l, which would be the case if the risk prerniunl is infinite. Without loss of generality, we can assume σ ゥ≧

匂 .

Frorn the first order condition, the level of effort for managerぢ is

θ

げ= ん 。

Assuming an intettor solution,Inanagerゲ

s best reply to rnanagerブ

's inVestin―

ent choice is

ば = ― 個

T h e c o n d 止 l o n t t r α; ∈ ( 0 , 1 ) 的 r 況 l v t t u e s o f 鈴 為 一ヴ < σ ぢブ< ] ・ I f

the covanance tt so sm】

l that σ

″<―ギ,the opdmtt vttue of α

づ為equ】

to one for low values of αブ. If the covariance is positive, manager t's best reply is not to invest in firHlブ . The abOVe conditions are the same as those for the unilateral investment model(1.e.mOde1 2-2,hereafter)to have

an interior solution. In the following analysis, we assume these conditions are satisfied for あE=1, 2.

The best reply functions for the investrnent choice in the bilateral model has several interesting properties.First,α;is independent of the first stage choices,九s and ttso Secondly,α;is decreasing in firmブ's

standard de宙

adon,の

,and the covattance,胡

.Thrdけ

,α

;蔦decreasing

16)The irst hequality condition tt deAved ttom a fact that α

ナis a decreashg functbn

of αブ, as will be proved later in another footnote. Based on this property, the upper

in σ

ゥ

>O as long as the counter investment,α

ブ

,ls nOt Zeだ

).This is

because, given other things cOnstant, a part of firHlづ's investrnent in firm ブ returns tO finttlづ through recursiveness Of crOss shareh01ding and thereby,

if irmぢ is riskier,the stOck investment in irmブ becOmes less effective.

Forth,α

すis decreasing in the opponent's investrnent arnount at an increas―

ing rate(1.e.α

づ

and α

ブ

are strategic substituteぎ

.The intuitlon is that

counter― investment decreases the marginal effectiveness of stock invest― ment to reduce risks.

Figure 5 is a representative best reply functiOn for managerづ .

Note that α

;三一σづ

ブ

/ギ whenげ=0,and the Ask premium fOr

managerづ

掩smallest atサ

イσ

7(1-乾/ギ),whch tt the same as the

equilibrium risk prernium under the unilateral model. The risk prernium

17)The proofs are as f0110ws.

等=等宰=ギ

相緋 均

i s n e g a t i v e s i n c e , f O r O < αブ< 1 , σ 材十 σ夕αブ< σ り十 σ7 ( 一 σ″σ号2 ) = 0 .新= 予

約静

is negative since一

ギ十σ′

ギ<― ギ十暢σ;2←αブ<_∽ σ;2

< 0 年 - 1 ≦ σ″/ σガ∽ ≦ 0 . Q.E.D.18)The proof is;

耕 =挙等 =競

・

2働

蔦n e g a t t t e d n c e ギ

+ αブ

σ

″> ギ 十( ―σ

″/ σ

ぢ

2 ) σ

″> O a s b n g a s t h e c O u n t e r

investment stays interior(1.e.o<αブ<― σり/σ方2). Q.E.D.

19)The first order derivative,

∂

α

す

(α

ブ

)= ― σ7ヴ十σ

み

(ギ十α

ブ

σ

″)2

∂αブる

最

舗i 軍

予

∂

, 臀

盤。

∬涯

還

昆[ 筈

↓

縦

⇔

σ

フ

ギ> 甥

> 仇

号

す

を

;塑

土

=-2σ

ヶ

is negative for σ″<0.156 The Hikone Ronso No.330

αi

一σij/σ

?

一σi j / σ

? αj

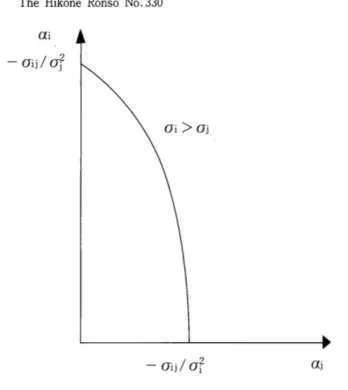

Figure 5:Firrn i's Reaction Function

becomes larger as qブ lncreases. At the other boundary solution, α ヶ=O wh― e n ギ = 一 σぢブ/ σ7 , a n d t h e r i s k p r e m i u m t t t h e l a r g e s t a t サ九夕σ7,Which is the same as the equlllbrium risk prernium under models l-1, 1-2, and 2 - 1 .

A Nash equllbrium to ths second stage game tt a pttr(α け,ギ )WhCh lies on both best reply functions. Interestingly, the best reply functions in this bilateral model coincide, which means that we have continuum of

equllibria. This result does not require the irms to be symrnetric, that is, o「l and σ 2 Can differ. This phenomenon is due to our specinc utility func― tion, which generates a certainty equivalent income in a mean_variance form. Other types of utility function may produce a unique solution to this st― age. Because of the existence of multiple equilibria, we have to irnpose an

additional assumption tO Before doing sO, let section:

solve the irst stage.

us deine a functiOn,ヵ

,aS we

did in the previOusThtt funchOn ttways takes a non_negative vttue fOr α

tt andげ

∈(0,1),

dnce σ

′+2∽α歩

十ギα歩

2=(σ

ぢ

_のαけ)2+2α

け

(∽十σ

づ

α

舟≧0,(1-α

;

げ)2≧

O and角

≧0.Using this functiOn,the risk premium becomes九

タ

ル/2.

The First Stage

ln order tO solve the first stage, we need to select an equilibrium tO the secOnd stage game.Let us assume firms are symmetric(1.e.σ ガ=∽ )

and select a symmetric equilibrium fOr the second stage game(1.e.α

け=

ぢ)・

The sharehdders andcipate ths equn拘

五um.From equadon 18,such

investment choice fOr manager づ

is

i f - 1 < σ″ < o . σづの

T h e c o n s t r a i n t o n αゥa n d αブb i n d s i f σ″/ σづc ヮ≧ 0 0 r σク/ σづ9 = 一

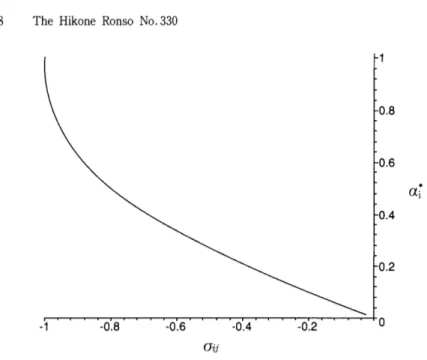

1. Figure 6 shows the syrnrnetric equilibriunl investrnent as a functiOn Of t h e c o v a r i a n c e , σぢぁ w h e n σづ= 9 = 1 .

The力 function under this symmetric equilibrium is

ガ =

It is irnportant to note that the risk prerniunl in this case lies between the risk prenllums in mode1 2-2 and in models l-1, 1_2, and 2-1:

考 イ 軟 1-石 み )≦琴 ガ ≦サ イ ヴ ・ Qの Shareholder づ's expected payoff is

( 1 - ん

―q わ( θ

; ―物) 十

命 づ

.

+2σ″α;十σ7α;2)

(1-α;ヴ)2

The Hikone Ronso No。 330

∽

Figure 6:α;as Function of σ″ at Symmetric Equilibrium:Bllateral Model Remembering pづ=θ づ― 物 and θ)=ん 竹om the second stage,the sharehold― eゴs expected payoff can be simplined t。(1-ん )(九ぁ― 物づ).The participa― tion constraint in the first stage is

掬―

が物―

シ ー

l y 毛

げ

≧

仇

Assunling a binding participation constraint, we can derive a reduced form of the shareholder's maxilnization problem silnilar to the one in mode1 2_2(equation ll).The solution is

ガ = 句= キ

・

20) The second order condition is satisied. it is easy to ind that the optimal ttt is

1201

As before, applying the chain rule, decreasing in the manager's degree 2 0 ) T h e s e c O n d o r d e r c o n d i t i o n , - 1 - メデ, i S n e g a t i v e f o r t h e d o m a i n s i n c e メデi S p o s i t i V e

\

with investment(mode1 2-2) Wi

bilateral investment model without model(mOdel l-2)

F i g u r e 7 : 切i a s F u n c t i o n o f γl i C o m p a r i s o n ( w h e n σl = σ2 = l a n d σ1 2 = 0 . 8 )

of risk averslon, ?んち and the degree of risk, σ ら while increasing in the covariance, 効 .The equilibriurn level of effort is lower than in the unllateral investment model with outside investment, but higher than in the model

without the investrnent opportunity. This can be easily proved because γ ゥ σ夕( 1 - σみ/ σ7 6 サ) ≦メデ≦ 角σ夕f r o m e q u a t i o n 1 9 .

The optimal wage is ガ = 0

Figure 7 shows the optilnal wages as a function of the manager's degree of risk averslon,for models l-2,2-2,and the bilateral investment model(

d e f i n i n g ( め, ブ) = ( 1 , 2 ) ) , w h e n σl = σ2 = l a n d σ1 2 = 0 . 8 . N o t e t h a t t h e relative position of the functions totally changes depending on the paramet― ers. For example, the function for mode1 2-2 can be located to the left of the function for model l-2 if l σ121 iS Small.

The Hikone Ronso No。 330

H 凋

=

122)In Figure 4, this shareholder's expected payoff is depicted as a function of角 (づ=1).It lies between the upper and lower lines,which,respectively, represents the expected payott with the investrnent opportunity(mode1 2-2),and without it(model l-1,1-2,and 2-1).This is,again,simply because

角σ

, ( 1 - σ

み

/ σ

? q つ

≦メデ三角σ7 f r o m e q u a t i o n 1 9 . H e n c e i t i s t r u e f o r a n y

value of parameters, σ づ, qブ and σ り, as long as the parameters keep the solution interior.

More generally,even if irms are not symmetric(1.e.σ ,半 αか and the anticipated equllibrium investment choices are not symmetric(1.e.αづ半 αブ), the expected payoff for both shareholders is bounded by the two lines in

igure 4 as bng as the somdonぉ

htttor.Ths為

Ob宙

ous shce tt σ

夕

(1-乾/σ7ギ)≦力≦角σ7血 gener劇

.

To conclude, shareholders benefit fronl the introduction of stOck invest配 1-ent opportunity even if the managers and shareholders of the two companies strategically choose their own variables. The shareholder's beneit, howev― er, is less compared to the situation where the investrnent is single sided. This is because, when it is mutual, the risk reduction effect of the stOck investment dechnes. As a consequence, in order to obtain the participation of managers who face a greater uncertainty, the shareholders must weak― en the link between the company's performance and managerial reward. The existence of outside investrnent opportunity itself, however, should still benefit the shareholders because such investment reduces the risk preHllum. We must also bear in Hlind that this happens only when the

4. Conclutting Remarks

The models presented in this paper combine the agency problem、 vith the risk_sharing argument for cOrporate shareholding. They are different

frorn Aoki's model in many respects. First, Operating pronts depend not on― ly on stOchastic events,but also on the level of effort which is endOgenous― ly deterrnined by managers, given the incentive contract. Secondly, investrll― ent decislons are also made non― cooperatively in each firm. Unlike Aoki's swap model, the investrnent does not have tO be reciprocal. Lastly, but most importantly, the degree of managerial reward's hnk to the company's performance, as well as a ix wage, are endogenously deterHlined by the shareholders, while these factors are not in Aoki's model.

With a unllateral investlnent rllodel,we ind that if rnanager's degree of risk aversion is small, shareholders offer high work incentives with a negative wage to the manager. In the extreme, if a manager is risk_neutral, the manager becomes the residual clairnant and pays a high “ franchise fee" ( 1 . e . n e g a t i v e w a g e ) t o t h e s h a r e h o l d e r . F o r m a n a g e r s w i t h a m e d i u m degree of risk aversiOn, shareh01ders lower the rate of managerial reward which is linked to the firnl's performance, and may have to pay a positive nxed wage to keep the managers in the cOmpany. If managers are highly risk averse, shareholders lower the link tO the performance further. The risk prenllum remains high because the managers are highly risk averse,

but is not so high because the managerial reward is linked 、 veakly to the performance of the company. Hence the wage dOes not have to be so high

to keep the managers in the company. With such factOrs serving to lower incentive, the pront of the company with highly risk averse managers is low.

162 The Hikone Ronso No.330

( 1 ) t h e m a n a g e r i s r i s k a v e r s e , ( 2 ) h e r m a n a g e r i a l r e w a r d i s l i n k e d w i t h the value of the irrn she manages,and 13)the operating pronts of invest―

ing and invested companies is negatively correlated. Corporate investlnent

is larger if the invested company's operating pront is iess volatile and/or if the covariance in the operating profits of the companies is more strong― ly negative.

With the bilateral investrnent decislon model, we nnd― 一一一in additlon to the above results― 一一一that corporate investrnent tends to be larger if

the investing company's operating profit is less volatile and/or if there is less counter investrnent froHl the invested firln to the investing irm. We also ind that shareholders' payoffs are lo、ver than in the unilateral investrn― ent model, because the mutuality of investment reduces the risk reduction effect of stock investrnent in the bilateral investrnent model.

The relevance of these outcomes to the existing empirical literature is as follows.

A c c o r d i n g t o K a p l a n ( 1 9 9 4 ) , m a n a g e r i a l c o m p e n s a t i o n i n m a n y c o m p a n i e s in Japan and the United States is linked more strongly to overall perforln― ance measures such as the rate of return on total assets or stock returns

than to sales―performance measures such as the growth rate of sales. Our models in this paper provide an explanation why the incentive contract is more likely to be based on overall performance which includes investrnent income, rather than sales performance which does not. The risk― sharing argument says that corporate shareholding reduces the risk borne by

managers compared to the case where no corporate shareholding is allowed. In our model, this benefits shareholders who extract all the rents from the managers. As we have seen, for this to happen, the perfomance paym― ent must be based on the value of the irm rather than operating profit. If shareholders choose the operating― pront―based payment scheme instead,

they must offer lower work incentives to managers and end up receiving lower payoffs.

Another rarnincation of our theoretical model is that companies with corporate stock investrllents exhibit lower but less volatile profits after dividends than companies without them. A positive investment is an indica一 tion of risk―averse managers. The more risk_averse are the managers, the equllibriunl level of effort, and hence the profit, is lower. Profits after dividends are less volatile in the irms with stock investment. In summary, compared to other arguments for corporate shareholding, our risk sharing model provides a more consistent explanatiOn for the styhzed facts that companies which are more involved in inter_corporate shareholding exhibit lower but less volatile profit rates measured by return on assets.

Finally, using panel data of 186」 apanese cOrporate grOup irms from 1980 to 1988,Nakano(1999)tests predictions drawn from the three maiOr arguments for corporate shareholding, including the risk_sharing argument. The study finds a weaker evidence to support the risk_sharing argument: Fiィms with less risky operating profits tend tO attract more investrnent, but the relationship between investrnent and the covariance in the firms' operating prOits is ambiguous. This possibly suggests that firms dO not efficiently use informatiOns on the riskiness of cOmpanies when making stock investment decislons.See Nakano(1999)for more detall.

RefererLces

[ 1 ] A o k i , M . ( 1 9 8 8 1 , 多ヵ 物めけづ9 ろ 肱 ∽ けわら a 初 駒 竹a 仇ケ7り物 け物 」のαt t S θ比 例切 7 , Cattbridgei Cambridge University Press.

[2] Bergibf,E.and E.Perotti(1994),“ The Governance Structure of the」apanese

Financial K夕 を竹 けs切!"。わ切物 aι げ 見 物αttCづαι』Cοttοη物づCS,36,259-284.

[3] Caves,R.E.and MI.Uekusa(1976),れ αttsけ克aι Oィθa物後aけづο物 あ%」 Opa物 ,Washington: DoC.,Brookings lnstitution,

164 The Hikone Ronso No.330

[4] Flath, D。 (1989), “Vertical lntegration by MIeans of Shareholding lnteriocks," r物 けθttaけ ぅοttaι 」 θ切 物 ι げ rttα ttsけ 克 aι Otta物 後 aけ あο句 ,7,369-380.

[5] Flath,D。 (1991),“ヽVhen is it rational for firms to acquire silent interests in rivals?," 助 けθttaけづοttaι」θ切物 aι QF妥乃冴循 け克aι Oィ9α物後αけウο物,9,573-583.

[6]Ito,T.and T.Hoshi(1992),“ Kigyo Gurupu Kessoku― do no Bunseki lAnalysis on the Degree of lntegration in Corporate Groups),"Horiuchi and Yoshino ed.,Cθ 物冴aあ ハ「うん0物 物ο拘 物グ切物 β切物sθ乃を,Tokyo:University of Tokyo Press.

[7]Kaplan,S.N。 (1994),“Top Executive Rewards and Firm Perfol■ lance:A Comparison

Of Japan and the United States,"」 θ切物 aι lア Pο ιづけ,caι Ecottο 物 7, 102,3,510-546.

[8]Korea Economic Planing Board lvariOus years),【 b9匂asけaけ体けあcaι予物aγboοん。 ‐ [9]Lincoln,」 .,M.Gerlach,and C.Ahmadiian(1996),“ Keiretsu Networks and Corporate

Performance in」 apan,"ム竹みθれcatt SOθぢοιOθづca↓妃ιυあθ切,61,67-88,

[10]Nakano,K。 (19991,“Corporate Shareholding in」apan「 Ph.D.dissertation,Universi― ty of British Coluttbia,

[11]Nakatani,I。 (1984),“The Economic Role of Financial Corporate Groupingr in M. Aoki(ed.),けんθ βcοttο9物をCム 物aιυsぢso/け んθしねpattθsθ Fづ― ,North―Holland. [12] Nihon Ginko(Bank Of」 apan),ス珍後のう何οんθぢ'Vθttpo lAnnual Economic Statistics

Report),Tokyo:Nihon Ginko Tokei Kyoku.

[13] Osano, H。 (1996), “IntercOrporate Shareholding and Corporate Control in the

」apanese firln,"Jθ 切竹降αι げ βa物 んウ物oα 物溺 Fあ物αttcθ,20, 1047-1068.

[14]Perotti,E。 (1992),`Cross―oWnerShip as a Hostage Exchange to Support Collabora― tion,"財 o%99θttaι attα Dθcあsづο物 ゴcοttο竹みあCS, 13,45-54.

[15]Reitman,D.(1994),“ Partia1 0wnership Arrangements and the Potential for Collu― slonギ 乃 切物 aιげ ЙぅαttSけ克aι EcOttο物づcs,42,313-322.

[16] Reynolds,R.and Bo Snapp(1986),“ The Competitive Effects of Partial EQuity lnterests and」 oint Ventures,"r物 けθttaけづοttaι JO切竹%aι げ rttαttsけγうoι Oィσa物ウ″aけぢο句, 4, 141-153.

[17] Tanigawa,Y。 (1986), “On帥 【utual Share Holding by Corporations,"Jcο %ο竹みあc Sけ物αあθs O切oγけθγι7,37,4,319-335.