These results suggest that the exit of the elderly from the labor force has no effect on job creation for the young. The calculation of the fixed benefit (ie the "basic pension benefit") is identical to that in the NPI. Shimizutani (2012) reveals the discouraging effect of the earnings test on labor supply decisions for workers aged 60–64.

Third, the disability pension program – which is not specific to the old-age pensions described above – covers some elderly people in Japan. We then need to "weight" the proportion of each path; this step is essential for calculating the OV and for determining the ways in which we can average the values along these paths. 6 There are two options for “stock estimator”. One is the "age-specific flow" (ie the proportion of workers at each age who enter the workforce at that age).

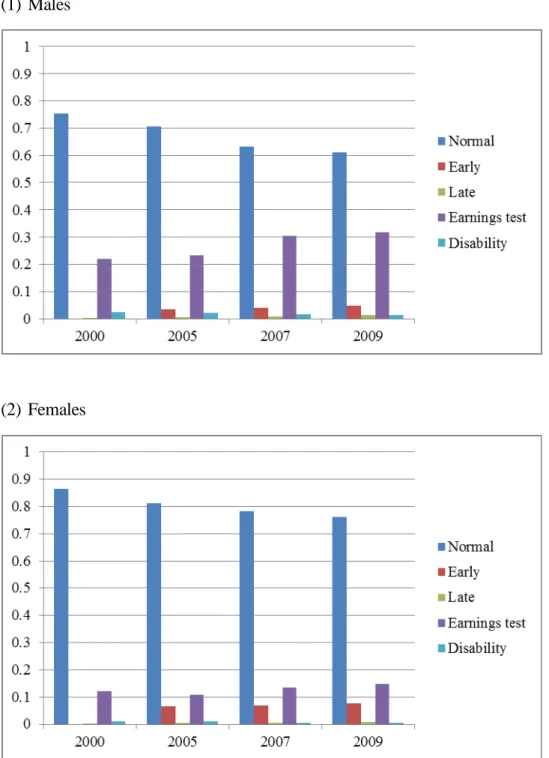

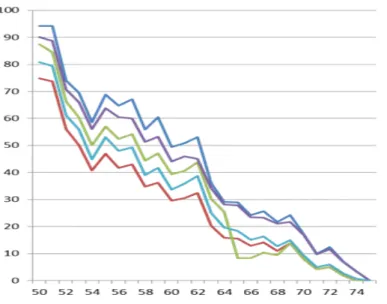

Another is the "aggregate flow" (ie, the share of workers starting at an initial age who eventually enter a path at any point). The top panel shows that the most dominant path to retirement for men is "Normal Claim", the proportion of which has seen a slight downward trend to 60% in recent years. The proportion of females under "Early claim" is greater than that for males, but it still constitutes a small part of the sample; the same applies to "Late claiming" and.

In the case of the EPI/MAI group, a highly educated claimant is more likely to claim at the normal eligibility age than a less educated claimant; this applies to both men and women.

Data description

Option value and health status

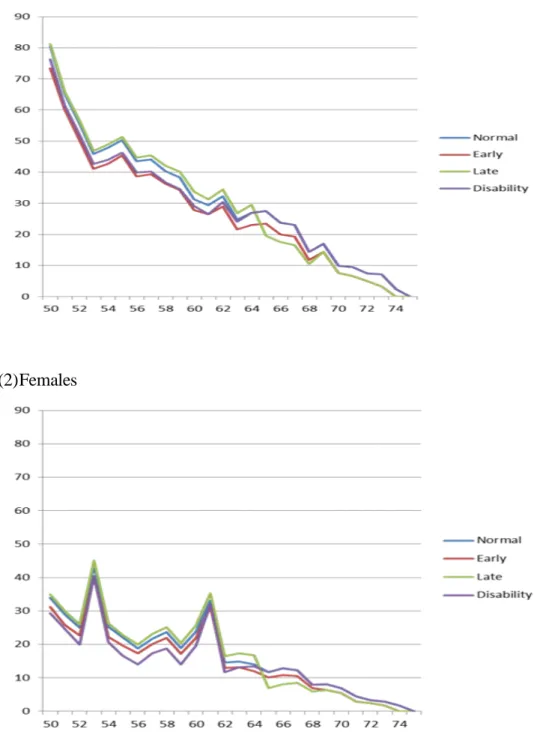

K has a value of 1–5 for the EPI/MAI beneficiaries and a value of 1–4 for the NPI beneficiaries. The most important components of the OV calculation are y(s), the labor income until retirement, and Brk(s), the pension income between retirement and death. First, we obtain the observed median earnings at each age (50–75 years) by gender and pension group (NPI or EPI/MAI); these are available from the JSTAR first wave data.

Third, we calculate the earnings projection for those under 50 or over 75, as wages are not observed in the JSTAR data. For simplicity, we assume that wages among people under 50 are the same as at 50, which means a flat earnings profile. Firstly, pension membership - ie. regardless of whether an individual belongs to the EPI/MAI group or the NPI group - available in the JSTAR data.

Second, the years of premium contributions are also available in the JSTAR data, and this is required for. Third, the career average monthly wage (CAMW) - the average pre-retirement labor income, which serves as the basis of the wage-proportional benefit - is estimated via the earnings projection, as explained above. We set the value of γ, the parameter of risk aversion, and κ, the parameter of labor disutility, equal to 1; we also set β, the discount rate, to 0.97.

The differences between EPI/MAI and NPI groups are (1) levels of OVs are generally higher for the former, (2) gaps between subgroups are smaller for the latter, and (3) the "Disability" group enjoys higher OVs beyond the mid-60s, but only in the latter case. The idea of this approach is to construct a simple index that depends on the first principal component of many health indicators. We use the first principal component of the 22 health indicators included in JSTAR, and the data consist of those collected from the first and second waves.7 The top panel of Appendix Table 1 reports the loadings on each health indicator; we use the variable as a continuous variable.

The bottom panel of Table 1 in the Appendix shows the percentile cutoffs for each gender quintile in the first and second waves. It is interesting that the threshold values for the transition from the first to the second quintile increased in 2009, while those for other transitions were lower in 2009; Deterioration in health due to aging is also evident in Figure 1 in the Appendix, which shows that the proportion of the fifth quintile (best health status) decreases with age, strengthening the rationale for using the health index and quintile.

Regression results and policy simulations

Regression results

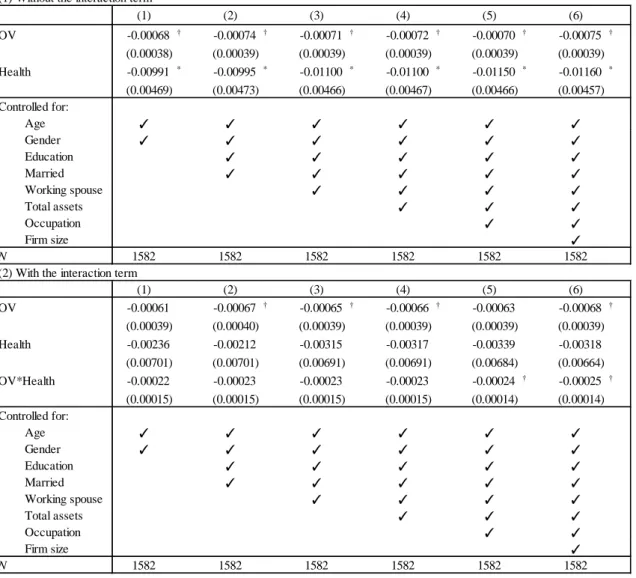

The dependent variable is an indicator that takes a value of 1 if individuals retired in 2009, and 0 otherwise. OVi, 2007, the main variable, is the OV for individual i, calculated according to the method described in the previous section . If healthier individuals are more sensitive to the OV, we should derive a negative coefficient for the term OV*Health.

For all models with different sets of control variables, we see a similar pattern in the OV and Health coefficients. An individual with a larger OV or better health status in 2007 is less likely to retire in 2009, after controlling for a number of household characteristics. 8 Some data are missing for each variable; this is especially true for total assets.

We impute the variable by assigning its mean value to those who have attributes similar to those of the respondent. The OV coefficients drop slightly compared to the levels in the upper panel, but remain significant at the 10% level. Meanwhile, the coefficients of the interaction term between OV and Health are all negative and significant at the 10% level for models (5) and (6), each of which includes a rich set of control variables.

Policy simulation

Upon closer examination, we find that the pension distribution shifts to the right when the weight on the disability course is raised to 20%, suggesting that a more generous early retirement will discourage people from staying in the workforce. Meanwhile, we see that a 10% cut in pension benefits will have only a negligible impact on the probability distribution of retirement.

Conclusion

The value of OV depends on the utility function parameters, such as the income-to-utility conversion parameters and the discount rate, all of which are conditionally assumed in the current study. Second, they should more accurately project wage profiles and capture different paths to retirement based on further information obtained from official statistical sources. Third, we should also model couples rather than individuals, since retirement decisions are likely to be made jointly by older couples: we should therefore include information on spouses' and survivors' pensions, which are ignored in this study.

This study used micro data collected by the Japan Study on Aging and Retirement (JSTAR), which was conducted by the Research Institute of Economics, Trade and Industry (RIETI) and Hitotsubashi University in 2007 and 2009. Social security programs and retirement around the World: The Relation to Youth Employment, Chicago: University of Chicago Press. Social Security and Retirement in Japan: An Assessment Using Micro-Data', in Jonathan Gruber and David Wise, eds.

Social Security Reforms and Labor Force Participation of the Elderly in Japan,” Japanese Economic Review, vol. Disability Pension Program and Labor Force Participation in Japan: A Historical Perspective,” in David Wise, ed. Social Security Programs and Retirement Around the World: Historical Trends in Death and Health, Employment, and Disability Insurance Participation and Reforms, University of Chicago Press, forthcoming.

Does social security lead to older people withdrawing from the labor force and creating jobs for young people? Programs and Retirement around the World: The Relationship to Youth Employment, Chicago: University of Chicago Press, pp. Social Security Earnings Test and the Labor Supply of the Elderly: New Evidence from Unique Survey Responses in Japan”, Japanese Economic Review, forthcoming.

The Labor Supply Effect of the Social Security Earnings Test Revisited: New Evidence from Its Elimination and Revival in Japan." Debate Paper No. New Evidence on Initial Transition from Career Jobs to Retirement in Japan," Industrial Relations vol. Invoking Behavior in Public Retirement Benefits: New Evidence from Japanese Study on Aging and Retirement (JSTAR)".

The Pension Inducement to Retire,” in David Wise, ed., Issues in the Economics of Aging, Chicago: University of Chicago Press,. Historical Trends in Mortality and Health, Employment and Disability Insurance Participation and Reforms, Chicago: University of Chicago Press, forthcoming.