I NDUSl'RIAL CHARACTERISTICS OF MANUFACTURER'S SALES COMPANY I N JAPAN

bY Hiroaki Seto

1. DEFINITrON OF MANUFACTURER'S SALES COMPANY1

Manufacturer's s a l e s company is a phenomenon peculiar t o Japanese economy a f t e r World War

J Iand contributed t o t h e economic growth i n t h e 1960s. We have, however, nothing but some case studies of t h i s subject so f a r . We have, therefore, t o s t a r t with t h e d e f i n i t i o n of manufacturer's saJ.es company (being abbreviated t o MSC).

Definition and cZassificatSon

MSC i s defined as follows: s a l e s company incorporated by manufac- t u r e r with i t s own c a p i t a l f o r t h e purpose t h a t t h e l a t t e r s e l l s i t s product through t h e fornor i n the domestic market.

The c l a s s i f i c a t i o n of stratum i s defined a s follows:

1. Exclusively dealing with a l l o r almost a l l products manufac- tured by i t s parent company (e.g., Toyota Motor - Toyots. Motor Sales).

Covering t h e whole Japan. Most of t h e sample points i n h i s stratum assume t h e self-sustaining form of t h e s a l e s division of p a e n t company.

I use "manufacturer" and "wholesaler" i n t h e a b s t r a c t . "Manu-

facturer" means an individual form of i n d u s t r i a l c a p i t a l and "whole-

saler" means an individual form of commercial c a p i t a l . It would be more

adequate t o use the word "manufacturing capital" o r "wholesaling capital".

2.

Exclusively dealing with a l l qr almost a l l products manufac- t u r e d by t h e d i v i s i o n of t h e parent company (e.g., TokyoSShibaura E l e c t r i c - Toshiba t r a d i n g ( e x c l u s i v e l y d e a l i n g with household e l e c t r i - c a l apparatus manufactured by t h e d i v i s i o n i n t h e parent company), Hita- c h i (manufacturing every kind o f e l e c t r i c a l machinery a s well a s Tokyo.- Shibaura E l e c t r i c ) - Hitachi Household E l e c t r i c a l Apparatus ( e x c l u s i v e l y d e a l i n g with household e l e c t r i c a l apparatus manufactured by t h e d i v i s i o n i n t h e parent company)) . Covering t h e whole Japan.

3. Local ( t e r r i t o r i a l ) MSC ( p r e f e c t u r a l o r sub-prefectural) . They

covers t h e whole Japan, though i n d i v i d u a l firms cover a p r e f e c t u r e o r smaller d i s t r i c t than it.

4. MSC a t s p e c i a l d i s t r i c t s ( s t r a t e g i c p o i n t s i n many c a s e s ) . 5

5-1. Dealing with a p a r t of t h e parent company's products. Cover- i n g t h e whole Japan.

5-2.

A s t h e same l e v e l a s a g e n t .

G

5-3, As t h e same l e v e l a s general t r a d i n g company (such a s Mitsui

&

Co. o r Mitsubishi S h o j i Kaisha) .

5-4.

Others.

MSC and Local MSG

Most of t h e manufacturers which own MSC a r e b i g businesses and a r e

o f t e n o l i g o p o l i s t i c i n t h e i r i n d u s t r i e s . Converses a r e not always t r u e .

We have had enough experience t o explain t h i s . One h a l f of automobile

manufacturers and household e l e c t r i c a l apparatus manufacturers own no

535 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -251- SALES COMPANY IN JAPAN

MSC i n our sense r e s p e c t i v e l y , though a l l t h e manufacturers belonging t o t h e s e i n d u s t r i e s have l o c a l MSC.

REMARK The reason why t h e r e s i d u a l h a l f own no MSC could be ex- p l a i n e d by two f a c t o r s : Turnover of c i r c u l a t i n g c a p i t a l and organiza- t i o n a l problems. Some of manufacturers can recover t h a t c i r c u l a t i n g c a p i t a l a s quickly a s a cash l i q u i d a t i o n . Some of them c a s t doubt on an a s s e r t i o n t h a t t h e advantages derived from independent MSC f a r out- weight t h e disadvantages which t h e y e n t a i l . These disadvantages may d e r i v e from o r g a n i z a t i o n a l problems.

Local MSC a c q u i r e s and e x p l o i t s new markets and h e l p s t h e i n c r e a s e

of a market s h a r e , i n s h o r t , marketing. Consequently MSC i s t o d i s -

charge another f u n c t i o n : MSC f u l f i l s i t s f u n c t i o n a s commercial c a p i t a l ,

t h a t i s , wholesaler. The r e a d e r could understand such a s i t u a t i o n from

marketing channel ( s e c t i o n 4

)2 . METHOD OF LIQUIDATION BETWEEN PARENT AND MSC

Commercial capital has a double function to perform for industrial capital: as sales agent and as financier. It sells or markets manu- factured products as the former, while buys them from industrial capi- tal on its own account as the latter, in other words, invests circulat- ing capital in its business. (It is to be noted that a manufacturer's sales division can properly fulfil its function as sales agent.) If industrial capital excludes commercial capital from sales agency and sells on its own account, the advantage resulting from commercial capi- tal's activities as financier is counterbalanced. If manufacturers can exclude their wholesalers without offsetting the advantage, it is pref- erable for it. The role is allotted to MSC. These have been consider- ed by another paper of my own El].

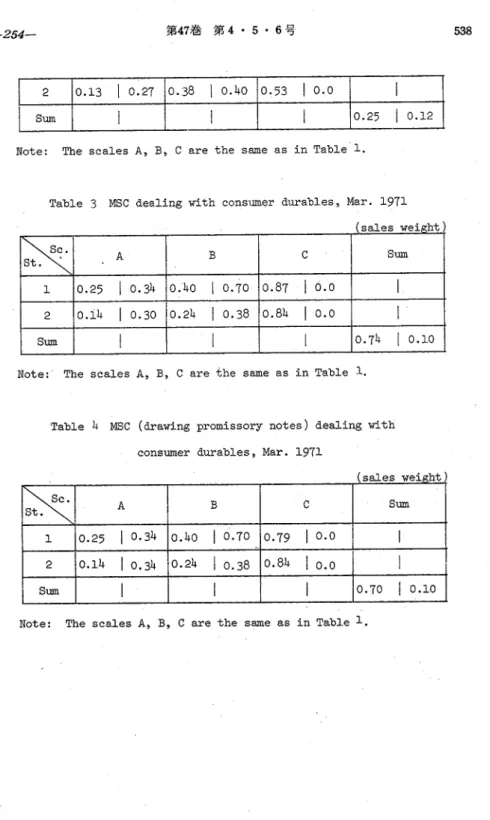

Predominant status of industries manufacturing consumer durabZes The proportion of the manufacturers of consumer durables of which MSC stand as financier to all the manufacturers owning MSC is 0.74 in

sales weight a able 3 ) , and the proportion of the manufacturers of con- sumer durables of promissory note liquidation of which MSC stand as financier is 0.70 to all the manufacturers owning MSC in sales weight ( Table 4). The recovery time of circulating capital in industries manu- facturing consumer durables is to be much longer than that of the others, because instalment selling is prevailing in these industries.

MSC will be thus found advantageous to these industries.

REMARK The turnover period is the mean recovery time. Circulat-

537 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -253- SALES COMPANY IN JAPAN

ing capital is represented by accounts

¬es receivable or current assets.

A parent manufacturer - a MSC owner - can quickly recover his capital invested in a production process with profit on a great scale at a time, with regularity and at the will of his

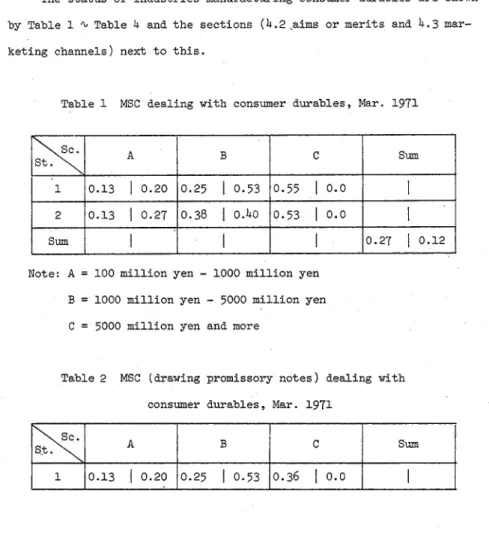

own.The status of industries manufacturing consumer durables are shown by Table 1

aTable 4 and the sections (4.2 ,aims or merits and 4.3 mar- keting channels) next to this.

Table 1 MSC dealing with consumer durables, Mar. 1971

Note: A = 100 million yen - 1000 million yen B = 1000 million yen - 5000 million yen C = 5000 million yen and more

Table 2 MSC (drawing promissory notes) dealing with consumer durables, Mar. 1971

C

0.55 1 0.0

0.53 1 0.0 I

B 0.25 1 0.53

0.38 1 0.40 I

A Sum

I I

0.27 1 0.12

'1 2 Sum

0.13 1 0.20

0.13 1 0.27 I

1

A 0.13 1 0.20

B 0.25 1 0.53

C 0.36 1 0.0

Sum I

I

0.25 1 0.12

Note: The s c a l e s A , B, C a r e t h e same a s i n Table 1. 7

Table 3 MSC d e a l i n g with consumer d u r a b l e s , Mar. 1971

Note: The s c a l e s A, B, C a r e t h e same a s i n Table 1.

( s a l e s weight )

Table 4 MSC (drawing promissory n o t e s ) d e a l i n g w i t h consumer d u r a b l e s , Mar. 1971

Sum

I I

0.74 1 0.10

Note: The s c a l e s A, B, C a r e t h e same a s i n Table

C0.87 1 0.0 0.84 1 0.0

I

( s a l e s weight

)B

0.40 1 0.70 0.24 1 0.38

I

1 2 Sum

A 0.25 1 0.34 0.14 1 0.30

I

Sum

I

I

0.70 1 0.10 C

0.79 1 0.0

0.84 1 0.0

I

B 0.40 1 0.70

0.24 1 0.38

I

1 2 sum

A 0.25 1 0.34 0.14 1 0.34

I

539 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -255- SALES COMPANY IN JAPAN

3. AIMS OR MERITS

Aims of incorporation of MSC are various and complicated. But we can distinguish a group of drawing MSC's promissory notes from another group of endorsed notes by MSC (this group includes a cash liquidation).

But it is not so much to be distinguished as indistinguishable whether it is an aim or a merit.

Aims of MSC are as follows:

a . Accelerating the turnover of parent's circulating capital (as MSC receives products from parent manufacturer, it draws a promis- sory note in the parent. MSC fulfils its function as financier. MSC fulfils also its function as sales agent for parent's products. MSC

/

has a double function to perform.

b . Spokesman of dealers to parent manufacturer and spokesman of the

parent to dealers. MSC has also the double function to perfom.

C.

A marketing channel for a new established productive division different from that of already established divisio?s. Many of sample points belonging to stratum 2 are regarded as so.

d,e. Keeping marketing channel for parent. It is characteristic of MSC belonging to this term that weak wholesalers were participated by manufacturer to keep the marketing channel which the wholesalers had held. Two kinds of such wholesalers exist as d) financier or e) not so.

f. Apparent discrimination between responsibilities of productive and sales division.

9 .

Price policy, price leadership.

h. Reconciliation of profit. MSC behaves so that it might reconcile parent's Profit

&Loss.

The following two terms are not aims but functions some of the sample points belonging to the above terms.

Z. Controlling local MSC. Automobile and household electrical apparatus industries are classified into this term.

j. Joint MSC. Two or more manufacturers jointly possess sales company of their own. A few in a special kind of steel, petroleum and soap industries are classified into this term.

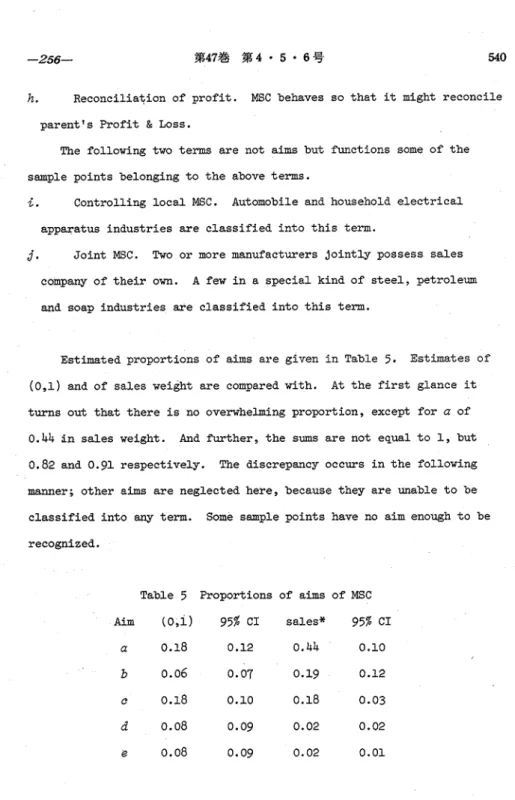

Estimated proportions of aims are given in Table 5. Estimates of (0,l) and of sales weight are compared with. At the first glance it turns out that there is no overwhelming proportion, except for a of 0.44 in sales weight. And further, the sums are not equal to 1, but 0.82 and 0.91 respectively. The discrepancy occurs in the following manner; other aims are neglected here, because they are unable to be classified into any term. Some sample points have no aim enough to be recognized.

Table 5 Proportions of aims of MSC Aim (0,l) 95% CI sales* 95% CI

a 0.18 0.12 0.44 0.10

b 0.06 0.07 0.19 0.12

c 0.18 0.10 0.18 0.03

d 0.08 0.09 0.02 0.02

e 0.08 0.09 0.02 0.01

541 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -257- SALES COMPANY IN JAPAN

Aim (0,l) 95% CI sales* 95% CI f 0.11 0.11 0.03 0.06 g 0.07 0.07 0.03 0.02

h 0.05 0.07 0.00 0.00

sum 0.82 0. 91

Note: * October 1970

Q,March 1971

Now, Table 5 shows that an estimated proportion of a is 0.18, b 0.06, c 0.18, d 0.08, e 0.08, f 0.11, g 0.07 and h 0.05 in (0,1), and then a 0.44, b 0.19, c 0.18, d 0.02, e 0.02, f 0.03, g 0.03 and h 0.00 in sales weight. The sum of a, b and c is 0.43 (0,l) and 0.81 (sales weight) respectively. It is an attribute of almost all of sample points belonging to a, b and c that the transaction between parent and MSC is liquidated by a promissory note drawn by MSC. This situation is

stated in comparison of Table 5 with Table 6. Table 6 showed propor- tions of aims about the group in which the transaction is liquidated by a promissory note drawn by MSC. In Table 6 the sum of a, b and c is 0.37 (0,l) and 0.79 (sales weight) respectively. The proportion of the promissory note liquidation a, b and c is 86%

(=0.37/0.43) (0,l) and

98% (= 0.79/0.81) (sales weight) respectively. This means that most of MSC incorporated to achieve aim a, b or c belong to the group of draw-

ing MSC's promissory note. It is to be noted that d, f and h do not

exist and e and g are negligibly small forthe sales-weighted propor-

t ion.

Table 6 Proportions of aims of the group in which the transaction is liquidated by the promissory note drawn by MSC

Aim or

merit 95% CI

a 0.18 0.12 0.44 0.10

b 0.06 0.07 0.17 0.12

'

merit a (including aim

a) 0.26 0.12 0.65 0.08

merit a ' 0.08 0.07 0.18 0.03 merit a or a '

(including aim

a) 0.34 0.14 0.83 0.07

Note: * October 1970 * March 1971

Merit a (including aim a) means a function or role to shorten the

turnover of circulating capital of parent is recognized as merit or

effect, whether it is an aim or not. MIrit a ' means that the emphasis

is laid on borrowing money by MSC, which results in shortening parent's

turnover period. i means a function or role to control local MSC and j

means joint MSC. An estimated proportion of merit a (including aim a)

is 0.26 (0~1) or 0.65 (sales weight), merit a ' 0.08 ( 0 , ~ ) or 0.18 (

sales weight), merit a or a ' (including aim a) 0.34 (0 $1) or 0.83 (

543 INDUSTRIAL CHARACTERISTICS OF MANUFACTURERS -259- SALES COMPANY IN JAPAN

s a l e s w e i g h t ) , i 0.08 ( 0 , l ) o r 0.63 ( s a l e s weight) and j 0.05 ( 0 , l ) o r 0.06 ( s a l e s weight) r e s p e c t i v e l y . A l a r g e d i f f e r e n c e between both estimated p r o p o r t i o n s of i i m p l i e s i n f l u e n t i a l s i t u a t i o n of automobile and household e l e c t r i c a l a p p a r a t u s i n d u s t r i e s i n t h e market where MSC e x i s t s , because t h e m a j o r i t y o f i belongs t o t h e s e i n d u s t r i e s . i

belongs t o s t r a t u m (1,C) o r ( 2 , ~ ) .

I n comparison of Table 6 o r 7 w i t h Table 10-2, it i s t o be noted t h a t t h e weight of a, b o r

Ci n t h e a t t r i b u t e group i n which t h e t r a n s a c t i o n i s l i q u i d a t e d by a promissory note drawn by MSC i s much more t h a n t h e weight of f , d o r h i n t h e a t t r i b u t e group where t h e t r a n s a c t i o n i s l i q u i d a t e d by an endorsed n o t e o r cash (Table 7 ) . The former i s equal t o 0.77 ( = 0.37/0.48) ( 0 , 1 ) , 0.90 (0.7910.88) ( s a l e s weight) and t h e l a t t e r i s equal t o 0.55 (= 0.22/0.40) ( 0 , 1 ) , D.56

(=

0.05/0.09) ( s a l e s w e i g h t ) .

Table 7 Proportions o f aims of t h e group i n which t h e t r a n s a c t i o n i s l i q u i d a t e d by endorsed n o t e s o r cash.

A i m ( 0 , l ) 95% CI s a l e s * 95% C I

b 0.0 0.0 0.0 0.0

c 0.03 0.05 0.0 0.01

d 0.08 0.09 0.02 0.02

e 0.03 0.05 0.01 0.01

f 0.09 0.10 0.03 0.06

g 0.03 0.05 0.01 0.03

h 0.05 0.07 0.00 0.00

Note: * October 1970

QMarch 1971

Table 8 Proportions of merits or roles of MSC sales*

Merit or role ((Id) 95% CI weight 95% CI merit a (including aim a) 0.29 0.13 0.65 0.08

merit a ' 0.13 0.09 0.21 0.03

merit a or a ' (including a) 0.42 0.15 - 0.86 0.07

i 0.09 0.02 0.65 0.10

j 0.13 0.10 0.08 0.10

Note: 1. * October 1970

%March 1971

2. The underlined values are alluded to in the text.

Table g Proportions of aims or merits of consumer durables industries sales*

Aim, merit, role (0,1) 95% CI weight 95% CI

a 0.11 0.09 0.39 0.06

b 0.04 0.05 0.16 0.12

C

0.08 0.23 0.07 0.17 0.72 0.03

merit a (including aim a) 0.15 0.10 0.53 0.10

merit a ' 0.08 0.07 0.20 0.03

merit a or a ' (including aim a) 0.24 0.12 0.74 0.10

i 0.07 0.01 - 0.64 0.10

Note: 1. * October 1970

.\,March 1971

2. The underlinged values are alluded to in the text.

Table 10 Proportions of aims or merits of the sample with

the promissory note drawn by MSC in addition to consumer durables

545 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -26.Z- SALES COMPANY IN ,JAPAN

Aim, merit sales*

(0,l) 95% CI weight 95% CI

a 0.11 0.09 0.39 0.06

b 0.03 0.05 0.13 0.12

C

0.08 0.22 0.07 0.17 20 0.03

merit a (including aim a) 0.15 0.10 0.53 0.10

merit a ' 0.07 0.07 0.17 0.03

merit a or a ' (including aim a) 0.22 0.12 - 0.70 0.10

Note: 1. * October 1970

cMarch 1971

2. The underlined values are alluded to in the text.

Let us consider, next, merit a, merit a or b and others of either the MSC1s promissory note liquidation or the endorsed note or cash liquidation, a, b, c, merit a and others of consumer durables and a, b, c, merit a and others of MSC's promissory note in addition to consumer durables in this order.

The situation of merit a or a ' (including a) among Table 8, 9 and

10 is as follows. The proportion of merit a or a ' (including a) is

0.42 (0,l) and 0.86 (sales weight) (Table 8) and then the proportion of

consumer durables in just above mentioned merit a or a ' is 57% ( =

0.24/0.42) or 86% ( = 0.74/0.86) respectively. This implies that merit

a or a ' is scattered not only in industries manufacturing consumer

durables, but also any other industries, though industries manufacturing

consumer durables contribute overwhelmingly to sales weight. Next, the

proportion of the promissory note liquidation in addition to consumer

durables in just mentioned merit a or a ' is 92%

( =0.22/0.24) or 95% (

= 0.70/0.74) respectively. Such a situation implies that almost all of the industries manufacturing consumer durables put merit a or a ' to a good use with liquidation by MSC's promissory note.

The situation of a, b and c between Table 9 and 10 is as follows.

The proportion of the sum of a, b or c of consumer durables is 0.23 ( 0,l) and 0.72 (sales weight) (Table 9) and then the proportion of con- sumer durables with MSC's promissory note in consumer durables is 96% (

= 0.22/0.23) and 96% (= 0.69/0.72) respectively. The situation of i between Table 8 and 9 is as follows. The proportion of i is 0.09 (0,l) and 0.65 (sales weight) (Table 8) and then the proportion of i of

industries manufacturing consumer durables in Just mentioned above role i

is 78% (= 0.07/0.09) (0,l) and 98% (= 0.6410.65) (sales weight) respec-

tively. j does not exist in industries manufacturing consumer durables,

but is 0.13 (0,l) and 0.08 (sales weight) in Table 8.

547 INDUSTRIAL CHARACTERISTICS OF MANUFACTURERS -263- SALES COMPANY IN JAPAN

4. MARKETING CHANNELS

The aim o r merit of MSC i s connected with i t s marketing channel.

Marketing channels a r e t a b u l a t e d i n Table 11. These channels given t h e r e a r e too simple f o r t h e reader t o understand r e a l channels i n a way a p p r o p r i a t e t o i t s e l f . But he w i l l roughly grasp a s i t u a t i o n i n i t s t o t a l i t y .

To channel 1 belongs mainly t h e camera and f i l m industry. I n t h i s i n d u s t r y two b i g firms had dominated t h e market channel, b u t o t h e r manufacturers t r i e d t o defend and e s t a b l i s h t h e i r own channels.

Furthermore, t h e d e c l i n e of t h e wholesaler i n t h i s market a s f i n a n c i e r f a c i l i t a t e d t h e i r p a r t i c i p a t i o n i n wholesaler c a p i t a l . The l i q u i d a t i o n by endorsed notes between parent manufacturer and MSC i s p r e v a i l i n g because of t h e weak f i n a n c i a l p o s i t i o n of MSC and perhaps o f r e l a t i v e l y

small c a p i t a l o f parent. Channel 1 i s connected with d of Table 7.

To channel 2 belongs t h e household e l e c t r i c a l apparatus industry.

This channel i s connected with merit a o r a' (including aim a ) and i of Table 6. The promissory note l i q u i d a t i o n p r e v a i l s i n t h i s induatry.

To channel 3 belongs t h e automobile industry. This channel i s connected with aim a and merit

a( i n c l u d i n g aim a). The promissory note l i q u i d a t i o n p r e v a i l s i n t h i s industry.

A t channel 4 government and l o c a l government And so on a r e u s e r s of MSC belonging t o t h e channel.

To channel 5 belongs t h e construction machinery i n d u s t r y and

others. An ideftl channel of t h i s i n d u s t r y i s t h e same a s t h e automobile

i n d u s t r y , t h a t i s , channel 3. Too much c a p i t a l i s necessary t o counter-

balance i n s t a b i l i t y o f t h e market and i n f e r i o r q u a l i t y of u s e r . It i s

not exact to call next to MSC a "retailer" in the case of construction machinery market. It is what is called a "dealer." The promissory note liquidation prevails in this industry. Other industries are various.

Cahnnel 5 is connected with aim a, c and merit a or b (including aim a ) of Table 6.

To channel 6 can be specified any particular industry of neither of drawing MSC1s promissory note nor endorsing note, but it is to be noted that the proportion (0,l) of this channel is large (showed below).

To channel 7 cannot be specified any particular industry. But the wholesaler of this channel is an independent commercial capital with much volume of capital.

Table 11 Marketing channels Participated W h o l e s a l e r

MSC Retailer - Consumer... 1

(agent

)Local MSC Retailer - Consumer -

2t Local MSC Consumer... 3

New 1 User ..- 4

incorporated

Retailer***- Consumer... 5 Local agent Retailer - Consumer.. 6

L - Local

wholesaler - Retailer - Consumer-.. 7 Note: 1. -- Camera and film

2. -- Household electrical apparatus 3. -- Automobile

5. -- Construction machinery

*** -- Dealing with product of higher price. Being nearer

549 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -265- SALES COMPANY IN .JAPAN

to Local MSC

Proportions of marketing channels are given in Table 12. The proportion of channel 1 is 0.15 (0,l) and 0.05 (sales weight) respec- tively, 0.05 (0,l) and 0.19 (sales weight) for 2, 0.06 (0,l) and 0.53 ( sales weight) for 3, 0.13 (0,l) and 0.02 (sales weight) for 4, 0.18 ( 0,l) and 0.08 (sales weight) for 5, 0.24 (0,l) and 0.05 (sales weight) for 6 and 0.05 (0,l) and 0.04 (sales weight) for 7.

Table 12 Proportions of marketing channels (sales*

(0,l) 95% CI 95% CI

Cha. 1 0.15 0.12 0.05 0.06 2 0.05 0.01 0.19 0.03 3 0.06 0.05 0.53 0.10

4 0.13 0.11 0.02 0.01

5 0.18 0.12 0.08 0.10

6 0.24 0.14 0.05 0.04

7 0.05 0.05 0.04 0.01 2 or 3 0.12 0.05 0.72

2 or 3 or 5 0.29 0.23 0.79

Note: 1. * October 1970 March 1971

5. INDUSTRIAL CHARACTERISTICS OF MSC

We have discussed the industrial characteristics of MSC from three points of view so fa. Methods of liquidation between parent and MSC, aims or merit and marketing c h a ~ e l s formulate the industrial charac- teristics of

MSG.5.1 Keeping the marketing channel for parent

It is characteristic of MSC belonging to this term that weak whole- salers were participated by manufacturer to keep the marketing channel which the wholesalers had held. The method of endorsed note liquida- tion prevails. We can find this type in the camera

&film industry.

The weight of this industry is given in Table 13 and 14. The bearing industry belongs to this type also.

Table 1 3 Camera

&film industry belonging to channel 1, Mar. 1971 Endorsement

Note: The scales A, B, C are the same as in Table 1.

Table 14 Camera

&film industry belonging to channel 1, Mar. 1971 Endorsement

A

. 1

2 sum

Sum

I I

0.08 I

B

0.0 I 0.0

0.13 1 0.27 I

0.13 1 0.20

0.0 ( 0.0

I

C -0.0 I 0.0

0.07 1 0.0

I

551 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -267- SALES COMPANY IN JAPAN

Note: The s c a l e s A, B, C a r e t h e same a s i n Table 1.

( s a l e s weight )

5.2 Differences among i n d u s t r i e s manufacturing consumer d u r a b l e s The common c h a r a c t e r i s t i c s i n i n d u s t r i e s manufacturing consumer durables displayed by t h e promissory n o t e l i q u i d a t i o n , t h e alm o r t h e m e r i t of MSC a s f i n a n c i e r and t h e channel - p a r e n t

-tMSC

-+l o c a l MSC

+consumers. But we can f i n d t h e d i f f e r e n c e , i f we observe i n d e t a i l . F i r s t t h e c o n s t r u c t i o n machinery i n d u s t r y i s d i f f e r e n t from t h e o t h e r s from t h e p o i n t of view of a ) t h e t u r n o v e r p e r i o d o f c i r c u l a t i n g c a p i t a l and b ) P r o f i t

&Loss, t h e n t h e automobile i n d u s t r y i n "sum

+r a t i o "

method c l e a r s t h e l a r g e s t p r o f i t i n a l l t h e i n d u s t r i e s manufacturing consumer d u r a b l e s , whereas it i n " r a t i o

-+sum" s u f f e r s a l o s s .

a ) The turnover p e r i o d of t h e c o n s t r u c t i o n machinery i n d u s t r y i n "sum

-t

r a t i o " method i s not d i f f e r e n t from t h e o t h e r s . The turnover period i n " r a t i o

-+sum" i s l a r g e r than t h e o t h e r s .

b ) P r o f i t b e f o r e t a x e s o f t h i s i n d u s t r y s u f f e r s a l o s s i n "sum

+r a t i o and " r a t i o

-+sum".

The c o n s t r u c t i o n machinery i n d u s t r y i s growing, b u t u n s t a b l e . Every automobile manufacturer i s not prosperous. A g r e a t d e a l of c a p i t a l i s necessary compared w i t h o t h e r i n d u s t r y . Small s c a l e c a p i t a l

Sum

I I

0.02 1 0.02

A

B

0.0 1 0.0 0.21 1 0.39

I

1 2 Sum

C 0.0 I 0.0 0.02 1 0.0

I

0.12 1 0.19

0.0 I 0.0

I

is disadvantageous.

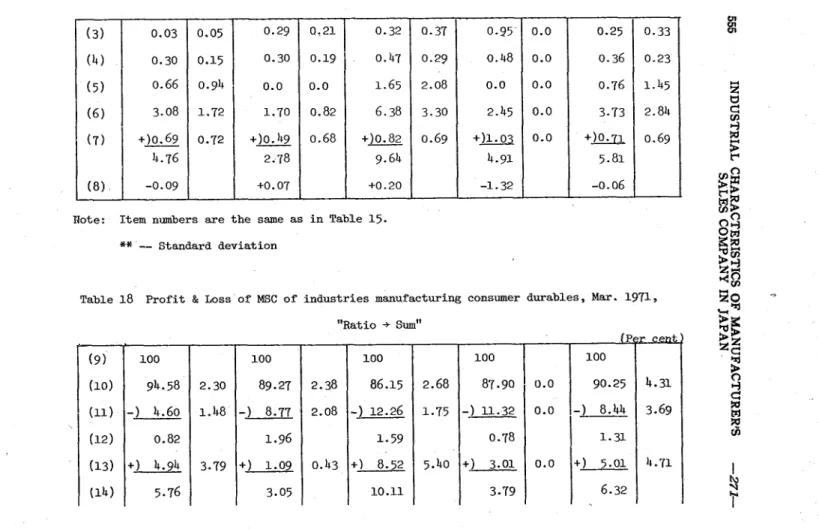

The characteristics are given by Table 15, 16, 17 and 18. The averages of five automobile, three household electrical apparatus, four construction machinery and one sash manufacturers are tabulated here.

There is no variance in "sum

+ratio", because we take all manufacturers considered for only one manufacturer in each industry. Weights of the household electrical apparatus industry and the automobile industry are given in Table 19 - 22.

Table 15 Turnover periods of industries manufacturing consumer durables, Mar. 1971, "Sum

+Ratio"

( m o n t h )

Note:

(1) (2)

(*I

(3)

(4)

(5)

(6) (7)

(8)

C average

14.95

- )8.12

(1.69) 6.83 0.20 0.29 0.59 3.77 +)0.43

5.35 1.48 A

average 6.24 -13.28 (0.75)

2 96

0.01 0.44 0.22 2.00

+u

3.00 -0.04

D average --.

7 68 -)4.09

(2.49) 3.59 0.95 0.48 0.0 2.45 +-

4.91 -1.32 B

average 7.53 -)4.43

(1.00 ) 3.10 0.25 0.36 0.0 2.19

+m

3.35 -0.25

\

- - - - - --

- Sum average

6.79

-13.69 (0.86)

3.10 0.10 0.42 0.16 2.10 +=

3.19

-0.09

553 INDUSTRIAL CHARACTERISI'ICS OF MANUFACTURER'S -269- SALES COMPANY I F JAPAN

( 1 )

K C ' S turnover period of current a s s e t s (including notes receiv- a b l e discouhted by bank)

( 2 ) P a r e n t ' s turnover period of accounts

¬es r e c e i v a b l e (drawn by MSC) t o MSC (including notes r e c e i v a b l e (drawn by MSC) d i s - counted by bank)

( 8 )

P a r e n t ' s turnover period of notes r e c e i v a b l e (drawn by MSC) d i s - counted by bank

( 3 ) MSC's turnover period of notes r e c e i v a b l e discounted by bank ( 4 ) MSC1s turnover period of stockholder's equity

( 5 ) MSC's turnover period of borrowed money (long-term) from p a r e n t ( 6 ) MSC's turnover period of borrowed money (short-term) from bank ( 7 ) MSC's turnover period of borrowed money (long-term) from bank ( 8 ) ( ( 1 ) - ( 2 ) ) - ( ( 3 ) + ( 4 ) + ( 5 )

+( 6 )

+( 7 ) )

Table 1 6 P r o f i t

&Loss o f MSC of i n d u s t r i e s manufacturing

consumer durables, Mar. 1971, "Sum +Ratio1'

(11) Selllng, administrative

&general expenses (12) Operating profit (or loss A)

(13)

Non-operatingIncome

/(14) Gross profit (or loss A) (15)

Non-operatingcharge

(16) Interest

&discount charge paid (17) Profit (or loss A) before taxes

Table 17 Turnover periods of lndustrles manufacturing consumer durables, Mar. 1971, "Ratlo

+Sum"

(month .-

) ,Sum

(1) (2)

(*I

average D

devla- tion**

average

7.68

-)h.Og (2.49)

3.59

B C

devla- tion**

0.0 0.0 (0.0)

Adevia- tion**

12.18

9.06

3.67 average

9.14

-)4.117

(1.57)

4.67

devia-

average average tion**

21.81 12.28 9.78

. -) 6.53 6.40 devia-

4.46

2.17 (0.98)

-13.52 (1.09)

2.85

(2.13) 5 75

(2.36) 1.65

(0.34)

-)11.97 (3.54)

9.84

Hote: Item numbers a r e t h e same a s i n Table 15.

** -- Standard deviation

Table 18 P r o f i t

&Loss of MSC of i n d u s t r i e s manufacturing consumer durables, Mar. 1971, 50

0+-

"Ratio

-tSum" gE 2+

zzi

'45 5 m

$

(Per 4

4.31 3.69

4.71 100

90.25 100 I

87.90 0.0 2.38

10.11 3.05

(14) (9) (10)

2.08

0.43 2.30

5.76 100

94.58 1 1

(12) 1

100 86.15 100

89-27 1.48

3.79 - 460

0.82

+ 9

3.79 1

2.68

-) 12.26 1.59

+)

8.52

-) 8.77 1.96

+) 1.09

6.32

I

1-75 -1 u . 3 2

0.0 - :

0.0 + 0 1

1 0.78

5.40 +) 3.01

q

A+

5

r l w o

t a ? ?

c o s m

-

I-.

I? - ?

O

2

---- -

? % 3 ?

m c o

-.

w

I

-.

w .9 n 5

ln

.-

rl? " ?

a t - w

, - I -

-

f

l

I

-

CU m

CU. '1

.z

n c v o

n'9 C:

c u e 0

-

I.?

C5

3 3

? -f.

CU

2

m n

a ? ? ? n

"v

l-

7

- - - n

Iw

t- r l 4 d- - -

-

557 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -273- SALES COMPANY IN JAPAN

Table 19 Household-electrical apparatus industry belonging to channel

2Mar. 1971. Drawing promissory notes

Note: The scales A, B, C are the same as in Table 1..

Table

20Household-electrical apparatus industry belonging to channel 2 Mar. 1971. Drawing promissory notes

1

B

0.0I

0.0A

0.0

I

0.0Note: The scales A, B, C are the same as in Table 1.

-

(sales weight

)A B C Sm

Table 21 Automobile industry belonging to channel 3 Mar. 1971. Drawing promissory notes

C

0 . 1

I

0.02 Sum

1

2 Sum1

Sum

I

0.20

1

0.0I

I

0.03

1

0.0

1

0.0 10.01

0.00.0

I

0.0 0.0I

0.0I I

A

,I

0.0

I

0.0 0.0I

0.0I -

B

0.251

0.53 0.0I

0.0I

1

2 Sum0.0

I

0.00.0

I

0.0I

0.03

1

0.0 0.621

0.0I

-,

C

0.27

1

0.00.07

1

0.0I

I -.

I

0.17 1 -

Sum

I I

0.05

1

Note: The s c a l e s A , B, C a r e t h e same a s i n Table 1.

Table 22 Automobile i n d u s t r y belonging t o channel 3 /Mar. 1971. Drawing promissory notes

Note: The s c a l e s A , B , C a r e t h e same a s i n ~ a b l e 1.

( s a l e s weight )

5.3 Functions of j o i n t MSC i n producers1 goods i n d u s t r i e s

It i s c h a r a c t e r i s t i c s of producers1 goods i n d u s t r i e s t h a t j o i n t MSC, which i s incorporated by s e v e r a l manufacturers, performs an impor- t a n t f u n c t i o n i n s t a b i l i z a t i o n of market p r i c e . But j o i n t MSC has not a double f u n c t i o n t o p e r f o m : a s s a l e s agent and a s f i n a n c i e r . The one g r e a t exception I know t o t h i s i s a j o i n t MSC i n t h e petroleum i n d u s t r y .

There a r e j o i n t MSC i n t h e c o l d r o l l e d s t a i n l e s s s t e e l s h e e t and p l a t e i n d u s t r y , t h e s t e e l b a r of small diameter i n d u s t r y , t h e c a b l e i n d u s t r y , t h e gear i n d u s t r y and t h e petroleum i n d u s t r y .

The r e s u l t s which gained by my survey of i n t e r v i e w t o t h e s e indus- t r i e s can b e c o n t r a c t e d i n t o two p a r t s , t h a t i s , a ) causes and b ) func- t i o n .

a ) causes of j o i n t MSC

Small-scale companies p r e v a i l i n some i n d u s t r y . They cannot supply

A B

0.40

1

0.700.0

I

0.0I

1

2Sum

0.0

I

0.00.0

I

0.0- I

C

0.761

0.00.16

1

0.0I

Sum

I I

0.50

1

559 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -275- SALES COMPANY IN ,JAPAN

t h e i r products correspondingly t o demand of u s e r s ( i n d u s t r i a l o n e s ) . Overproduction and underproduction, consequently, extremely i r r e g u l a r p r i c i n g s have been repeated. Users of t h e s e products cannot formulate d e f i n i t e production planning. These companies and u s e r s agree on balanced supply and demand a t a s t a b l e market p r i c e . These u s e r s a r e of growing i n d u s t r y i n t h e 1960s. On s t a b i l i z a t i o n of t h e market p r i c e i s placed r e s t r i c t i o n s of The Antimonopoly L e g i s l a t i o n .

Another i n d u s t r y have ha$ enough experience a s t o o v e r f i c i l i t i e s of production. The depression c a r t e l have been approved i n t h i s indus- t r y . The market p r i c e was u n s t a b l e . J o i n t MSC of t h i s i n d u s t r y was approved by The F a i r Trade Commission, because t h e market s h a r e of t h i s j o i n t MSC i s not so l a r g e .

b ) f u n c t i o n

J o i n t MSC a r e expected t o f u l f i l i t s f u n c t i o n a s producer of a s t a b l e market p r i c e and a s t a b l e supply corresponding t o a demand. But a s t a b l e market p r i c e i s r e a l i z e d , only i f t h e p r i c e i s s t a b l e even a t a heavy production c o s t . I f a market i s very i r r e g u l a r , t h e demand becomes u n s t a b l e . This r e a c t s on production Thus j o i n t MSC would not be a b l e t o f u l f i l i t s f u n c t i o n . A g r e a t d e a l of c a p i t a l i s n e c e s s a r y

f o r t h e s t a b l e market p r i c e .

Another f u n c t i o n of j o i n t MSC i s t o a s s i g n kinds of product t o i t s

c o n s t i t u e n t members This assignment c o n t r i b u t e s t o a r e d u c t i o n i n

p r o d u c t i o n c o s t s . '

6. CONCLUSION

Commercial c a p i t a l has a double f u n c t i o n t o perform f o r i n d u s t r i a l c a p i t a l : a s s a l e s agent and a s f i n a n c i e r . It s e l l s o r markets manufac- t u r e d products a s t h e former, while buys them from i n d u s t r i a l c a p i t a l on i t s own account, a s t h e l a t t e r , i n other words, i n v e s t s c i r c u l a t i n g c a p i t a l i n i t s b u s i n e s s . ( I t i s t o be noted t h a t a manufacturer's s a l e s d i v i s i o n can p r o p e r l y f u l f i l i t s f u n c t i o n a s s a l e s a g e n t . ) I f i n d u s t r i a l c a p i t a l excludes commercial c a p i t a l from s a l e s agency and s e l l s on i t s own account, t h e advantage r e s u l t i n g from commercial capi- t a l ' s a c t i v i t i e s a s f i n a n c i e r i s counterbalanced. I f manufacturers can exclude t h e i r wholesalers without o f f s e t t i n g t h i s advantage, it i s

,

p r e f e r a b l e f o r it. The rolw i s a l l o t t e d t o MSC.

By t h e method of l i q u i d a t i o n of t h e t r a n s a c t i o n between MSC and

i t s p a r e n t manufacturer t h e f u n c t i o n of MSC can be i d e n t i f i e d . While

t h e promissory n o t e l i q u i d a t i o n i s connected i n d i s s o l u b l y w i t h MSC a s

f i n a n c i e r , t h e endorsed n o t e l i q u i d a t i o n i s connected c l o s e l y with MSC

a s s a l e s agent. A i m s of MSC of promissory n o t e l i q u i d a t i o n a r e d i f f e r -

e n t from t h o s e of MSC o f endorsed n o t e l i q u i d a t i o n . A i m a ( a c c e l e r a t -

i n g t h e t u r n o v e r of p a r e n t ' s c i r c u l a t i n g c a p i t a l ) , b (spokesman of

d e a l e r s t o p a r e n t manufacturer and spokesman of t h e p a r e n t t o d e a l e r s )

and c ( a marketing channel f o r a new e s t a b l i s h e d productive d i v i s i o n

being d i f f e r e n t from t h a t o f a l r e a d y e s t a b l i s h e d d i v i s i o n s ) a r e con-

nected w i t h MSC of promissory note l i q u i d a t i o n . Moreover, most of t h e

MSC o f aim b and c can p r o p e r l y f u l f i l t h e i r f u n c t i o n a s f i n a n c i e r .

There i s no remarkable aim f o r MSC of endorsed note l i q u i d a t i o n . A i m

d , e (keeping marketing channel f o r parent ) , f (apparent d i s c r i m i n a t i o n

561 INDUSTRIAL CHARACTERISTICS OF MANUFACTURERS

-277-SALES COMPANY IN JAPAN

of r e s p o n s i b i l i t i e s between productive and s a l e s d i v i s i o n ) and h ( r e c o n c i l i a t i o n o f p r o f i t ) a r e connected w i t h MSC of t h i s method o f l i q u i d a t i o n .

We can recognize t h e l a r g e weight of i n d u s t r i e s manufacturing consumer durables o f MSC's promissory note l i q u i d a t i o n and of m e r i t a

o r a' ( i n c l u d i n g aim a ) from t h e p o i n t of view of s o c i a l reproduction.

The p r o p o r t i o n of m e r i t a o r a' ( i n c l u d i n g aim a ) of manufacturers of consumer durables i s 0.74 and t h e p r o p o r t i o n of m e r i t a o r a' ( i n c l u d - i n g aim a ) of 5nanufacturer.s of consumer durables o f MAC'S promissory note l i q u i d a t i o n i s 0.70. 0.945 = 0.70/0.74.

REMARK Merit a ( i n c l u d i n g aim a ) means a f u n c t i o n o r r o l e t o s h o r t e n t h e turnover of c i r c u l a t i n g c a p i t a l of parent. It i s recognized a s m e r i t o r e f f e c t , whether it i s an aim o r n o t . Merit a' means t h a t t h e emphasis i s l a i d on borrowing money by MSC, which r e s u l t s i n s h o r t - ening p a r e n t ' s turnover period.

Marketing channels a r e a l s o connected with t h e method of l i q u i d a - t i o n . There i s one t o one correspondence between marketing channels and i n d u s t r i e s . Channel 1 corresponds t o t h e camera

&f i l m i n d u s t r y of endorsed n o t e l i q u i d a t i o n . This channel i s connected with aim d.

Channel 2 corresponds t o t h e household e l e c t r i c a l a p p a r a t u s i n d u s t r y of

MSC's promissory note l i q u i d a t i o n . Channel 3 corresponds t o t h e auto-

mobile i n d u s t r y of MSC's promissory n o t e l i q u i d a t i o n . Channel 5 cor-

responds t o t h e c o n s t r u c t i o n machinery i n d u s t r y of MSC's promissory

n o t e l i q u i d a t i o n . These 2, 3, 5 channels a r e connected with m e r i t a o r

a' (including aim a ) .

There i s no room f o r doubt t h a t MSC i s c l o s e l y connected with con-

sumers' goods i n d u s t r i e s . But t h e r e a r e a few i n d u s t r i e s of producers'

goods of which j o i n t MSC i s c h a r a c t e r i s t i c . J o i n t MSC has a function

t o perform. It i s incorporated t o balance supply with demand a t a

s t a b l e market p r i c e . But it cannot be s a i d t h a t j o i n t MSC properly

f u l f i l i t s function, because The Antimonopoly L e g i s l a t i o n p l a c e s r e -

s t r i c t i o n s on such a MSC. J o i n t MSC be admitted only under g r e a t re-

s t r i c t i o n s .

563 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -279- SALES COMPANY IN JAPAN

APPENDIX

1. Preliminary survey

Purpose: Determination of population (manufacturers owning MSC) f o r t h e sake of sample survey of interview.

Date

:From J u l y 1971 t o December 1971 Method

:By mail

Subject: A l l t h e manufacturing business companies (except p u b l i c a t i o n , p r i n t i n g and t h e r e l a t e d ) whose c a p i t a l stocks a r e g r e a t e r than o r equal t o 100 m i l l i o n yen.

The r a t i o of response: 0.9754 (2969/3044)

Result

:The number o f manufacturers owning MSC i s given:

2. Sample survey o f interview

Date

:From August 1 9 7 1 t o December 1972 Subject: Stratum 1 and 2

-

Stratum Number

Sampling f r a c t i o n : The sampling f r a c t i o n i s 5 125 1

123

Note: Stratum and s c a l e a r e abbreviated t o S t . and Sc.

r e s p e c t i v e l y .

unclas- sifiable

33

----

Sum 5 37 2

79

Sum A

C~~--

3 35

B 4 142

7 / 21 1 2 / 1 2 10 / 29 1 6 / 1 6 1

2 sum

31 / 94 1 3 / 38

-

, ' /

2.1 Inappropriate sample

From interview it turned out inappropriate to calculate the propor- tion in the usual manner (well known formula), because particular strata

(scale A) yielded many inappropriate sample points. The reasons are thus. Manufacturers belonging to scale A are often subsidiaries of big manufacturers and the former sells their products to the latter which owns MSC. In such a case the former gave me the same response as the latter that they own MSC. Such a case was classified into the inap- propriate group. Manufacturers which were incorporated by parent, which is sales company, were also classified into the inappropriate group.

The number of inappropriate sample points is given below. The number of non-response is also given below. It is notable that many of joint enterprises of Japanese and foreign enterprise rejected response.

Proportion of inappropriate sample

2.2 Formula of estimation

We cannot use the well-known formula = 1 p . ; . , a-2 =

I 2 2x

1 2 sum

R N. - n . P ( l - P i )

1 2 . - 2 pi2 (P is the population proportion, Ni is the i=l Ni - 1 n i

1 2 sum 13131

5113 /I /

1 1 7 0110 /I /

3118

01 8

/I /

11 / 11 / /I 1 21 6

2110

/ I /

11 /

- .

/ I / /I /

A B C S u m

1112

-

0116 /I /

A B C S u m

0111 1/16 /I 1

I

565 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -281- SALES COMPANY IN JAPAN

population s i z e of stratum i, ni i s t h e sample s i z e of stratum i , 8 i s t h e number o f s t r a t a , z2 i s t h e sampling f r a c t i o n of i, 2 i s t h e e s t i - mate of t h e population p r o p o r t i o n ) , because t h e population may vary. I n our sample survey i n a p p r o p r i a t e sample p o i n t s a r e t o o l a r g e t o n e g l e c t . Consequently an estimate i s not unbiased. We can use t h e method of r a t i o estimate:

N n n .

- Nu iu -

where Y = - , 5 = -

N , y i = - , x i = n zv ;

Ni s t h e s i z e o f popula-

ni i

t i o n , N i s t h e number or sample p o i n t s of some a t t r i b u t e , f o r example,

Ut h e number o f parent companies which a r e l i q u i d a t e d by notes drawn by MSC, Nv i s t h e whole number o f manufacturers owning MSC, ni i s t h e sam- p l e s i z e of stratum i , n i s t h e numter of sample p o i n t s which possess

iu

some a t t r i b u t e , f o r example, t h e number qf parent companies which a r e l i q u i d a t e d by notes drawn by MSC i n stratum i o f sample and n . i s t h e

zv

whole number o f parent companies owning MSC i n stratlZm i o f t h e sample, r 2 i s t h e mean square e r r o r . I n p a r t i c u l a r % and y mean various

i

types of r a t i o a s i n t h e following manner:

-

0+ s a l e s t o MSC + s a l e s t o MSC + *..

Yi = n.

Formula (1) gives t h e ( 0 , l ) r a t i o and formula ( 2 ) may be called t h e weighted r a t i o by s a l e s . Furthermore, fortunately, turnover peridds of

c a p i t a l a r e given by t h e above method. It i s given, f o r example,:

-

0+ accounts

¬es receivable t o MSC +

0 + " 'x i - - n?:

(3)

-

0+ monthly s a l e s t o MSC +

0+ .-.

Yi - n.

We assume 2 . 7 v a s 95% confidence i n t e r v a l . The r e l i a b i l i t y of t h e i n t e r v a l i s proved about the mean by MIDZUNO

[ 2 ] .The s t a t i s t i c which we consider, however, i s Y - . Although t h e r e i s no doubt about

Y

t h e a p p l i c a b i l i t y of the formula, yet a l i t t l e room f o r doubt about im- mediate application of tkie value of 2.7.

Formula ( 3 ) may be s a i d "taking sum, and then taking r a t i o . "

Reversely ' t a k i n g r a t i o , and then taking sum" i s possible and can be

expressed as follows:

567 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -283- SALES COMPANY IN JAPAN

5 and r-2 a r e t h e same a s above formula. Where i s t h e value of t h e

Z $3

j t h sample point o f some p a r t i c u l a r a t t r i b u t e f o r t h e i t h stratum,

Siji s t h e number o f sample p o i n t s o f a p a r t i c u l a r a t t r i b u t e f o r t h e i t h stratum, n . i s t h e sample s i z e of t h e i t h stratum, ni i s t h e number o f

2

appropriate sample p o i n t s of t h e i t h stratum. There i s ample room f o r doubt a s t o whether t h e formula o f rZ2 i s a p p l i c a b l e t o t h i s c a s e , but a r a t i o n a l i n t e r p r e t a t i o n o f which i s t o be expected i n t h e near f u t u r e . We w i l l giire no r-2 i n l a t e r t a b l e s f o r such a reason.

Z

Two d i f f e r e n t approaches t o MSC correspond t o t h e above two calcu- l a t i o n method. I f we t r y t o i n v e s t i g a t e t h e influence of MSC on s o c i a l reproduction, "sum

-tr a t i o " method w i l l be applied. I f we want t o know how each of MSC behaves, " r a t i o

-tsum" method w i l l be applied. The values i n Table 1 7 and 1 8 a r e of " r a t i o

+sum." Others a r e given by

"sum

+r a t i o . "

s e v e r a l turnover periods a r e defined a s follows:

manu,facturer

turnover period of accounts

¬es r e c e i v a b l e t o MSC

accounts

¬es r e c e i v a b l e / average monthly s a l e t o MSC turnover period of notes (drawn by MSC) r e c e i v a b l e discounted by bank

notes r e c e i v a b l e discounted by bank / average monthly s a l e t o MSC MSC

turnover period of current a s s e t s

c u r r e n t a s s e t s / average monthly s a l e turnover period o f accounts

¬es r e c e i v a b l e

accounts

¬es r e c e i v a b l e / average monthly s a l e

turnover period of notes receivable discounted by bank

notes receivable discounted by bank / average monthly s a l e turnover period of stockholder's equity

stockholder's equity / average monthly s a l e

turnover period of borrowed money (long-term) from parent manufacturer borrowed money (long-term) from parent manufacturer / average

monthly s a l e turnover period of borrowed money (short-term) from bank

borrowed money (short-term) from bank / average monthly s a l e turnover period of borrowed money (long-term) from bank

borrowed money (long-term) from bank / average monthly s a l e

569 INDUSTRIAL CHARACTERISTICS OF MANUFACTURER'S -285- SALES COMPANY IN JAPAN

REFERENCE

[ I ] H. Seto, "A study of the turnover of circulating capital and manu- facturer's sales company in Japan based on a sample survey", Research Paper Series No. 3, Department of information science, College of Economics, Kagawa University, 1974.

ACKNOWLEDGEMENTS

The author ought to note that but for the following persons' sup- port, he could not have accoumplished this work:

Administrative Management Agency and Ministry of Finance for their per- mission for Statistics of Incorporated Enterprises,

Prof. S. Endo, President of this university and Prof. M, Kimura, ex-Dean of this college, for their support to the sample survey of interview, Prof. H. Kimura and Ass. Prof. K. Oyabu for their contribution to statistical treatment,

Prof. K. Matsuda of Kobe Univ. and Ass. Prof. N. Sato of Aoyama Gakuin Univ., for their valuable comments,

the interviewees of the sample survey for their friendly responses, The Documentation Center For Business Analysis The Research Institute for Economics

&Business Administration Kobe Univ. and the Economic

9