1. I nt r oduc t i on

Si nc e t he e a r l y 1970s c ount r i e s ’ c hoi c e s of e xc ha nge r a t e r e gi me ha ve s i gni f i c a nt l y c ha nge d.

Imme di a t e l y a f t e r t he br e a kdown of t he Br e t t on Woods s ys t e m of f i xe d e xc ha nge r a t e s i n 1973 whe n t he wor l d’ s ma j or c ur r e nc i e s be ga n t o f l oa t , mos t de v e l ope d c ount r i e s c on- t i nue d t o pe g t he i r e xc ha nge r a t e s t o a s i ngl e c ur r e nc y or a ba s ke t of c ur r e nc i e s .

Howeve r , s i nc e t he l a t e 1970s , t he r e ha s be e n a s t e a dy f a l l i n t he numbe r of de ve l opi ng c ount r i e s t ha t ma i nt a i n s ome t ype of f or ma l pe gge d e xc ha nge r a t e , a nd a c onc omi t a nt r i s e i n t he numbe r of c ount r i e s wi t h mor e f l e xi bl e r e gi me s .

Expl a na t i ons t o a c c ount f or t hi s t r e nd i nc l ude : l a r ge e xc ha nge r a t e f l uc t ua t i ons a mong t he ma j or c ur r e nc i e s t ha t f ol l owe d t he br e a kdown of t he Br e t t on Woods s ys t e m, a c c e l e r a t i on of i nf l a t i on f ol l owi ng oi l s hoc ks of t he 1970s a nd 1980s , i nc r e a s e s i n c a pi t a l mobi l i t y, a nd a s e r i e s of e xt e r na l s hoc ks i nc l udi ng a s t e e p r i s e i n i nt e r na t i ona l i nt e r e s t r a t e s , a s l owdown of gr owt h i n t he i ndus t r i a l c ount r i e s , a nd t he de bt c r i s i s .

1)For e i gn Exc ha nge Ra t e Sys t e ms — A Re a s s e s s me nt

Os a mu Kur i ha r a * a nd Chr i s Cz e r ka ws ki **

(Received on October11,2006)

* AssociateProfessor,Faculty ofSociology,HiroshimaKokusaiGakuin University

** Professor,Faculty ofEconomics,HiroshimaShudo University

1) Thesteady fallin thenumberofcountrieswith softpegscontinued in the1990s,buttheshiftwas towardsboth floating ratesand hard pegs. Forthegroup of22 developed marketeconomies (DME),33 emerging marketeconomies(EME),and otherdeveloping countries(0)16 theresults areasfollows:In 1991,59 percentofdeveloping countrieshad somekind ofsoftpeg regime. By 1999,thisproportion had fallen to 34 percentwhiletheshareoffloating regimesincreased from 25 to 42 percent,and theshareofhard pegsfrom 16 to 24 percent. Theshiftaway from softpegs and towardsboth cornersisobserved in allthreecountry groupsbutalargepartoftheexpansion on thehard peg sideresultsfrom thecreation oftheEMU which reduced thenumberofDMEswith asoftpeg regimefrom 11 to one. TheEMEswith asoftpeg regimefellfrom 21 to 14. Fiveof these(Indonesia,Thailand,Russia,Brazil,and Mexico)moved to floating regimes,and two (Argentinaand Bulgaria)instituted currency board arrangements. Among otherdeveloping countries,alargershifthasbeen towardsflexibility;only six smallcountriesmoved to hard peg regimes.

The pol a r i z a t i on i n t he c ur r e nc y r e gi me c hoi c e ha s l e d s ome a ut hor s t o c onc l ude t ha t s of t pe g r e gi me s i n c ount r i e s ope n t o i nt e r na t i ona l c a pi t a l f l ows a r e not s us t a i na bl e f or e xt e nde d pe r i - ods , a nd t ha t t he s e c ount r i e s s houl d move a wa y f r om t he mi ddl e t o wa r ds bot h e xt r e me s of t he e xc ha nge r a t e s pe c t r um whe r e t he r i s k i s mi ni ma l ( di s a ppe a r i ng mi ddl e , t wo- c or ne r s ol ut i ons ) .

He nc e t he y mus t e i t he r f l oa t f r e e l y or f i x t r ul y a nd t hus c r e di bl y unde r a ha r d pe g r e gi me .

In r e c e nt ye a r s , t he “ t wo- c or ne r s ol ut i on” ha s be c ome a ne w or t hodoxy i n t he c hoi c e of a n e xc ha nge r a t e r e gi me f or de v e l opi ng c ount r i e s .

Thene w or t hodoxy ha s be e n c ha l l e nge d by a numbe r of a ut hor s ( Fr a nke l 1999, Coope r 1999, Edwa r ds 2000, Wi l l i a ms on 2000) .

2)The c hoi c e of whe t he r t o ha ve a f i xe d or f l oa t i ng e xc ha nge r a t e r e gi me r e ma i ns a c ont r ove r - s i a l i s s ue f or ma n y c ount r i e s i n t he de v e l opi ng wor l d.

Acc or di ng t o r e s e a r c h by Da vi d Fi e l d- i ng a nd Mi c ha e l Bl e a ne y, pr e s e nt e d t o t he Roya l Ec onomi c Soc i e t y a t t he Annua l Conf e r e nc e a t Wa r wi c k Uni ve r s i t y on Thur s da y 2 Apr i l , 1998, a dhe r e nc e t o a f i xe d e xc ha nge r a t e doe s he l p ke e p i nf l a t i on l ow.

Att he s a me t i me , ma i nt e na nc e of a f i xe d e xc ha nge r a t e ove r a l ong pe r i od of t i me r e qui r e s c ommi t me nt t o ma c r oe c onomi c pol i c i e s whi c h e ns ur e t ha t ba l a nc e of pa yme nt s

2) In particular,theseauthorshaveargued that:“comersolutions”arenotfreefrom problems:“corner solutions”may beappropriateunderspecificcircumstancesforalimited numberofdeveloping countries:moving away from softpegstowardsmoreflexibility doesnotmean freefloating:and intermediateregimesaremorelikely to beappropriateformorecountriesthan thecornersolutions. A recentchallengecamefrom theFrench and Japanesefinanceministries. In adiscussion paper jointly prepared fortheAsiaand European FinanceMinisters’meeting in January 2001,they pointed outthemain shortcomingsofthetwo extremesolutionsand stated thatan intermediate regimewhereby theexchangeratemoveswithin agiven implicitorexplicitband with itscenter pegged to abasketofcurrencieswould beappropriateformany emerging marketeconomies (ASEM 2001). Such aregimeshould bebacked by consistentand sustainablemacroeconomicand structuralpoliciesand may beaccompanied,foracertain period and underspecificconditions,by market-based regulatory measuresto curb excessivecapitalinflows. Crockett1994,Eichengreen 1994,Obstfeld and Rogoft(1995),Summers2000,Eichengreen 2000. Fisherargued thatthedis- appearing middleisdueto thelogicoftheimpossibletrinity (Fisher2001). Frankeland others (2000)stressed thattherelativedifficulty to verify theintermediateregimes,particularly thebroad band regimespegged to abasketofcurrencies,isalso acriticalfactorto explain why intermediate regimesarelessviablethan thecornersolutions. Edwards(2000)noted:“From ahistoricalper- spectivethecurrentsupportforthetwo-cornerapproach islargely based on theshortcomingsofthe softpegs...,and notthehistoricalmeritsofthetwo cornersystems”. Frankel(1999)observed:

“Neitherpurefloating norcurrency boardssweep away alltheproblemsthatcomewith modem globalized financialmarkets. Centralto theeconomists’creed isthatlifealwaysinvolvestrade offs. Countrieshaveto tradeofftheadvantagesofmoreexchangeratestability againsttheadvan- tagesofmoreflexibility. Ideally,they would pick thedegreeofflexibility thatoptimizeswith respectto thistradeoff. Optimization often,though notalways,involvesan interiorsolution”. See. Frankel,J.A.,“No singleCurrency RegimeisRightforallCountriesoratallTimes”, NBER 1999:Edwards,ibidem.

de f i c i t s do not pe r s i s t .

3)Among t he ot he r f a c t or s i nf l ue nc i ng mone t a r y gr o wt h, t he mos t i mpor t a nt i s t he de gr e e of ope nne s s of t he e c onomy ( t ha t i s , t he s i z e of i nt e r na t i ona l t r a de r e l a t i v e t o t he e c onomy’ s t ot a l out put ) .

More ope n e c onomi e s t e nd t o ha ve l owe r mone t a r y gr owt h r a t e s , pe r ha ps be c a us e t he ba l a nc e of pa yme nt s di s c i pl i ni ng me c ha ni s m i s s t r onge r .

Ac ount r y i n t he t op 5% wi t h r e ga r d t o ope nne s s c a n be e xpe c t e d t o ha v e a mone t a r y gr o wt h r a t e a bout 4% l o we r t ha n t he a v e r a ge .

An i mpor t a nt di f f e r e nc e be t we e n f i xe d a nd f l e xi bl e e xc ha nge r a t e r e gi me s i s i n t he t r a ns - mi s s i on pr oc e s s l i nki ng mone t a r y gr o wt h a nd r e a l e c onomi c gr o wt h wi t h i nf l a t i on.

In t he or y , a n i nc r e a s e i n mone t a r y gr o wt h or a r e duc t i on i n r e a l e c onomi c gr o wt h i n a f l e xi bl e e xc ha nge r a t e r e gi me ought t o l e a d t o a pr opor t i ona t e i nc r e a s e i n t he i nf l a t i on r a t e .

In a f i x e d e xc ha nge r a t e r e gi me , t he e f f e c t s wi l l be l e s s t ha n pr opor t i ona t e be c a us e s ome pr i c e s ( t hos e of goods t r a de d on i nt e r na t i ona l ma r ke t s ) wi l l not be i nf l ue nc e d by wha t ha ppe ns i n t he dome s t i c e c onomy .

Most ma c r o da t a s ho ws t ha t a 1% i nc r e a s e i n mone t a r y gr o wt h i n a f i x e d e xc ha nge r a t e s ys t e m c a n be e xpe c t e d t o i nc r e a s e t he i nf l a t i on r a t e by j us t 0. 5%.

4)Ye t l i t t l e c ons e ns us ha s e me r ge d a bout how e xc ha nge r a t e r e gi me s a f f e c t c ommon ma c - r oe c onomi c t a r ge t s , s uc h a s i nf l a t i on a nd gr owt h.

Ata t he or e t i c a l l e ve l , i t i s di f f i c ul t t o e s t a b- l i s h una mbi guous r e l a t i ons hi ps be c a us e of t he ma ny wa ys i n whi c h e xc ha nge r a t e s c a n i nf l ue nc e a nd be i nf l ue nc e d by ot he r ma c r oe c onomi c v a r i a bl e s .

Like wi s e , e mpi r i c a l s t udi e s t ypi c a l l y f i nd no c l e a r l i nk be t we e n t he e xc ha nge r a t e r e gi me a nd ma c r oe c onomi c pe r f or ma nc e .

5)3) Fielding and Bleaney examined theimpactofthechoiceofexchangerateregimeon inflation rates across80 low and middleincomecountries. They found that:Themostdirectinfluenceofafixed exchangerateisthatittendsto encouragemonetary disciplinein agovernmentsincerapid mone- tary expansion leadsto painfulbalanceofpaymentsdeficits. Controlling forotherfactors,the averagefixed exchangeratecountry hasarateofmonetary growth 12% lowerthan theaverage flexibleexchangeratecountry.

4) See“ExchangeRateRegimes,Monetary Discipline& Inflation”,by David Fielding and Michael Bleaney presented attheRoyalEconomicSociety,1998,AnnualConferenceatWarwick University.

Also comparewith:Ghosh,A.,Ostry,J,Gulde,A-M.,Wolf,H.(1999),“DoestheExchangeRate RegimeMatterforInflation and Growth?”,EconomicIssuesNo2,InternationalMonetary Fund, Washington D.C.

5) Williamson,J.“Estimating Equilibrium ExchangeRates”,InstituteofInternationalEconomics, 1994. Also Williamson,J.,“ExchangeRateRegimesforEmerging Markets:Reviving theInterme- diateOption”,InstituteforInternationalEconomics,September2000;Schulstad,Paul,and Serrat, A.(1995),An EmpiricalExamination ofa MultilateralTargetZoneModel(Banco deEspana: Documento deTrabajo no.9532).;Svensson,LarsE.O.(1992),“An Interpretation ofRecent Research on ExchangeRateTargetZones”,JournalofEconomicPerspectives,6(4),Fall. Tara- poreCommittee(1997),ReportoftheCommitteeon CapitalAccountConvertibility (Mumbai: ReserveBank ofIndia). Ortiz,Guillermo,and Agustin Carstens(2000),“TheExperiencewith a→

Thi s pa pe r i s or ga ni z e d i nt o f our s e c t i ons .

Thef i r s t one gi ve s a n i nt r oduc t i on t o t he t opi c , t he s e c ond de a l s wi t h t e r mi nol ogy a nd pe r i odi z a t i on, t he t hi r d one wi t h ma c r oe c onomi c a dj us t - me nt s unde r di f f e r e nt c ur r e nc y s ys t e ms a nd t he f our t h one i s a s ynt he t i c s umma r y .

Apopr e c i a t i on f or I ns t i t ut e of Adv a nc e d St udi e s , Hi r os hi ma Shudo Uni v e r s i t y f or f i na nc i a l a s s i s t a nc e i n publ i s hi ng t hi s pa pe r

2. For e i gn Exc hange Rat e Sys t e m, Te r mi nol ogy and Pe r i odi z at i on

Be yond t he t r a di t i ona l f i xe d- f l oa t i ng di c hot omy l i e s a s pe c t r um of e xc ha nge r a t e r e gi me s .

The de f a c t o be ha vi or of a n e xc ha nge r a t e , mor e ove r , ma y di ve r ge f r om i t s de j ur e c l a s s i f i c a t i on.

Whi l e i t i s c us t oma r y t o s pe a k of f i xe d a nd f l oa t i ng e xc ha nge r a t e s , r e gi me s a c t ua l l y s pa n a c on- t i nuum, r a ngi ng f r om pe gs t o t a r ge t z one s , t o f l oa t s wi t h he a vy , l i ght , or no i nt e r v e nt i on.

Thet r a di t i ona l di c hot omy c a n ma s k i mpor t a nt di f f e r e nc e s a mong r e gi me s .

Mos t c ur r e nt a na l ys e s us e a t hr e e - wa y c l a s s i f i c a t i on: pe gge d, i nt e r me di a t e ( i . e . , f l oa t i ng r a t e s , b ut wi t hi n a pr e de t e r mi ne d r a nge ) , a nd f l oa t i ng.

Regi me s c a n be c l a s s i f i e d a c c or di ng t o e i t he r t he publ i c l y s t a t e d c ommi t me nt of t he c e nt r a l ba nk ( a de j ur e c l a s s i f i c a t i on) or t he obs e r ve d be ha vi or of t he e xc ha nge r a t e ( a de f a c t o c l a s s i f i c a t i on) .

Nei t he r me t hod i s e nt i r e l y s a t i s f a c t or y .

Ac ount r y t ha t c l a i ms t o ha v e a pe gge d e xc ha nge r a t e mi ght i n f a c t i ns t i ga t e f r e - que nt c ha nge s i n pa r i t y .

Ont he ot he r ha nd, a c ount r y mi ght e xpe r i e nc e ve r y s ma l l e xc ha nge r a t e move me nt s , e ve n t hough t he c e nt r a l ba nk ha s no obl i ga t i on t o ma i nt a i n a pa r i t y .

Thea ppr oa c h us ua l l y t a ke n i s t o r e por t r e s ul t s a c c or di ng t o t he s t a t e d i nt e nt i on of t he c e nt r a l ba nk, but t o s uppl e me nt t he s e r e s ul t s by c a t e gor i z i ng t he nonf l oa t i ng r e gi me s a c c or di ng t o whe t he r or not c ha nge s i n pa r i t y we r e f r e que nt .

Thedejurec l a s s i f i c a t i on us e s t he I MF’ s Annua l Re por t on Exc ha nge Ar r a nge me nt s a nd Exc ha nge Re s t r i c t i ons , whi l e t he

defactoc l a s s i f i c a t i on i s ba s e d on a s ur v e y of I MF de s k of f i c e r s f or e a c h c ount r y .

The f ol l o wi ng c l a s s i f i c a t i on s ys t e m ( r a nke d on t he ba s i s of t he de gr e e of f l e xi bi l i t y of t he a r r a nge me nt ) ha s be e n wi de l y us e d i n t he l i t e r a t ur e : i nde pe nde nt f l oa t i ng, ma na ge d f l oa t i ng,

Floating ExchangeRateRegime:TheCaseofMexico”,paperpresented to aconferenceon “Interna- tionalFinancialMarkets:TheChallengeofGlobalization”atTexasA and M University,31 March;

Pisani-Ferry,Jean,and BenoitCoeure(1999),“TheExchange-RateRegimeAmong MajorCurrenci- es”,paperpresented to theIMF Conferenceon Key Issuesin Reform oftheInternationalMonetary and FinancialSystem,Washington,May 28-29;Rose,Andrew (1996),“ExchangeRateVolatility, Monetary Policy,and CapitalMobility:EmpiricalEvidenceon theHoly Trinity”,JournalofInter- nationalMoneyand Finance.

→

c r a wl i ng ba nds , c r a wl i ng pe gs , pe gge d wi t hi n ba nds , f i xe d pe g a r r a nge me nt s , c ur r e nc y boa r d a r r a nge me nt s , a nd e xc ha nge a r r a nge me nt s wi t h no s e pa r a t e l e ga l t e nde r ( Fr a nke l 1999, Edwa r ds a nd Sa v a s t a no 1999, I MF 1999) .

Her e we c a n e xt e nd t hi s c l a s s i f i c a t i on t o c l a r i f y t he de gr e e of f l e xi bi l i t y a l l owe d by s ome of t he s e r e gi me s , t he r e by ma ki ng i t e a s i e r t o c ompa r e t he a l t e r na - t i v e r e gi me s pr opos e d by v a r i ous a ut hor s .

Fir s t , a ne w “ l i ght l y ma na ge d f l oa t ” r e gi me i s a dd- e d, whi c h i nvol ve s onl y l i ght i nt e r ve nt i ons i n t he f or e i gn e xc ha nge ma r ke t t o mode r a t e e xc e s s i v e f l uc t ua t i ons .

Theke y di f f e r e nc e be t we e n a “ l i ght l y ma na ge d f l oa t ” a nd a “ ma na ge d f l oa t ” i s t ha t , i n t he l a t t e r , t he gove r nme nt ha s a n i de a whe r e t he e xc ha nge r a t e s houl d be t o ma i nt a i n c ompe t i t i v e ne s s a nd i nt e r v e ne s t o ke e p t he r a t e c l os e t o i t .

In t he f or me r , t he r a t e i s e s s e nt i a l l y de t e r mi ne d i n t he ma r ke t by de ma nd a nd s uppl y .

Sec ond, t he c r a wl i ng ba nd r e gi me i s di vi de d i nt o “ c r a wl i ng br oa d ba nd” a nd “ c r a wl i ng na r r o w ba nd” s ys t e ms .

Abr oa d ba nd r e gi me ( s a y , a bout +/ – 15 pe r c e nt a r ound t he c e nt r a l pa r i t y) pr o vi de s mor e f l e xi bi l i t y a nd i s c l os e r t o a f l oa t i ng s ys t e m i n t e r ms of i t s me r i t s a nd s hor t c omi ngs .

Ana r r o w ba nd s ys t e m ( t he Br e t t on Woods s ys t e m, a nd pr e - 1992 Eur ope a n Mone t a r y Sys t e m) , on t he ot he r ha nd, c a n be put t oge t he r wi t h t he ot he r f i x e d e xc ha nge r a t e r e gi me s .

6)The f or e i gn e xc ha nge r a t e s ys t e ms a r e r a nke d on t he ba s i s of t he de gr e e of f l e xi bi l i t y of t he e xc ha nge r a t e .

Atone e nd of t he s pe c t r um i s i nde pe nde nt f l oa t i ng, a r e gi me whi c h pr ovi de s ma xi mum f l e xi bi l i t y , a l l o wi ng t he e xc ha nge r a t e t o be de t e r mi ne d f r e e l y i n t he ma r ke t by s up- pl y a nd de ma nd.

Curr e nc y uni on/ dol l a r i z a t i on c ons t i t ut e s t he ot he r e xt r e me whe r e t he e xc ha nge r a t e doe s not e xi s t be c a us e t he mone t a r y a ut onomy i s f ul l y s ur r e nde r e d a nd a s ha r e d c ur r e nc y or a not he r c ount r y’ s c ur r e nc y i s us e d a s t he onl y l e ga l t e nde r .

Thee i ght r e gi me s be t we e n t he s e e xt r e me s s how de c r e a s i ng f l e xi bi l i t y a s one move s f r om t he f l oa t i ng r e gi me s t owa r ds c ur r e nc y uni on/ dol l a r i z a t i on.

Tos i mpl i f y t he pr e s e nt a t i on a nd be t t e r s t r uc t ur e t he di s - c us s i on, t he t e n r e gi me s a r e a r r a nge d unde r t he f ol l o wi ng f our r e l a t i v e l y homoge ne ous gr oups : ( a ) f l oa t i ng r e gi me s ( i nde pe nde nt f l oa t i ng, l i ght l y ma na ge d f l oa t ) ; ( b) I nt e r me di a t e r e gi me s ( ma na ge d f l oa t , c r a wl i ng br oa d ba nd) ; ( c ) Sof t pe g r e gi me s ( c r a wl i ng na r r o w ba nd, c r a wl i ng pe g, pe gge d wi t hi n ba nds , f i xe d pe g) ; a nd ( d) ha r d pe g r e gi me s ( c ur r e nc y boa r d, c ur r e nc y uni on/ dol l a r i z a t i on) .

The pos t - wa r hi s t or y of c ur r e nc y r e gi me s i s us ua l l y di vi de d i nt o t hr e e pe r i ods :

6) SeeEdwards,S.and.Savastano,M.A “ExchangeRatein Emerging Economies:Whatdo we Know? Whatdo WeNeed to Know”,Working Paper7228,NBER July 1999,and also See Frankel,J.A.,“No singleCurrency RegimeisRightforallCountriesoratallTimes”,NBER 1999.

( a )

Pegged exchangerateregime(Second World War– June1997)Thi s r e gi me wa s f i r s t a dopt e d a f t e r t he Se c ond Wor l d Wa r .

Theva l ue of t he ba ht wa s i ni - t i a l l y e i t he r pe gge d t o a ma j or c ur r e nc y/ gol d or t o a ba s ke t of c ur r e nc i e s .

Theba s ke t r e gi me wa s a dopt e d f r om No v e mbe r 1984 unt i l J une 1997.

Duri ng t hi s pe r i od, t he Exc ha nge Equa l i - z a t i on Fund ( EEF) woul d a nnounc e a nd de f e nd t he ba ht va l ue a ga i ns t t he US dol l a r da i l y , whos e mone t a r y a nd f i na nc i a l me a s ur e s we r e ma i nl y de s i gne d t o be i n l i ne wi t h t he pe gge d e xc ha nge r a t e r e gi me .

( b)

Monetarytargeting regime(1997–2000)Af t e r t he a dopt i on of t he f l oa t i ng e xc ha nge r a t e s ys t e m i n 1997, mos t Sout h- Ea s t As i a n c ount r i e s r e c e i ve d f i na nc i a l a s s i s t a nc e f r om t he I MF.

Duri ng i mpl e me nt a t i on of t he I MF pr ogr a m, mone t a r y t a r ge t i ng r e gi me wa s a dopt e d.

Under t hi s r e gi me , t he Wor l d Ba nk t a r ge t e d t he dome s t i c mone y s uppl y us i ng a f i na nc i a l pr ogr a mmi ng a ppr oa c h i n or de r t o e ns ur e ma c r oe c onomi c c ons i s t e nc y a s we l l a s t o r e a c h t he ul t i ma t e obj e c t i ve s of s us t a i na bl e gr o wt h a nd pr i c e s t a bi l i t y .

TheBa nk s e t t he da i l y a nd qua r t e r l y mone t a r y ba s e t a r ge t s , on whi c h i t s da i l y l i qui di t y ma na ge me nt wa s ba s e d.

Dai l y l i qui di t y ma na ge me nt wa s e s s e nt i a l l y a i me d a t a voi di ng e xc e s s i ve vol a t i l i t y i n i nt e r e s t r a t e s a nd e ns ur i ng l i qui di t y i n t he f i na nc i a l s ys t e m.

( c )

Inflation targeting regime(May1997-present)Af t e r t he I MF pr ogr a m wa s i nt r oduc e d c e nt r a l ba nks ma de a n e xt e ns i ve r e a ppr a i s a l of bot h t he dome s t i c a nd t he e xt e r na l e n vi r onme nt a nd c onc l ude d t ha t t he t a r ge t i ng of mone y s uppl y i s goi ng t o be l e s s e f f e c t i ve t ha n t he t a r ge t i ng of i nf l a t i on.

Thema i n c a us e f or c ha nge wa s t ha t t he r e l a t i ons hi p be t we e n mone y s uppl y a nd out put gr o wt h wa s be c omi ng l e s s s t a bl e , e s pe c i a l l y i n t he pe r i od a f t e r t he ma j or c r i s i s a nd t he unc e r t a i nt y i n c r e di t e xt e ns i ons a s we l l a s t he r a pi dl y c ha ngi ng f i na nc i a l s e c t or .

3. For e gn Exc hange Rat e s ys t e ms i n Sout h Eas t and Nor t h Eas t As i a

Macr oeconomi c per f or mance under al t er nat i ve e xchange r at e r e gi mes ha ve been a

s ubj e c t of c ont i nui ng r e s e a r c h a nd c ont r ove r s y.

Usi ng a t hr e e - wa y c l a s s i f i c a t i on ( pe gge d, i nt e r -

me di a t e , a nd f l oa t i ng r a t e s ) , a n e a r l i e r s t udy ( Ghos h a nd ot he r s , 1996) whi c h i nc l ude d 136 c oun-

t r i e s f or t he pe r i od 1960- 89, a na l yz e d t he l i nk be t we e n e xc ha nge r a t e r e gi me s , i nf l a t i on a nd

gr o wt h

7).

As t r ong r e s ul t of t he s t udy i s t ha t pe gge d e xc ha nge r a t e s a r e a s s oc i a t e d wi t h l o we r i nf l a t i on a nd l e s s va r i a bi l i t y.

Thea ut hor s a r gue d t ha t t hi s wa s due t o a di s c i pl i ne e f f e c t — t he pol i t i c a l c os t s of f a i l ur e of de f e ndi ng t he pe g i nduc e di s c i pl i ne d mone t a r y a nd f i s c a l pol i c y — a nd a c onf i de nc e e f f e c t — t o t he e xt e nt t ha t t he pe g i s c r e di bl e , t he r e i s a s t r onge r r e a di ne s s t o hol d dome s t i c c ur r e nc y , whi c h r e duc e s t he i nf l a t i ona r y c ons e que nc e s of a gi ve n e xpa ns i on i n mone y s uppl y .

Thes t udy a l s o f ound t ha t pe gge d r a t e s a r e a s s oc i a t e d wi t h hi ghe r i n ve s t me nt b ut c or r e l a t e d wi t h s l o we r pr oduc t i vi t y gr o wt h.

Onne t , out put gr o wt h i s s l i ght l y l o we r unde r pe gge d e xc ha nge r a t e s c ompa r e d t o f l oa t i ng a nd i nt e r me di a t e r e gi me s .

In a ddi t i on, t he v a r i - a bi l i t y of gr o wt h a nd e mpl oyme nt i s gr e a t e r unde r t he pe gge d r e gi me s .

8)A numbe r of me t hodol ogi c a l we a kne s s of t he s e s t udi e s ha ve be e n poi nt e d out ( Edwa r ds a nd Sa va s t a no, 1998; Mus s a a nd ot he r s , 2000) .

9) Fir s t , t he y do not c ont r ol f or t he c ount r y c i r - c ums t a nc e s ( de gr e e of c a pi t a l mobi l i t y, s i z e , de gr e e of i nt e gr a t i on, a nd ma c r oe c onomi c pol i c i e s ) .

For i ns t a nc e , i n s ome c ount r i e s , t he c or r e l a t i on be t we e n i nf l a t i on a nd t he e xc ha nge r a t e wa s due t o f i s c a l i ndi s c i pl i ne r a t he r t ha n t o a n e xoge nous de c i s i on t o a dopt a f l e xi bl e e xc ha nge r a t e .

Se c ond, c l a s s i f i c a t i on of t he e xc ha nge r a t e r e gi me s us e d i n t he s e s t udi e s i s t he of f i c i a l one r e por t e d by t he c ount r i e s (

dejure) r a t he r t ha n t he a c t ua l (

defacto) r e gi me .

Asnot e d e a r l i e r , di s c r e pa nc i e s be t we e n t he t wo a r e of t e n s ubs t a nt i a l .

Thir d, t he s e s t udi e s i mpl i c i t l y a s s ume t ha t a l l e xc ha nge r a t e r e gi me s i n t he i r s a mpl e we r e s us t a i na bl e ( t ha t i s , c ons i s t e nt wi t h ma c - r oe c onomi c pol i c i e s ) a nd t ha t a l l c ha nge s i n r e gi me s we r e v ol unt a r y .

Thef our t h we a kne s s i s r e l a t e d t o r e ve r s e c a us a l i t y .

Thes e s t udi e s do not a ddr e s s t he i s s ue whe t he r f i xe d e xc ha nge r a t e s de l i ve r l ow i nf l a t i on by a ddi ng di s c i pl i ne a nd c r e di bi l i t y t o t he c onduc t of ma c r oe c onomi c pol i c i e s , or i s i t t ha t c ount r i e s wi t h l ow i nf l a t i on c hoos e pe gge d e xc ha nge r a t e s t o i ndi c a t e t he i r

7) SeeGhosh,A.R.,Gulde,A.M.,Ostry,J.D.and Wolf,H.(1996):“DoestheExchangeRate RegimeMatterforInflation and Growth”;IMF EconomicIssues2,1996.

8) A morerecentIMF study thatextendstheperiod ofanalysisto themid-1990sreportssimilarfind- ings(IMF 1997). However,in an analysisoftherecentexperiencewith increasing capitalmarket integration and thereplacementoffixed exchangeratesin the1990s,Caramazaand Aziz(1998) found thatthedifferencesin inflation and outputgrowth between fixed and flexibleregimesareno longersignificant.

9) SeeSebastian Edwards& Savastano,MiguelA.(1998):“TheMorning After:TheMexican Peso in theAftermath ofthe1994 Currency Crisis”;NBER Working Papers6516,NationalBureau ofEco- nomicResearch,Inc.

See Mussa, M., Masson, P., Swoboda, A., Jadresic, E., Mauro, P. and Berg, A. (2000):

“ExchangeRateRegimesin an Increasingly Integrated World Economy”;IMF OccasionalPaper 193,2000.

i nt e nt i on t o ma i nt a i n t he i r a nt i - i nf l a t i ona r y s t a nc e .

10)Al l ASEAN Sout h- Ea s t a nd t he de ve l ope d Nor t h- Ea s t As i a n c ount r i e s us e a f or m of a ma n- a ge d f l oa t i ng e xc ha nge r a t e s ys t e m wi t h c e r t a i n modi f i c a t i ons .

Theol d f i xe d- r a t e e xc ha nge s ys t e ms we r e a ba ndone d a nd t he f l oa t i ng s ys t e m wa s s e e n a s r e f l e c t i ng ma r ke t f or c e s r a t he r t ha n t he a r t i f i c i a l de f e nc e of a c ur r e nc y by t he gove r nme nt .

Ac ount r y t ha t di d not ne e d t o i nt e r ve ne t o s uppor t i t s c ur r e nc y woul d not ne e d t o ma i nt a i n huge f or e i gn- e xc ha nge r e s e r ve s .

On t he ot he r ha nd, t he pos t - I MF f or e i gn e xc ha nge a r r a nge me nt s a r e modi f i e d a ga i n.

Aft e r t he As i a n c r i s i s a l l As i a n e c onomi e s ga ve wa ys t o a nt i - i nf l a t i ona r y mone t a r y di s c i pl i ne .

Somea c a - de mi c s s t a r t e d t o a r gue t ha t t he f l oa t i ng- s ys t e m ha d c a us e d a l l t he wor l d’ s i l l s , a nd t ha t , i n a n y c a s e , f e w c ur r e nc i e s we r e f r e e f l oa t i ng.

11) Most As i a n c ount r i e s ha d a ‘ di r t y’ ma na ge d f l oa t i ng s ys t e m; i . e . , t he y i nt e r v e ne d whe n t he y f e l t t ha t t he c ur r e nc y wa s be l o w or a bo v e t he mone t a r y t a r ge t .

Ont he ot he r ha nd, i n a l l As i a n c ount r i e s i nt e r na t i ona l r e s e r ve s ha d

increasednot de c r e a s e d c ont r a r y t o t he a c a de mi c e xpe c t a t i ons .

Thei nf l a t i on r a t e s s e e me d t o be s i gni f i c a nt l y hi ghe r t ha n unde r t he f i xe d s ys t e m.

Curr e nc i e s be c a me de t e r mi ne d not by t he f unda me nt a l f or c e s of pur c ha s i ng powe r pa r i t y but by t he s pe c ul a t i on a nd a r bi t r a ge of t he i nt e r na t i ona l mone y ma r ke t .

Theot he r f e a t ur e of t hi s r e gi on wa s t ha t i nt e r na t i ona l t r a de be c a me ove r - whe l me d by i nt e r na t i ona l f l ows of f unds a s a de t e r mi na nt of e xc ha nge r a t e s .

Ont he ot he r ha nd, c ount e r e d s ome pr opone nt s of f r e e l y f l oa t i ng e xc ha nge r a t e s , i f go v e r nme nt s kno w be t t e r

10) Using datafrom 159 countriesforthe1974–99 period,Levy-Yeyatiand Sturzenegger(2000)reclas- sified theexchangeratesinto threegroups(float,intermediate,fixed)and estimated thecorrelation between theactual(defacto)exchangerateregimesand macroeconomicperformance. Themain findingsinclude:(a)fixed exchangerateregimesseem to haveno significantimpacton theinflation levelwhen compared with purefloats,whileintermediateregimesaretheclearunder-performers; (b)pegsaresignificantly and negatively correlated with percapitaoutputgrowth in non-industrial countries;(c)outputvolatility declinesmonotonically with thedegreeofregimeflexibility;and (d) realinterestratesappearto belowerunderfixed ratesthan underfloating ratesbecauseofthelower uncertainty associated with fixed rates. SeeLevy-Yeyatiand Sturzenegger“Classifying Exchange RateRegimes:Deedsvs.Words”,UTDT

11) Ethier,Wilfred,and Bloomfield,ArthurI.(1975),“Managing theManaged Float”,Princeton Essaysin InternationalFinanceno.112;Goodhart,Charles,and Delargy,P.J.R.(1998),“Financial Crises:PluscaChange,plusc’estlaMemeChose”,InternationalFinance1(2),261–87;Fratzscher, Marcel(1998),“TheImpactofExchangeRateRegimesand Stability on Macroeconomic Performance:An EmpiricalAnalysis”,mimeo;McKinnon,Ronald I.(2000),“AftertheCrisis,the EastAsian DollarStandard Resurrected:An Interpretation ofHigh-Frequency Exchange-Rate Pegging”,paperpresented to aconferenceoftheASEAN EconomicAssociationsin Singaporeon 7–8 September;Ortiz,Guillermo,and Agustin Carstens(2000),“TheExperiencewith aFloating ExchangeRateRegime:TheCaseofMexico”,paperpresented to aconferenceon “International FinancialMarkets:TheChallengeofGlobalization”atTexasA and M University,31 March.

t ha n t he ma r ke t whe r e a n e xc ha nge r a t e be l ongs , t he n t he y s houl d, on a ve r a ge , be a bl e t o ma ke a pr of i t by b uyi ng whe n c ur r e nc y i s unde r v a l ua t e d a nd s e l l i ng whe n c ur r e nc y i s ove r v a l ua t e d.

Ye t t he e vi de nc e de mons t r a t e d t he oppos i t e : c e nt r a l - ba nk i nt e r ve nt i on s e e me d t o be mi s t i me d, l os i ng mor e of t e n t ha n Ma l a ys i a , Tha i l a nd 1997, Ta i wa n 1998, Ma l a ys i a 1998, Si nga por e 1999.

I n Appe ndi x 1 we pr e s e nt t he mor e i mpor t a nt s ys t e ma t i c a nd i ns t i t ut i ona l f or e i gn e xc ha nge de v e l opme nt s i n As i a n c ount r i e s .

I n Tha i l a nd unde r t he ma na ge d f l oa t s ys t e m, t he va l ue of t he ba ht i s de t e r mi ne d by ma r ke t f or c e s .

Ther e f e r e nc e r a t e f or i nt e r ba nk s pot t r a ns a c t i ons i s a vol ume - we i ght e d a ve r a ge of i nt e r ba nk s pot r a t e s on t he pr e vi ous t r a di ng da y .

Ther e f e r e nc e r a t e f or c omme r c i a l ba nks ’ c ount e r t r a ns a c t i ons i s a s i mpl e a ve r a ge of t he s ubmi t t e d r a t e s a c r os s a l l c omme r c i a l ba nks on t he pr e vi ous t r a di ng da y .

Fore i gn e xc ha nge c ount e r r a t e s c ons i s t of t he buyi ng a nd s e l l i ng r a t e s f or 27 c ur r e nc i e s .

12)Some c ount r i e s , f or e xa mpl e Ta i wa n, ha v e a f l oa t i ng e xc ha nge r a t e s ys t e m i n whi c h ba nk- e r s s e t r a t e s i nde pe nde nt l y of t he a ut hor i t i e s .

TheTa i wa n a ut hor i t i e s , howe ve r , c ont r ol t he l a r ge s t ba nks a ut hor i z e d t o de a l i n f or e i gn e xc ha nge .

Fourt e e n f or e i gn ba nks a r e e nga ge d i n f or e i gn e xc ha nge bus i ne s s .

Thenumbe r of pr i va t e dome s t i c ba nks pe r mi t t e d t o de a l i n f or e i gn e xc ha nge i s s t e a di l y i nc r e a s i ng.

13)I n I ndone s i a t he gove r nme nt ha s ma i nt a i ne d t he c on ve r t i bi l i t y of t he r upi a h s i nc e t he 1960’ s .

Ther e ha ve be e n no f or e i gn e xc ha nge c ont r ol s s i nc e 1972.

Thego v e r nme nt f ol l o ws a ma na ge d f l oa t ba s e d on a ba s ke t of ma j or t r a di ng c ur r e nc i e s , i nc l udi ng t he dol l a r .

Curr e nt pol i c y i s t o ma i nt a i n t he c ompe t i t i ve ne s s of t he r upi a h t hr ough a gr a dua l de pr e c i a t i on a ga i ns t t he dol l a r , a t a r a t e of a bout 5% a ye a r .

Sinc e 21 J une 1973, Ma l a ys i a ha s a dopt e d t he f l e xi bl e e xc ha nge r a t e r e gi me .

Bank Ne ga r a Ma l a ys i a e xe r c i s e s t he opt i on t o i nt e r ve ne whe n de e me d ne c e s s a r y i n or de r t o e v e n out s ha r p e xc ha nge r a t e f l uc t ua t i ons .

12) Forexamplein Thailand,thecentralbank announced theadoption ofinflation targeting in May 2000. Thecentralbank decided to launch inflation targeting undertheexisting legalframework, whereby theMonetary Policy Board (MPB)wasfirstappointed on 5 April2000 and vested with thepowerto decidemonetary policy by theGovernor. TheBoard,with 9 members,comprised dis- tinguished externalexpertsand thetop managementofthecentralbank. TheMPB had theauthor- ity to setthedirection ofmonetary policy with pricestability astheoverriding objective,and also to refinetheinflation targeting framework to suittheThaieconomy.

13) Taiwan’sCentralBank ofChina(CBC)intervenesin theforeign exchangemarketwhen itfeelsthat speculation or“drasticfluctuations”in theexchangeratemay impairnormalmarketadjustments. Two toolstheCBC usesto influencetheforeign exchangemarketarerestrictionson banks’over- boughtand oversold positionsand limitson banks’foreign liabilities. TheCBC also limitstheuse ofderivativeproductsdenominated in New Taiwan dollars.

Si nc e mi d- J ul y 1997, Ba nk Ne ga r a ha d a l l owe d t he r i nggi t t o be de t e r mi ne d by ma r ke t f or c e s , but s t a r t e d i nt e r ve ni ng a ga i n i n e a r l y J a nua r y 1998 i n or de r t o s t op ma r ke t pa ni c , f ol l ow- i ng t he f r e e f a l l of t he r upi a h.

In mone y ma r ke t i nt e r ve nt i ons , t he c e nt r a l ba nk ha s ha d t o e xe r - c i s e gr e a t c a r e t o e ns ur e t ha t t he t i mi ng of t he i nt e r ve nt i ons i s j us t r i ght , whi c h i s not a l wa ys e a s y t o a c hi e v e .

Kor e a ’ s c a s e i s pa r t i c ul a r l y i mpor t a nt f or ot he r Sout h- Ea s t As i a n e c onomi e s .

Kore a ’ s e xc ha nge r a t e s ys t e m i s a f r e e - f l oa t i ng s ys t e m.

At ot a l of 29 e xc ha nge r a t e s of t he Kor e a n Won a ga i ns t ot he r c ur r e nc i e s a r e di s s e mi na t e d no w, i n v ol vi ng t he U. S.

Doll a r , J a pa ne s e Ye n, Eur o ( a nd i t s me mbe r c ount r i e s ’ c ur r e nc i e s ) , Br i t i s h Pound, Si nga por e Dol l a r , Tha i Bha t , a nd s o on.

Excha nge r a t e s of t he Kor e a n Won a ga i ns t t he U. S.

Doll a r a r e obt a i ne d f r om a c t ua l f or - e i gn e xc ha nge t r a ns a c t i ons be t we e n f or e i gn e xc ha nge ba nks t hr ough f or e i gn e xc ha nge br oke r c ompa ni e s .

Excha nge r a t e s of t he Kor e a n won a ga i ns t ot he r c ur r e nc i e s a r e a ut oma t i c a l l y de t e r - mi ne d i n r e l a t i on t o t he e xc ha nge r a t e of t he U. S.

Doll a r a ga i ns t t he s e c ur r e nc i e s i n t he i nt e r na - t i ona l f or e i gn e xc ha nge ma r ke t .

TheBa nk of Kor e a di s s e mi na t e s t he e xc ha nge r a t e da t a a s a s e r vi c e t o t he publ i c , but t he da t a a r e or i gi na l l y pr ovi de d by f or e i gn e xc ha nge br oke r c ompa ni e s .

I n t he 1980s , t he e xc ha nge r a t e de t e r mi na t i on i n Kor e a ha d be e n gr e a t l y i nf l ue nc e d by gov- e r nme nt di s c r e t i on.

In a s ma l l ope n e c onomy , whi c h r e l i e s he a vi l y on i nt e r na t i ona l t r a de f or i t s gr o wt h, t he c ur r e nt a c c ount i s a ma j or c ont r ol v a r i a bl e us e d by t he gove r nme nt t o ma i nt a i n ma c r oe c onomi c s t a bi l i t y .

Kore a wa s no e xc e pt i on t o t hi s s t yl i z e d f a c t .

Ass uc h, t he Kor e a n gove r nme nt ha d f r e que nt l y i nt e r ve ne d i n t he f or e i gn e xc ha nge ma r ke t t o a t t a i n a de s i r e d l e ve l of t he c ur r e nt a c c ount ba l a nc e .

Ther e a l e f f e c t i ve e xc ha nge r a t e i s a t r a de we i ght e d a ve r a ge of r e a l e xc ha nge r a t e s of Kor e a ’ s ma j or t r a di ng pa r t ne r s a nd ha s be e n c ons i de r e d a s a us e f ul i ndi c a t or f or a c ount r y’ s pr i c e c ompe t i t i ve ne s s i n t he gl oba l ma r ke t .

If t he r e a l e f f e c t i ve e xc ha nge r a t e f a l l s , i t i mpl i e s t ha t t he Kor e a n won de pr e c i a t e s a ga i ns t t he c ur r e nc i e s of ma j or t r a di ng pa r t ne r s , t he r e by i nc r e a s i ng t he pr i c e c ompe t i t i ve ne s s of Kor e a n pr oduc t s i n t he wor l d ma r ke t .

The f a c t t ha t gove r nme nt di s c r e t i on ha s di s a ppe a r e d i n t he 1990s i s ma i nl y a t t r i b ut a bl e t o

t he i nt r oduc t i on of t he Ma r ke t Ave r a ge Exc ha nge Ra t e Sys t e m i n Ma r c h 1990.

Unli ke ot he r

pa s t e xc ha nge r a t e s ys t e ms , t hi s s ys t e m, t o a s ubs t a nt i a l de gr e e , l e f t t he e xc ha nge r a t e t o be

de t e r mi ne d by ma r ke t f or c e s .

Conse que nt l y , i t ha s c ont r i but e d s i gni f i c a nt l y t o t he e f f i c i e nt

f unc t i oni ng of t he f or e i gn e xc ha nge ma r ke t .

Neve r t he l e s s , i t f a i l e d t o r e move a l l t he ma r ke t

i ne f f i c i e nc y a s i t s t i l l l i mi t e d da i l y e xc ha nge r a t e f l uc t ua t i ons .

In f a c t , t he da i l y e xc ha nge r a t e

ba nd ma i nt a i ne d unt i l De c e mbe r 15, 1997 ha s pr ovi de d a r oom f or t he e xc ha nge r a t e t o be pe r -

s i s t e nt l y mi s a l i gne d, pa r t i c ul a r l y i n t he l a t e r pe r i ods of t he 1990s .

14)Tr a de - r e l a t e d f unds f l o w f r e e l y i nt o a nd out of Ta i wa n.

Alt hough Ta i wa n r e l a xe d s ome r e s t r i c t i ons on c a pi t a l a c c ount t r a ns a c t i ons i n 1995, mos t not a bl y r e s t r i c t i ons on por t f ol i o i nve s t - me nt s , i t s t i l l ma i nt a i ns a r a nge of c ont r ol s on i nwa r d a nd out wa r d c a pi t a l f l ows t ha t l i mi t de ma nd f or t he Ne w Ta i wa n Dol l a r a nd r e duc e upwa r d pr e s s ur e s on i t s v a l ue .

The da i l y e xc ha nge r a t e ba nd unde r t he Ma r ke t Ave r a ge Exc ha nge Ra t e Sys t e m a s s ume d a s i mi l a r r ol e i n Kor e a by ma ki ng t he e xc ha nge r a t e move me nt s s t a bl e .

Alt hough t he s t a bl e e xc ha nge r a t e move me nt s pl a y a pos i t i ve r ol e i n a t t r a c t i ng f or e i gn c a pi t a l , c a pi t a l i nf l o ws t e nd t o put upwa r d pr e s s ur e s on t he r e a l va l ue of t he dome s t i c c ur r e nc y.

This ha s i nde e d ha ppe ne d i n Kor e a .

Thec ont i nui ng i nc r e a s e i n c a pi t a l i nf l o w i n t he 1990s wa s a c c ompa ni e d by pe r s i s - t e nt r e a l a ppr e c i a t i on of t he Kor e a n won a s t he r e a l e xc ha nge r a t e c ont i nue d t o de c l i ne ove r t i me .

In r e t r os pe c t , t he pr e s s ur e s f or f ut ur e de pr e c i a t i on of t he nomi na l won/ dol l a r e xc ha nge r a t e a ppe a r t o ha ve bui l t up a s l a t e a s 1996.

Thegr owt h r a t e of Kor e a n e xpor t s de c l i ne d dr a ma t i c a l l y f r om 31. 5% i n 1995 t o 4. 1% i n 1996.

Thema r ke t ma y ha ve i nt e r pr e t e d t hi s de c l i ne i n e xpor t s a s a s i gna l t ha t t he c ur r e nt a c c ount de f i c i t of 4. 8% i n GDP woul d not be s us t a i na bl e .

Simi l a r l y, t he e xt e r na l l i a bi l i t y t o e xpor t s a l mos t doubl e d t o 125. 3% i n 1996 f r om 63. 6% i n 1995.

15)4. Mac r oe c onomi c be ne f i t s and di s advant age s of f or e i gn e xc hange r at e s ys t e ms

4. 1

Operationalcurrencysystemsin world economyThe e xpe r i e nc e s wi t h i mpl e me nt a t i on of t he e xc ha nge r a t e s ys t e ms ma y s ugge s t s ome ge n- e r a l i z a t i ons a bout t he c ondi t i ons unde r whi c h v a r i ous r e gi me s woul d f unc t i on r e a s ona bl y we l l

— t hough t he r e a r e ma ny e xc e pt i ons .

Thef l oa t i ng s ys t e ms , i t wa s s ugge s t e d, woul d be a n

14) Thedaily exchangerateband undertheMarketAverageExchangeRateSystem assumed asimilar rolein Koreaby making theexchangeratemovementsstable. Although thestableexchangerate movementsplay apositiverolein attracting foreign capital,capitalinflowstend to putupward pres- sureson therealvalueofthedomesticcurrency. Thishasindeed happened in Korea. Thecon- tinuing increasein capitalinflow in the1990swasaccompanied by persistentrealappreciation of theKorean won astherealexchangeratecontinued to declineovertime. In retrospect,thepres- suresforfuturedepreciation ofthenominalwon/dollarexchangerateappearto havebuiltup aslate asin 1996. Thegrowth rateofKorean exportsdeclined dramatically from 31.5% in 1995 to 4.1%

in 1996. Themarketmay haveinterpreted thisdeclinein exportsasasignalthatthecurrent accountdeficitof4.8% in GDP would notbesustainable. Similarly,theexternalliability to exportsalmostdoubled to 125.3% in 1996 from 63.6% in 1995.

15) SeeMacrostatisticsforKorea. Ministry ofFinanceData,2001.

a ppr opr i a t e c hoi c e f or me di um a nd l a r ge i ndus t r i a l i z e d c ount r i e s a nd s ome e me r gi ng ma r ke t e c onomi e s t ha t ha ve i mpor t a nd e xpor t s e c t or s t ha t a r e r e l a t i ve l y s ma l l c ompa r e d t o GDP , b ut a r e f ul l y i nt e gr a t e d i nt o t he gl oba l c a pi t a l ma r ke t s a nd ha v e di v e r s i f i e d pr oduc t i on a nd t r a de , a de e p a nd br oa d f i na nc i a l s e c t or , a nd s t r ong pr ude nt i a l s t a nda r ds .

Ont he ot he r ha nd, t he ha r d pe g s ys t e m s e e ms t o be mor e a ppr opr i a t e f or c ount r i e s s a t i s f yi ng t he opt i mum c ur r e nc y a r e a c r i t e r i a ( c ount r i e s i n t he Eur ope a n Ec onomi c a nd Mone t a r y Uni on) , s ma l l c ount r i e s a l r e a dy i nt e - gr a t e d i nt o a l a r ge r ne i ghbor i ng c ount r y ( dol l a r i z a t i on i n Pa na ma ) , or c ount r i e s wi t h a hi s t or y of mone t a r y di s or de r , hi gh i nf l a t i on, a nd l o w c r e di bi l i t y of pol i c yma ke r s t o ma i nt a i n s t a bi l i t y a nd t ha t ne e d a s t r ong a nc hor f or mone t a r y s t a bi l i z a t i on ( c ur r e nc y boa r d i n Ar ge nt i na a nd Bul ga r i a ) . Pos s i bl y , t he s of t pe g r e gi me s woul d be be s t f or c ount r i e s wi t h l i mi t e d l i nks t o i nt e r na t i ona l c a pi t a l ma r ke t s , l e s s di ve r s i f i e d pr oduc t i on a nd e xpor t s , a nd s ha l l o w f i na nc i a l ma r ke t s , a s we l l a s c ount r i e s s t a bi l i z i ng f r om hi gh a nd pr ot r a c t e d i nf l a t i on unde r a n e xc ha nge r a t e - ba s e d s t a bi l i - z a t i on pr ogr a m ( Tur ke y) .

Thes e a r e l a r ge l y but not e xc l us i ve l y non- e me r gi ng ma r ke t de ve l op- i ng c ount r i e s .

Thei nt e r me di a t e r e gi me s , a mi ddl e r oa d be t we e n f l oa t i ng r a t e s a nd s of t pe gs , ai m t o i ncor por at e t he benef i t s of f l oat i ng and pegged r egi mes whi l e avoi di ng t hei r s hor t c omi ngs .

They a r e be t t e r s ui t e d f or e me r gi ng ma r ke t e c onomi e s a nd s ome ot he r de ve l op- i ng c ount r i e s wi t h r e l a t i ve l y s t r onge r f i na nc i a l s e c t or a nd t r a c k r e c or d f or di s c i pl i ne d ma c - r oe c onomi c pol i c y .

16)4. 2

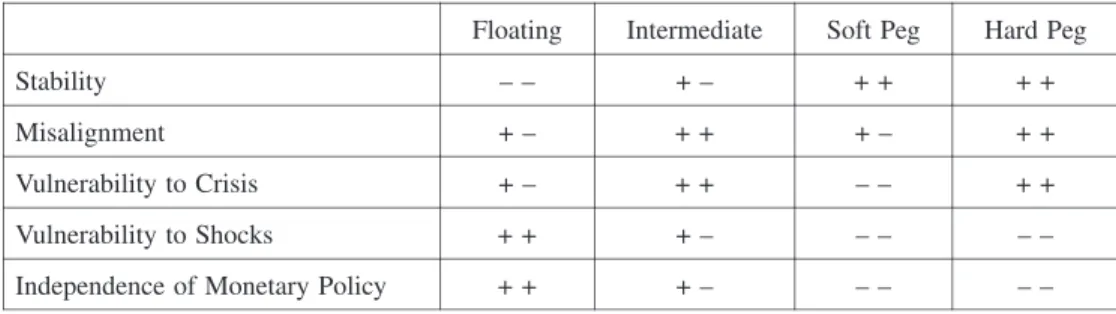

Advantagesand DisadvantagesofForexsystemsAs i ndi c a t e d e a r l i e r i n t hi s s t udy , a l l e xc ha nge r a t e r e gi me s of f e r di f f e r i ng be ne f i t s a s we l l a s c os t s ( s e e Ta bl e 1) .

The ma i n a dv a nt a ge s of t he f l oa t i ng r e gi me s a r e t he i r r e l a t i ve i n vul ne r a bi l i t y t o c ur r e nc y c r i s i s , a nd t he i r a bi l i t y t o a bs or b a dve r s e s hoc ks a nd pur s ue a n i nde pe nde nt mone t a r y pol i c y .

The s e a dva nt a ge s c ome wi t h t he c os t of hi gh s hor t - t e r m e xc ha nge r a t e vol a t i l i t y a nd l a r ge me di um- t e r m s wi ngs c ha r a c t e r i z e d by mi s a l i gnme nt .

Att he ot he r e nd of t he s pe c t r um, t he ha r d pe g r e gi me s pr ovi de ma xi mum s t a bi l i t y a nd c r e di bi l i t y f or mone t a r y pol i c y, a nd l ow t r a ns -

16) Dollarization isagenericnameused to mean thereplacementofanationalcurrency by aforeign currency aslegaltender,which would refernotonly to theuseofthedollar,butalso forinstanceto theuseoftherand,franc,etc. A notableexception isDenmark which isin theEurope’sExchange RateMechanism (ERM)and isthuspegging within aband. Mussa,M.,Masson,Swoboda,P.,Jad- resic,A.E.,Mauro,P.and Berg,A.“ExchangeRateRegimesin an Increasingly Integrated World Economy”,IMF OccasionalPaper193,2000. McKinnon,R.I.,“Euroland and Asiain aDollar- Based InternationalMonetary System:MundellRevisited”,1999.

a c t i on c os t s a nd i nt e r e s t r a t e s , but s uf f e r f r om t he l os s of l e nde r of l a s t r e s or t r ol e of t he c e nt r a l ba nk a nd s e i gni or a ge r e ve nue .

Twobi g a dva nt a ge s of t he s of t pe g r e gi me s a r e t ha t t he y ma i n- t a i n s t a bi l i t y a nd r e duc e t r a ns a c t i on c os t s a nd t he e xc ha nge r a t e r i s k whi l e pr o vi di ng a nomi na l a nc hor f or mone t a r y pol i c y.

Thes e a dva nt a ge s ha ve be e n unde r mi ne d by a s ubs t a nt i a l i nc r e a s e i n gl oba l c a pi t a l mobi l i t y i n t he 1990s .

Thes of t pe g r e gi me s , i n c ount r i e s ope n t o i nt e r na - t i ona l c a pi t a l f l o ws , a r e i nhe r e nt l y vul ne r a bl e t o c ur r e nc y c r i s e s .

Bygi vi ng up s ome nomi na l s t a bi l i t y f or gr e a t e r f l e xi bi l i t y , t he i nt e r me di a t e r e gi me s a i m t o ge t t he be s t of bot h wor l ds : t o pr ovi de a l i mi t e d nomi na l a nc hor f or i nf l a t i ona r y e xpe c t a t i ons , but a l s o a voi d vol a t i l i t y a nd ove r v a l ua t i on, a nd r e duc e t he r i s k of c ur r e nc y c r i s i s by r e s t or i ng t he t wo- wa y be t f or s pe c ul a - t or s wi t h br oa d s of t ba nds .

Ani mpor t a nt c ons e ns us on t he c hoi c e of e xc ha nge r a t e r e gi me s i s t ha t no s i ngl e e xc ha nge r a t e r e gi me i s be s t f or a l l c ount r i e s or a t a l l t i me s ( Fr a nke l 1999, Mus s a a nd ot he r s 2000, i bi de m) .

Thec hoi c e woul d v a r y de pe ndi ng on t he s pe c i f i c c ount r y c i r c um- s t a nc e s a t t he t i me pe r i od i n que s t i on ( t he s i z e a nd ope nne s s of t he c ount r y t o t r a de a nd f i na n- c i a l f l ows , s t r uc t ur e of i t s pr oduc t i on a nd e xpor t s , s t a ge of i t s f i na nc i a l de ve l opme nt , i t s i nf l a t i ona r y hi s t or y , a nd t he na t ur e a nd s our c e of pot e nt i a l s hoc ks i t f a c e s ) , a nd t he c ount r y’ s pol i c y obj e c t i ve s whi c h woul d i n vol ve t r a de - of f s .

Theul t i ma t e c hoi c e woul d be de t e r mi ne d by t he r e l a t i ve we i ght s gi ve n t o t he s e f a c t or s . .

In s e l e c t i ng t he opt i mum de gr e e of f l e xi bi l i t y ma c r oe c onomi c pol i c y ma ke r s us ua l l y pl a c e hi ghe r we i ght s on t hi ngs t ha t woul d mi ni mi z e s hor t t e r m s oc i o- e c onomi c c os t s .

17)I n f l oa t i ng r e gi me s , t he r e a l a nd nomi na l e xc ha nge r a t e s a r e e ndoge nous v a r i a bl e s de t e r - mi ne d i n t he ma r ke t by de ma nd a nd s uppl y .

Thegove r nme nt a nd t he mone t a r y a ut hor i t y do

17) Frankel,J.A.,“No singleCurrency RegimeisRightforallCountriesoratallTimes”,NBER 1999.

Frankel,J.,E.Fajnzylber,S.Schmukler,and L.Serven,“Verifying ExchangeRateRegimes”,May 2000;Mussa,M.,P.Masson,A.Swoboda,E.Jadresic,P.Mauro,and A.Berg,“ExchangeRate Regimesin an Increasingly Integrated World Economy”,IMF OccasionalPaper193,2000.

Table1 Main Trade-OffsWhen Selecting an ExchangeRateSystem in an Open Economy Hard Peg SoftPeg

Intermediate Floating

+ + + +

+ – – –

Stability

+ + + –

+ + + –

Misalignment

+ + – –

+ + + –

Vulnerability to Crisis

– – – –

+ – + +

Vulnerability to Shocks

– – – –

+ – + +

IndependenceofMonetary Policy

not de t e r mi ne wha t t he r a t e s houl d be a nd do not ma ke a ny e f f or t t o gui de t he r a t e t o wa r ds a de s i r e d l e ve l or z one .

Epis odi c a nd a d hoc i nt e r ve nt i ons i n a l i ght l y ma na ge d r e gi me a r e i n t he s pi r i t of “ l e a ni ng a ga i ns t t he wi nd” .

They a i m t o s l ow t he e xc ha nge r a t e move me nt s a nd da mpe n e xc e s s i v e f l uc t ua t i ons , a nd a r e not i nt e nde d t o de f e nd a n y pa r t i c ul a r r a t e or z one .

I n c ont r a s t , i n a l l ot he r r e gi me s ( wi t h t he e xc e pt i on of a c ur r e nc y uni on/ dol l a r i z a t i on whe r e t he na t i ona l c ur r e nc y i s gi ve n up a l t oge t he r ) , t he gove r nme nt ne e ds t o ha ve a n i de a whe r e t he r e a l e xc ha nge r a t e s houl d be t o e ns ur e t ha t t he na t i ona l e c onomy i s c ompe t i t i ve .

Typic a l l y, t he l ong- r un e qui l i br i um r e a l e xc ha nge r a t e i s e s t i ma t e d ba s e d on t he e c onomi c f unda me nt a l s of t he c ount r y , a nd a v a r i e t y of pol i c y a nd i ns t i t ut i ona l a r r a nge me nt s a r e ma de t o ke e p t he a c t ua l r a t e s uf f i c i e nt l y c l os e t o i t o v e r t he me di um- t e r m.

18)The c l a s s i f i c a t i on of f or e i gn e xc ha nge r a t e s ys t e ms i s pr e s e nt e d i n Ta bl e 2.

This i s t he f unc t i ona l br e a kdo wn of t he s ys t e ms a c c or di ng t o t he me t hodol ogy pr opos e d by St a nl e y Fi s he r of t he I MF .

Whi l e t he i nde pe nde nt l y f l oa t i ng wa s t he ma i n f e a t ur e of t he de v e l ope d ma r ke t e c onomi e s ( i nc l udi ng J a pa n) , t he e me r gi ng de ve l opi ng e c onomi e s di s pl a y a mor e s t r uc t ur e d pa t t e r n ( s e e Ta bl e 3) .

The pi c t ur e be c ome s c l e a r e r i f we gr oup t he s e e c onomi e s i nt o a ppr opr i a t e c a t e gor i e s ( s e e Ta bl e 4 a nd 5) .

Ac c or di ng t o Ta bl e 4, t he mos t c ommon s ys t e m s e e ms t o be i nde pe nde nt f l oa t i ng ( 13 e c onomi e s ) , t he n ot he r c on ve nt i ona l f i xe d pe gs ( 7 e c onomi e s ) , c r a wl i ng ba nds e xc ha nge r a t e s ( 5 e c onomi e s ) , a nd c ur r e nc y boa r ds ( 3 e c onomi e s ) .

The “ r e s t of t he wor l d” di s pl a ye d a s i gni f i c a nt l y di f f e r e nt pa t t e r n ( s e e Ta bl e 5) .

Her e t he c ur r e nc y boa r d a nd ot he r a r r a nge me nt s wi t hout a s e pe r a t e l e ga l t e nde r pr e domi na t e .

Thef i xe d pe gs f ol l ow a nd t he ma na ge d f l oa t i s muc h l e s s pr a c t i c e d.

Inde pe nde nt f l oa t i ng i s us e d by l e s s

18) Activemanagementoftheexchangerateundertheseregimescan provideadeveloping country with an additionalstrong policy toolto correctmisalignmentand to influencethebalanceofpay- ments,tradeflows,investment,and production. Theearlierdebateaboutexchangerateregimes waslargely abouttheirinfluenceon monetary disciplineand credibility,and thetrade-offbetween flexibility and credibility. Floating regimesprovidemaximum discretion formonetary policy,but discretion comeswith theproblem oftime-inconsistency. Thatis,ifagovernmenttendsto misuse itsdiscretion and cannotkeep itspromiseoflow inflation today,itwillbedifficultto getpeopleto believeitsfuturepolicy announcements. Therefore,restraintsneed to beputon governmentto ensurethatdiscretion isnotmisused and economicpolicesareconsistentand sustainableand that thereisnotgoing to beinflation.(SeeforexampleP.Krugman remarksofopen marketeconomies, ibidem)

t ha n 20% of a l l c ount r i e s unde r r e vi e w.

I t wa s ge ne r a l l y a gr e e d t ha t f l oa t i ng r e gi me s woul d ha ve a n i nf l a t i ona r y bi a s , a nd t ha t t he de gr e e of di s c i pl i ne a nd c r e di bi l i t y woul d i nc r e a s e wi t h a de c l i ne of f l e xi bi l i t y.

Thema i n a r gu- me nt i n f a vor of f i xe d r a t e s wa s t he i r a bi l i t y t o i nduc e di s c i pl i ne a nd ma ke t he mone t a r y pol i c y mor e c r e di bl e be c a us e a dopt i on of l a x mone t a r y ( a nd f i s c a l ) pol i c y woul d e v e nt ua l l y l e a d t o a n e xha us t i on of r e s e r ve s a nd c ol l a ps e of t he f i xe d e xc ha nge r a t e s ys t e m i mpl yi ng a bi g pol i t i c a l c os t f or t he pol i c y ma ke r s .

Thena t ur e of de ba t e ha s c ha nge d s i gni f i c a nt l y wi t h t he s t e a dy i nc r e a s e i n i nt e r na t i ona l c a pi t a l f l ows .

Soft pe g r e gi me s i n a numbe r of e me r gi ng ma r ke t e c onomi e s ope n t o gl oba l f i na nc i a l ma r ke t s ha ve c ol l a ps e d i n t he 1990s .

Dif f i c ul t y i n ma i n- t a i ni ng c r e di bi l i t y unde r s of t pe gs whe n t he c a pi t a l a c c ount i s ope n i s a ke y f a c t or t ha t br ought

Table2 Forex Systemsin Developed MarketEconomies(pre-Euro) Exchange Arrangement OtherArea

countries Exchange

Arrangement Euro Area

countries

IF Australia

NS Austria

IF Canada

NS Belgium

HB Denmark

NS Finland

CBA Hong Kong

NS France

IF Japan

NS Germany

IF New Zealand

NS Ireland

MF Norway

NS Italy

MF Singapore

NS Netherlands

IF Sweden

NS Portugal

IF Switzerland

NS Spain

IF United States

IF United Kingdom

Note:Economieslisted in theMSCIDeveloped Marketsindex.

Key:

NS = Arrangementswith no separatelegaltender CBA = Currency board

FP = Otherconventionalfixed pegs HB = Pegged ratein horizontalband CP = Crawling peg

CB = Rateswithin crawling bands

MF = Managed floatwith no pre-announced exchangeratepath IF = Independently floating

Source:IMF,AnnualReport2000

Table3 Forex systemsin Emerging MarketEconomies

Exchange Arrangemen Latin

America Exchange

Arrangemen Europe&

MiddleEast Exchange

Arrangemen Asia

Exchange Arrangemen Africa

CBA Argentina

CBA Bulgaria

FP China

FP Morocco

IF Brazil

MF Czech Republi IF

India MF

Nigeria

IF Chile

FP Egypt

IF Indonesia

IF South Africa

IF Colombia HB

Greece IF

Korea

IF/NS Ecuador

CB Hungary

FP Malaysia

IF Mexico

CB Israel

FP Pakistan

NS Panama

FP Jordan

IF Philippines

IF Peru

CB Poland

CB SriLanka

CB Venezuela FP

Qatar MF

Taiwan

IF Russia

IF Thailand

CP Turkey

Note:Economieslisted eitherand/orin theMSCIEmerging Marketsand EMBI+ indices. Key:Every key isthesameasin theTable2.

Source:IMF,AnnualReport2000

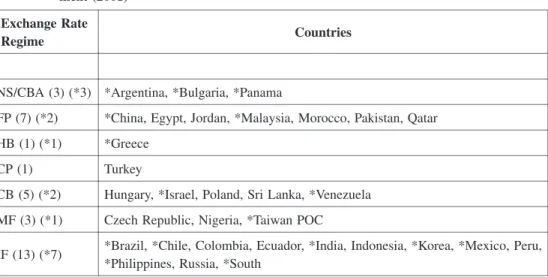

Table4 Forex Systemsin Emerging MarketCountriesGrouped by ExchangeRateArrange- ment(2001)

Countries ExchangeRate

Regime

*Argentina,*Bulgaria,*Panama NS/CBA (3)(*3)

*China,Egypt,Jordan,*Malaysia,Morocco,Pakistan,Qatar FP (7)(*2)

*Greece HB (1)(*1)

Turkey CP (1)

Hungary,*Israel,Poland,SriLanka,*Venezuela CB (5)(*2)

Czech Republic,Nigeria,*Taiwan POC MF (3)(*1)

*Brazil,*Chile,Colombia,Ecuador,*India,Indonesia,*Korea,*Mexico,Peru,

*Philippines,Russia,*South IF (13)(*7)

Note:* indicatescountry whoseweightin eithertheEMBI+ orMSCIindex is2% orgreater. Numbersin parenthesisindicatenumberofcountriesin each group;asterisked numbersareself- explanatory.

Key:Every key isthesameasin theTable2.

Source:IMF,AnnualReport2000

t he s e pe gs down.

Toa c hi e ve c r e di bi l i t y qui c kl y , s ome a ut hor s a r gue d t ha t t he s e c ount r i e s ne e d t o mo v e e i t he r t o ha r d pe gs or f l oa t i ng r a t e s .

4. 3

Balancebetween exchangeratestabilityand flexibilityI ns t i t ut i ona l l y bi ndi ng mone t a r y a r r a nge me nt s unde r ha r d pe gs t i e a gove r nme nt ’ s ha nds t o pr ovi de i r r e ve r s i bl e f i xe d r a t e s a nd ma i nt a i n ma xi mum c r e di bi l i t y .

Thel ong- r un e qui l i br i um r e a l e xc ha nge r a t e i s t he r e a l r a t e t ha t , f or gi ve n va l ue s of “ e c onomi c f unda me nt a l s ” ( ope nne s s , pr oduc t i vi t y di f f e r e nt i a l s , t e r ms of t r a de , publ i c e xpe ndi t ur e , di r e c t f or e i gn i n v e s t me nt , i nt e r na - t i ona l i nt e r e s t r a t e s , e t c . ) i s c ompa t i bl e wi t h t he s i mul t a ne ous a c hi e ve me nt of i nt e r na l a nd e xt e r - na l e qui l i br i a .

The ot he r wa y t o s ol ve t he c r e di bi l i t y pr obl e m i s t o f l oa t t he c ur r e nc y: t ha t i s , not ma ke a ny pr omi s e s a bout t he e xc ha nge r a t e a t a l l .

Thef l oa t i ng r e gi me s ma y e xhi bi t hi gh s hor t - t e r m e xc ha nge r a t e vol a t i l i t y a nd me di um- t e r m s wi ngs t ha t a r e onl y we a kl y r e l a t e d t o e c onomi c f unda me nt a l s .

This i s l a r ge l y e xpl a i ne d by t he f a c t t ha t t he e xc ha nge r a t e i s a l s o a n a s s e t pr i c e

Table5 Forex Systemsin AllOtherCountriesGrouped by ExchangeRateArrange- ments,2001

Countries ExchangeRate

Regime

Antiguaand Barbuda,Benin,Bosniaand Herzegovina,BruneiDarussalam, BurkinaFaso,Cameroon,CentralAfrican Rep.,Chad,Congo (Rep.of),Côte d’Ivoire,Djibouti,Dominica,

NS/CBA (31)

Aruba,Bahamas,Bahrain,Bangladesh,Barbados,Belize,Bhutan,Botswana, CapeVerde,Comoros,ElSalvador,Fiji,Iran,Iraq,Kuwait,Latvia,Lebanon, Lesotho,Macedonia

FP (38)

Cyprus,Iceland,Libya,Vietnam HB (4)

Bolivia,CostaRica,Nicaragua,Tunisia CP (4)

Honduras,Uruguay CB (2)

Algeria,Azerbaijan,Belarus,Burundi,Cambodia,Croatia,Dominican Rep., Ethiopia,Guatemala,Jamaica,Kenya,KyrgyzRepublic,Lao PDR,Malawi, Mauritania,Paraguay,

MF (23)

Afghanistan,Albania,Angola,Armenia,Congo (Dem.Rep.),Eritrea,Gambia, Georgia,Ghana,Guinea,Guyana,Haiti,Kazakhstan,Liberia,Madagascar,Mau- ritius,Moldova,

IF (29)

Key:Every key isthesameasin theTable2.

Source:IMF,AnnualReport2000

i nf l ue nc e d s t r ongl y by s hor t - t e r m f i na nc i a l f l ows whi c h a r e s ubj e c t t o s pe c ul a t i on, ma ni a s , pa n- i c s , he r di ng, a nd c ont a gi on.

Asc a pi t a l ma r ke t i nt e gr a t i on de e pe ns , c a pi t a l ma r ke t t r a ns a c t i ons i nc r e a s i ngl y domi na t e c ha nge s i n e xc ha nge r a t e s .

Det e r mi ne d i n t hi s ma nne r , e xc ha nge r a t e s ma y de ve l op t he i r o wn s hor t - t e r m a nd me di um- t e r m dyna mi c s t ha t ove r whe l m t he goods a nd s e r vi c e s ma r ke t t r a ns a c t i ons .

Vola t i l i t y i s s ubs t a nt i a l l y hi ghe r i n de ve l opi ng c ount r i e s wi t h t hi n f or e i gn e xc ha nge ma r ke t s us ua l l y domi na t e d by a r e l a t i ve l y s ma l l numbe r of ma r ke t pa r t i c i - pa nt s , a nd ma y be c ompounde d by a l a c k of pol i t i c a l s t a bi l i t y a nd di s c i pl i ne d ma c r oe c onomi c e n vi r onme nt .

I n a wor l d wi t h hi gh c a pi t a l mobi l i t y, e ve n s ma l l a dj us t me nt s i n i nt e r na t i ona l por t f ol i o a l l o- c a t i ons t o de ve l opi ng e c onomi e s c a n r e s ul t i n l a r ge s wi ngs i n c a pi t a l f l ows c r e a t i ng l a r ge vol a t i l - i t y i n e xchange r at es .

Because t hei r f i nanci al mar ket s ar e poor l y de vel oped, hedgi ng pos s i bi l i t i e s a r e l i mi t e d i n de ve l opi ng c ount r i e s .

High e xc ha nge r a t e v ol a t i l i t y c r e a t e s unc e r - t a i nt y , i nc r e a s e s t r a ns a c t i on c os t s a nd i nt e r e s t r a t e s , di s c our a ge s i nt e r na t i ona l t r a de a nd i n ve s t - ment , and f uel s i nf l at i on.

Themedi um- t er m s wi ngs ar e i dent i f i ed wi t h s ubs t ant i al mi s a l i gnme nt .

This i s a pa r t i c ul a r l y s e r i ous c onc e r n f or de ve l opi ng c ount r i e s be c a us e pe r s i s - t e nt r e a l e xc ha nge r a t e vol a t i l i t y a nd mi s a l i gnme nt ha ve be e n a s s oc i a t e d wi t h uns us t a i na bl e t r a de de f i c i t s , a nd l o we r e c onomi c gr o wt h ove r t he me di um a nd l ong r un ( Ghur a a nd Gr e nne s 1993, Ra z i n a nd Col l i ns 1997, El ba da wi 1998, Wor l d Ba nk 2000) .

19)Pe r s i s t e nt ove r v a l ua t i on i s us ua l l y i de nt i f i e d a s a s t r ong e a r l y wa r ni ng f or c ur r e nc y c r i s i s ( Ka mi ns ky a nd ot he r s 1998) .

It i s a l s o r e c ogni z e d t ha t , wi t h hi gh v ol a t i l i t y i n e xc ha nge r a t e , i t i s ve r y ha r d t o de ve l op l ong- t e r m dome s t i c f i na nc i a l ma r ke t s .

Thede gr e e of vol a t i l i t y of t he nomi na l e xc ha nge r a t e de c r e a s e s a s one move s a l ong t he e xc ha nge r a t e s pe c t r um t owa r ds de c r e a s i ng f l e xi bi l i t y .

Theha r d pe g r e gi me s wi t h t he i r s t r ong a nd c r e di bl e i ns t i t ut i ona l a r r a nge me nt s gua r a nt e e nomi na l e xc ha nge r a t e s t a bi l i t y.

Under a c ur r e nc y boa r d a r r a nge me nt , s uc c e s s f ul l y a l i gni ng t he e xc ha nge r a t e t o a l a r ge a nd s t a bl e c ount r y mi ni mi z e s e xc ha nge r a t e r i s k, a nd e nc our a ge s i nt e r na t i ona l t r a de a nd i n ve s t me nt .

If c ount r y c i r c ums t a nc e s a l l ow i t , goi ng one s t e p f ur t he r a nd a c t ua l l y a dopt i ng t he ne i ghbor ’ s c ur r e nc y a s one ’ s own, woul d e l i mi - na t e t r a ns a c t i ons c os t a s we l l pr omot i ng f ur t he r t r a de a nd i n ve s t me nt .

Thes of t pe g r e gi me s c a n ma i nt a i n s t a bl e a nd c ompe t i t i ve e xc ha nge r a t e s onl y i f t he a ut hor i t i e s s e t t he r a t e a t a

19) World Bank,“GlobalEconomicProspectsand theDeveloping Countries”,Washington DC,2000.

27;Ghura,D.and Grennes,T.“TheRealExchangeRateand MacroeconomicPerformancein Sub- Saharan Africa”,JournalofDevelopmentEconomics,Vol.42:155–174,October1993;Elbadawi, I.,“RealExchangeRatePolicy and Non-TraditionalExportsin Developing Countries”,WIDER, TheUN University,Helsinki.

s us t a i na bl e l e ve l c ons i s t e nt wi t h t he e c onomi c f unda me nt a l s a nd c onvi nc e t he ma r ke t s wi t h di s - c i pl i ne d ma c r oe c onomi c pol i c i e s a nd c r e di bl e i ns t i t ut i ons of t he i r a bi l i t y t o ke e p i t t he r e .

How-e ve r , t he y c a n not gua r a nt e e a n a bs e nc e of mi s a l i gnme nt , pa r t i c ul a r l y i n c ount r i e s ope n t o i nt e r na t i ona l c a pi t a l f l o ws .

Ass ho wn s o ma ny t i me s i n t he pa s t , l a c k of mone t a r y a nd f i s c a l di s c i pl i ne , i na ppr opr i a t e f i na nc i a l pol i c i e s , a nd r e a l e xt e r na l a nd dome s t i c s hoc ks c a n l e a d t o mi s a l i gnme nt s a nd de v a s t a t i ng c ur r e nc y c r i s e s unde r t he s of t pe g r e gi me s .

20)The i nt e r me di a t e r e gi me s pr ovi de s c ope f or s e t t i ng a n a ppr opr i a t e ba l a nc e be t we e n e xc ha nge r a t e s t a bi l i t y a nd f l e xi bi l i t y .

If s uppor t e d by s ound ma c r oe c onomi c pol i c i e s , t he y c a n ke e p t he va r i a t i ons i n t he e xc ha nge r a t e wi t hi n r e a s ona bl e bounds , da mpe ni ng t he de gr e e of unc e r t a i nt y whi l e pe r mi t t i ng e nough f l e xi bi l i t y t o a dj us t t he pa r i t y ( t he c e nt e r of t he ba nd) t o e c onomi c f unda me nt a l s .

They a r e t he r e f or e l e s s s us c e pt i bl e t o vol a t i l i t y a nd mi s a l i gnme nt t ha n s of t pe g a nd f l oa t i ng r e gi me s i f t he a ut hor i t i e s a r e not c ommi t t e d t o de f e ndi ng t he e dge s of t he ba nd a nd, whe n t he ne e d a r i s e s , a l l o w t he e xc ha nge r a t e t o go out s i de t he e dge s .

Hi gh vol a t i l i t y of t he e xc ha nge r a t e i n t he f l oa t i ng r e gi me s gi ve s r i s e t o a phe nome non c a l l e d “ f e a r of f l oa t i ng” .

Acc or di ng t o r e c e nt s t udi e s , f e w de ve l opi ng c ount r i e s t ha t c l a i m t o be i mpl e me nt i ng a f l oa t i ng e xc ha nge r a t e pol i c y , do i n f a c t a l l o w t he i r e xc ha nge r a t e t o f l oa t ( Ca l v o a nd Re i nha r t 2000) .

Compar e d t o t he Uni t e d St a t e s a nd J a pa n, i nt e r na t i ona l r e s e r ve s , r e s e r ve mone y, a nd i nt e r e s t r a t e s i n t he s e c ount r i e s ha ve be e n mor e vol a t i l e , a nd t he i r e xc ha nge r a t e s mor e s t a bl e , whi c h i ndi c a t e t ha t t he y e f f e c t i ve l y ma i nt a i n s ome ki nd of ma na ge d or pe gge d r e gi me .

“Fe a r of f l oa t i ng” i s e xpl a i ne d l a r ge l y by t he f a c t t ha t e xc ha nge r a t e vol a t i l i t y i s mor e da ma gi ng t o t r a de , a nd t he pa s s - t hr ough f r om e xc ha nge r a t e s wi ngs t o i nf l a t i on i s f a r hi ghe r i n de ve l opi ng c ount r i e s .

Fea r of a ppr e c i a t i ng be c a us e of s hor t - t e r m c a pi t a l i nf l ows a nd l os i ng c ompe t i t i ve ne s s i s a l s o a f a c t or f or not l e t t i ng t he e xc ha nge r a t e f l oa t f r e e l y .

Ake y pr obl em of f ear f ul f l oat i ng i s i t s l ack of t r ans par enc y and ver i f i abi l i t y whi ch hei ght s unc e r t a i nt y .

21)Fl oa t i ng i t s e xc ha nge r a t e pe r mi t s a c ount r y t o us e i t s mone t a r y pol i c y ( a nd ot he r ma c - r oe c onomi c pol i c i e s ) t o s t e e r t he dome s t i c e c onomy be c a us e mone t a r y pol i c y doe s not ha v e t o be s ubor di na t e d t o t he ne e ds of de f e ndi ng t he e xc ha nge r a t e .

Give n t ha t c yc l i c a l c ondi t i ons di f f e r s i gni f i c a nt l y a mong c ount r i e s , t he a bi l i t y of a c ount r y t o r un a n i nde pe nde nt mone t a r y pol -

20) Kaminsky,G.,Lizondo,S.,and Reinhart,C.“Leading IndicatorsofCurrency Crisis”,IMF Staff Papers,Vol45,No.1:1–48,March 1998.

21) SeeCalvo,G.A.and Reinhart,C.M.“FearofFloating”,2000a. Calvo,G.A.andReinhart,C.M.

“Fixing forYourLife”,2000b.