A study on the development of method for

environmentally conscious management in Chinese manufacturing

中国製造業における環境配慮経営の促進に向けた評価 手法の開発に関する研究

2012 年 7 月

SUN,MEI

孫 美

CHAPTER 1 INTRODUCTORY CHAPTER

1.2 Research background 1-2

1.2.1 Position of Chinese manufacturing in the world 1-2

1.2.2 Transformation of Chinese manufacturing 1-7

1.2.3 Change of environment management of China 1-9

1.3 Study purpose 1-13

1.4 Framework of the study 1-17

Reference 1-21

CHAPTER 2 DEVELOPMENT OF ENVIRONMENT MANAGEMENT STRATEGY IN CHINESE MANUFACTURING

2.1 Trend of environment management 2-1

2.1.1 Definition of Environment Management Strategy (EMS) and Environment

Management System (EMS) 2-1

2.1.2 Content of environment management strategy 2-3

2.1.3 Current status of environment management strategy in China 2-3 2.2 Feasibility of application of environment management strategy in China 2-4 2.2.1 Support and problem in environment management 2-4 2.2.2 Eager and support for environment conscious product 2-5 2.2.3 Promotion of environment report and challenge 2-9

2.2.4 Support and problem in enterprise value 2-14

2.2.5 Promotion of green financing 2-15

2.3 Proposal for applying environmental strategy in China 2-17

2.3.1 Popular environment management tool 2-17

2.3.2 Proposal for applying environmental strategy 2-19

2.4 Conclusion 2-20

Reference 2-21

CHAPTER 3 ANALYSIS OF ENVIRONMENTAL LEGISLATION RISK AND CONSTRUCTION OF GLOBAL ECO-DESIGN STANDARDS DATABASE FOR CHINESE MANUFACTURING

3.1 Research background and purpose 3-1

3.2 Investigation of Japanese and Chinese environment law and regulation system 3-4

3.3 Analysis of Legislation risk on Chinese manufacturing 3-25 3.3.1 Identification of risk weighting of environment regulation 3-25 3.3.2 Forecast of legislation risk for sectors of manufacturing 3-31 3.4 Investigation of environment standardization in world 3-33 3.4.1 Importance of knowing well about the global environment standards 3-33 3.4.2 Main environment standards affecting manufacturing in the world 3-39 3.4.3 Influence of environment standardization to Chinese manufacturing 3-45 3.5 Database construction responding to global environmental standards for Chinese

export 3-46

3.5.1 Construction of database of eco design 3-46

3.5.2 Application of database for export manufacturing 3-47

3.6 Conclusion 3-48

Reference 3-49

CHAPTER 4 PROPOSAL OF MODIFIED MATERIAL FLOW COST ACCOUNTING AND ITS INTEGRATION IN FINANCIAL REPORT

4.1 Research background and purpose 4-1

4.1.1 Definition of Material flow cost accounting 4-1 4.1.2 Difference of MFCA and Material Flow Accounting 4-2

4.1.3 Current research of MFCA 4-2

4.2 Problem of current MFCA 4-4

4.2.1 Discontinuity of current MFCA calculation 4-4

4.2.2 Inaccuracy of cost allocation in current MFCA 4-6 4.3 Modification of current MFCA and financial report improvement based on 4-9 4.3.1 Modification of accounting calculation method of MFCA 4-9

4.3.2 Integration of MFCA and ERP 4-14

4.3.3 Financial report improvement based on the MFCA 4-16 4.4 Case study of modified MFCA in Chinese small enterprise 4-18

4.4.1 Company profile 4-18

4.4.2 Definition of quantity center 4-18

4.4.3 Data information collection and cost calculation 4-19

4.4.4 Draw the income statement in October 2011 4-20

4.5 Conclusion 4-21

Reference 4-23

SYSTEM AND CONSTRUCTION OF CSR DATABASE FOR CHINESE MANUFACTURING

5.1 Introduction 5-1

5.1.1 The definition of corporate social responsibility (CSR) 5-1

5.1.2 Philosophic theory of CSR 5-1

5.1.3 Subjects and contents of CSR 5-2

5.2 Purpose of the study 5-3

5.2.1 Current status of CSR 5-3

5.2.2 Study purpose 5-5

5.3 Establishment of indicator system of CSR assessment 5-6

5.3.1 Current status of CSR assessment 5-6

5.3.2 Establishment of CSR indicator 5-7

5.4 Construction of CSR database in China and Japan 5-27

5.4.1 Structure of CSR database 5-27

5.4.2 Content of CSR database 5-28

5.5 Investigation enterprises how to take CSR both in China and Japan in

Manufacturing 5-32

5.5.1 Method 5-32

5.5.2 Result and analysis 5-33

5.6 Conclusion 5-42

Reference 5-45

CHAPTER 6 PROPOSAL OF CORPORATE SUSTAINABLE DEVELOPMENT ASSESSMENT BASED ON CSR FOR CHINESE

MANUFACTURING

6.1 Investigation of current status of Socially Responsible Investment indices 6-1 6.1.1 Definition of socially responsibility investment 6-1 6.1.2 Investing strategy of socially responsibility investment 6-2

6.1.3 Socially responsibility investment index 6-3

6.1.4 Introduction of main SRI indices 6-6

6.2 Analysis of sustainability of corporate development 6-7

6.2.1 Exclusion of SRI indices 6-7

6.2.2 Analysis of assessment method of SRI indices 6-8 6.3 Current status of Chinese social responsibility investment 6-15

6.3.3 Disadvantage of SSE-RI selection method 6-16 6.4 Investigation of new CSR assessment base on the analytical hierarchy process

6-18 6.4.1 Constructing the index system based on analytical hierarchy process 6-18

6.4.2 Establishing Hierarchical structure 6-19

6.4.3 Pairwise comparison 6-20

6.4.4 Analysis result about weighting of indictor 6-23

6.4.5 Assessment of CSR Performance 6-23

6.5 Conclusion 6-24

Reference 6-26

CHAPTER 7 CONCLUSION AND FUTURE PROSPECT

7.1 Conclusion of this study 7-1

7.1.1 Development of environment management strategy in Chinese

manufacturing 7-1

7.1.2 Analysis of environmental legislation risk and construction of global

eco-design standards database for Chinese manufacturing 7-1 7.1.3 Proposal of Modified Material Flow Cost Accounting and its integration in

Financial Report 7-2

7.1.4 Development of CSR Assessment with Indicator System and Construction of

CSR Database for Chinese Manufacturing 7-3

7.1.5 Proposal of Corporate Sustainable Development Assessment Based on CSR

for Chinese Manufacturing 7-5

7.2 Future prospect of the study 7-6

7.2.1 Future prospect 1: Enlarge content of database of environment standards and

database of CSR practice 7-6

7.2.2 Future prospect 2:Combination of MFCA and ELP 7-6 7.2.3 Future prospect 3:Check effectiveness of SRI method in Chapter 6 7-8 ACKNOWLEDGEMENT AC-1

APPENDIX APP-1

RESEARCH ACHIEVEMENT AC-1

A STUDY ON THE DEVELOPMENT OF METHOD FOR

ENVIRONMENTALLY CONSCIOUS MANAGEMENT IN CHINESE MANUFACTURING

Abstract

Chapter 1 Introductory Chapter

This chapter introduced research background and illustrated research purpose.

Chinese manufacturing developed very fast, output of many products was ranked in top one or two in the world. In 2008, the value added in manufacturing of China is listed in top two in the world. Manufacturing is developing fast, and development speed is faster than other main manufacturing countries. However, high development of Chinese manufacturing relied on low labor cost and high resource consumption, this kind of development model of Chinese manufacturing is unsustainable, and manufacturing have heavy impact on environment.

Energy consumption per GDP of China listed in top 2 in the main manufacturing countries in 2005, and discharged a large amount of ozone depleting substance and hazardous waste.

Chinese manufacturing is facing transformation. New manufacturing should be low energy consumption, low environment pollution and high economic profit. Environment management method of government is also changing from treatment of end of pipe to control of pollutant source. The aims of Environment Management Strategy are plus economic profit and minus environment impact. Current research proved that Environment Management, Material Flow Cost Accounting, Corporate Social Responsibility can enhance economic profit and reduce environment impact. This study aimed at development of Environment Management Strategy in Chinese manufacturing. at last, this chapter drew study framework.

Chapter2 Development of Environment Management Strategy in Chinese Manufacturing

This chapter first identified definition of environment management strategy and environment management, pointed out environment management of this study is a strategy which integrates many activities in management and production such as material flow cost accounting, environment report, green purchase, green marketing and so on. Research and application of environment management strategy in China is fewer. Therefore, this chapter investigated the feasibility of application of environment management strategy in China from six aspects, (1) Support and problem in environment management (2) Eager and support for green product (3) Support and problem in environment data record (4) Promotion of environment report and challenge (5) Support and problem in enterprise value (6) Promotion of green financing. This chapter concluded that application of environment management strategy in China is feasible. However, mass of Chinese product is recalled because of green

barrier, environment report is lack of quantity description, CSR performance of Chinese enterprise is poor, and there is not assessment standard for financial support. For this problems, this thesis draw proposals of database construction for eco design, application of Material Flow Cost Accounting, database construction of Corporate Social Responsibility and assessment of Corporate Social Responsibility.

Chapter 3 Analysis of Environmental Legislation Risk and Construction of Global Eco-design Standards Database for Chinese Manufacturing

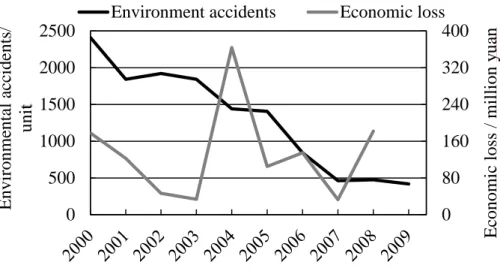

Environment accident reported by China is smaller than that of Japan, the environmental accidents are decreasing, but economic loss is not decreasing, therefore enterprise should enhance the environment management level and avoid environment risk. China speeded up environmental legislation in last ten years, environment regulations was enacted in time and fast. New environment legislation will bring risk for manufacturing. This chapter assessed legislative risk of every environment regulation from environment pollution and legislation process, and find contamination of soil, PM 2.5 and underground water problem, food and packaging recycling may take highest risk for manufacturing. After assessment of environment pollution intensity of sectors, this chapter forecast environment legislative risk for sectors and concluded that manufacture of metal products, agricultural product manufacture of paper and paper products will face highest environment legislative risk in the coming years. On the other hand, export value took more than half of GDP in average from 2007 to 2011. In recent years, Nations issued a large amount of environment standards; as a result, Chinese exported products suffered recall in main target nation of export because product did not meet requirement of eco-design. In China, small and medium-sized enterprises took more than half of total enterprise in manufacturing. For small and medium-sized enterprises, it is difficult to know well about all environment standards in world. This paper constructed database of global environment standards. This database can draw report of environmental requirement about restricted chemicals, waste disposal and energy-saving for product exported to different nations.

Chapter 4 Proposal of Modified Material Flow Cost Accounting and its integration in Financial Report

Material Flow cost accounting is an effective environment management tool which can visualize any waste so as to reduce the waste in the production process. However, cost allocation method of current MFAC is not accurate and cumbersome, especially for the sectors with a large number of system cost, allocating system cost by the weight ratio of positive and negative product will lead to serious error. System cost is divided into the system cost for waste disposal and system cost for the production in modified MFCA and added three account subjects which are defective product, positive product and waste. This paper

illustrated the shortcoming of current MFCA through adopting the modified calculation method to case example of the Ministry of Economy Trade and Industry. To promote the application of MFCA in China, this chapter integrated MFCA and Enterprise resource planning (ERP). Based on the integration of MFCA and ERP, this study drew proposal for income statement. At last, this study applied MFCA to a drug chemical plant in China, and drew the modified income statement for this company.

Chapter 5 Development of CSR Assessment with Indicator System and Construction of CSR Database for Chinese Manufacturing

To achieve sustainable development, enterprise not only need take environment responsibility but also need take other responsibility in the future. This chapter firstly introduced definition of corporate social responsibility, philosophic theory of CSR and subjects and contents of CSR. In China, many enterprises consider donation as CSR in China.

More than half of enterprise in top 300 had not taken any management measures of CSR or disclosed any CSR information to the public as bystanders. To promote the development of CSR in Chinese enterprise, this paper integrated ISO26000 and Chinese CSR report guideline (CASS-CSR1.0) and established an overall CSR indicator system which includes 50 indicators for environment, market and social responsibility, and limited the scope of every indicator for CSR assessment in Chapter 6. Based on the CSR indicator system, this chapter constructed a CSR database; it included 30 CSR guideline and compact, more than 300 CSR actions. Finally, this paper collected and sorted the CSR practices of 20 Chinese enterprises and 20 Japanese enterprises, and found Chinese enterprises should enforce the responsibility management and make more effort to take environment responsibility. In market responsibility, Chinese enterprise should take more action in product safety and quality, emphasize on the protection of customer data and privacy. In environment responsibility, Chinese enterprise should apply specific environment management tool like application of environment accounting, development of environment education and so on. For Japanese enterprise which is operating in China, it should pay attention to employee care and social problem solution.

Chapter 6 Proposal of Corporate Sustainable Development Assessment Based on CSR for Chinese Manufacturing

To create the sustainable society, we have to establish a good capital market in which the company with better CSR performance can finance easily. This paper analyzed the current status of SRI Indices, summarized the assessment methods of SRI indexes in the world. The financial data method applied by Chinese capital market ignored the performance assessment of CSR action and ignored CSR difference of industrial feature. Therefore, based on the indicator and database of CSR in Chapter 5, this study surveyed importance of different

indicators by questionnaire, and identified the weighting of CSR indicator by Analytical Hierarchy Process. At last this study applied it to Chinese companies, assessed CSR performance. This kind of assessment method can revise the error of financial method of Shanghai Stock Exchange-Socially investment.

Chapter 7 Conclusion and Future Prospect

This study aimed at development of method for environmentally conscious management in Chinese manufacturing.by investigation of current status of environment management, green product and marketing, environment record and report, enterprise value and financial support, concluded that development of Environment Management Strategy is feasible in China. To promote the application of Environment Management Strategy in China, this study constructed eco design database and CSR database which collected a large amount of information of global environment standards and CSR practice. Through comparison study, this study found manufacture of metal products, agricultural product and manufacture of paper and paper products will face high environment legislative risk. This study also modified MFCA by cost allocation and setting of account subject. At last, by improvement of SRI based on analysis of CSR practice to support the spread of Environment Management Strategy.

In the further study, we will enlarge database of environment standards and CSR, and construct web database to achieve query of eco design and CSR practice online. When enterprise gives proposal based on analysis of MFCA, we need take not only cost but also environment load into account, in the future, I will assess the rationality of proposal based on MFCA by ELP to ensure comprehensive environment load and cost are reduced at the same time. On the other hand, we will select stock with high CSR performance by analytical hierarchy process, and check return of investment.

Chapter 1

Introductory Chapter

Content

1.1 Introduction ... 1-1 1.2 Research background ... 1-2 1.2.1 Position of Chinese manufacturing in the world ... 1-2 1.2.2 Transformation of Chinese manufacturing ... 1-7 1.2.3 Change of environment management of China ... 1-9 1.3 Study purpose ... 1-13 1.4 Framework and composition of the study ... 1-17 Reference ... 1-21

Figure

Fig 1.1 Rise rate of manufacturing from 2007 to 2011 ... 1-4 Fig 1.2 Average rise rate of different sectors of manufacturing from 2007-2011... 1-4 Fig 1.3 Energy consumption per GDP of every county in 2005 ... 1-5 Fig 1.4 Emission of CO2 inmain manufacturing countries in 2007 ... 1-5 Fig 1.5 Change of CO2 since 1990 of main manufacturing country ... 1-6 Fig 1.6 Ozone Depleting Substance of main countries in 2008 ... 1-6 Fig 1.7 Percentage of labor cost in output of manufacturing ... 1-8 Fig 1.8 Average rise rate of sector in manufacturing ... 1-8 Fig 1.9 Amount of enterprise which are required to close or change location ... 1-9 Fig 1.10 Investment in Anti-pollution Projects of China from 2006-2010... 1-11 Fig 1.11 Investment in treatment of industrial pollution sources and new construction

projects ... 1-11 Fig 1.12 Various waste discharge per value added of industry from 2005-2010 ... 1-12 Fig 1.13 Ratio of utilized industrial solid wastes in China from 2005-2010 ... 1-12 Fig 1.14 Energy consumption per GDP of China since 2005 ... 1-13 Fig 1.15 Structure of paper ... 1-18

Table

Table 1.1 Industry classification of ISIC ... 1-1 Table 1.2 Division of manufacturing ... 1-2 Table 1.3 Ranks of main factors in the world in 2009 ... 1-3 Table 1.4 Hazardous wastes of several main countries from 2003-2008 ... 1-7 Table 1.5 Current research about the environmental law risk of enterprise ... 1-14 Table 1.6 Former research of EM, MFCA and CSR ... 1-16 Table 1.7 Former research of SRI and assessment of CSR ... 1-17

1.1 Introduction

International Standard Industrial Classification of all Economic Activities (ISIC) is the international reference classification of productive economic activities. The publication's main purpose is to provide a set of activity categories that can be utilized for the production of statistics according to activity. The industries of ISIC are shown in the Table 1.1.

Table 1.1 Industry classification of ISIC1-1)

Category Industry

A Agriculture, hunting and forestry B Fishing

C Mining and quarrying D Manufacturing

E Electricity, gas and water supply F Construction

G Wholesale and retail trade; repair of motor vehicles, motorcycles and personal and household goods

H Hotels and restaurants

I Transport, storage and communications J Financial intermediation

K Real estate, renting and business activities

L Public administration and defence; compulsory social security M Education

N Health and social work

O Other community, social and personal service activities P Private households with employed persons

Q Extra-territorial organizations and bodies

Manufacturing is defined as the physical or chemical transformation of materials of components into new products, including assembly of component parts of manufactured products and recycling of waste materials.1-2) The divisions of Chinese manufacturing are shown in the Table 1.2, which is a little bit different with the divisions of UN. People need product in life. Manufacturing is a process which involves tools and labor to produce goods for use or sale. It refers to a range of human activity, from handicraft to high tech, but is most commonly applied to industrial production, in which raw materials are transformed into finished goods on a large scale.1-3)

Table 1.2 Division of manufacturing1-4) Division of manufacturing

Processing of Food from Agricultural Products Manufacture of Foods

Manufacture of Beverages Manufacture of Tobacco Manufacture of Textile

Manufacture of Textile Wearing Apparel, Footware, and Caps Manufacture of Leather, Fur, Feather and Related Products Processing of Timber, Manufacture of Wood, Bamboo, Manufacture of Furniture

Manufacture of Paper and Paper Products Printing, Reproduction of Recording Media

Manufacture of Articles for Culture, Education and Sport Processing of Petroleum, Coking, Processing of Nuclear Fuel Manufacture of Raw Chemical Materials and Chemical Products Manufacture of Medicines

Manufacture of Chemical Fibers Manufacture of Rubber

Manufacture of Plastics

Manufacture of Non-metallic Mineral Products Smelting and Pressing of Ferrous Metals Smelting and Pressing of Non-ferrous Metals Manufacture of Metal Products

Manufacture of General Purpose Machinery Manufacture of Special Purpose Machinery Manufacture of Transport Equipment

Manufacture of Electrical Machinery and Equipment

Manufacture of Communication Equipment, Computers and Manufacture of Measuring Instruments and Machinery for Manufacture of Artwork and Other Manufacturing

Recycling and Disposal of Waste

1.2 Research background

1.2.1 Position of Chinese manufacturing in the world 1) The production of China manufacturing

China manufacturing industry has enjoyed a very fast development and its general scale has ranked in top places in the world with very obvious comparative advantages internationally.

At current, as the pillar industry of the national economy of China, the manufacturing industry serves as the dominant sector for economic growth and basis for economic transformation. As an important basis for the economic and social development, the manufacturing industry is the main channel for employment in cities and towns of China and the major embodiment of international competitiveness of China. As the main symbol of the improvement of comprehensive national power of China in the past over 20 years, the comprehensive development and optimized upgrading of the manufacturing industry have enabled China to primarily establish the status as a big country of manufacturing and laid the sound foundation for China to transformed to be a strong country of manufacturing.

According to the calculation of IHS GlobalInsight, in 2010, the production value of Chinese manufacturing has up to 10 trillion, taking 19.8% of world production value of manufacturing, is higher than manufacturing production value of United State with the percentage of 19.4%. From the 1895 to 2009, United State was always the top 1 country with the largest manufacturing production value.

There is other data of year 2009 showing the capability of China manufacturing, as shown in the Table 1.3.

Table 1.3 Ranks of main factors in the world in 20091-5)

Factors Ranks in the world

Gross Domestic Product 3

Foreign Trade Total 2

Exports 1

Production of Crude Steel 1

Production of Cement 1

Production of Woven Cotton Fabrics 1 2) Rate of rise of China Manufacturing

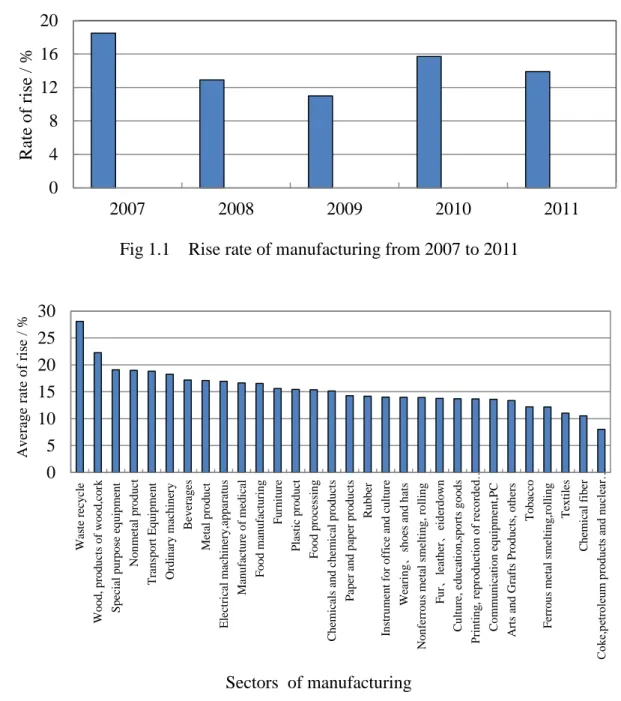

In the past five years, the rise rate of China manufacturing is keeping in a higher level. As shown in the Fig 1.1. We can find the rate of manufacturing rise decreased in 2008 and 2009 because of world financial crisis, but it increased quickly from 2010. Therefore, we can conclude that the rise rate the Chinese manufacturing is keep very high. The Fig 1.2 shows us the average rise rate of manufacturing. We can find the Waste recycling, Wood, products of wood, cork, Special purpose equipment, Nonmetal product, Transport Equipment, Ordinary machinery, Beverages, Metal product, Electrical machinery and apparatus, Manufacture of medical, Food manufacturing, Furniture manufacturing, Plastic product, Food processing, Chemicals and chemical products increased by more than average 15% year on year. Only the sector of Textiles, Chemical fiber, Coke, petroleum products and nuclear fuel developed relatively slowly.

Fig 1.1 Rise rate of manufacturing from 2007 to 2011

Fig 1.2 Average rise rate of different sectors of manufacturing from 2007-2011 3) Energy consumption and environment pollution

Manufacturing transforms raw materials into finished goods, it consumes raw material and energy; meanwhile manufacturing have heavy impact on environment, emitting a lot of waste water, waste gas and waste solid. The Fig 1.3 shows us the energy consumption per GDP in many countries; we can find the manufacturing of China is consuming energy in a high rate.

As we know Brazil, Russia, India and India are known simply as the BRIC. They are the emerging economies. We can find the energy consumption per GDP of China is also higher in the BRIC. The U.S. Japan, Korea, Germany, UK and France are old manufacturing counties.

Fig 1.4 shows us the CO2 emissions of main counties in 2007. We can find the CO2 emission 0

4 8 12 16 20

2007 2008 2009 2010 2011

Rate of rise / %

0 5 10 15 20 25 30

Waste recycle Wood, products of wood,cork Special purpose equipment Nonmetal product Transport Equipment Ordinary machinery Beverages Metal product Electrical machinery,apparatus Manufacture of medical Food manufacturing Furniture Plastic product Food processing Chemicals and chemical products Paper and paper products Rubber Instrument for office and culture Wearing、shoes and hats Nonferrous metal smelting, rolling Fur、leather、eiderdown Culture, education,sports goods Printing, reproduction of recorded… Communication equipment,PC Arts and Grafts Products, others Tobacco Ferrous metal smelting,rolling Textiles Chemical fiber Coke,petroleum products and nuclear…

Average rate of rise / %

Sectors of manufacturing

of China is highest in 2007 with 6538.37 million ton. It is more than that of U.S. CO2

emissions of China is most in the BRIC, and it became more than the old manufacturing nations like the U.S. Japan, Korea, and Germany and others. The Fig 1.15 shows us the change since 1990; we can find China, India, Brazil, and Korea increasing considerably since 1990. But CO2 emissions of China increased most since 1990. The emission of U.S. is more but it did not increase so much, compared to the emission in 1990. Emission of Russian Federation, Germany, and UK decreased since 1990.

Fig 1.3 Energy consumption per GDP of every county in 20051-4)

Fig 1.4 Emission of CO2 inmain manufacturing countries in 20071-5)

0 2 4 6 8 10

Energy consumption / quadrillion 1015 Btu

Nations

0 1400 2800 4200 5600 7000

CO2emission / mio. tonnes

Nations

Fig 1.5 Change of CO2 since 1990 of main manufacturing country1-5)

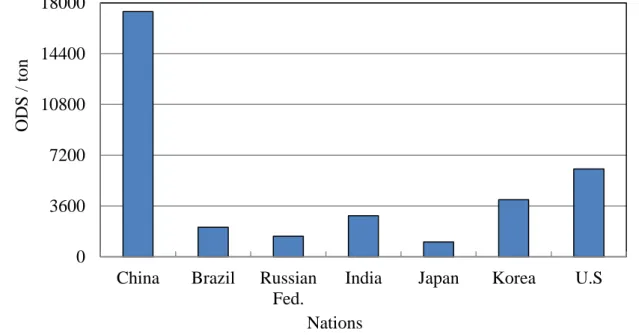

About the ozone depleting, Fig 1.6 shows us the all Ozone Depleting Substance (ODS) of main manufacturing countries in 2008. We can find the ODS of China is highest. There are not statistic data about the NOX , GHG and SO2 of China.

Fig 1.6 Ozone Depleting Substance of main countries in 20081-6) -40

0 40 80 120 160 200

Change since 1990 / %

Nations

0 3600 7200 10800 14400 18000

China Brazil Russian Fed.

India Japan Korea U.S

ODS / ton

Nations

About hazardous wastes, the main hazardous wastes came from China, Germany, Russian Federation, United States and Philippines. The amounts of hazardous wastes are more than one million ton as shown in the Table 1.4.

Table 1.4 Hazardous wastes of several main countries from 2003-20081-5)

nation 2003 2004 2005 2006 2007 2008 2009

China 11700 9950 11620 10840 10790 13570 14300

Russian Fed. 287272 142766 142497 140011 287653 122883 141019

India --- --- -- 8140 --- --- ---

Philippines 2265 707 1670 11786 1130 164939 1901

Germany 19515 20000 --- 21705 --- 22323 ---

Korea 2913 --- --- --- --- --- ---

U.S. 27376 34788 --- --- --- ---

France --- 9617 --- 9622 --- 10893 ---

UK 4991 7973 --- 8448 --- 7285 ---

To conclusion, the manufacturing of China is facing transformation. The high energy consumption and heavy environment pollution illustrated the current development of manufacturing is not sustainable.

1.2.2 Transformation of Chinese manufacturing

Up to now, the high development of Chinese manufacturing relies on low labor cost and intensive resource mining. As shown in Figure1.7, the percentage of labor cost in total output of manufacturing was less than many other main manufacturing counties in 2010. In recent years, labor cost is increasing; main manufacturing area of China Southeast became lack of labor because of low salary. In the future, the salary must increase. On the other hand, mass mining supported high development of manufacturing. From Fig 1.8, we can find, from 2007 to 2011, average rise rate of five mining sectors like other mining, ferrous mining, nonmetal mining, nonferrous mining, coal exploitation and washing listed in top 20 in total. And average rise rate of wood products of woodcock was ranked in top 5. However labor cost must increase, resource will exhaust. This kind of development model is not sustainable.

The major task of China at the new stage in the new century is to realize industrialization.

Industrialization usually refers to the process whereby the number of labors involved in the manufacturing industry and the second industry is increasing and that involved in the primary industry is reducing. China has been at the middle stage of industrialization and its industrialization has not been realized. Under the background of significant development of global scientific and technical revolution and the spreading of informatization, China has

Fig 1.7 Percentage of labor cost in output of manufacturing 1-7)

Fig 1.8 Average rise rate of sector in manufacturing1-8)

abandoned the road of traditional industrialization, while take the new path of industrialization driven by informatization. The new industrialization features high content of science and technology, good economic benefits, low energy consumption and environmental pollution and full playing of the advantage of human resources. The former four features are

0 4 8 12 16 20

Israel Germany United Kingdom Canada New Zealand Hong Kong,China France Spain United States Netherlands Italy South Africa Kazakhstan Brazil Poland Russian Fed. Czech Republic Japan Iran Singapore Indonesia Philippines Malaysia China India

percentage of labo cost in total ouput / %

0 7 14 21 28 35

Average rise rate / %

requirements to adapt to global tremendous scientific and technical progresses and the economic sustainable development. The last feature is put forth according to the national situation of China, which has abundant human resources. The main tasks of China to adjust the industrial structure in future is to take the new path of industrialization, enhance independent innovation abilities, encourage and support the development of advanced production capacities and restrict and abandon backward production capabilities with the Reform and Opening-up and scientific and technical progress as the drive, avoid blind investment and low-level repeated construction and promote the optimal upgrading of industrial structure. Pursuit of development mode focusing on conservation, environmental protection and safety will be the main development direction of China's manufacturing industry.1-7)

1.2.3 Change of environment management of China

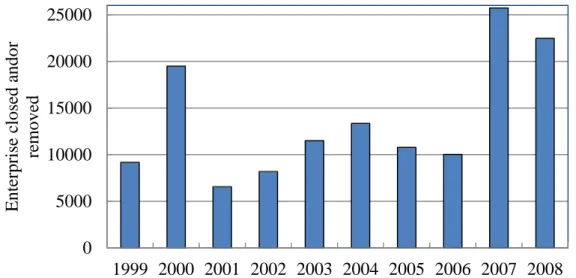

Environment management of government focuses on the pollution treatment in the past, administration departments imposed administrative penalty or closed enterprise. Take one example as shown in Fig 1.9, to meet the temporary environment requirement of holding Olympic, a large amount of enterprises were closed or removed in 2007 and 2008. As a result, enterprise moved to new place and continually pollute. Meanwhile, government imposed administrative penalty on enterprise, as shown in Fig 1.10, administrative penalty was increasing since 1998. However, some enterprise would like to pay administrative penalty rather than reduce pollutant discharge.

Fig 1.9 Amount of enterprise which are required to close or change location1-10) 0

5000 10000 15000 20000 25000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 Enterprise closed andor removed

Fig 1.10 Amount of administrative penalty from 1998 to 20101-11)

In current, government changed environmental management method, focused on improvement of environment quality, enforced control of pollution source, and research and development of environment technology.

Enforcement of Circular Economy Law on January 1, 2009, marked the qualitative breakthrough of Chinese environment law, which identified the development direction of Chinese economic. The sustainable development was recognized the basic state policy. The sustainable development got unprecedented attention. The central government will allocate funds and capital to enterprises to encourage innovation in recycling technologies, and provide tax breaks to enterprises introducing and using energy-efficient technologies and equipment. The law requires

a. Government to closely monitor energy consumption and pollution emissions in heavy consuming and polluting industries including the steel and non-ferrous metal production, power generation, oil refining, construction, and printing industries;

b. Government departments to promote recycling and improve energy-saving and waste-reutilization standards and develop policies to divert capital into environment friendly industries;

c. Industrial enterprises to introduce water-saving technologies, strengthen management, and install water-saving equipment in new buildings and projects;

d. Crude oil refining, power generation, steel and iron production plants to stop using oil-fired fuel generators and boilers, in favor of clean energy, such as natural gas and alternative fuels;

e. Enterprises to recycle and make comprehensive use of coal mine waste, coal ash, and other waste materials; and encourages farmers and rural administrators to recycle straw, livestock waste, and farming by-products to produce methane.1-13)

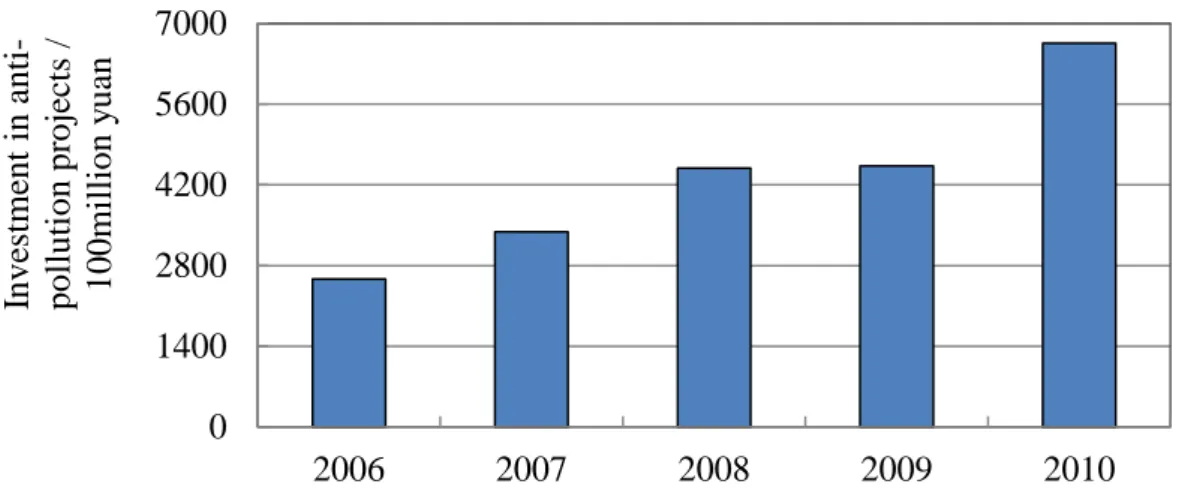

Fig 1.10 show us the Investment in Anti-pollution Projects, we can find the total investment in anti-pollution projects has been increasing since 2006.

0 30000 60000 90000 120000 150000

Administrative penalty / unit

Fig 1.10 Investment in Anti-pollution Projects of China from 2006-2010

Fig 1.11 shows us the investment in treatment of industrial pollution sources and new construction project; Construction Projects-"Three-Simultaneity" regimen is an important regiment of environment protection in China. It required the environment components of new construction project have to be designed, constructed and used simultaneously with the project. We can find China enforced investment in environment components for

"Three-Simultaneity" new construction projects since 2000. It reflected fully that ways of environment protection of China has been changed.

Fig1.11 Investment in treatment of industrial pollution sources and new construction projects

3) The progress made by China in environment protection

In the effort of government and people, the environment treatment made great progress in China. The value added of an industry, also referred to as gross domestic product

0 1400 2800 4200 5600 7000

2006 2007 2008 2009 2010

Investment in anti- pollution projects / 100million yuan

0 500 1000 1500 2000 2500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Investment / 100 million yuan Investment I treatment of industrial pollution sources

investment in environment components of

construction projects

(GDP)-by-industry, is the contribution of a private industry or government sector to overall GDP. Value added equals the difference between an industry’s gross output (consisting of sales or receipts and other operating income, commodity taxes, and inventory change) and the cost of its intermediate inputs (including energy, raw materials, semi-finished goods, and services that are purchased from all sources). The Fig 1.12 shows us the various waste discharge per value added of Industry from 2005-2010. We can find the all of waste water discharge per value added of industry, COD discharge per value added of industry, emission of SO2 per value added of industry and industrial solid wastes discharged per value added of industry decreased.

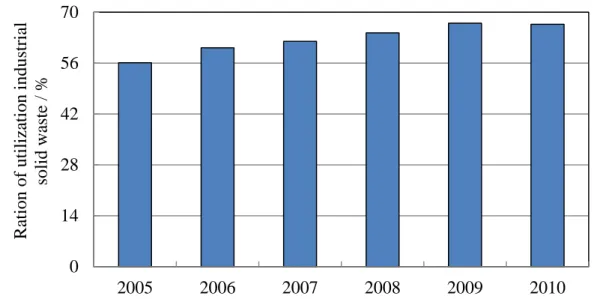

Fig 1.12 Various waste discharge per value added of industry from 2005-20101-14) On the other hand, the ratio of utilized industrial solid wastes also increased as shown in the Fig 1.13. More and more solid wastes are recovered, recycled and reused. Meanwhile, the energy consumption per GDP also decreased as shown in the Fig 1.14.

Fig 1.13 Ratio of utilized industrial solid wastes in China from 2005-20101-13)

0 50 100 150 200 250 300

Waste Water (ton/10000 yuan)

COD (kg/10000 yuan)

SO2(kg/10000 yuan)

Industrial Solid Wastes (kg/10 000

yuan) Discharge per value added of industry

Discharges and units

2005 2006 2007 2008 2009 2010

0 14 28 42 56 70

2005 2006 2007 2008 2009 2010

Ration of utilization industrial solid waste / %

Fig 1.14 Energy consumption per GDP of China since 20051-5)

To conclusion, since 2005, clean production of China manufacturing make great progress.

The discharges of pollutants was reduced, the energy consumption per GDP also was reduced.

China enforced the utilization of waste. The manufacturing of China is developing forwards to a cleaner and sustainable direction.

However, According to rank of the Environment Performance Index (EPI) issued by the Yale Center for Environmental Law and Policy (YCELP) and the Center for Earth Information Science Information Network (CIESIN) at Columbia University, China was ranked in 116 during 132 countries in 2012. The 2012 Environment Performance Index ranks 132 countries in the following ten policy categories1-14):

• Environmental Health

• Water (effects on human health)

• Air Pollution (effects on human health)

• Air Pollution (ecosystem effects)

• Water Resources (ecosystem effects)

• Biodiversity and Habitat

• Forests

• Fisheries

• Agriculture

• Climate Change

1.3 Study purpose

China is aiming at establishing society of environment-friendly and resource-saving.

Government, research organization, financial origination and enterprise are trying their best to make it come true together. Meanwhile, the global society is also focus very much on the environment protection and sustainable development. Manufacturing is facing transformation;

Enterprise is facing more and more challenge of environment. Environment Management Strategy aims at reducing environment load and enhancing economic profit. Environment

0 0.25 0.5 0.75 1 1.25

2005 2006 2007 2008 2009 2010

Energy consumption / (tce/ 10000 yuan)

Management Strategy (EMS) includes clean product, environment business and social construction. it integrated mass of activities of management and production. This study will promote the application of EMS in China. In clean production, this study will promote application of Material Flow Cost Accounting. In environment business, this study will promote eco design of product. In social construction, this paper will improve Corporate Social Responsibility performance for Chinese manufacturing. Finally, to provide a capital market for application of EMS, this paper will investigate Socially Responsibility Investment.

1) Know well the environmental regulation to avoid environmental risk

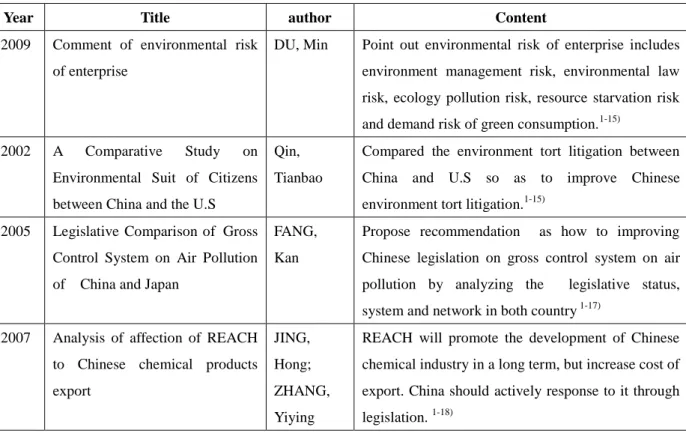

Environment risk includes environment management risk, environmental law risk, ecology pollution risk, resource starvation risk and demand risk of green consumption. Generally law scholars focus on improvement of Chinese environmental law. The research about environmental legislative risk of enterprise is few. Scholars improve Chinese environmental law by comparison study with other countries as shown in Table 1.5. The advanced experience of other countries gives a great help to Chinese environmental development. In the consideration of rapid development of Chinese environment laws and regulations, manufacturing will be confronted with the risk coming from environmental regulation. This paper will assess the environmental risk for manufacturing by comparison with Japanese environment law system. On the other hand, scholar also investigated the global environment standard and its affection to China. This paper will expend this kind of research in order that enterprise can know well about global environment standards

Table 1.5 Current research about the environmental law risk of enterprise

Year Title author Content

2009 Comment of environmental risk of enterprise

DU, Min Point out environmental risk of enterprise includes environment management risk, environmental law risk, ecology pollution risk, resource starvation risk and demand risk of green consumption.1-15)

2002 A Comparative Study on Environmental Suit of Citizens between China and the U.S

Qin, Tianbao

Compared the environment tort litigation between China and U.S so as to improve Chinese environment tort litigation.1-15)

2005 Legislative Comparison of Gross Control System on Air Pollution of China and Japan

FANG, Kan

Propose recommendation as how to improving Chinese legislation on gross control system on air pollution by analyzing the legislative status, system and network in both country 1-17)

2007 Analysis of affection of REACH to Chinese chemical products export

JING, Hong;

ZHANG, Yiying

REACH will promote the development of Chinese chemical industry in a long term, but increase cost of export. China should actively response to it through legislation. 1-18)

2) Enhance environment management (EM) level to get competitiveness

After ensuring avoid of environmental risk, enterprises have to enhance environment management level so as to avoid environment risk and enhance the competitiveness.

According to research of some scholars as shown in the Table 1.6, the environmental management level of Chinese enterprise is still very low. To help Chinese manufacturing enhancing the level of environment conscious operation, this paper will help enterprise establish the environment management strategy. The main driven factors of environment management is benefit and social responsibility, 1-20) environment management should be improved from these both aspects, Material Flow Cost Accounting (MFCA) is just a new environment management tool which can achieve the economic and environmental benefit.

Under MFCA, the flows and stocks of materials within an organization are traced and quantified in physical units (e.g. mass, volume) and the costs associated with those material flows are also evaluated. The resulting information can act as a motivator for organizations and managers to seek opportunities to simultaneously generate financial benefits and reduce adverse environmental impacts. 1-19) Scholar had proved that MFCA can improve corporate profit by research. And MFCA are popular in Japan, the Ministry of Economics, Trade and Industry (METI) has been promoted the application of MFCA, many Japanese companies have adopted MFCA. And, METI also published the report of MFCA application every year to introduce the case example and guideline about how to apply MFCA. To promote the application of MFCA in global, the International Organization for Standardization (ISO) also provides a general framework for material flow cost accounting (MFCA) named as ISO 14051:2011. Chinese company also need catch up this global trend of environment management. To promote the application of MFCA in China, this paper will introduce it and research it in further, so as to make it more easily applied. The other driven factors of environment management is social responsibility, consequently, this paper also investigate the current status of Corporate Social Responsibility (CSR) and to promote the CSR. According to former research of other scholars, the CSR level of Chinese enterprise is still very low.

However, CSR is booming in the world, ISO issued the ISO 26000 to promote the application of CSR IN 2011. This paper will investigate how to take corporate social responsibility. To help enterprise taking better the Corporate Social Responsibility, this paper illustrated the practice or action of every kind of responsibility, through this illustration, enterprise can not only know about the content of every kind of responsibility but also it can adopt these practice, it will be a good guideline for enterprise to take social responsibility. Meanwhile, to learn from Japanese enterprise, this paper established a database about the CSR practice, analyzed the current status of Japanese enterprise and give proposal for Chinese enterprise.

Table 1.6 Former research of EM, MFCA and CSR

Topic Year Title Author Content

EM 2011 Enterprise Motivation for Environment Management

CHEN, Liang It concluded that enterprise environmental management is primarily driven by benefit and social responsibility.1-19)

2010 An empirical study on the driving mechanism of proactive corporate

environmental management in China

Xianbing Liu, et al

Through survey, found proactive environmental management level was moderately low

Currently.1-21)

MFCA 2010 Report of introduction demonstration and domestic countermeasure of MFCA

METI Introduced the theory of MFCA, case example of MFCA application, and simply method of MFCA application.1-22)

2010 The Impacts of MFCA Management to Corporate Financial Performances

Michiyasu NAKAJIMA, Asako KIMURA

Examine that MFCA can improve corporate profit on the financial performances.1-23)

2010 International Standardization of MFCA (ISO 14051)

Propharm Japan Co., Ltd.al et.

Introduced the current status of MFCA, and explain the relationship of ISO 14051 and ISO 14000 standards.1-24)

2008

applied the MFCA to a zinc smelter

Xiao Xu al et.

Applied the MFCA to a zinc smelter, It is good application of MFCA to Chinese enterprise, but compared to case study of Japan, no creation.1-25) CSR 2009 Construct and Evaluate the

Indicators

System of Corporate Social Responsibility

ZHU Lilong, YOU Jianxin

Divide CSR into economics, laws, ethical, charity and environmental responsibility; establish an indicators system of CSR and evaluation model on CSR through the analytical hierarchy process.1-27) 2010 Relationship of Corporate

Social Responsibility and Corporate Financial Performance: Controversy and Unification

LI

Jian-sheng,LI Wei

More empirical studies concluded CSR have positive relationship with corporate financial performance,.

However corporate social responsibility converting into corporate financial performance needs social responsibility market, and the good manner and strategy by which corporation undertakes corporate social responsibility.1-28)

2011 Research report of corporate social responsibility of China

CASS Investigate CSR of top 100 Chinese enterprise, concluded that enterprise scored very low.1-26) 2011 ISO2006 ISO Addresses subjects, principle and actions of CSR1-28)

2) Make good financing environment for sustainable development of society

To stimulate society to develop towards a sustainable society, it is necessary to guide capital to invest in programmes with society responsibility. Meanwhile, if the enterprise focusing on sustainable development can easily finance, it will promote greatly the development of programmes of sustainable development. According to the former researchas shown in the Table 1.7, Socially Responsibility Investment (SRI) investors are willing to accept suboptimal financial performance to pursue social or ethical objectives, and cooperate social responsibility have a positive effect on the return of stock. The global financial institutes also promote industry to develop towards a direction of harmony society and environmental sustainability. In the future, pursuing profit maximization will be replaced by social responsibility maximization as the goal of enterprise. Only the enterprise responsible for society can develop sustainably. Therefore, this paper will investigate the current status of SRI, summarize the assessment method of SRY, and analyze the advantage and disadvantage of various investment method of SRI so as to make proposal for Chinese SRI.

Table 1.7 Former research of SRI and assessment of CSR

Year Title Author Content

2002 Environment policy of World Bank and affection to China

XU, Jing Analyzed environment policy of World Bank, affection to China and response of China. Pointed out the importance of combination of environment assessment and financing. 1-30) 2008 The stocks at stake: Return and risk

in socially responsible investment

T Rients Galema, et al

nvestigate the effect of socially responsible investment (SRI) on stock returns. And conclude that diversity, environment and product – has a significant impact on stock returns.1-31)

2008 Research of AHP Model on Combination between the Social Responsibility and the Economic Benefits in Corporation

Yingchen WANG.et al

Describes the important role that the social responsibility plays in the development of the corporation. Through using the AHP, we can obtain the optimal combination between the social responsibility and economic efficiency of the corporation.1-33) 2011 Socially responsible investments:

Institutional aspects, performance, and investor behavior

Luc Renneboog, et al

Existing studies hint but do not unequivocally demonstrate that SRI investors are willing to accept suboptimal financial performance to pursue social or ethical objectives. 1-32)

1.4 Framework and composition of the study

To promote the environment conscious operation of manufacturing in China, these paper developed method for environmental conscious management from the risk analysis of external regulations, internal environment conscious management and financing. The structure of paper is shown in Fig 1.15. This study first introduced the position of Chinese manufacturing in world and operation background of Chinese manufacturing, and then investigated the environment law of Chinese and the environmental standards of world. To

promote the environment management level, next, this paper investigated the environment management strategy and MFCA. And then, expand to all CSR actions of world. To promote the application of CSR, this paper further investigated the SRI. At last, summarized the conclusion and prospect the further research.

Fig 1.15 Structure of paper

This thesis is composed by seven chapters. The main contents of every chapter are shown as following.

Chapter 1, this chapter illustrated the research background from the position of Chinese manufacturing, national background of environmental policy and green barrier in international trade. And it identified the research purpose of promoting the environment conscious management in manufacturing. Meanwhile, it summarized the current status of research and pointed out the creativeness and necessity of research.

Chapter2 first identified difference of definition of environment management strategy and environment management, pointed out environment management of this study is a strategy which integrates many activities in management and production such as material flow cost accounting, environment report, green purchase, green marketing and so on. Research and application of environment management strategy in China is fewer. Therefore, this chapter investigated the feasibility of application of environment management strategy in China from six aspects, (1) Support and problem in environment management (2) Eager and support for

green product (3) Support and problem in environment data record (4) Promotion of environment report and challenge (5) Support and problem in enterprise value (6) Promotion of green financing. This chapter concluded that application of environment management strategy in China is feasible. However, mass of Chinese product is recalled because of green barrier, environment report is lack of quantity description, CSR performance of Chinese enterprise is poor, and there is not assessment standard for financial support. For this problems, this thesis draw proposals of database construction for eco design, application of Material Flow Cost Accounting, database construction of Corporate Social Responsibility and assessment of Corporate Social Responsibility.

Chapter 3 is Analysis of Environmental Legislation Risk and Construction of Global Eco-design Standards Database for Chinese Manufacturing

Environment accident reported by China is smaller than that of Japan, the environmental accidents are decreasing, but economic loss is not decreasing, therefore enterprise should enhance the environment management level and avoid environment risk. China speeded up environmental legislation in last ten years, environment regulations was enacted in time and fast. New environment legislation will bring risk for manufacturing. This chapter assessed legislative risk of every environment regulation from environment pollution and legislation process. After assessment of environment pollution intensity of sectors, this chapter forecast environment legislative risk for sectors. On the other hand, export value took more than half of GDP in average from 2007 to 2011. In recent years, Nations issued a large amount of environment standards; as a result, Chinese exported products suffered recall in main target nation of export because product did not meet requirement of eco-design. In China, small and medium-sized enterprises took more than half of total enterprise in manufacturing. For small and medium-sized enterprises, it is difficult to know well about all environment standards in world. This paper constructed database of global environment standards. This database can draw report of environmental requirement about restricted chemicals, waste disposal and energy-saving for product exported to different nations.

Chapter 4 modified material flow cost accounting and its integration in financial report.

Material Flow cost accounting is an effective environment management tool which can visualize any waste so as to reduce the waste in the production process. However, cost allocation method of current MFAC is not accurate and cumbersome, especially for the sectors with a large number of system cost, allocating system cost by the weight ratio of positive and negative product will lead to serious error. System cost is divided into the system cost for waste disposal and system cost for the production in modified MFCA and added three account subjects which are defective product, positive product and waste. This paper illustrated the shortcoming of current MFCA through adopting the modified calculation method to case example of the Ministry of Economy Trade and Industry. To promote the application of MFCA in China, this chapter integrated MFCA and Enterprise resource