Fiscal Policy for a Sustainable Healthcare and Pension System in Thailand under an Aging Population:

Case Study from Japan

Supanun Chumjai

1Visiting Scholar

Policy Research Institute, Ministry of Finance, Japan

1 The views and opinions expressed in this paper are those of the author’s and do not necessarily reflect the views and opinions of the Fiscal Policy Office, Ministry of Finance, Thailand or Policy Research Institute.

2

Contents

ABSTRACT 5

LIST OF ABBREVIATIONS 6

LIST OF FIGURES 7

LIST OF TABLES 9

CHAPTER I: INTRODUCTION 9

1.1 Paper Objective 9

1.2 A Summary Review of the Aging Population in Thailand and Government Policies 10

CHAPTER II: LITERATURE REVIEW 12

CHAPTER III: THAILAND HEALTHCARE AND PENSION SYSTEM 14

3.1 Thailand Healthcare System 14

3.1.1 Civil Servant Medical Benefit Scheme (CSMBS) 15

3.1.2 Social Security Scheme (SSS) 16

3.1.3 Universal Coverage Scheme (UCS) 17

3.2 Thailand Pension System 20

3.2.1 Pillar 0: “A non-contributory pillar” 22

3.2.2 Pillar 1: “A mandatory defined benefit pillar” 23

3.2.3 Pillar 2: “A mandatory defined contribution pillar” 24 3.2.4 Pillar 3: “A voluntary defined contribution pillar” 24

3.2.5 Proposed National Pension Fund (NPF) 26

CHAPTER IV: JAPAN HEALTHCAREANDPENSION SYSTEM 27

4.1Japan Healthcare System 27

4.1.1 National Health Insurance 28

4.1.2 Employees’ Health Insurance 29

4.1.3 Late-state Medical Care System for the Elderly 30

4.2 Japan Pension System 33

4.2.1 National Pension Insurance 33

3

4.2.2 Employees’ Pension Insurance 35

4.2.3 Voluntary Pension Insurance 37

4.2.4 Public Assistance System 39

CHAPTER V: THE COMPARISON BETWEEN THAILAND AND JAPAN 40

5.1 Reformation of Social Security System 40

5.2 Healthcare System 41

5.2.1 The System 41

5.2.2 Financial Resource 42

5.2.3 Method of Payment to Healthcare Providers 42

5.2.4 The Role of Private Stakeholders 43

5.2.5 Budget Allocation 43

5.2.6 Summary 45

5.3 Pension System 48

5.3.1 The System 48

5.3.2 Financial Resource 49

5.3.3 Budget Allocation 49

5.3.4 Government Policy for the Pension System 51

5.3.5 Summary 51

5.4 Fiscal Policy 55

5.5 Local Authorities Organizations (LAOs) 56

CHAPER VI: CONCLUSION AND POLICY RECOMMENDATION 57

6.1 Healthcare System 57

6.1.1 The National System 57

6.1.2 Administration and Management 58

6.1.3 Financial Resources 60

6.1.4 The Role of Private Stakeholders 61

6.2 Pension System 61

4

6.2.1 The System 61

6.2.2 Financial Resources 62

6.3 Fiscal Policy 64

6.4 Local Authorities Organizations (LAOs) 64

REFERENCES 66

5 ABSTRACT

Given the rapid increase in elderly citizens,Thailand is going to become an “aged society” by 2030. Therefore, it is obvious that Thailand will face many challenges. In terms of policy, the Ministry of Finance should understand what kinds of problems await the country under this situation, what is needed to deal with these problems, and what kind of policies and strategies are needed to efficiently maximize the competitiveness of the country. The objectives of this paper are to learn how to create efficient policy which provides benefits for both of senior citizens and the Thai government by learning from the experience of the Japanese government and to suggest efficient and sustainable policies to the Thai government that will help to manage the budget for the healthcare and pension system, which will ultimately prevent the government’s fiscal risk in the future. This paper also studies the Japanese Healthcare and Pension system, for which all data and information come from the Ministry of Health, Labour and Welfare and Budget Bureau. Comparisons for significant issues such as the management and financial resources for the Japanese and Thai Healthcare and Pension systems show that the Thailand government should reform some schemes of its Healthcare and Pension system to prevent a huge fiscal burden from arising due to the aging population. However, besides making efficient and sustainable fiscal policies and other related policies, the government should be a leader in educating people about financial literacy. Thailand’s citizens also need to prepare themselves by maintaining good health and saving money to live adequately after their retirement.

6 LIST OF ABBREVIATIONS

AMCs Asset Management Companies

CGD Comptroller General’s Department CSMBS Civil Servant Medical Benefit Scheme

DRGs Diagnosis Related Groups

EPI Employees’ Pension Insurance

GPF Government Pension Fund

IMF International Monetary Fund

MAAs Mutual Aid Association

MoPH Ministry of Public Health

NHA National Health Assembly

NHC National Health Commission

NHCO National Health Commission Office

NHI National Health Insurance

NHSO National Health Security Office

NPF National Pension Fund

NSF National Saving Fund

PVD Provident Fund

RMF Retirement Mutual Fund

SSF Social Security Fund

SSO Social Security Office

SSS Social Security Scheme

UCS Universal Coverage Scheme

7 LIST OF FIGURES

Figure 1: CSMB’s Actual Expenses as a Percentage of National Budget 15

Figure 2: SSS’s Budget as a Percentage of National Budget 17

Figure 3: MoPH’s Budget as a Percentage of National Budget 18 Figure 4: Government Budget for the Elderly as a Percentage of National Budget 21

Figure 5: Pension System in Thailand 22

Figure 6: Structure of the Long-Term Care Insurance System 31 Figure 7: Government Budget for the Healthcare System of National Budget 32 Figure 8: Government Budget for the Long-Term Care System of National Budget 32

Figure 9: Japanese Pension System 33

Figure 10: Government Budget for Pension System of National Budget 37 Figure 11: Healthcare's Budget as a Percentage of National Budget (Thailand) 44 Figure 12: Healthcare's Budget as a Percentage of GDP (Thailand) 44 Figure 13: Healthcare and Long-Term Care's Budget as a Percentage of National Budget (Japan) 44 Figure 14: Healthcare and Long-Term Care’s Budget as a Percentage of GDP (Japan) 44 Figure 15: Government Budget for the Elderly as a Percentage of National Budget (Thailand) 50 Figure 16: Government Budget for the Elderly as a Percentage of GDP (Thailand) 50 Figure 17: Pension’s Budget as a Percentage of National Budget (Japan) 50 Figure 18: Pension’s Budget as a Percentage of GDP (Japan) 50

8 LIST OF TABLES

Table 1: Thailand’s Population Projections over 30 years from 2010-2040 10 Table 2: Brief Characteristics of Three Main Healthcare Schemes in Thailand 19 Table 3: Government Budget on Elderly Income Security for FY 2013 to 2017 21

Table 4: Old Age Allowance (Baht) 22

Table 5: Pension Calculation 23

Table 6: The Benefit for an Insured Person Base on Duration of Contribution 24 Table 7: The Ceiling of Co-contribution from the Government by Age 25

Table 8: Summary of National Health Insurance 28

Table 9: Summary of Employees’ Health Insurance 29

Table 10: Summary of Late–State Medical Care System for the Elderly 30 Table 11: Summary of National Pension (As of the end of March 2014) 35 Table 12: Summary of Employees’ Pension Insurance (As of the end of March 2014) 36 Table 13: The break-down by age, Public Assistance Recipients (2010) 39 Table 14: Comparison the Type of System between Thailand and Japan in each group 45 Table 15: Comparison the Type of Organization between Thailand and Japan in each group 46 Table 16: Comparison the Pension System between Thailand and Japan in each group 52 Table 17: Comparison the Organization of Pension System between Thailand and Japan 53

9

CHAPTER I: INTRODUCTION

1.1 Paper Objective

At present, demographic change in Thailand is an issue of significant interest, as an aging society will have massive implications for public finance. According to Bloomberg Visual data, Thailand is ranked the third most speedily aging population in the world (behind South Korea and Japan). The number of people aged over 60 in Thailand will increase from 8.4 million in 2010 to 20.5 million in 2040, and the number of people aged over 80 will increase from 1 million to 4 million during the same period. Along with this rapid increase of elderly citizens, it is obvious that Thailand will face many challenges. In terms of policy, the Ministry of Finance should understand what kinds of problems await the country, what is needed to deal with these problems, and what kind of policies, especially fiscal policies, and strategies are needed to efficiently maximize the competitiveness of the country

Since Japan has been faced with this situation for a decade, Japan is one of the good models for Thailand to study regarding how the government manages the budget and tax policy to handle an aged society. According to a document issued by the Japanese government, the government started taking care of older people by enacting a special law in 1973, and the government has launched many programs since then. Therefore, it can be said that the Japanese government has aggregated sufficient experience to deal with an aged society, for which some programs are successful and others were not. Based on these experiences, Japan has been developing an efficient law to provide sustainable long-term benefits for senior citizens. Furthermore, the Japanese government also has sufficient tools to control the fiscal risk through budget management and tax policies. As a result, Japan has been and will be the role model for other countries wishing to study how to deal with an aged society.

The objective of this study is to learn how to create efficient law that provides efficient benefits for both senior citizens and the Thai government. This objective is pursued by examining the many policies and programs conducted by the Japanese government and suggesting efficient and sustainable policies to the Thai government to help manage the budget for healthcare and the pension system, which will control the government’s fiscal risk in the future.

10

The result of this study may contribute to the suggestion of efficient and sustainable policies for the Thai government that may help to handle problems in an aged society and to manage the fiscal risks that come with such a society.

1.2 A Summary Review of Aging Population in Thailand and Government Policies

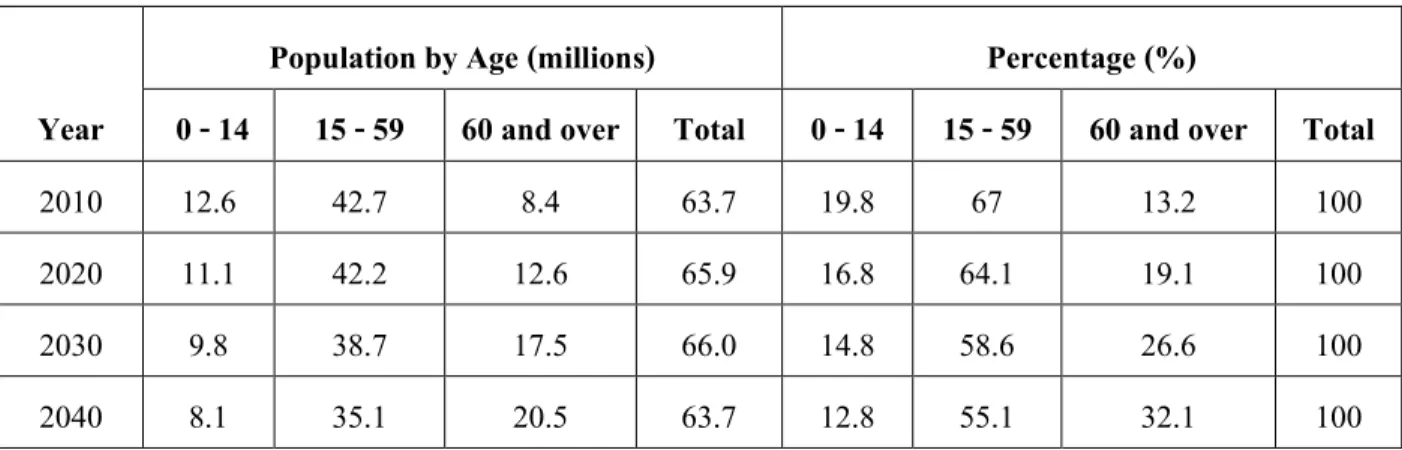

Thailand’s number of older people has been growing recently. According to the Office of the National Economic and Social Development Board of Thailand (see table 1), the number of people aged 60 and over was only 8.4 million, or 13% of the population in 2010. However, by 2040, Thailand’s aging population is expected to increase to 20.5 million, accounting for 32% of the population. This means that out of every four Thais, one person will be a senior.

Table 1: Thailand’s Population Projections over 30 years from 2010-2040

Population by Age (millions) Percentage (%)

Year 0 - 14 15 - 59 60 and over Total 0 - 14 15 - 59 60 and over Total

2010 12.6 42.7 8.4 63.7 19.8 67 13.2 100

2020 11.1 42.2 12.6 65.9 16.8 64.1 19.1 100

2030 9.8 38.7 17.5 66.0 14.8 58.6 26.6 100

2040 8.1 35.1 20.5 63.7 12.8 55.1 32.1 100

Source: Office of the National Economic and Social Development Board of Thailand as of September 20th, 2017

In terms of care and support for older people, the data collected for the Situation of Older People in Thailand report in 2007, which was revised again in 20112, showed that the well-being of the Thai older people has continued to develop. The number showed that only 15% of persons 60 and over mentioned that they need some assistance with their daily living activities; at age 75 and over, many people required more care and support from their family. However, these statistics do not account for the fact that 50% of older people do not have a child living in the same house or same area and 16% do not have living children. Moreover, the report showed that 75% of Thai elderly are satisfied with their financial status. In fact, 33% of older people still work daily

2 Knodel, John and Napaporn Chayovan, 2013. “The Changing Well-being of Thai Elderly: An Update from the 2011 Survey of Older Persons in Thailand.”

HelpAge International.

11

and 90.3% of them work in at least an informal manner. Another source of elderly income comes from government pension, or old age allowance, and from their family.

Regarding government policies relating to older people, the Thai government established the “National Committee of Senior Citizens”, and now the government’s current policies and programs are following with the second National Plan for Older Persons, which started in 2002 and will conclude in 2021. The National Plan focuses on the development of policies and efficient programs to support the elderly. At present, there are some successful program activities from the plan, such as the program for promoting a positive attitude toward elderly people, the program of promoting health for the elderly, and the program of social protection of the elderly.

Although the plan is being successfully implemented, the government still needs to be a leader to encourage cooperation from all participating sectors and to achieve the plan.

In addition, the government has been concerned about the healthcare and pension system for older people. For example, the government launched the universal coverage policy on health care finance to cover the 22% of the total population that was not covered by any kind of healthcare scheme in 2011. In terms of a pension system, in 2009, the government established the social pension policy called “the old age allowance”, which is financed from the annual budget through the Ministry of Interior. This scheme provided a secure income for older people. Even though the sum is not too high, the pension does serve its function as a social protection mechanism because it is a dependable source of income regardless of a person’s economic condition. Moreover, the Thai government has launched many schemes for supporting older people with their healthcare and pension system. There are some different conditions and benefits for each scheme, and this paper elaborates on those details in a later section.

In terms of projecting the fiscal burden of elderly citizens, the IMF’s technical assistance report in 2015 suggested that Thailand is facing the steep demographic transition and therefore could have important fiscal implications through its impact on age-related public spending. The projection models on public pension and health spending that the Ministry of Finance can use to monitor and evaluate the public pension and health systems on an ongoing basis. However, the IMF mentioned that there are several schemes from both the pension and health systems which are not yet well understood. Also, a comprehensive assessment of the fiscal burden

12

of public pension and health systems for the medium and long term is urgently needed. Moreover, the IMF mentioned that in order to project the fiscal burden away from public pension and health systems, a good model is needed.

In addition to Thailand, other developing countries should also be concerned about this issue.

According to the Report “Live Long and Prosper: Ageing in East Asia and the Pacific, 2016” from the World Bank, both Thailand and other developing countries are “getting old before getting rich”, which means the capability of the government to manage the speedily-aging population is more constrained than more developed countries, where the population grew rich while their working age populations were still growing. Moreover, the report showed that two thirds of Thais expected that the government will be their primary fund of financial support in old ages. Further, the report suggested that Thais should understand the situation; the rapid aging of the population is not just about old people, it concerns everybody. The government must think about a broad range of policy reforms. For example, the government should consider the policy related to how families decide how many children to have and strengthen public support for child care and a work-life balance for parents.

Moreover, policy reform will be needed to ensure that social security, health and long-term care systems achieve wide coverage and adequate financial protection for the elderly, while ensuring that public spending remains sustainable.

II. LITERATURE REVIEW

The United Nation (2001) uses above 60 years to refer to the elderly and categorizes a country’s level of aging population into three levels as follows:

1) “Ageing Society” refers to a society or country where the population of 60 years old and above is higher than 10% of the total population or a society or country where the population of 65 years old and above is higher than 7% of the total population.

2) “Aged Society” refers to a society or country where the population of 60 years old and above is higher than 20% of the total population or society or country where the population of 65 years old and above is higher than 14% of the total population.

13

3) “Super-aged Society” refers to a society or country where the population of 65 years old and above is higher than 20% of the total population.

Thailand’s projected population (from table 1) and the level of the aging population by the UN revealed that Thailand is going to be an “Aged Society” in 2030. Therefore, management of the aging society and policy guidelines are required in Thailand. According to Sunward (2015), Thailand’s preparation for an aging society in accordance with the government’s strategy to create good quality old age population together with the creation of improvement social security system for the elderly has not yet fulfilled the objective fromthe 2nd National Plan (2001-2021). However, in the past 5 years, welfare for the elderly has been continuously mobilized through government policy at a national level. A significant example is the promotion of saving for old age by the National Saving Fund Act B.E. 2554, which officially came into force on 20th August 2015.

Moreover, Suwanrada (2015) estimated the overall fiscal burden for the government under different pension schemes and concluded that in 2017, accumulated fiscal burden will be around 266,760 million baht, which will increase to around 473,439 million baht in 2040 or approximately 3.69% per year on average.

In terms of policy implementation, Sakunpanit (2012) emphasized analyzing the source of finances and methods used to raise money by the elderly in terms of efficiency, fiscal impacts and fiscal sustainability in the implementation of various policy alternatives. Sakunpanit pointed out that the fiscal burden for the government from the UCS scheme will increase due to the aging population. Therefore, if the government believes that the national health security is in need, “an increase in tax imposition and revision of the contribution of the UCS scheme” is suitable fiscal restructuring that will offer accessible healthcare provision for all. In addition, the government should examine the possibility of restructuring the management of pension funds and fiscal sustainability under different systems as well.

In addition, it’s obvious that the government will face a fiscal burden due to Thailand becoming a more aged society. However, the government should not be the only ones ready for that situation; the elderly should prepare themselves for the situation as well. Yodying & Suppanuta (2015) stated that Thailand cannot avoid being an aged society in the future, and therefore the government should increase elderly involvement in preparing for health and well-being into older age by promoting health, training healthcare providers, and supporting income security, social protection and poverty prevention. In addition, the government should

14

develop a supportive environment focusing on care givers and develop a positive image of aging. In order to succeed at all of the above, the efforts should be implemented through partnership with national and provincial government as well as community based organizations.

Furthermore, the source of income for older people is a significant point, and the government will need to develop an efficient policy to provide a source of income. According to Knodel, Prachuabmoh, & Chayovan (2015), who cited an update based on the 2014 Survey of Older Persons in Thailand, 40% of older persons worked during the prior 12 months; this is a slight decrease from 2011 but above the levels reported in the 1994 and 2002 surveys. The clear majority (85%) of persons 60 and older received the government Old Age Allowance in 2014, up from 81% in 2011; these high levels reflect the transformation of the program in 2009 into a universal social pension. Although almost 80% of older persons received some income from their children, only 37% reported children as their main source of income, down from 40% in 2011. For 15%, the Old Age Allowance was their main source of income in 2014, up modestly from 11% in 2011. Therefore, it is quite obvious that older people currently rely on the Old Age Allowance from the government more than in the past. Although the amount of the Old Age Allowance is small, it is still a significant source of income for older people. The government should perhaps allocate a greater amount of their budget to support an increase in the allowance that will be sufficient for old people to have a good quality of life.

CHAPTER III. THAILAND HEALTHCARE AND PENSION SYSTEM

3.1 Thailand Healthcare System

There are currently three main healthcare schemes in Thailand provided by the government: the Civil Servant Medical Benefit Scheme (CSMBS), which is organized bythe Comptroller General’s Department (CGD) under the Ministry of Finance, the Social Security Scheme (SSS), which is organized bythe Social Security Office (SSO) under the Ministry of Labour, and the Universal Coverage Scheme (UCS), which is organized by the National Health Security Office (NHSO) under the National Health Security Board and chaired by the public health minister from the Ministry of Public Health (MoPH). Moreover, there are other public health insurance schemes managed by state enterprises to provide healthcare coverage to their employees.

15 3.1.1 Civil Servant Medical Benefit Scheme (CSMBS)

Government employees and their dependents are covered under the CSMBS scheme starting from the beginning of employment. There are two types of reimbursement: direct payment and indirect payment. If patients register for the direct payment system at a public hospital, public hospitals can claim all expenses through the CSMBS. On the other hand, if the patients do not register for direct payment at a public hospital, the patients should reimburse through their affiliated office. However, service cost reimbursement at private health facilities is limited and only for accidents or life-threatening emergencies.

In terms of budget allocation, the government allocates to this scheme about 60,000 million baht every fiscal year, at 12,000 baht per person for 5 million people. However, the actual expense of CSMBS was actually higher than the annual budget for most years. From FY 2013 to FY 2017, the government disbursed the actual expense for CSMBS at 66,466, 59,772, 62,353, 71,036 and 73,870 million baht, respectively3. Therefore, it is obvious that the annual budget for the CSMBS does not completely cover the actual expenses, and the government must use money from the Central Fund to support CSMBS (see figure 1).

Figure 1: CSMBS’s Actual Expense as Percentage of National Budget

Million Baht Percentage (%)

3 Collected by Fiscal Policy Bureau, Fiscal Policy Office. As of September 20th, 2017

1,835,000 1,700,000 2,070,000 1,700,000 2,070,000 2,380,000 2,575,000 2,776,000 2,733,000

61,723 62,398 61,844 61,587 66,466 59,772 62,353 71,036 73,870

3.4

3.7

3.0

3.6

3.2

2.5 2.4 2.6 2.7

- 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

- 500,000 1,000,000 1,500,000 2,000,000 2,500,000 3,000,000

2009 2010 2011 2012 2013 2014 2015 2016 2017

National Budget CSMBS's Actual Expense CSMBS's Actual Expense as Percentage of National Budget

16 3.1.2 Social Security Scheme (SSS)

Launched in 1990, the SSS is a compulsory insurance scheme for employees in the private sector. The scheme only covers the employees themselves, and its inpatient and outpatient services are provided through both private and public hospitals. The SSS payment mechanism operates on a capitation basis, and copayments are added for some necessary but expensive services. Its source of funds comes from employees, employers, and the government. Under the SSS scheme, restrictions are applied. Health benefits under the SSS scheme begin after 3 months of contributions and the benefits continue for up to 6 months after unemployment.

Employees receive protection benefits under a total of seven circumstances,: illness or accident, physical disability, death not related to performance of work, child delivery, old age, child assistance, and unemployment. In terms of contribution from the government, the budget is allocated to the SSS through the Social Security Fund (SSF) every fiscal year. From FY 2013 to FY 2017, the government disbursed the budget for SSF as 30,920, 24,899, 27,992, 28,049 and 41,464 million baht, respectively4. The number of SSS members was approximately 10.33 million people in 2016, which means the budget for each person was about 2,860 baht.

The government will allocate the budget to the SSS depending on its policy and economic situation at that time.

For a decade, the government has spent around 1.2 % of the national budget on the healthcare and pension system through the SSS (see figure 2). However, as a contributor under the law, the government allocates a budget to the SSS less than the stated amount. As a result, the government debt to the SSS is 74,500 million baht, as of March 2017.

4 Budget in Brief, Bureau of Budget FY 2013 to FY 2017

17 Figure 2: SSS’s budget as Percentage of National Budget

Million baht Percentage (%)

Source: Budget Bureau (FY 2003- FY 2017), Thailand

3.1.3 Universal Coverage Scheme (UCS)

The National Health Security Office (NHSO) is a public organization under the Ministry of Public Health (MoPH) and was established in 2002. NHSO’s responsibility is to create health security for every Thai citizen, whereby “every person born as Thai should feel secure irrespective of being sick or healthy.” NHSO operates the “Universal Coverage Scheme” (UCS), which is responsible for developing a service system that is easy to access, an effective information system for communications, an evidence-based system of health care delivery and that enables the freedom to choose a registration facility in accordance with one’s personal preferences for convenience and necessity.

The UCS is the product of a long string of efforts to improve equity in health. Under this scheme, all Thais who are not the member of the CSMBS or SSS are eligible to enroll by registering with a contracting unit (a district healthcare provider network). Once registered, an individual will receive a gold card that entitles them to free care at health centers in their home district and other contracted hospitals, plus referrals to provincial or tertiary care hospitals in urban areas. Moreover, members are entitled to a comprehensive benefits package,

1,660,000 1,835,000 1,700,000 2,070,000 1,700,000 2,070,000 2,380,000 2,575,000 2,776,000 2,733,000

21,590 22,798 17,228 23,489 11,165 30,920 24,899 27,992 28,049 41,464

1.3 1.2

1.0 1.1

0.7

1.5

1.0 1.1 1.0

1.5

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6

- 500,000 1,000,000 1,500,000 2,000,000 2,500,000 3,000,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

National Budget SSS's Budget SSS's Budget as percentage of National Budget

18

which provided similar coverage to the pre-existing health insurance schemes and was recently extended to cover more expensive services.

In terms of funding, the UCS was mostly financed by income taxes, so it was proportionately more heavily funded by the rich than the poor people. Primarily, users paid a co-payment of 30 baht per visit.

However, collection of the co-payments ultimately cost more than the revenue it generated. The UCS budget, determined by the number of beneficiaries multiplied by a standard per-person rate, also increased in absolute and per capita terms. In FY 2003, the government allocated a budget of 27,138 million baht to the USC; by FY 2017, this amount had increased to 123,466 million. The proportion of the USC budget is about 4% of the national budget, on average. The number of USC members was approximately 50 million people in 2016, which means the budget was around 2,220 baht for each person.

In addition, other than budget allocation to NHSO directly, the government also allocates budget to MoPH to operate other agencies under the NHSO, such as the Department of Medical Service, the Department of Health Service Support, and the Department of Health. The total budget from FY 2013 to FY 2017 was 99,788, 106,103, 109,658, 123,542 and 130,764 million baht, respectively5. The government spends around 9%

of the national budget for the healthcare and pension system through NHSO and MoPH each year (see Figure 3).

5 Budget in Brief, Bureau of Budget FY 2013 to FY 2017

19

Figure 3: MoPH’s Budget as a Percentage of the National Budget

Million baht Percentage (%)

Source: Bureau of the budget (FY 2003- FY 2017)

Since there are three main healthcare schemes (see Table 2) in Thailand, there are many questions about the differences among the schemes, such as the budget from the government for each person, the benefit from each package, and the method of claim or reimbursement. However, it can be explained that CSMBS is the welfare that the government provides for its employees. Therefore, 100% of the funding comes from the government. On the other hand, the SSS is social welfare for which 3 parties, the government, employers and employees, contribute to with funds. UCS is a national welfare programs for all citizens who are not civil servants and cannot join the SSS; like CSMBS, UCSi is 100% financed from the government. However, to sustain all three healthcare systems due to the aging population will be very challenging for the government.

Some schemes should be reformed, and the government should seriously concern itself with minimizing fiscal risk in the future.

Table 2: Basic Characteristics of the Three Main Healthcare Schemes in Thailand

Employment Contributions,

Coverage Entry

Condition (s) Health Insurance

Scheme

Type of

Payment Benefit

Package Claim,

Reimbursement Organizations Related or Systems

Notes Government

employees and their dependents (parents,

- Government - Membership is 5 million people

- CSMBS - Fee-for-

service - Diagnostic related-

OP and IP services at any public healthcare facilities,

1. When direct payment was set up, hospital claims through the CSMBS

1. Hospitals 2. Central office of Health Information (CHI)

Service cost reimburseme nt at private health facilities is limited and

1,660,000 1,835,000 1,700,000 2,070,000 1,700,000 2,070,000 2,380,000 2,575,000 2,776,000 2,733,000

141,834 152,593 161,010 187,963 199,370 208,533 221,280 224,622 246,551 254,230

9 8 9 9

12

10 9 9 9 9

- 2 4 6 8 10 12 14

- 500,000 1,000,000 1,500,000 2,000,000 2,500,000 3,000,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

National Budget MoPH's and UCS's budget MoPH's and UCS'S budget as percentage of national budget

20

Employment Contributions,

Coverage Entry

Condition (s) Health Insurance

Scheme

Type of

Payment Benefit

Package Claim,

Reimbursement Organizations Related or Systems

Notes spouse and

up to 3 children < 21 years old.)

(approximately 7.5 % of total population)

Group (DRG) method for inpatient (IP) - Per item with ceiling for outpatient (OP)

except for health promotion and disease prevention (PP) services

2. Without direct payment setup, the patients can get reimburse through their affiliated office.

3. CSMBS 1. Patients 2. Patients’

affiliated office 3. GFMIS system 4. CSMBS

only for accident or emergency threaten to life.

Formal private employees

- Government, Employers, And Employees - Membership is 12 million people (approximately 17.5% of total population)

>= 3-month Of contributions, and up to 6- month after unemployed

Less than 7-month of Contributions Within the first 3-month of contributions

SSS

UCS

- Capitation - DRG method with global budget for IP

OP and IP services at main contractor or subcontrac tors, or refer as needed, except for PP services

1. No

reimbursement for basic package included in capitation.

2. reimbursement for IP and additional vertical programs 3. patient reimburses for emergency services out of service network.

1. Hospitals 2. SSO provincial branch office 3. SSO

1. Patients 2. SSO provincial branch office 3. SSO

Service cost reimburseme nt at private health facilities is limited and only as needed.

Unemployed, or another informal sector workers

- Government - Membership is 50 million people (approximately 75% of national population) + nonregistered qualified citizens (2%)

Does not have any other government health benefit.

UCS - Capitation - DRG method with global budget for IP

- OP and IP services at primary care contractors , or refer as need - Health promotion and disease prevention (PP) programs for all citizens

1. No

reimbursement for basic package included in capitation.

2. Reimbursement for IP and additional vertical programs

1. Hospitals 2. Central office of Health Information (CHI) on some vertical programs 3. The ministry of public health (MOPH) on PP programs 4. National Health Security Office (NHSO)

When they are eligible to UCS, the first service is covered and register is requited at the Health facilities.

(only registered UCS are count for government budget allocation.) Source: Journal of the Thai Medical Informatics Association, 2015

3.2 Thailand Pension System

As mentioned above, Thailand is dealing with a rapidly growing population of older persons. Therefore, the Thai Government has allocated funds from the annual budget to provide old-age income security to elderly.

As can be seen from Table 3, the government budget for old-age income security has increased each year from

All claims and reimbursements are managed under the UCS scheme claim

UCS for Pregnancy

UCS

21

FY 2013 to 2017. It can also be noted that the government budget on old-age is around 11.4% on average as percentage of national budget (see Figure 4).

Table 3: Government Budget on Old-Age Income Security for FY 2013 to 2017

Scheme 2013 2014 2015 2016 2017

Old Age Allowance 58,500 56,500 57,000 58,000 59,000

Social Security Fund* 30,920 24,900 28,000 27,000 41,400

Government Pension 124,000 132,200 149,500 175,700 179,000

Government Pension Fund 35,000 47,000 45,300 46,000 46,000

National Saving Fund 500 - - 600 650

Total (Million baht) 248,920 260,600 279,800 307,300 326,050

Source: Bureau of Fiscal policy, Fiscal Policy Office as of October 1st, 2016

Note: for 7 circumstances, namely: illness or accident; physical disability; death not related to performance of work; child delivery; old age, child assistance and unemployment

Figure 4: Government Budget for Old-Age as Percentage of National Budget

Million baht Percentage (%)

Source: Bureau of Fiscal Policy, Fiscal Policy Office as of October 1st, 2016

In Thailand

,

the current pension system is comprised of 4 pillars, namely a non-contributory pillar, a mandatory defined benefit pillar, a mandatory defined contribution pillar, and a voluntary defined contribution pillar (see Figure 5)2,070,000 2,380,000 2,575,000 2,776,000 2,733,000 248,920 260,600 279,800 307,300 326,050

12.0 10.9 10.9 11.1 11.9

10.0 10.5 11.0 11.5 12.0 12.5

- 500,000 1,000,000 1,500,000 2,000,000 2,500,000 3,000,000

2013 2014 2015 2016 2017

National Budget Government's Budget for old-age Government's Budget as percentage of National Budget

22 Figure 5: Pension System in Thailand

Source: Bureau of Saving and Investment Policy, Fiscal Policy Office as of September 20th, 2017

3.2.1 Pillar 0: “A non-contributory pillar”

Old Age Allowance - the scheme is a non-contributory social protection which aims to guarantee basic income for Thai citizens aged 60 and above. Persons qualified to receive the allowance are Thai elderly who do not receive pensions from the central and local government, thereby excluding civil servants who receive pensions from the central or local government. The amount of this allowance depends on the age of the recipient as follows:

Table 4: Old Age Allowance (Baht)

Age Allowance per Month

60-69 600

70-79 700

80-89 800

90 and above 1,000

Source: Ministry of Social Development and Human Security as of September 20th, 2017

23

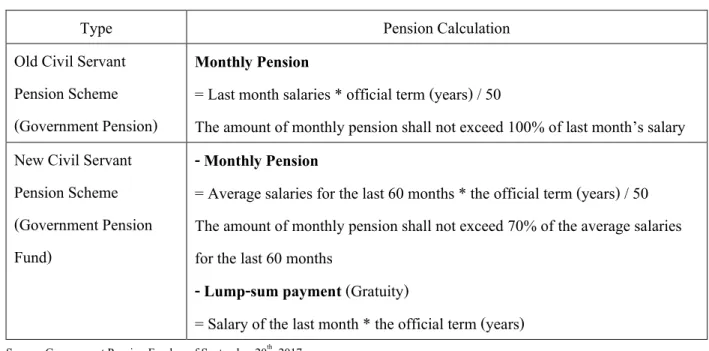

The Civil Servant Pension Scheme - the scheme is a non-contributory defined benefit plan for government officials (5 million people) and financed out of government budget allocation. Under the Civil Servant Pension Scheme, government officials are entitled to receiving a pension in the form of a monthly payment, provided that they have at least 25 years of service, or 10 years of service if aged over 50. For other cases, the government official will receive lump sum benefits after working at least 10 years or one year of service if aged above 50.

There are two types of pension calculations for the government officials. One is for the old Civil Servant Pension Scheme, which is for civil servants entering service before 1997. The second one is for the new Civil Servant Pension Scheme, which is for civil servants entering service after 1977 (see Table 5).

Table 5: Pension Calculation

Type Pension Calculation

Old Civil Servant Pension Scheme (Government Pension)

Monthly Pension

= Last month salaries * official term (years) / 50

The amount of monthly pension shall not exceed 100% of last month’s salary New Civil Servant

Pension Scheme (Government Pension Fund)

- Monthly Pension

= Average salaries for the last 60 months * the official term (years) / 50 The amount of monthly pension shall not exceed 70% of the average salaries for the last 60 months

- Lump-sum payment (Gratuity)

= Salary of the last month * the official term (years)

Source: Government Pension Fund as of September 20th, 2017

3.2.2 Pillar 1: “a mandatory defined benefit pillar”

Social Security Fund (SSF) – the fund was established in 1990 under the Social Security Fund Act B.E. 2532 (1990). SSF covers formal sector private employees (12 million people). Employers and employees are both mandated by law to make contributions to the fund. In terms of financing, the scheme is financed by tripartite contributors which are government (1% of salary), employers and employees (each 3% of salary but not above 450 baht per month, as the salary base used to calculate must range between 1,650 and 15,000 baht).

24

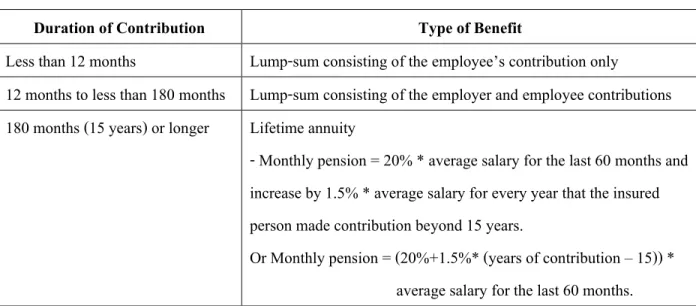

An insured person will receive a lump-sum payment or a pension paid monthly when they retire at 55 years old for a life time. The monthly payment depends on the duration for each insured person has contributed as follows:

Table 6: The benefit for an insured person based on duration of contribution

Duration of Contribution Type of Benefit

Less than 12 months Lump-sum consisting of the employee’s contribution only

12 months to less than 180 months Lump-sum consisting of the employer and employee contributions 180 months (15 years) or longer Lifetime annuity

- Monthly pension = 20% * average salary for the last 60 months and increase by 1.5% * average salary for every year that the insured person made contribution beyond 15 years.

Or Monthly pension = (20%+1.5%* (years of contribution – 15)) * average salary for the last 60 months.

Source: Bureau of Saving and Investment Policy, Fiscal Policy Office as of September 20th, 2017

3.2.3 Pillar 2: “A mandatory defined contribution pillar”

Government Pension Fund (GPF) – the fund is a defined contribution fund established on March 27th, 1997 under the Government Pension Fund Act B.E. 2539 (1996). The scheme is a mandatory defined contribution plan for civil servants who were employed after March 27, 1997. Other civil servants who were employed before that time can choose whether or not to apply to become a member of the fund. Members are required to contribute 3% of their salaries every month; the government, as their employer, adds the same amount to the fund. Members can also make a higher contribution of up to 15% of their salary. The number of the members as of 31 December 2016 was around 1 million people6.

3.2.4 Pillar 3: “A voluntary defined contribution pillar”

(1) Provident Fund (PVD) – the fund is an occupational pension and established under an agreement between employer and employees for the purpose of offering retirement saving to employees. When

6 Government Pension Fund annual report of 2016

25

the fund is set up, employer and employees both are required to make contributions together which range from 2% to 15% of the salary in each employee.

In terms of termination, it comes about by either one of three factors: retirement at 55 or older as stipulated in the governing rules, resignation, or death. When membership is determined, members are entitled to a full amount of benefit package in accordance with the fund article. In addition, portability among provident funds and installment payments are allowed by law.

(2) National Saving Fund (NSF) – the fund is a new voluntary retirement saving program which was introduced by the government in 2011 (beginning operations in 2015). It is intended to cover Thai citizens who are not covered by any other pension schemes, particularly informal workers. In terms of membership, Thai Nationals aged 15–60 are eligible to become a member of NSF. Under the scheme, members can contribute from 50 to 13,200 baht per year. The government will be a co-contributor in this scheme together with members, depending on the amount of (members) contribution and age with a ceiling as follows:

Table 7: The ceiling of co-contribution from the government by age

Age of Member Co-contribution from the government 15 - 30 50% with a ceiling of 600 baht per year 30 - 50 80% with a ceiling of 860 baht per year 50 and above 100% with a ceiling of 1,200 baht per year

Source: National Saving Fund as of September 20th, 2017

If retirement begins at age 60, a member will receive a pension paid monthly for a lifetime; the amount of the pension varies depending on the amount of contributions made.

(3) Retirement Mutual Fund (RMF) – the fund is a voluntary long-term fund suitable for individuals earning income in such forms as wages, salary, and freelance income. Moreover, it is particularly suitable for those who are not a member of a provident fund, government pension fund or otherwise wish to further enhance their current retirement savings. Investors who invest in RMF will get tax exemption up to a maximum of 15% of the annual taxable income. However, the amount of the 15% annual taxable income has to combine to government pension funds, provident funds, private teacher aid funds, and pension insurance premiums, and the total investment shall not exceed 500,000 baht.

26 3.2.5 Proposed National Pension Fund (NPF)7

The Ministry of Finance proposed the National Pension Fund (NPF), which is a mandatory provident fund appropriate for formal workers that fit into Pillar 2. Since there are several pillar pension systems in Thailand, some groups of workers are liable to be in poverty in their old age, especially those who rely merely on pension from the Social Security Fund. In accordance with the basic protection of the social security system, the amount of post-retirement income will be very low, at around 19% of a workers’ last month’s salary; this is far from a sufficient level at around 50%. For this reason, the government has to take action to prepare a sufficient monthly pension for those people to reduce the risk of a huge fiscal burden on elderly welfare systems in the long run.

There are three main objectives to set up the NPF as following:

(1) The most important objective is to ensure an adequate post-retirement income with no less than 50% of workers’ latest salary

(2) The government expects the fund to be financially self-sustained due to the defined-contribution features of the fund

(3) The fund is expected to increase long-term domestic savings, by approximately 60 billion baht or 1,700 million USD in the first year, up to 1.78 trillion baht or 50,000 million USD by the tenth year.

In addition, the fund will be regulated by the Ministry of Finance, while the Stock Exchange of Thailand will regulate asset management companies who will manage the investment of the fund.

In terms of features of NPF8, the fund is expected to cover employees in the private sector, temporary employees in the public sector and employees of stat-owned enterprise; approximately 11 million formal workers in total will be covered under this law. For contributions, both employers and employees are obliged to make monthly saving to the fund at a rate of 3% of the salary. This rate will be increased to 5%, 7% and 10%

within 10 years and with the wage ceiling at 60,000 baht per month. However, employees who would like to

7Bureau of Saving and Investment Policy, Fiscal Policy Office as of September 30th, 2017

8 Draft of the National Pension Act is currently under the consideration of the Council of the State as of September 30th, 2017

27

contribute more can contribute up to 15% of their salary. For employees who earn less than 10,000 baht per month, they do not have to make contributions and their employers will contribute alone to the fund.

Once employees get to 60 years old, they will receive a 20-year pension or lump-sum payments from the fund of a total amount equal to the balance of their individual accounts. For investment, the fund will be managed by asset management companies (AMCs) that will be approved by the NPF board. In addition, the members will get the exemption of taxation on contribution, returns from investment, and pension benefits.

Eventually, the government expects that the establishment of the fund will help increase the post-retirement income of formal workers from 20% to 50% of their pre-retirement income.

CHAPTER IV: JAPAN HEALTHCARE AND PENSION SYSTEM

Japan became an aged population country more than 40 years ago. According to 2015 census data released by the Ministry of Internal Affairs and Communications, Japanese people aged 65 or over make up a record 26.7% of Japan’s population of 127 million, which increased by 3.7 % since the last survey was conducted in 2010. The increasing number of older people in Japan will affect the number of workers in the future. Government data showed the number of workers in Japan is projected to fall by 7.9 million, or 12.4%, to 55.61 million by 2030. Moreover, the overall population will drop to 86 million in 2060, with the proportion of people aged 65 or over reaching nearly 40% of the total.

Therefore, it is obvious that the government is challenged by the aging population and declining fertility. As a result, social security expenses have been increasing sharply. On the other hand, the number of contributors from workers is decreasing rapidly, creating doubt about how the government will sustain the current security system.

4.1 Japan Healthcare system

According to the Ministry of Health, Labour and Welfare, all Japanese people are secured under public health insurance. Nowadays, there are three main healthcare insurance systems in Japan.

28 4.1.1 National Health Insurance (NHI)

This system is operated by municipalities and NHI associations for individuals who are aged less than 74 years old and not the member of employees’ insurance system. Therefore, the members in this system are self-employed individuals, farmers, non-regular employees, unemployed people, and retired persons under self- employees’ health insurance. The financial resources of NHI come from premiums and state subsidies. In terms of the premium, it is calculated for each household depending on the ability to pay. For payment, NHI is a co- payment between members and the government, which is different depending on its condition (see Table 8).

Table 8: Summary of National Health Insurance

Types of Member Premium Financial resources Co-payment Type 1

Farmers, self-employed individual, non-regular employees, etc.

(operated by municipalities and NHI associations) Type 2

Retired person under employees’ health insurance (operated by NHI

associations)

Calculated for each household depending on the benefits received and ability to pay

(levy calculation formulas differ among insurers)

1. Premium

2. Municipalities and NHI associations will subsidy at 41% of benefit expenses, etc.

None (healthcare expenses for retirees who were waged earners for at least 20 years and enroll in NHI are covered by municipally administered NHI using contributions from Employees Insurance)

1. 30% for people after reaching compulsory education age until 69 years old

2. 20% for people before reaching compulsory education age

3. 20% for people 70 - 74 years old 20%

(except people who have more than certain level of income will pay 30%)

4. 10% for those already turned 70 years old by the end of March 2014

Source: The ministry of Health, Labour and Welfare as of June 2015.

29 4.1.2 Employees’ Health Insurance

The members under this system are general employees, national public employees, local public employees, and private school teachers/staff. There are different insurers operating health insurance depending on the type of members. The Japan Health Insurance Association operates health insurance for employees of small and medium companies. Health Insurance Societies operate health insurance for employees of large companies. Mutual aid associations operate health insurance for national public employees, public employees, and private school teacher/staff. Table 9 shows the differences of financial funding, premiums and government subsidies for each type. For example, the premium (equal between employers and employees) for employees of small and medium companies is 10% while the premium for employees of large companies is not fixed and depends on the insurers. However, this system involves a co-payment, where all insured individuals must pay 30% of the service expenses. In case of type 3, the premium varies depending on the core insured person’s income and additional subscribers.

Table 9: Summary of Employees’ Health Insurance

Types of Member Premium Financial resources Co-payment

Type 1

Employees of large companies (operated by health insurance society)

Different among health insurance society

1. Premium

2. State subsidy from the budget at fixed amount

Insured person must pay 30%

Type 2

Employees of small and medium companies

(operated by Japan health insurance association)

10%

(National average)

1. Premium

2. State subsidy from the budget at16.4% of benefit expenses, etc.

Insured person must pay 30%

Type 3

- National public employees - Local public employees - Private school teachers/staff (operated by mutual aid association)

- from 6% to 10%

- 12%

- 7.56%

(as of September 2010)

1. Premium

2. Administrative cost (depends on Insured person)

Insured person must pay 30%

Source: Ministry of Health, Labour and Welfare as of June 2015.

30 4.1.3 Late – state Medical care system for the elderly

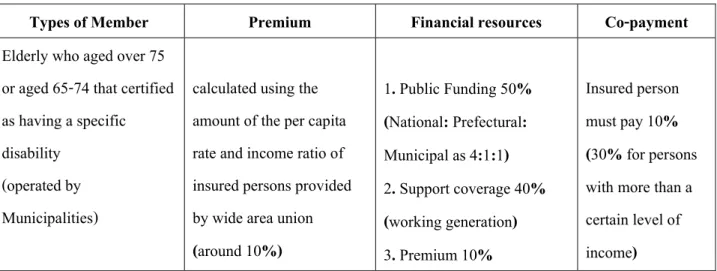

The system is provided for elderly people at least 75 years old or between 65-74 years old and certified as having a specific disability by a wide area union operated by Municipalities (NHI) (see Table 10). For the funding term, the funding resources come from the premium at 10%, which is calculated by using the amount of the per capita rate and income ratio of insured persons provided by wide area union, the government subsidy at 50% and support coverage from working generation at 40%. The insured person must pay basically 10%.

Table 10: Summary of the Late–State Medical Care System for the Elderly

Types of Member Premium Financial resources Co-payment

Elderly who aged over 75 or aged 65-74 that certified as having a specific disability

(operated by Municipalities)

calculated using the amount of the per capita rate and income ratio of insured persons provided by wide area union (around 10%)

1. Public Funding 50%

(National: Prefectural:

Municipal as 4:1:1) 2. Support coverage 40%

(working generation) 3. Premium 10%

Insured person must pay 10%

(30% for persons with more than a certain level of income)

Source: Ministry of Health, Labour and Welfare as of June 2015

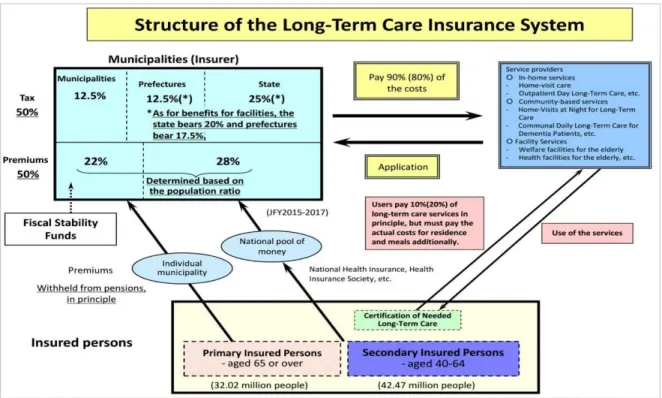

Besides the healthcare system, Japan provides long-term care insurance through a system established in 2000. One of the objectives for this system is to separate long-term care from coverage of healthcare insurance and decrease cases of "social hospitalization" as the first step toward restructuring the social security system9. The system is for people aged 65 or above or aged 40-64 and in need of long-term care. The service is provided to the former regardless of the causes of their illnesses and to the latter if they have terminal cancer or diseases caused by aging, such as Arthrorheumatism.

The municipalities and special wards in the metropolitan area are an insurer of public long-term care.

The source of fund comes from the premiums (insured person) and taxation equally (50:50). In terms of

9 Ministry of Health, Labour and Welfare, Japan.

31

premiums, 22% is collected from insured persons aged 65 and the rest (28%) comes from those aged 40-64. For taxation, the contribution comes from state (25%), prefecture (12.5%) and municipalities (12.5%). Furthermore, this system involves co-payments between insured person and municipalities. The insured person must pay 10%

or 20% depending on their income, and municipalities pay for the rest at 90% or 80% (Figure 6).

Figure 6: Structure of the Long-Term Care Insurance System

Source: Annual report 2016 Edition, Ministry of Health, Labour and Welfare.

Regarding budget allocation, the Japanese government allocates the budget for social securities through the Ministry of Health, Labour and Welfare. The percentage of the social security budget was, on average, about 3% of general account from FY 2008 to 201710. Figures 7 and 8 show the budget allocation data for healthcare and long-term care, which was collected from the Budget Bureau and Ministry of Health, Labour and Welfare.

On average, the government allocated 11% of the national budget to general healthcare and 3% of the national budget to long-term care. Therefore, it can be noted that the government allocates 14% of the national budget in total to both systems, which is almost half as much as is allocated from the national budget for social security.

10 The data of FY 2009 to 2011 and 2015 were calculated by the writer using probability of trend and average number from historical data.