Challenges

著者 Usui Norio

journal or

publication title

Kansai University review of economics

volume 6

page range 1‑25

year 2004‑03

URL http://hdl.handle.net/10112/12091

•—--—--- ‑

---~-iK a n s a i U n i v e r s i t y Review o f Economics N o . 6 ( M a r c h 2 0 0 4 ) , p p . 1 ‑ 2 5

I n d o n e s i a ' s New Block Grant T r a n s f e r :

I t s E q u a l i z a t i o n Performance and Remaining Challenges*

N o r i o U s u i

A key p r i n c i p l e i n successful f i s c a l d e c e n t r a l i z a t i o n i s t o guaran‑

tee a reasonable balance between expenditure needs and revenue c a p a c i t i e s a t lower l e v e l s of government. This paper reviews the a l l o c a t i o n methods of Indonesia's new block grant transfer scheme, a mainstay of intergovernmental f i s c a l r e l a t i o n s a f t e r d e c e n t r a l i z a ‑ t i o n , and assesses i t s e q u a l i z a t i o n performance by conducting sim‑

p i e simulation e x e r c i s e s . Before a l l e l s e , e q u a l i z a t i o n function of the block grant needs to be more c l e a r l y d e f i n e d . Major challenges r a i s e d a r e : 1 ) conceptual and design weaknesses of f i s c a l capacity and expenditure needs s p e c i f i c a t i o n s i n the a l l o c a t i o n formula; 2 ) unequalizing e f f e c t s of non‑formula a l l o c a t i o n s , i n p a r t i c u l a r b a l ‑ ancing f a c t o r a l l o c a t i o n s ; 3 ) inappropriate sharing arrangement between provinces and l o c a l governments; and 4 ) p r o h i b i t i o n of non‑negative t r a n s f e r s .

Keywords: Block Grant, Expenditure Needs, F i s c a l C a p a c i t y , E q u a l i z a t i o n Performance

1 . I n t r o d u c t i o n

A f t e r a l o n g p e r i o d o f c e n t r a l i z e d a u t h o r i t a r i a n r u l e , I n d o n e s i a i n i t i a t e d a d r a s t i c d e c e n t r a l i z a t i o n program i n f i s c a l year ( F Y ) 2 0 0 1 . Although v a r i o u s e f f o r t s were made t o empower r e g i o n a l governments1 even b e f o r e t h e d e c e n t r a l i z a t i o n , p o l i t i c a l d i f f i c u l t i e s i n m a i n t a i n i n g n a t i o n a l u n i t y a f t e r t h e 1 9 9 7 economic c r i s i s c r e a t e d a s t r o n g and u r g e n t need t o d e c e n t r a l i z e t h e c o u n t r y f o r t h e f i r s t time i n I n d o n e s i a . The h i e r a r c h i c a l r e l a t i o n s h i p b e ‑

* T h i s p a p e r u p d a t e s a n a l y s e s o f I n d o n e s i a ' s b l o c k g r a n t a l l o c a t i o n methods i n my p r e v i o u s p a p e r s , U s u i ( 2 0 0 3 a ) and U s u i ( 2 0 0 3 b ) , b a s e d on new i n f o r m a t i o n and r e c e n t d e v e l o p m e n t s . The a u t h o r would l i k e t o t h a n k P r o f e s s o r M. G . A s h e r ( N a t i o n a l U n i v e r s i t y o f S i n g a p o r e ) , D r . B . B i k a l e s ( A s i a n Development B a n k ) , P r o f e s s o r S . H o n d a i ( K o b e U n i v e r s i t y ) , and P r o f e s s o r K . Hashimoto ( K a n s a i U n i v e r s i t y ) f o r t h e i r comments on e a r l i e r d r a f t s . D i s c u s s i o n s w i t h D r . B . D . L e w i s ( R e s e a r c h T r i a n g l e l n s t i t u t e / M O F a d v i s o r ) a r e d e e p l y a p p r e c i a t e d . A p a r t o f t h i s s t u d y was f i n a n c e d by t h e K a n s a i U n i v e r s i t y G r a n t ‑ i n ‑ A i d f o r t h e F a c u l t y J o i n t R e s e a r c h Program 2 0 0 3 . The u s u a l d i s c l a i m e r a p p l i e s . 1 I n t h i s p a p e r , t h e t e r m " r e g i o n a l government" encompasses b o t h p r o v i n c i a l and l o c a l g o v e r n ‑

m e n t s , w h i l e " l o c a l government" r e f e r s t o K o t a and K a b u p a t e n .

ー

tween p r o v i n c i a l and l o c a l governments c a l l e d Kota ( m u n i c i p a l i t y o r c i t y ) and Kabupaten ( r e g e n c y o r d i s t r i c t ) was e l i m i n a t e d , and a l l l o c a l govern‑

ments became f u l l y autonomous and r e s p o n s i b l e f o r p l a n n i n g , manage‑

ment, f i n a n c i n g , and major p u b l i c s e r v i c e d e l i v e r i e s . While p r o v i n c i a l governments a l s o a c t as autonomous r e g i o n s , they r e t a i n a h i e r a r c h i c a l r e l a t i o n s h i p w i t h t h e c e n t r a l government. At t h e same t i m e , about two m i l ‑ l i o n c e n t r a l c i v i l s e r v a n t s , who worked a t r e g i o n a l o f f i c e s o f c e n t r a l l i n e m i n i s t r i e s , were t r a n s f e r r e d a d m i n i s t r a t i v e l y t o r e g i o n a l governments.

I n d i s c u s s i n g d e c e n t r a l i z a t i o n i n developing c o u n t r i e s , we c o n f r o n t a b a s i c q u e s t i o n about t h e r e l a t i o n s h i p be

切eend e c e n t r a l i z a t i o n and e c o ‑ nomic g r o w t h . Some emphasize t h a t d e c e n t r a l i z a t i o n can l e a d t o macro‑

economic i n s t a b i l i t y , which can i n h i b i t economic g r o w t h , and o t h e r s argue t h a t , i n developing c o u n t r i e s , d e c e n t r a l i z a t i o n can n o t r e a p i t s b e n e f i t s due t o i n s t i t u t i o n a l and human r e s o u r c e c o n s t r a i n t s . We i n s i s t , however, t h a t d e c e n t r a l i z a t i o n i n c r e a s e s economic e f f i c i e n c y i n p u b l i c spending a n d , t h a t i t can t h e r e f o r e be growth e n h a n c i n g . There a r e w e l l e s t a b l i s h e d i m p l e ‑ mentation p r i n c i p l e s which can h e l p t o r e a l i z e d e c e n t r a l i z a t i o n i n a way which i s l i n k e d t o e f f i c i e n c y and which enhances g r o w t h : 1 ) e x p e n d i t u r e s should f o l l o w c a p a c i t i e s ; 2 ) revenues should f o l l o w e x p e n d i t u r e s ; and 3 ) d e c e n t r a l i z a t i o n should be d e f i c i t ‑ n e u t r a l .

Although I n d o n e s i a ' s d e c e n t r a l i z a t i o n i s deeply r o o t e d i n t h e s p e c i f i c p o l i t i c a l m o t i v a t i o n , a key o b j e c t i v e i s t o i n c r e a s e economic e f f i c i e n c y by u t i l i z i n g t h e i n f o r m a t i o n advantages o f lower l e v e l s o f government i n pub‑

l i c s p e n d i n g . I n t e r g o v e r n m e n t a l f i s c a l r e l a t i o n s should be e s t a b l i s h e d t o guarantee a r e a s o n a b l e b a l a n c e between e x p e n d i t u r e r e s p o n s i b i l i t i e s and revenue i n s t r u m e n t s a v a i l a b l e t o r e g i o n a l governments. A b a s i c p r i n c i p l e i s t h a t e x p e n d i t u r e r e s p o n s i b i l i t i e s should come f i r s t , and revenue r e s p o n s i ‑ b i l i t i e s should be assigned n e x t . Without a c a r e f u l assessment o f f i s c a l needs t o f i n a n c e newly devolved e x p e n d i t u r e r e s p o n s i b i l i t i e s , i t i s n o t p o s ‑ s i b l e t o e f f i c i e n t l y determine revenue assignments t o r e g i o n a l govern‑

ments. However, i n r e a l i t y , I n d o n e s i a ' s d e c e n t r a l i z a t i o n s t a r t e d without c l e a r e x p e n d i t u r e a s s i g n m e n t s . Although t h e Government o f I n d o n e s i a ( t h e Government) l i s t e d newly devolved f u n c t i o n s o f r e g i o n a l governments2,

2 D e c e n t r a l i z a t i o n laws and r e g u l a t i o n s d e f i n e r o l e s o f r e g i o n a l governments o n l y i n g e n e r a l t e r m s :

l o c a l governments t a k e primary r e s p o n s i b i l i t i e s f o r p u b l i c w o r k s , h e a l t h , e d u c a t i o n , a g r i c u l t u r e ,

communication, i n d u s t r y and t r a d e , i n v e s t m e n t , environment, l a n d m a t t e r s , c o o p e r a t i v e s , and

human r e s o u r c e s , w h i l e p r o v i n c i a l governments p l a y c o o r d i n a t i n g r o l e s .

一

3

t h e r e i s s t i l l c o n s i d e r a b l e c o n f u s i o n on about how a u t h o r i t y between t h e d i f f e r e n t l e v e l s o f government should be demarcated. A c c o r d i n g l y , o b l i g a ‑ t o r y f u n c t i o n s f o r l o c a l governments and t h e i r minimum s e r v i c e s t a n d a r d s have n o t y e t been e s t a b l i s h e d .

Compared w i t h t h e vague e x p e n d i t u r e a s s i g n m e n t s , t h e Government has prepared r e l a t i v e l y c l e a r revenue a s s i g n m e n t s . B e f o r e FY2001, t h e r e e x i s t e d two t r a n s f e r s from t h e c e n t e r t o r e g i o n s : ( i ) Subsidy t o Regions ( S D O ) , which was mainly used t o f i n a n c e s a l a r i e s o f r e g i o n a l c i v i l s e r v a n t s ; and ( i i ) R e g i o n a l Development Funds (INPRES) f o r r e g i o n a l development a c t i v i t i e s . Since F Y 2 0 0 1 , both t r a n s f e r s have been e l i m i n a t e d and i n s t e a d combined i n t o t h e G e n e r a l A l l o c a t i o n Fund ( D A U ) , a b l o c k g r a n t . I n d o n e s i a a l s o expanded t h e revenue s h a r i n g system t o a s s i g n each r e g i o n a l govern‑

ment i t s share o f revenues from t a x e s on p e r s o n a l income, l a n d and b u i l d ‑ i n g , t r a n s f e r o f l a n d s and b u i l d i n g s , f o r e s t r y , m i n i n g , f i s h e r i e s , o i l , and n a t u r a l g a s . Another newly i n t r o d u c e d t r a n s f e r was t h e S p e c i a l A l l o c a t i o n

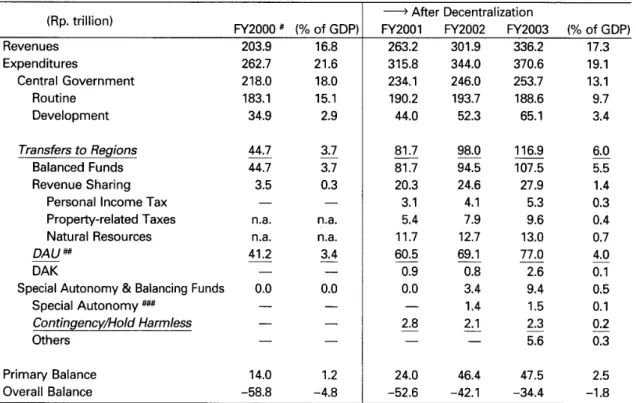

Table 1 C e n t r a l Budgets and T r a n s f e r s to Regions

( R p . t r i l l i o n ) 一 A f t e rD e c e n t r a l i z a t i o n

FY2000

# (%o f GDP) FY2001 FY2002 FY2003

(%o f GDP) Revenues 2 0 3 . 9 1 6 . 8 2 6 3 . 2 3 0 1 . 9 3 3 6 . 2 1 7 . 3 Expenditures 2 6 2 . 7 2 1 . 6 3 1 5 . 8 3 4 4 . 0 3 7 0 . 6 1 9 . 1 C e n t r a l Government 2 1 8 . 0 1 8 . 0 2 3 4 . 1 2 4 6 . 0 2 5 3 . 7 1 3 . 1 Routine 1 8 3 . 1 1 5 . 1 1 9 0 . 2 1 9 3 . 7 1 8 8 . 6 9 . 7 Development 3 4 . 9 2 . 9 4 4 . 0 5 2 . 3 6 5 . 1 3 . 4 T r a n s f e r s t o Regions 4 4 . 7 3 . 7 8 1 . 7 9 8 . 0 1 1 6 . 9 6 . 0 Balanced Funds 4 4 . 7 3 . 7 8 1 . 7 9 4 . 5 1 0 7 . 5 5 . 5 Revenue Sharing 3 . 5 0 . 3 2 0 . 3 2 4 . 6 2 7 . 9 1 . 4 Personal Income Tax 3 . 1 4 . 1 5 . 3 0 . 3 P r o p e r t y ‑ r e l a t e d Taxes n . a . n . a . 5 . 4 7 . 9 9 . 6 0 . 4 N a t u r a l Resources n . a . n . a . 1 1 . 7 1 2 . 7 1 3 . 0 0 . 7 DAU## 4 1 . 2 3 . 4 6 0 . 5 6 9 . 1 7 7 . 0 4 . 0

OAK 0 . 9 0 . 8 2 . 6 0 . 1

S p e c i a l Autonomy & Balancing Funds 0 . 0 0 . 0 0 . 0 3 . 4 9 . 4 0 . 5 S p e c i a l Autonomy

###1 . 4 1 . 5 0 . 1 Contingency/Hold Harmless 2 . 8 2 . 1 2 . 3 0 . 2

Others 5 . 6 0 . 3

Primary Balance 1 4 . 0 1 . 2 2 4 . 0 4 6 . 4 4 7 . 5 2 . 5 O v e r a l l Balance ‑58.8 ‑ 4 . 8 ‑52.6 ‑ 4 2 . 1 ‑34.4 — 1.8 Notes:

#annualized. # # SDO plus INPRES f o r FY2000.

###Additional DAU to Papua f o r i t s s p e c i a l autonomy.

Source: Ministry of Finance.

Fund ( D A K ) , a matching o r earmarked g r a n t , which aimed t o impose n a t i o n a l p r i o r i t i e s at~egional l e v e l a n d / o r f i n a n c i n g p r o j e c t s which have s p i l l over e f f e c t s a c r o s s r e g i o n s . F u r t h e r , t h e r e g i o n a l t a x and l e v y law was r e v i s e d t o s t r e n g t h e n regions'revenue m o b i l i z i n g c a p a c i t i e s .

A f t e r t h e d e c e n t r a l i z a t i o n , t h e t o t a l amount o f c e n t r a l t r a n s f e r s (DAU, revenue s h a r i n g , DAK, and o t h e r t r a n s f e r s ) was d r a s t i c a l l y i n c r e a s e d ( T a b l e 1 ) . The amounts f o r FY2001, FY2002, and FY2003 were R p . 8 1 . 7 t r i l l i o n , R p . 9 8 . 0 t r i l l i o n , and R p . 1 1 6 . 9 t r i l l i o n , o r 5 . 7 , 5 . 8 , and 6 . 0 p e r c e n t o f GDP, r e s p e c t i v e l y , much h i g h e r than t h e R p . 3 3 . 5 t r i l l i o n o r 3 . 7 p e r c e n t o f GDP f o r FY2000. DAU has t a k e n up about 70 p e r c e n t o f t o t a l t r a n s f e r s . R e g i o n a l budgets a l s o show t h a t DAU i s t h e most i m p o r t a n t revenue source f o r r e g i o n a l governments. I n FY2001, DAU a l l o c a t i o n accounted f o r 6 7 . 9 p e r ‑ c e n t o f t o t a l l o c a l government r e v e n u e s . Even a t t h e p r o v i n c i a l l e v e l , which a c q u i r e d h i g h e r revenue m o b i l i z a t i o n c a p a c i t y due t o t h e new r e g i o n a l t a x assignments, i t t a k e s up more than 20 p e r c e n t ( T a b l e 2 ) . A l l t h i s i n d i c a t e s t h a t DAU has become a mainstay o f t h e new i n t e r g o v e r n m e n t a l t r a n s f e r s i n d e c e n t r a l i z e d I n d o n e s i a .

T a b l e 2 R e g i o n a l Budgets

FY20QQ# FY2001

Provinces L o c a l Governments Provinces L o c a l Governments ( R p . b i l l . ) (%) ( R p . b i l l . ) (%) ( R p . b i l l . ) (%) ( R p . b i l l . ) (%) Revenues 1 2 , 9 8 4 1 0 0 . 0 39,654 1 0 0 . 0 29,396 1 0 0 . 0 79,459 1 0 0 . 0

Previous Year's Surplus 1 , 1 7 9 9 . 1 1 , 7 5 2 4 . 4 4 , 0 6 7 1 3 . 8 2 , 1 5 1 2 . 7 Region's Own Revenues 3,953 3 0 . 4 3,596 9 . 1 1 0 , 1 3 4 3 4 . 5 5,225 6 . 6 Balanced Funds 7,820 6 0 . 2 33,299 8 4 . 0 1 4 , 1 5 9 4 8 . 2 68,816 8 6 . 6 Tax Sharing 706 5 . 4 3,739 9 . 4 4 , 2 9 0 1 4 . 6 5,718 7 . 2 Non‑Tax Sharing 996 7 . 7 714 1 . 8 3,206 1 0 . 9 8,266 1 0 . 4

匹 絆 6,114 4 7 . 1 28,379 7 1 . 6 6 , 5 0 7 2 2 . 1 53,992 四

OAK### 3 0 . 0 467 1 . 2 156 0 . 5 839 1 . 1 L o c a l Borrowing 32 0 . 2 1 , 0 0 8 2 . 5 1 1 0 . 0 484 0 . 6 Others

゜ 0 . 0 ゜ 0 . 0 1 , 0 2 5 3 . 5 2,783 3 . 5

Expenditures 1 1 , 6 3 5 1 0 0 . 0 37,689 1 0 0 . 0 23,093 1 0 0 . 0 69,623 1 0 0 . 0 Routine Expenditure 5,934 5 1 . 0 25,147 6 6 . 7 1 4 , 6 9 9 6 3 . 7 48,255 6 9 . 3 Personnel Expenditure 2 , 0 4 2 1 7 . 6 1 8 , 5 2 1 4 9 . 1 5 , 7 6 3 2 5 . 0 35,289 5 0 . 7 Non‑Personnel Expenditure 3 , 8 9 2 3 3 . 4 6,626 1 7 . 6 8,936 3 8 . 7 12,966 1 8 . 6 Development Expenditure 5 , 7 0 1 4 9 . 0 1 2 , 5 4 3 3 3 . 3 8,394 3 6 . 3 21,368 3 0 . 7

Balances (% t o t o t a l revenues) 1 , 3 4 9 1 0 . 4 1 , 9 6 5 5 . 0 6 , 3 0 3 2 1 . 4 9,836 1 2 . 4 Notes: # annualized.

##SDO plus INPRES for FY2000. # # # S p e c i f i c purpose INPRES f o r FY2000.

Source: Ministry of Finance.

5

T h i s paper a n a l y z e s I n d o n e s i a ' s b l o c k g r a n t (DAU) a l l o c a t i o n methods i n t h e f i r s t t h r e e y e a r s a f t e r t h e d e c e n t r a l i z a t i o n . The DAU a l l o c a t i o n scheme has been undergoing almost annual r e v i s i o n s , and each o f t h e s e r e v i s i o n s has brought new problems i n i t s wake. I t i s very i m p o r t a n t t o review these p a s t e x p e r i e n c e s a t t h i s s t a g e i n o r d e r t o c l a r i f y major con‑

s t r a i n t s and t o e s t a b l i s h c l e a r p o l i c y d i r e c t i o n s f o r I n d o n e s i a p r o g r e s s . T h i s paper i s o r g a n i z e d a s f o l l o w s : S e c t i o n 2 r e v i e w s DAU a l l o c a t i o n methods i n t h e p a s t t h r e e y e a r s ; S e c t i o n 3 assesses t h e e q u a l i z a t i o n performance o f t h e c u r r e n t DAU a l l o c a t i o n method by conducting simple simulation e x e r ‑ c i s e s . The f i n a l s e c t i o n summarizes major c o n c l u s i o n s .

2 . DAU A l l o c a t i o n Methods: Review

The t o t a l DAU amount i n t h e c e n t r a l budget i s s e t a t a minimum 25 p e r c e n t o f t h e c e n t r a l government's domestic r e v e n u e s . T h i s amount i s shared between p r o v i n c i a l and l o c a l governments a t a r a t e o f 1 0 p e r c e n t and 90 p e r c e n t , r e s p e c t i v e l y . R e f l e c t i n g i t s d i f f i c u l t f i s c a l c o n d i t i o n , t h e Government has a l l o c a t e d t h e minimum, 25 p e r c e n t , o f i t s domestic revenues i n t h e p a s t t h r e e yea r s 包 I na d d i t i o n , t h e c e n t r a l budget c o n t a i n s o t h e r t r a n s f e r s t o t a k e i n t o a c c o u n t : 1 ) s p e c i a l autonomy f o r Papua p r o v i n c e ( t w o p e r c e n t o f t o t a l DAU s i n c e F Y 2 0 0 2 ) ; 2 ) h o l d harmless ( s i n c e F Y 2 0 0 2 ) , which i s d i s ‑ cussed i n t h e l a t e r p a r t o f t h i s p a p e r ; and 3 ) contingency (FY2001 and F Y 2 0 0 3 ) 4 .

DAU i s d e f i n e d a s an e q u a l i z a t i o n g r a n t t o r e g i o n s . However, i t i s v e r y i m p o r t a n t t o d e f i n e t h e concept o f " e q u a l i z a t i o n " b e f o r e a n a l y z i n g t h e e q u a l i z a t i o n e f f e c t o f DAU. Some d e f i n e i t a s e q u a l i z a t i o n o f per c a p i t a r e v ‑ e n u e s , w h i l e o t h e r s c o n s i d e r i t t o be an e q u a l i z a t i o n o f per c a p i t a t r a n s f e r s . There seems t o be c o n f u s i o n about t h e concept o f e q u a l i z a t i o n amongst p o l i c y makers and r e s e a r c h e r s . However, i t must be noted t h a t government r e g u l a t i o n No. 1 0 4 / 2 0 0 0 c l e a r l y s t i p u l a t e s t h a t t h e g e n e r a l a l l o c a t i o n fund s h a l l be a l l o c a t e d w i t h t h e purpose o f e q u a l i z i n g t h e f i n a n c i a l c a p a c i t y among r e g i o n s t o f i n a n c e spending r e q u i r e d t o implement d e c e n t r a l i z a t i o n scheme, which means t h a t a key o b j e c t i v e o f DAU i s t o e q u a l i z e f i s c a l

3 According t o t h e GTZ d e c e n t r a l i z a t i o n n e w s l e t t e r ( N o . 5 1 ) , t h e Government has agreed w i t h t h e p a r ‑ l i a m e n t ( D P R ) t o r a i s e t h e percentage o f DAU t o 26 p e r c e n t from FY2004.

4 I t i s t o be noted t h a t t h e s e funds a r e r e c o r d e d o u t s i d e t h e DAU budget and c a t e g o r i z e d a s s p e c i a l

autonomy and b a l a n c i n g funds i n t h e c e n t r a l b u d g e t .

c a p a c i t i e s a c r o s s r e g i o n s t o f i n a n c e t h e i r e x p e n d i t u r e n e e d s . To t h i s e n d , t h e Government has s e t o u t a " f i s c a l gap" formula f o r DAU a l l o c a t i o n . However, t h e Government h e s i t a t e d t o d i s t r i b u t e a l l DAU based on t h i s f o r ‑ mula, and i n s t e a d made some adjustments t o a c t u a l DAU a l l o c a t i o n s . DAU a l l o c a t i o n t o a r e g i o n a l government i i s based on t h r e e f a c t o r s :

DAUi = BFAi + FFAi + LSFAi

where BFA i s b a l a n c i n g f a c t o r a l l o c a t i o n , FFA i s formula f a c t o r a l l o c a t i o n , and LSFA i s lump‑sum f a c t o r a l l o c a t i o n ( T a b l e 3 ) .

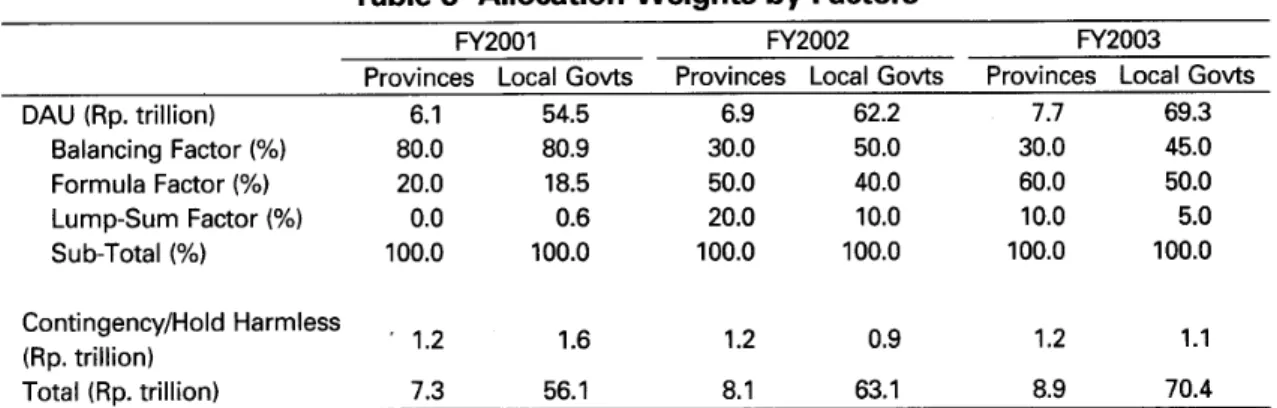

Table 3 A l l o c a t i o n Weights by F a c t o r s

FY2001 FY2002 FY2003 P r o v i n c e s L o c a l Govts P r o v i n c e s L o c a l Govts P r o v i n c e s L o c a l Govts DAU ( R p . t r i l l i o n ) 6 . 1 5 4 . 5 6 . 9 6 2 . 2 7 . 7 6 9 . 3

B a l a n c i n g F a c t o r (%) 8 0 . 0 8 0 . 9 3 0 . 0 5 0 . 0 3 0 . 0 4 5 . 0 Formula F a c t o r (%) 2 0 . 0 1 8 . 5 5 0 . 0 4 0 . 0 6 0 . 0 5 0 . 0 Lump‑Sum F a c t o r (%) 0 . 0 0 . 6 2 0 . 0 1 0 . 0 1 0 . 0 5 . 0 S u b ‑ T o t a l (%) 1 0 0 . 0 1 0 0 . 0 1 0 0 . 0 1 0 0 . 0 1 0 0 . 0 1 0 0 . 0 C o n t i n g e n c y / H o l d Harmless ・1.2 1 . 6 1 . 2 0 . 9 1 . 2 1 . 1 ( R p . t r i l l i o n )

T o t a l ( R p . t r i l l i o n ) 7 . 3 5 6 . 1 8 . 1 6 3 . 1 8 . 9 7 0 . 4 Source: M i n i s t r y o f F i n a n c e .

F u r t h e r , a d d i t i o n a l t r a n s f e r s have been d i s t r i b u t e d i n t h e p a s t t h r e e y e a r s . I n FY2001, t h e f i r s t year o f d e c e n t r a l i z a t i o n , t h e Government a l l o ‑ c a t e d a t o t a l o f R p . 2 . 8 t r i l l i o n ( R p . 1 . 2 t r i l l i o n t o p r o v i n c e s , and R p . 1 . 6 t r i l l i o n t o l o c a l governments) a s c o n t i n g e n c y funds t o accommodate a d d i t i o n a l s a l a r y c o s t s i n t h e r e g i o n s due t o t h e c e n t r a l l y ‑ i n i t i a t e d r e t r o a c t i v e s a l a r y i n c r e a s e . Since FY2002, t h e Government has prepared another f u n d , which i s i n c l u d e d i n s p e c i a l autonomy and b a l a n c i n g funds i n t h e c e n t r a l b u d g e t , f o r h o l d harmless a l l o c a t i o n , which we d i s c u s s i n t h e n e x t s e c t i o n . Ap‑

pendix t a b l e summarizes DAU a l l o c a t i o n procedures i n t h e p a s t t h r e e y e a r s .

2 . 1 . Formula F a c t o r A l l o c a t i o n :

The formula f a c t o r a l l o c a t i o n aims a t a l l o c a t i n g DAU based on t h e f i s c a l

gaps ( F G ) o f r e g i o n a l governments. T o t a l amounts o f DAU a l l o c a t e d t o t h i s

7

f a c t o r a r e d i s t r i b u t e d t o r e g i o n s a c c o r d i n g t o t h e i r r e l a t i v e f i s c a l g a p s . The f i s c a l gap i s d e f i n e d a s t h e d i f f e r e n c e between e x p e n d i t u r e needs ( E N ) and f i s c a l c a p a c i t y ( F C ) .

FG 戸 ENi‑FCi

Under t h i s d e f i n i t i o n , f i s c a l gaps i n some r e g i o n s , i n p a r t i c u l a r those t h a t have h i g h revenue c a p a c i t i e s , can be n e g a t i v e , which, i n t h e o r y , i m p l i e s n e g a t i v e DAU a l l o c a t i o n s t o such r e g i o n s . However, under t h e c u r r e n t s y s ‑ t e r n , a n e g a t i v e DAU a l l o c a t i o n i s n o t p e r m i t t e d , so t h e f i s c a l gaps f o r such

r e g i o n s a r e s e t a t z e r o .

E x p e n d i t u r e needs i n t h e FY2001 formula were d e f i n e d a s a product o f average r e g i o n a l government e x p e n d i t u r e and t h e f i s c a l needs i n d e x :

EN・‑‑ = ---~

0 ̲1 P ( + o p i A r e a , + P o v h e a d ; + C o s t ,

4 巧 /n 砂 叫 n 巧 h e a d , j n 砂 C o s t , / n )

where APBDEXPr i s t o t a l r e g i o n a l government e x p e n d i t u r e s ( p a s t a c t u a l d a t a was u t i l i z e d ) , Pop i s t h e p o p u l a t i o n , Area i s s u r f a c e a r e a , Povhead i s t h e head account p o v e r t y i n d e x ( p e r c e n t a g e o f people below t h e p o v e r t y l i n e ) , C o s t i s a c o s t i n d e x , n i s t h e number o f r e g i o n a l governments, T i n d i c a t e s t h e t o t a l o f t h e v a r i a b l e s .

A f a t a l weakness o f t h i s s p e c i f i c a t i o n i s i t s t r e a t m e n t o f average f i s c a l n e e d s . Under t h i s d e f i n i t i o n , t h e Government assumed t h a t aggregate f i s ‑ c a l need a f t e r d e c e n t r a l i z a t i o n was e q u a l t o a c t u a l r e g i o n a l governments' e x p e n d i t u r e s b e f o r e d e c e n t r a l i z a t i o n , s i n c e a c t u a l e x p e n d i t u r e d a t a b e f o r e d e c e n t r a l i z a t i o n was u t i l i z e d . We a l s o n o t e t h a t t h e Government gave each v a r i a b l e e q u a l weight ( 1 / 4 ) . However, t h e r e was no e m p i r i c a l assessment o f t h e v a l i d i t y o f t h i s as a measure o f r e g i o n s ' f i s c a l n e e d s , nor was i t p o s s i b l e f o r t h e Government t o judge t h e a p p r o p r i a t e n e s s o f t h i s assessment, s i n c e f i s c a l needs could n o t be e v a l u a t e d without c l e a r e x p e n d i t u r e assignments and t h e i r c o s t e s t i m a t i o n s .

Another problem l i e s i n t h e t r e a t m e n t o f t h e c o s t i n d e x . T h i s i s i n t e n d e d

t o measure r e g i o n a l d i f f e r e n c e s i n p u b l i c s e r v i c e d e l i v e r y c o s t s , which a r e

assumed t o be p o s i t i v e l y r e l a t e d t o e x p e n d i t u r e n e e d s . Because c o s t s d i f f e r

g r e a t l y between r e g i o n s , i t i s i m p o r t a n t t o i n c o r p o r a t e a measure o f t h i s

c o s t d e f e r e n t i a l . However, i n g e n e r a l , t h e c o s t i n d e x should be s t r u c t u r e d t o

a d j u s t t h e f i s c a l needs d i f f e r e n t i a l a f t e r c o n s i d e r i n g o t h e r f a c t o r s , i . e . , popu‑

l a t i o n , a r e a , and p o v e r t y . I n t h e above f o r m u l a , t h e c o s t index i n f l u e n c e s f i s c a l needs a f t e r i t s e f f e c t has been averaged w i t h o t h e r t h r e e o t h e r v a r i ‑ a b l e s .

F o r FY2002, t h e Government s l i g h t l y r e v i s e d t h e d e f i n i t i o n o f e x p e n d i ‑ t u r e needs and adopted d i f f e r e n t weights f o r t h e v a r i a b l e s . These changes were a l s o i n c o r p o r a t e d f o r FY2003. However, i t i s s t i l l d i f f i c u l t t o e v a l u a t e t h e impacts o f t h i s change on improving t h e measurement o f r e g i o n s ' t r u e f i s c a l needs without knowing t r u e e x p e n d i t u r e assignments and t h e i r c o s t i m p l i c a t i o n s . There i s no c o n v i n c i n g e x p l a n a t i o n by t h e Government f o r t h i s change.

A P B D E X P r ( P a p , A r e a ; P

E N i = • 0.4• + 0.1•

I +0.1•

o v g a p i

+04• C o s l i

n ' f P 1 J J 1 , j n p r e a . n

幻P a v g a p , j n ・ fC o s t ; / n )

The p o v e r t y index i s another i s s u e . I n t h e FY2002 f o r m u l a , t h e head account p o v e r t y index ( P o v 加 ad) o f t h e FY2001 f o r m u l a , was r e p l a c e d by t h e p o v e r t y gap index ( P o v g a p ) , which i s measured by t h e average p r o p o r ‑ t i o n a t e d i s t a n c e o f t h e poor from t h e p o v e r t y l i n e . The p o v e r t y gap index i n t e n d s t o c a p t u r e t h e depth o f p o v e r t y . However, i t i s n o t c l e a r which i n d e x i s a b e t t e r measure o f t h e f i s c a l needs o f r e g i o n a l governments f o r p o v e r t y a l l e v i a t i o n . F u r t h e r , we may need t o c o n s i d e r whether any p o v e r t y r e l a t e d i n d e x needs t o be i n c l u d e d i n t h e assessment o f e x p e n d i t u r e n e e d s . As mentioned, a c l e a r demarcation o f a u t h o r i t y between d i f f e r e n t l e v e l s o f government has n o t y e t been w e l l e s t a b l i s h e d i n I n d o n e s i a . I f primary r e s p o n s i b i l i t y f o r p o v e r t y a l l e v i a t i o n f a l l s on t h e c e n t r a l government, t h e r e i s no need f o r any p o v e r t y i n d e x t o be i n c l u d e d i n t h e f o r m u l a . These i s s u e s need t o be c a r e f u l l y reviewed f o r f u t u r e r e v i s i o n s .

F i s c a l c a p a c i t y i n FY2001 was d e f i n e d a s t h e average sum o f r e g i o n a l own revenues ( P A D ) , shared revenues from l a n d and b u i l d i n g t a x ( P B B ) and l a n d s and b u i l d i n g s t r a n s f e r t a x (BPHTB) times t h e f i s c a l c a p a c i t y i n d e x :

FC 戸 (PADr+ PBBr + BPH'I'Br)• ̲ l ̲ (NRO,IGRDP, NNRO,IGRDP, L F , ! P o p ,

n 3 NROr!GRDPr NNROr!GRDPr + + L F r ! P o p r )

where NRO i s n a t u r a l r e s o u r c e s e c t o r GDP, NNRO i s n o n ‑ n a t u r a l r e s o u r c e

︐

s e c t o r GDP, GRDP i s r e g i o n a l GDP, and LF i s working age p o p u l a t i o n . There a r e some c o n c e p t u a l problems w i t h t h i s f o r m u l a t i o n . F i r s t , i t i s n o t c l e a r why t h e Government d i d n o t i n c o r p o r a t e shared revenues from p e r s o n a l income t a x and n a t u r a l r e s o u r c e s . N e g l e c t i n g these revenues i m p l i e s t h a t t h e f i s c a l c a p a c i t i e s o f some r e g i o n s w i t h broad t a x bases a n d / o r abundant n a t u r a l r e s o u r c e s w i l l i n e v i t a b l y be u n d e r e s t i m a t e d , and w i l l t h e r e f o r e a t t r a c t l a r g e r DAU a l l o c a t i o n s . A p o s s i b l e e x p l a n a t i o n f o r t h i s may be t h a t t h e s e shared revenue d a t a were n o t a v a i l a b l e when the Government e s t a b l i s h e d t h e f o r m u l a . Second, t h e r e i s no s p e c i f i c reason to employ both n a t u r a l r e s o u r c e s e c t o r GDP and n o n ‑ n a t u r a l r e s o u r c e s e c t o r GDP i n t h e d e f i n i t i o n , s i n c e t h e sum o f t h e two v a r i a b l e s must be e q u a l to t h e t o t a l r e g i o n a l GDP. T h i r d , i t i s n o t c o n s i s t e n t t o use t h e working age p o p u l a t i o n a s a v a r i a b l e t o measure f i s c a l c a p a c i t y , s i n c e t h e l a b o r f o r c e can be regarded as a f a c t o r o f p r o d u c t i o n , i . e . , r e g i o n a l GDP, which has a l r e a d y been i n c o r p o r a t e d i n t o t h e d e f i n i t i o n .

I n FY2002, t h e f i s c a l c a p a c i t y d e f i n i t i o n was s i m p l i f i e d and much im‑

p r o v e d . F i s c a l c a p a c i t y i s t h e sum o f a r e g i o n ' s own and shared r e v e n u e s : FCi=P

ゆi + PBBi + BPHTBi + PPHi + 0.75• SDAi

where PAD i s a r e g i o n ' s p o t e n t i a l own r e v e n u e s , PPH i s shared p e r s o n a l income t a x r e v e n u e , and SDA i s shared n a t u r a l r e s o u r c e s r e v e n u e s .

S i n c e t h e r e g i o n ' s p o t e n t i a l own revenue i s measured as a f u n c t i o n of manufacturing and s e r v i c e s e c t o r GDP (GRDPMS), t h i s r e v i s i o n can p r o v i d e a t a x m o b i l i z i n g i n c e n t i v e t o r e g i o n a l governments. T h i s i s one o f t h e s i g ‑ n i f i c a n t improvements i n t h e FY2002 f o r m u l a .

P

ゆi = / 3 o + /31• GRDPMS け &

However, we n o t e t h a t , d e s p i t e t h e improvements, t h e FY2002 f i s c a l capac‑

i t y d e f i n i t i o n has another s e r i o u s problem. According t o t h i s d e f i n i t i o n , only

75 p e r c e n t o f shared revenues from n a t u r a l r e s o u r c e s can be i n c l u d e d i n

f i s c a l c a p a c i t y . C o n s i d e r i n g t h e s i g n i f i c a n t c o u n t e r ‑ e q u a l i z i n g e f f e c t o f n a t ‑

u r a l r e s o u r c e revenue s h a r i n g , a l l ( 1 0 0 p e r c e n t ) o f shared n a t u r a l r e s o u r c e

revenue should have been regarded as i n c r e a s i n g a r e g i o n ' s f i s c a l c a p a c i t y .

However, a lower 75 p e r c e n t weighting was i n t r o d u c e d a f t e r s t r o n g l o b b y ‑

i n g by some r e g i o n a l governments, i n p a r t i c u l a r some from r e s o u r c e r i c h

r e g i o n s .

As i n FY2002, t h e Government u t i l i z e d t h e r e g i o n ' s p o t e n t i a l own r e v ‑ enues ( P . 紅) as a component o f f i s c a l c a p a c i t y c a l c u l a t i o n f o r FY2003 DAU a l l o c a t i o n . However, only h a l f o f t h e p o t e n t i a l revenues were i n c o r p o r a t e d i n t o t h e a c t u a l c a l c u l a t i o n . As mentioned, t h e r e was no need t o c o n s i d e r any d i s i n c e n t i v e t o r e g i o n a l governments'tax m o b i l i z a t i o n e f f o r t s s i n c e , as a m a t t e r o f f a c t , t h e Government has u t i l i z e d e s t i m a t e d p o t e n t i a l revenues s i n c e FY2002. The Government might consider t h a t t h e simple r e g r e s s i o n method could n o t c a p t u r e r e g i o n a l governments'potential revenue c a p a c i ‑ t i e s a c c u r a t e l y . I f t h a t i s t h e c a s e , they would be w e l l a d v i s e d t o use a c t u a l r e g i o n a l own revenue d a t a , and some p o r t i o n , s a y , i n t h i s case 50 p e r c e n t , o f t h e a c t u a l r e g i o n a l own revenues as a component o f r e g i o n a l govern‑

m e n t s ' f i s c a l c a p a c i t y c a l c u l a t i o n .

FCi=0.5•P..

ゆi + PBBi + BPHTBi + PPHi + 0.75• SDAi

We n o t e t h a t , i n t h e p a s t t h r e e y e a r s , t h e f i s c a l gap formula has been a p p l i e d only t o t h e r e s i d u a l s o f DAU: t h e Government f i r s t determined a l l o ‑ c a t i o n amounts f o r b a l a n c i n g and lump‑sum f a c t o r a l l o c a t i o n s , which a r e d i s c u s s e d i n t h e f o l l o w i n g p a r t s , and t h e remaining amounts were d i s ‑ t r i b u t e d based on t h e f o r m u l a . I n FY2001, t h e s h a r e s o f formula f a c t o r a l l o ‑ c a t i o n s , both f o r p r o v i n c e s and l o c a l governments, made up only about 20 p e r c e n t o f t o t a l DAU a l l o c a t i o n amounts. Although h i g h e r shares o f DAU have been based on t h e formula i n FY2002 and FY2003, i t s shares remained a t 60 p e r c e n t ( p r o v i n c e s ) and 50 p e r c e n t ( l o c a l governments) even i n FY2003.

2 . 2 . B a l a n c i n g F a c t o r A l l o c a t i o n

I n FY2000, when t h e DAU a l l o c a t i o n method f o r FY2001 was discussed

w i t h i n t h e Government, t h e r e was s e r i o u s concern over p o s s i b l e m i s ‑

matches between expenditure r e s p o n s i b i l i t i e s and revenue assignments

i n r e g i o n a l b u d g e t s . Of p a r t i c u l a r r e l e v a n c e was one o f t h e most serous

c o n c e r n s , r e l a t i n g t o u n c e r t a i n t y about a d d i t i o n a l s a l a r y c o s t s due t o t h e

l a r g e ‑ s c a l e c e n t r a l s t a f f t r a n s f e r , which was t o be f i n a n c e d by t h e r e g i o n s

a f t e r d e c e n t r a l i z a t i o n . As mentioned, about two m i l l i o n c i v i l s e r v a n t s were

scheduled t o be t r a n s f e r r e d t o r e g i o n a l governments. However, a t t h i s

s t a g e , t h e Government d i d n o t have any r e l i a b l e d a t a r e g a r d i n g t h e s t a f f t o

1 1

be t r a n s f e r r e d t o each r e g i o n a l government. To address t h e i s s u e , t h e Government decided on one measure f o r l o c a l governments and another f o r p r o v i n c e s . For l o c a l governments, t h e Government f i r s t decided t o a l l o ‑ c a t e 30 p e r c e n t o f SDO and 1 0 p e r c e n t o f INPRES i n a d d i t i o n t o t h e a n n u a l ‑ i z e d t o t a l amount o f SDO and INPRES a l l o c a t e d i n FY2000 t o each l o c a l government. The Government assumed t h a t t h e a d d i t i o n a l s a l a r y c o s t s c o u l d be f i n a n c e d by t h e 30 p e r c e n t i n c r e a s e i n SDO and t h e 1 0 p e r c e n t i n c r e a s e i n INPRES. The t o t a l amount o f t h e b a l a n c i n g f a c t o r a l l o c a t i o n made up as much as 80 p e r c e n t o f t h e t o t a l DAU a v a i l a b l e t o l o c a l govern‑

ments (DAU 叫 i nFY2001.

BFA戸 1.3•

SDOi + 1.1• INPRES1

T h i s measure c o u l d n o t be a p p l i e d t o p r o v i n c i a l governments s i n c e t h e t o t a l amounts o f SDO and INPRES r e c e i v e d by p r o v i n c e s i n FY2000 were g r e a t e r than t h e t o t a l DAU a v a i l a b l e t o p r o v i n c e s ( 1 0 p e r c e n t o f t o t a l DAU) i n FY2001. The Government u t i l i z e d t h e t o t a l amounts o f SDO and INPRES, without t h e a d d i t i o n a l 30 p e r c e n t o f SDO and 1 0 p e r c e n t o f INPRES, t o determine t h e b a l a n c i n g f a c t o r amounts t o p r o v i n c e s . F o l l o w i n g t h e a l l o c a ‑ t i o n t o l o c a l governments ( a b o u t 80 p e r c e n t f o r t h e b a l a n c i n g f a c t o r a l l o c a ‑ t i o n ) , 80 p e r c e n t o f DAU a v a i l a b l e t o p r o v i n c e s (DAUTP) was d i s t r i b u t e d as t h e b a l a n c i n g f a c t o r a l l o c a t i o n :

BFA,=( SDO, + INPRES,)

i ( S D O i + INPRESi) •0.8•DAU TP

1、

I n FY2002, t h e Government adopted wage b i l l f o r c i v i l s e r v a n t s , i n p l a c e o f SDO and INPRES, t o i n c o r p o r a t e s a l a r y c o s t s o f r e g i o n a l governments e x p l i c i t l y , and a l l o c a t e d 30 p e r c e n t ( p r o v i n c e s ) and 50 p e r c e n t ( l o c a l gov‑

ernments) o f t h e t o t a l DAU amounts as t h e b a l a n c i n g f a c t o r a l l o c a t i o n s . The b a l a n c i n g f a c t o r a l l o c a t i o n s covered about 77 p e r c e n t and 3 1 p e r c e n t o f t o t a l s a l a r y c o s t s o f p r o v i n c e s and l o c a l governments, r e s p e c t i v e l y . I n FY2003, w h i l e i t s share was s l i g h t l y reduced t o 45 p e r c e n t f o r l o c a l govern‑

ments, t h e same share ( 3 0 p e r c e n t ) was d i s t r i b u t e d a s t h i s f a c t o r f o r p r o v i n c e s . However, a s we a n a l y z e i n t h e n e x t s e c t i o n , b a l a n c i n g f a c t o r a l l o c a t i o n s have s i g n i f i c a n t l y undermined t h e e q u a l i z i n g e f f e c t o f DAU.

F u r t h e r , we n o t e t h a t t h e wage and s a l a r y ‑ b a s e d b a l a n c i n g f a c t o r a l l o c a ‑

t i o n s s i n c e FY2002 may encourage one p a r t i c u l a r moral h a z a r d . I n o r d e r t o s u c c e s s f u l l y i n t e g r a t e t h e l a r g e numbers o f f o r m e r l y c e n t r a l i z e d c i v i l s e r ‑ v a n t s , i t i s e s s e n t i a l t h a t r e g i o n a l governments s t r i v e t o implement e f f i c i e n t management and r e s t r u c t u r i n g . One d i s i n c e n t i v e t o t h i s p r o c e s s may be t h e f a c t t h a t l a r g e r p e r s o n n e l expenses without any e f f o r t towards g r e a t e r e f f i c i e n c y w i l l a t t r a c t h i g h e r DAU a l l o c a t i o n s t o such r e g i o n s .

2 . 3 . Lump‑Sum F a c t o r A l l o c a t i o n

I n FY2001, a f t e r t h e Government c a l c u l a t e d t h e DAU a l l o c a t i o n t o each r e g i o n based on t h e d r a f t c e n t r a l b u d g e t , t h a t budget was r e v i s e d f o l l o w i n g p a r l i a m e n t a r y d e b a t e . The lump‑sum f a c t o r a l l o c a t i o n was i n t r o d u c e d t o e q u a l i z e d i s t r i b u t i o n o f t h e i n c r e a s e d amount o f DAU f o l l o w i n g t h e r e v i ‑ s 1 o n .

However, i n FY2002, t h e Government r e t a i n e d t h e lump‑sum a l l o c a ‑ t i o n s b o t h f o r p r o v i n c e s and l o c a l governments: 20 percent o f DAUTP ( p r o v i n c e s ) and 1 0 p e r c e n t o f DAUTL ( l o c a l governments) were d i s t r i b u t e d e q u a l l y . I t was n o t c l e a r why t h e Government r e t a i n e d t h i s component f o r FY2002, s i n c e t h e lump‑sum f a c t o r was i n t r o d u c e d j u s t t o r e a l l o c a t e t h e i n c r e a s e d amount o f DAU due t o t h e budget r e v i s i o n i n FY2001. I t i s c l e a r l y e v i d e n t t h a t t h e lump‑sum a l l o c a t i o n s could s e r v e a s an i n c e n t i v e t o c r e a t e new l o c a l governments, and i n f a c t , 1 2 new l o c a l governments were e s t a b ‑ l i s h e d i n FY2001 and 22 i n FY2002. To address t h i s c r i t i c i s m , t h e FY2003 DAU a l l o c a t i o n p r o p o s a l prepared by t h e u n i v e r s i t y c o n s o r t i u m , recom‑

mends the a b o l i t i o n o f t h i s component. However, t h e Government u l t i ‑ mately decided t o r e t a i n i t , although i t s a l l o c a t i o n s h a r e s were dropped t o 1 0 p e r c e n t ( p r o v i n c e s ) and 5 p e r c e n t ( l o c a l governments).

2 . 4 . Hold Harmless A l l o c a t i o n : P o l i t i c a l I n t e r v e n t i o n

I n FY2001, when the Government submitted the FY2002 DAU a l l o c a t i o n p r o p o s a l , t h e p a r l i a m e n t r e q u e s t e d a r e v i s i o n o f DAU a l l o c a t i o n t o guaran‑

t e e t h a t no r e g i o n a l government could r e c e i v e l e s s DAU than i n FY2001.

A f t e r s t r o n g p o l i t i c a l p r e s s u r e , t h e Government r e v i s e d t h e a l l o c a t i o n by

r e a l l o c a t i n g a p a r t o f DAU from s u r p l u s r e g i o n s , where proposed amounts

f o r FY2002 were l a r g e r than FY2001 a l l o c a t i o n s , t o d e f i c i t r e g i o n s , and by

a l l o c a t i n g an a d d i t i o n a l R p . 2 . 1 t r i l l i o n from i t s budget t o accommodate the

p a r l i a m e n t ' s r e q u e s t . T h i s i s t h e o r i g i n o f t h e s o ‑ c a l l e d hold harmless a l l o ‑

c a t i o n .

13

We n o t e t h a t t h e h o l d harmless component was very d i f f e r e n t from t h e b a l a n c i n g f a c t o r a l l o c a t i o n d e s c r i b e d i n t h e e a r l i e r p a r t o f t h i s p a p e r . I t r e f l e c t s s t r o n g l o b b y i n g a c t i v i t i e s by some r e s o u r c e r i c h r e g i o n s who might have l o s t o u t under t h e o r i g i n a l p r o p o s a l . Some b e l i e v e d t h a t t h e h o l d harmless component c o u l d be j u s t i f i e d by government r e g u l a t i o n N o . 1 0 4 / 2 0 0 0 , which s t a t e s t h a t " t h e p r o p o s a l o f t h e R e g i o n a l Autonomy Advisory C o u n c i l (DPOD) s h a l l t a k e t h e b a l a n c i n g f a c t o r i n t o a c c o u n t " .

However, i n p r i n c i p l e , t h i s r e g u l a t i o n was prepared t o make i t p o s s i b l e f o r t h e Government t o a l l o c a t e a p a r t o f DAU on non‑formula b a s i s t o a v o i d p o s s i b l e mismatches between e x p e n d i t u r e r e s p o n s i b i l i t i e s and revenue assignments i n r e g i o n s . As d i s c u s s e d , on t h i s p r i n c i p l e , a p a r t o f DAU was a l l o c a t e d a s t h e b a l a n c i n g f a c t o r a l l o c a t i o n s i n FY2001 (based on p a s t SDO and INPRES) and FY2002 ( b a s e d on c i v i l s e r v a n t s a l a r i e s ) . I n FY2003, t h e h o l d harmless component was r e t a i n e d . A f t e r r e a l l o c a t i n g a p a r t o f DAU from s u r p l u s l o c a l governments ( R p . 1 . 2 t r i l l i o n ) t o d e f i c i t r e g i o n s , an a d d i ‑ t i o n a l R p . 1 . 1 t r i l l i o n was d i s t r i b u t e d from t h e c e n t r a l b u d g e t . For p r o v i n c e s , an a d d i t i o n a l R p . 1 . 2 t r i l l i o n was f i n a n c e d by t h e c e n t r a l budget without any r e a l l o c a t i o n among p r o v i n c e s .

3 . E q u a l i z a t i o n Performance: Simulation E x e r c i s e s

T h i s s e c t i o n a n a l y z e s t h e e q u a l i z a t i o n performance o f t h e c u r r e n t ( F Y 2 0 0 3 ) DAU a l l o c a t i o n method. The e q u a l i z a t i o n e f f e c t o f DAU can be assessed by comparing f i s c a l i n d i c a t o r s among r e g i o n a l governments b e f o r e and a f t e r DAU a l l o c a t i o n . However, two i s s u e s need t o be c l a r i f i e d b e f o r e our a n a l y ‑ s i s . F i r s t , we have t o s e l e c t t h e most a p p r o p r i a t e f i s c a l i n d i c a t o r f o r a s ‑ s e s s i n g t h e e q u a l i z a t i o n performance o f DAU. T h i s means t h a t we need t o e s t a b l i s h a c l e a r concept o f " e q u a l i z a t i o n " . There a r e v a r i o u s concepts o f e q u a l i z a t i o n such as p e r c a p i t a revenues and p e r c a p i t a t r a n s f e r s e t c . , and our c o n c l u s i o n depends on t h e d e f i n i t i o n we employ f o r our a n a l y s i s . There a r e some r e s e a r c h e s on t h e e q u a l i z a t i o n performance o f DAU.

R e f l e c t i n g t h e l a c k o f a common understanding o f t h e concept o f e q u a l i z a ‑ t i o n , some use p e r c a p i t a r e v e n u e s , w h i l e o t h e r s use d i f f e r e n t i n d i c a t o r s as a t a r g e t i n d i c a t o r t o measure e q u a l i z a t i o n p e r f o r m a n c e . Even among p o l i c y makers, i t seems t h a t t h e r e i s no c l e a r consensus on t h e concept o f e q u a l ‑ i z a t i o n . However, as we have mentioned, I n d o n e s i a ' s laws and r e g u l a t i o n s c l e a r l y d e f i n e t h a t a key o b j e c t i v e o f DAU a l l o c a t i o n i s t o e q u a l i z e t h e f i s c a l

‑‑-~

c a p a c i t i e s o f r e g i o n a l governments t o f i n a n c e t h e i r e x p e n d i t u r e n e e d s . T h i s i m p l i e s t h e e q u a l i z a t i o n o f n e i t h e r per c a p i t a revenues nor per c a p i t a t r a n s ‑ f e r s , b u t t h e e q u a l i z a t i o n o f f i s c a l c a p a c i t i e s t o f i s c a l n e e d s . We t h e r e f o r e need t o e v a l u a t e i t s e q u a l i z a t i o n performance by a n a l y z i n g how w e l l r e ‑ g i o n a l governments'fiscal c a p a c i t i e s can f u l f i l l t h e i r e x p e n d i t u r e needs a f t e r a l l o c a t i o n o f DAU.

N e x t , we need t o e s t a b l i s h proper measures o f f i s c a l needs and f i s c a l c a p a c i t y . However, as discussed i n t h e preceding s e c t i o n , v a r i o u s weak‑

nesses a r e found both i n t h e f i s c a l c a p a c i t y and e x p e n d i t u r e needs d e f i n i ‑ t i o n s u t i l i z e d i n t h e c u r r e n t f o r m u l a . I n t h i s a n a l y s i s , we d e f i n e a r e g i o n a l government f i s c a l c a p a c i t y (FC

りa s :

FCi*=P

切i + PBBi + BPHTB け PPHi + SDAi + DAUi

T h i s s p e c i f i c a t i o n means t h a t 100 p e r c e n t o f t h e p o t e n t i a l r e g i o n ' s own r e v ‑ enues ( P A f ) ) and shared revenues from n a t u r a l r e s o u r c e s e c t o r s ( S D A ) a r e t a k e n i n t o account as components o f r e g i o n s ' f i s c a l c a p a c i t i e s . We n o t e t h a t , i n t h e c u r r e n t DAU a l l o c a t i o n f o r m u l a , o n l y 50 p e r c e n t and 75 p e r c e n t o f b o t h revenues a r e i n c o r p o r a t e d i n t o t h e f i s c a l c a p a c i t y c a l c u l a t i o n s . E x p e n d i t u r e needs assessment i s much more p r o b l e m a t i c . As mentioned, t h e r e a r e some s e r i o u s f l a w s i n t h e c u r r e n t e x p e n d i t u r e needs f o r m u l a t i o n . We recommend s t r o n g l y t h a t t h e Government s e t up a more a p p r o p r i a t e e x p e n d i t u r e needs i n d i c a t o r . However, i n t h e c u r r e n t s i t u a t i o n , no i n d i c a t o r can c a p t u r e t h e t r u e e x p e n d i t u r e needs o f r e g i o n a l governments, s i n c e t h e r e i s no c l e a r demarcation o f a u t h o r i t y between t h e d i f f e r e n t l e v e l s o f government. For t h a t m a t t e r , c o s t e s t i m a t i o n s o f t h e new expenditure r e s p o n s i b i l i t i e s a r e o n l y p o s s i b l e a f t e r d e c e n t r a l i z a t i o n . We thus use t h e c u r r e n t e x p e n d i t u r e needs f o r m u l a t i o n developed by the Government, b e a r i n g i n mind i t s s h o r t c o m i n g s .

To a n a l y z e t h e e q u a l i z a t i o n performance o f t h e c u r r e n t DAU a l l o c a t i o n

method, we f i r s t c a l c u l a t e t h e r a t i o o f e x p e n d i t u r e needs t o cumulative

r e g i o n a l government's revenue f o r a l l p r o v i n c e s and l o c a l governments

( T a b l e 4 ) . The cumulative r e g i o n a l government's revenue i s d e f i n e d as

cumulative r e v e n u e s , which begins with the r e g i o n ' s p o t e n t i a l own r e v ‑

enues ( P . 紅) and adds shared revenues from personal income tax (PPH),

l a n d a n d b u i l d i n g t a x ( P B B ) , l a n d and b u i l d i n g t r a n s f e r t a x (BPHTB), and

n a t u r a l r e s o u r c e s ( S D A ) , and DAU. Changes i n t h e c o e f f i c i e n t o f v a r i a t i o n

1 5

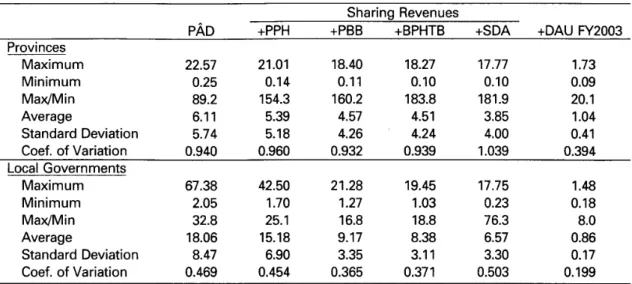

Table 4 V a r i a t i o n s o f Expenditure Needs ( E N ) to Cumulative Revenue R a t i o s

Sharing Revenues

PAD +PPH +PBB +BPHTB +SDA +DAU FY2003 Provinces

Maximum 2 2 . 5 7 2 1 . 0 1 1 8 . 4 0 1 8 . 2 7 1 7 . 7 7 1 . 7 3 Minimum 0 . 2 5 0 . 1 4 0 . 1 1 0 . 1 0 0 . 1 0 0 . 0 9 Max/Min 8 9 . 2 1 5 4 . 3 1 6 0 . 2 1 8 3 . 8 1 8 1 . 9 2 0 . 1 Average 6 . 1 1 5 . 3 9 4 . 5 7 4 . 5 1 3 . 8 5 1 . 0 4 Standard D e v i a t i o n 5 . 7 4 5 . 1 8 4 . 2 6 4 . 2 4 4 . 0 0 0 . 4 1 C o e f . o f V a r i a t i o n 0 . 9 4 0 0 . 9 6 0 0 . 9 3 2 0 . 9 3 9 1 . 0 3 9 0 . 3 9 4 L o c a l Governments

Maximum 6 7 . 3 8 4 2 . 5 0 2 1 . 2 8 1 9 . 4 5 1 7 . 7 5 1 . 4 8 Minimum 2 . 0 5 1 . 7 0 1 . 2 7 1 . 0 3 0 . 2 3 0 . 1 8 Max/Min 3 2 . 8 2 5 . 1 1 6 . 8 1 8 . 8 7 6 . 3 8 . 0 Average 1 8 . 0 6 1 5 . 1 8 9 . 1 7 8 . 3 8 6 . 5 7 0 . 8 6 Standard D e v i a t i o n 8 . 4 7 6 . 9 0 3 . 3 5 3 . 1 1 3 . 3 0 0 . 1 7 C o e f . o f V a r i a t i o n 0 . 4 6 9 0 . 4 5 4 0 . 3 6 5 0 . 3 7 1 0 . 5 0 3 0 . 1 9 9

show t h e e q u a l i z a t i o n e f f e c t o f newly added t r a n s f e r s . The r e s u l t s i n d i c a t e t h a t t h e DAU a l l o c a t i o n s have a s i g n i f i c a n t e q u a l i z i n g e f f e c t : a f t e r t h e DAU a l l o c a t i o n s , c o e f f i c i e n t s o f v a r i a t i o n o f both p r o v i n c e s and l o c a l govern‑

ments drop s i g n i f i c a n t l y from t h e i r l e v e l s b e f o r e t h e DAU a l l o c a t i o n s have been made.

However, i f we check t h e r a t i o o f e x p e n d i t u r e needs t o f i s c a l c a p a c i t i e s (FC , whichcorrespond t り o t h e r a t i o a f t e r DAU a l l o c a t i o n s , t h e r e s t i l l remain very l a r g e d i f f e r e n c e s i n t h e r a t i o b o t h w i t h i n p r o v i n c e s and l o c a l govern‑

F i g u r e 1 Histogram o f Expenditure Needs ( E N ) t o F i s c a l C a p a c i t y ( F C * ) R a t i o s : FV2003 DAU A l l o c a t i o n s

8 Provinces

6•--- 5•--- 4

い‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑3

い‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑‑゜

T o t a l Samples=30

0 . 2 0 . 4 0 . 6 0 . 8 1 1 . 2 1 . 4 1 . 6 1 . 8 EN/FC*

200 L o c a l Governments T o t a l

Samples=348

150 L ‑ ‑ ‑ ‑ ‑ ‑ ‑ ‑ ‑ ・ ・ ・ ‑ ‑ ‑ ‑ ‑ ‑ ‑ ‑ ・ ・ ・ ・ ・ ・ ・ —·

—··--···--··· 一 ● 一 ● ● 一100

>---―ー一•---50•---

゜

0 . 2 0 . 4 0 . 6 0 . 8 1 1 . 2 1 . 4 1 . 6 1 . 8

EN/FC*

ments. F o r p r o v i n c e s , t h e h i g h e s t r a t i o i s about 20 times l a r g e r than t h e l o w e s t , and f o r l o c a l governments, t h e h i g h e s t i s e i g h t times l a r g e r than t h e l o w e s t . F u r t h e r , t h e r e s u l t s show t h a t some r e g i o n s can n o t f i n a n c e t h e i r e x p e n d i t u r e needs even a f t e r t h e DAU a l l o c a t i o n s a r e made, w h i l e o t h e r r e g i o n s enjoy more than enough revenues t o f i n a n c e t h e i r e x p e n d i ‑ t u r e n e e d s . F i g u r e 1 shows t h e histogram o f e x p e n d i t u r e needs t o f i s c a l c a p a c i t y r a t i o s . I t i n d i c a t e s t h a t i n 60 p e r c e n t o f p r o v i n c e s ( 1 8 out o f a t o t a l 30 p r o v i n c e s ) and 1 7 p e r c e n t o f l o c a l governments ( 5 9 out o f a t o t a l 348 l o c a l governments), t h e i r revenue c a p a c i t i e s a r e l e s s than t h e i r e x p e n d i t u r e n e e d s . T h i s i m p l i e s t h a t f u r t h e r assessment o f t h e c u r r e n t DAU a l l o c a t i o n method i s r e q u i r e d t o improve t h e e q u a l i z a t i o n performance o f DAU.

To c l a r i f y t h e weaknesses o f t h e c u r r e n t DAU a l l o c a t i o n method, we conduct simple s i m u l a t i o n e x e r c i s e s 互 We summarize t h e assumptions employed i n Table 5 . The DAU a l l o c a t i o n f o r FY2003 i s s e t as t h e b a s e l i n e . I n t h e f i r s t case ( C a s e 1 ) , t h e h o l d harmless a l l o c a t i o n i s dropped, which means t h a t DAU i s d i s t r i b u t e d a c c o r d i n g t o t h r e e f a c t o r s , namely lump‑

sum f a c t o r , b a l a n c i n g f a c t o r , and formula f a c t o r . The s i m u l a t i o n r e s u l t o f t h i s s c e n a r i o and a comparison w i t h t h e b a s e l i n e case enables us t o e v a l u ‑ a t e t h e impact o f t h e h o l d harmless a l l o c a t i o n on t h e e q u a l i z a t i o n p e r f o r ‑ mance o f DAU. I n Case 2 , we f u r t h e r drop t h e lump‑sum a l l o c a t i o n and assume t h a t t h e amount f o r m e r l y a l l o c a t e d as lump‑sum a l l o c a t i o n i s d i s ‑ t r i b u t e d a c c o r d i n g t o t h e formula f a c t o r . F i n a l l y , i n Case 3 , we drop t h e b a l ‑ a n c i n g f a c t o r a l l o c a t i o n and assume t h a t a l l DAU i s a l l o c a t e d based on t h e f o r m u l a .

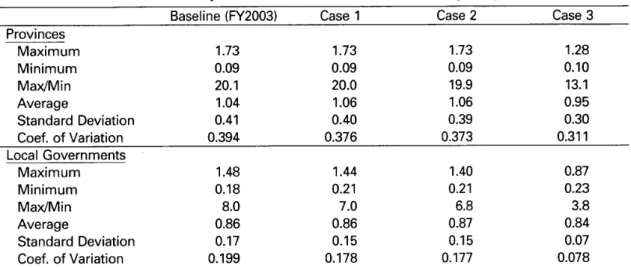

The r e s u l t s c o n f i r m t h a t t h e h o l d h a r m l e s s , lump‑sum, and b a l a n c i n g f a c t o r a l l o c a t i o n s have undermined t h e e q u a l i z a t i o n e f f e c t o f DAU b o t h f o r p r o v i n c e s and l o c a l governments. I n p a r t i c u l a r , t h e u n e q u a l i z i n g e f f e c t o f t h e b a l a n c i n g f a c t o r a l l o c a t i o n i s much more s i g n i f i c a n t than t h a t o f t h e o t h e r two f a c t o r s . Without t h e s e a l l o c a t i o n s , which means a 100 p e r c e n t formula based a l l o c a t i o n , r e g i o n a l f i s c a l c a p a c i t i e s t o f i n a n c e e x p e n d i t u r e needs can be e q u a l i z e d t o a much g r e a t e r e x t e n t ( T a b l e 6 ) . Thus, t h e r e i s s t i l l a l o n g way t o go b e f o r e t h e expected e q u a l i z a t i o n e f f e c t o f DAU i s r e a l ‑ i z e d .

With t h e s o l e l y formula based a l l o c a t i o n , t h e f i s c a l c a p a c i t i e s o f a l l l o c a l

5 A l l d a t a u t i l i z e d i n t h e s i m u l a t i o n e x e r c i s e s a r e a v a i l a b l e from t h e website o f D i r e c t o r a t e G e n e r a l o f

C e n t r a l and L o c a l F i s c a l B a l a n c e , M i n i s t r y o f F i n a n c e ( w w w . d j p k p d . g o . i d ) .

Table 5 Assumptions for Simulation Exercises B a s e l i n e ( F Y 2 0 0 3 )

P r o v . L o c a l G o v t . B a l a n c i n g Factor(%) 3 0 . 0 4 5 . 0 Formula F a c t o r ( % ) 6 0 . 0 5 0 . 0 Lump‑Sum Factor(%) 1 0 . 0 5 . 0 Hold Harmless yes yes

Case 1 P r o v . L o c a l G o v t .

3 0 . 0 4 5 . 0 6 0 . 0 5 0 . 0 1 0 . 0 5 . 0 no no

Case 2 P r o v . L o c a l G o v t .

3 0 . 0 4 5 . 0 7 0 . 0 5 5 . 0 0 . 0 0 . 0 no no

1 7

Case 3 P r o v . L o c a l G o v t .

0 . 0 0 . 0 1 0 0 . 0 1 0 0 . 0 0 . 0 0 . 0 no no

Table 6 Variations of Expenditure Needs (EN) to F i s c a l Capacity (FC*) Ratios B a s e l i n e ( F Y 2 0 0 3 ) Case 1 Case 2 Case 3 P r o v i n c e s

Maximum 1 . 7 3 1 . 7 3 1 . 7 3 1 . 2 8 Minimum 0 . 0 9 0 . 0 9 0 . 0 9 0 . 1 0 Max/Min 2 0 . 1 2 0 . 0 1 9 . 9 1 3 . 1 Average 1 . 0 4 1 . 0 6 1 . 0 6 0 . 9 5 Standard D e v i a t i o n 0 . 4 1 0 . 4 0 0 . 3 9 0 . 3 0 C o e f . o f V a r i a t i o n 0 . 3 9 4 0 . 3 7 6 0 . 3 7 3 0 . 3 1 1 L o c a l Governments

Maximum 1 . 4 8 1 . 4 4 1 . 4 0 0 . 8 7 Minimum 0 . 1 8 0 . 2 1 0 . 2 1 0 . 2 3 Max/Min 8 . 0 7 . 0 6 . 8 3 . 8 Average 0 . 8 6 0 . 8 6 0 . 8 7 0 . 8 4 Standard D e v i a t i o n 0 . 1 7 0 . 1 5 0 . 1 5 0 . 0 7 C o e f . o f V a r i a t i o n 0 . 1 9 9 0 . 1 7 8 0 . 1 7 7 0 . 0 7 8

governments become greater than their expenditure needs. In contrast, in case of 18 provinces whose fiscal capacities are less than their expenditure needs under the current DAU allocation method, their expenditure needs to fiscal capacity ratios s t i l l remain less than one, even with the solely formula based allocation (Table 7 ) 6 . O n average, the ratios for provinces are higher

6 I n FY2001, p r o v i n c i a l governments c a r r i e d over more than R p . 6 t r i l l i o n i n s a v i n g s t o t h e n e x t f i s c a l year ( T a b l e 2 ) , which may imply t h a t p r o v i n c e s enjoyed more t h a n enough f i n a n c i a l r e s o u r c e s t o meet t h e i r e x p e n d i t u r e n e e d s . However, t h e r e a r e some i s s u e s we have t o c o n s i d e r b e f o r e a c c e p t ‑ i n g t h i s c o n c l u s i o n . F i r s t , t h e delayed disbursement o f shared revenues needs t o be acknowledged.

Shared r e v e n u e s , i n p a r t i c u l a r those from n a t u r a l r e s o u r c e s , were d i s b u r s e d t o r e g i o n s a t a very

l a t e s t a g e o f t h e f i s c a l y e a r . A c c o r d i n g l y , a m a j o r i t y o f r e g i o n s c a r r i e d over a major p a r t o f t h e d i s ‑

t r i b u t e d revenues i n t o t h e n e x t y e a r . A second f a c t o r i s t h e l o n g ‑ c o n t i n u i n g t r a d i t i o n o f l a t e budget

a p p r o v a l by l o c a l p a r l i a m e n t s , which slows down projects'bi~ding p r o c e s s e s , r e s u l t i n g i n l e s s time

t o f i n a l i z e them. Even b e f o r e d e c e n t r a l i z a t i o n , I n d o n e s i a ' s r e g i o n a l governments had been running

s u r p l u s e s o f f i v e t o 15 p e r c e n t ( o f t o t a l r e v e n u e s ) every y e a r . F u r t h e r , t h e FY2001 d e c e n t r a l i z a t i o n

added another f a c t o r c o n t r i b u t i n g t o t h e slow disbursement o f r e g i o n a l e x p e n d i t u r e s : an i n c e s s a n t

war between r e g i o n a l o f f i c i a l s ( e x e c u t i v e s ) and l e g i s l a t o r s . T h i s problem a r i s e s from an i m p e r f e c t

d e f i n i t i o n o f d e c i s i o n making power w i t h i n r e g i o n a l governments. F o r d e t a i l s , see U s u i and Armida

A l i s j a h b a n a ( 2 0 0 3 ) .

than those f o r l o c a l governments. T h i s i m p l i e s t h a t , a t l e a s t i n t h e a g g r e ‑ g a t e , l o c a l governments r e c e i v e more adequate DAU a l l o c a t i o n than p r o v i n c e s . Table 8 shows aggregate f i s c a l n e e d s , f i s c a l c a p a c i t i e s , f i s c a l g a p s , and DAU a l l o c a t i o n s both f o r p r o v i n c e s and l o c a l governments, c l e a r l y showing t h a t t o t a l DAU a v a i l a b l e t o p r o v i n c e s i s l e s s than t h e i r t o t a l f i s c a l g a p s , w h i l e l o c a l governments enjoy more than enough DAU a l l o c a ‑ t i o n s t o make up t h e i r f i s c a l g a p s . F u r t h e r , t h e t a b l e suggests t h a t t o t a l p o o l o f DAU i s more than enough a t aggregate l e v e l t o f u l f i l l t o t a l f i s c a l gaps both o f p r o v i n c e s and l o c a l governments. As mentioned, under the c u r r e n t a l l o c a t i o n system, p r o v i n c e s and l o c a l governments s p l i t t h e t o t a l DAU budget 10 percent and 90 p e r c e n t , r e s p e c t i v e l y . Our r e s u l t s suggest t h a t a more a p p r o p r i a t e s h a r i n g arrangement i s r e q u i r e d , a t l e a s t i f t h e Government a p p l i e s t h e c u r r e n t e x p e n d i t u r e needs f o r m u l a t i o n t o both p r o v i n c e s and l o c a l governments.

T a b l e 7 D i s t r i b u t i o n o f E x p e n d i t u r e Needs ( E N ) t o F i s c a l C a p a c i t y ( F C * ) R a t i o s

B a s e l i n e ( F Y 2 0 0 3 ) Case 1 Case 2 Case 3 ( N o . ) (%) ( N o . ) (%) ( N o . ) (%) ( N o . ) ( % ) Provinces

EN/FC*> 1 18 6 0 . 0 18 6 0 . 0 18 6 0 . 0 18 6 0 . 0 EN/FC*< 1 12 4 0 . 0 12 4 0 . 0 12 4 0 . 0 12 4 0 . 0 T o t a l 30 1 0 0 . 0 30 1 0 0 . 0 30 1 0 0 . 0 30 1 0 0 . 0 L o c a l Governments

EN/FC*> 1 59 1 7 . 0 55 1 5 . 8 57 1 6 . 4

゜ 0 . 0

EN/FC*< 1 289 8 3 . 0 293 8 4 . 2 291 8 3 . 6 348 1 0 0 . 0 T o t a l 348 1 0 0 . 0 348 1 0 0 . 0 348 1 0 0 . 0 348 1 0 0 . 0

T a b l e 8 A g g r e g a t e F i s c a l Gaps and DAU A l l o c a t i o n s f o r FV2003 ( R p . b i l l i o n ) Expenditure F i s c a l

F i s c a l Gaps

##DAU FY2003 DAU/

Needs C a p a c i t i e s

#F i s c a l Gaps Provinces 1 7 , 3 9 2 1 2 , 6 9 1 1 0 , 2 5 9 8 , 8 5 1 0 . 8 6 3 L o c a l Governments 74,093 1 5 , 5 4 1 60,064 70,389 1 . 1 7 2 T o t a l 91,484 28,233 70,324 79,240 1 . 1 2 7 N o t e s :

#The Government's d e f i n i t i o n , not F C * .

##