Kagawa University Economic Review Vol. 76, No. 3, December 2003, 187‑212

Transaction‑Based Land Price Indices for Commercial and Office Land during the Bubble Economy in Japan

Y oshiro Y amamura

Abstract

This study discusses the actual time‑series pattern in commercial and office land prices during a bubble period in Tokyo Central Business District in the late 1980's to early 1990's, a period described as Japanese bubble. A varying‑parameter approach, which allows the implicit prices to vary intertemporally in relation to the attributes, is employed for constructing a transaction‑based price index. Forward extensions of a conventional hedonic index require that parameters of a hedonic model are newly estimated at every extension, using a new data set in which the latest available transaction information is added into an existing data set. These extensions imply that the existing values of the index might vary because hedonic estimators, especially those of time dummy variables, can change. Moreover, a price index that keeps the implicit prices fixed may be biased since implicit prices can be unstable when land values fluctuate sharply as in a bubble period. This study 1s, therefore, an examination of the reliability of indices based on respective approaches and an investigation of the movement of implicit prices over a specific time period. Transaction‑based price indices within the Tokyo CBD are developed for the period from 1981 to 1992. It is shown that the bubble began to form in early 1984 and that the initial collapse began in 1989. Both of these dates are much earlier than the times observed in the appraisal land price index. Furthermore, our results indicate that implicit prices vary

‑188‑ Kagawa University Economic Review

over time and provide evidence of the usefulness and reliability of the varying parameter approach when a market is experiencing the effects of a bubble economy.

1 Introduction

710

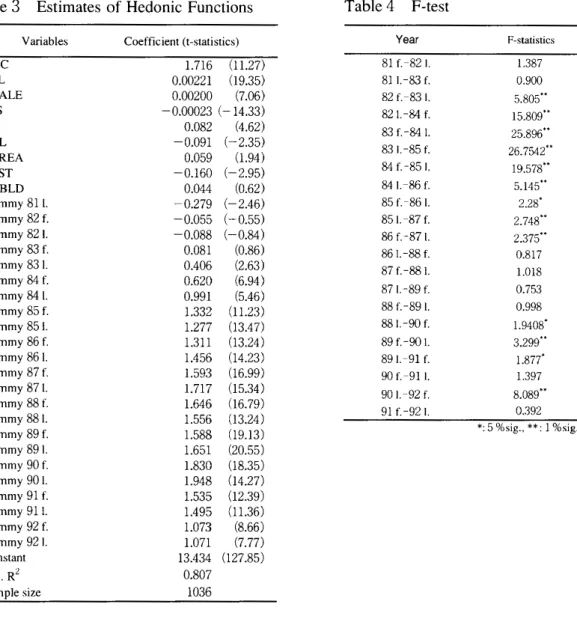

Despite the dramatic effects of the land price bubble in the late 1980s and its collapse, which produced an economic depression in Japan that continued for most of the 1990s, there has been little analysis to construct and understand the land price indices used for commerce. That is partly because of lack of available land price data, and also because land price is less important in North American and European countries, where urban areas have been developed and occupied by durable housing and offices. Property prices in Japan, however, are dependent heavily on the value of land. It is well known that until the bubble burst, the primary motivation to own property was not to gain the cash flow in future but to acquire the capital gain in land value since land prices had been consistently increasing. Thus, it is worth examining the land price changes during the bubble period. Unfortunately, most land price indices in Japan are constructed using assessed land prices‑. Based on transaction data, some rent and price indices in Tokyo have been recently developed, but they are indices for housing and make use of the conventional hedonic method, which has fixed parameters of independent variables in the hedonic equation. Price indices that hold the implicit prices fixed may be biased since implicit prices can be unstable when land values fluctuate sharply as in a bubble period. This study thus attempts to construct land price indices for commercial and office use in Tokyo central business district during the 1981 and 1992 by employing time‑varying (1) It is closely related to the institutional characteristics of land use and buyer constraints for purchasing land in Japan. They are 1) no control on subdividing land; 2) flexible zoning and mixed use ; and 3) ease to obtain mortgages for purchasing land. The last characteristic was dismissed at the end of the bubble period as a result of strong government mtervention.

711

Transaction‑Based Land Price Indices for Commercial and Office Land

during the Bubble Economy in Japan ‑]89‑

parameter method which allows the implicit prices in relation to the attributes to vary intertemporally. Moreover, the differences between the indices used in this study and the appraisal‑based index provided by the Japanese government, which is commonly used as the land price index, are discussed.

The paper is organized as follows. Section 2 reviews the existing thesis on constructing the index and presents the method used to build the index for the Tokyo CBD and the descriptive statistics of the data. In Section 3, hedonic equations are estimated, and the resulting indices are compared with the official appraisal price changes. A discussion of the sample selection bias and precision measures among indices is presented in Section 4.

2 Method Used to Estimate the Index

As Hill, Knight, and Sirmans (1997), among others, clearly stated, there are three methods to construct a price index for assets or property : hedonic, repeat sales, and hybrid.

The repeat sales model was developed by Bailey, Muth, and Nourse (1963). Although this method has been used in many studies because it offers the advantage that the specification of equation forms and selectivity of variables can be eliminated, the sample selection bias and the inefficiency for obtaining data remain problematic. Case and Quigley (1991) proposed a method that combines the repeat sales model with the hedonic model, and Hill, Knight, and Sirmans (1997) solved the error heteroskedasticity problem using Harvey's method (1976). However, Hill et al. use constant implicit prices in their models. Interestingly, Meese and Wallace (1997) noted that the constant implicit price hypothesis was rejected in Oakland and Fremont in 1970 and 1988 by a comparison of the repeat sales, hedonic, and hybrid methods. The reason for the development of hybrid models is partly the motivation to examine the prices of the age and depreciation of housing, which are essential for estimating the rate of return of a housing investment. It should be noted that vacant