The Wage Schedule of a Risk Averse Manager in an Insurance Market

Mahito Okura

■Abstract

This research investigates the wage schedule of a manager in an insurance firm when the manager is risk averse, using a principal ‑ agent framework. The results of this research are as follows. In the case of a monopoly market, a perfectly fixed wage is submitted. In contrast, when the market includes more than one insurance firm, a perfectly fixed wage is not the equilibrium. In addition, this research derives the result that when the number of insurance firms is rela- tively small, if the number of insurance firms increases, the weight of a performance-based wage rises. In contrast, when the number of insurance firms is relatively large, even if the number of insurance firms increases, the weight of a performance-based wage may remain constant.

■Keywords

Wage schedule, Manager, Insurance market

*This article was originally presented at Insurance Theory Seminars and 15 APRIA annual conference. The author would like to acknowledge the financial support by the Ministry of Education, Culture, Sports, Sci- ence, and Technology, Grand-in-Aid for Young Scientists ,21730339. /Acceptance on October26,2011.

1.Introduction

M any studies have implicitly or explicitly assumed that insurers are risk neutral. This assumption may not be realistic because insurers must deal with uncertainty, and current insurance business laws in many countries do not allow insurers to impose an addi- tional insurance premium after an insurance contract is accepted. In addition, the word “insurers”should be carefully considered. In other words, “who”makes important decisions in an insurance firm, such as setting the insurance premium, choosing insurance product posi- tions, developing the insurance business abroad, and so forth? The answer to this question is “managers”. From that viewpoint, many kinds of insurersʼdecisions can be interpreted as managersʼdeci- sions. Then, it seems natural to assume that insurers are not risk neutral, because managers are risk averse and they want to avoid uncertainty in relation to their wages.

Some studies have analyzed an insurance market where insurers are not risk neutral. For example, Stone (1973)introduced an insurer that behaves to maximize its profit, subject to constraints on stability and survival of the underwriting process. Borch(1974)ar- gued that in order to reach the security level required, each person will have to pay not only a net insurance premium but also a safety loading. Hoy(1988)assumed that identical risk-averse insurers have a constant degree of absolute risk aversion. Hogarth and Kunreuther

(1992)and Kunreuther et al.(1993)examined survey data on insurersʼbehavior and concluded that insurers may not be risk neu- tral . Polborn(1998)considered a duopolistic insurance market in

The Wage Schedule of a Risk Averse Manager in an Insurance Market

1) In relation to these studies, see also Shapira(1993).

which homogenous risk-averse insurers competed in their insurance premiums. Picard(2000)built a model in which a risk-averse audi- tor checked whether policyholders misrepresented their losses.

Golubin(2006)investigated Pareto-optimal insurance policies when both insurer and insured are risk averse.

The purpose of this article is to investigate the wage schedule of a manager in an insurance firm when that manager is risk averse, by using a principal‑agent framework. In particular, this research will shed light on the relationship between the wage schedule style

(e.g., a performance-based wage or a fixed wage)and the number of insurance firms. It is easy to imagine that the wage schedule style tends to favor performance-based wages when the number of insurance firms increases because the competition becomes fierce and stockholders(or members of a mutual )want managers to make greater efforts. However, this article mainly investigates how the un- certainty per se affects the wage schedule style. For that reason, this article will determine the relationship between the wage sched- ule style and the number of insurance firms without incentive schemes for managersʼactivities.

This article is organized as follows. Section 2builds the model.

Sections3and4derive the results from the model in monopoly and duopoly markets. Section 5derives the relationship between the wage schedule style and the number of insurance firms by examining a market with insurance firms. Concluding remarks are presented in Section6.

2.The Model

Suppose that there is one(weakly)risk-averse manager and one

保険学雑誌 第 617号

ジ イレ

処理していま す。訂正時注 意

ュラー

risk-neutral stockholder(or a member of a mutual)in an insurance firm. In this case, the manager and the stockholder can be interpret- ed as the “agent”and the “principal”, respectively, in a principal‑agent framework.

Let denote the number of insurance firms . 0represents the insurance money for an insured paid by insurance firm for

∈ 1,2 . This is a random variable because each insurer can- not previously know how much insurance money it will pay at the date of the policy. For simplicity, we assume that the random vari- able is mutually independent and its mean and variance are the same. In addition, is assumed to be distributed in the normal dis- tribution function μ,σ , whereμ≡ represents the mean of an insurance money payout andσ ≡ − μ represents the vari- ance of an insurance money payout .

The demand function for insurance firm is as follows:

= − +γ

∑

, …⑴where γ∈ 0,1. is the insurance demand of insurance firm . and represent the insurance premiums of insurance firms and .

Assume that all managers have the same degree of risk aversion.

n a binomial rather than a normal distrib

2) The following setting of this model is partially indebted to Okura (2006). However, Okura(2006)analyzed quantity competition rather than the insurance premium(price) .

3) Obviously, when an insured is not involved in an accident, then = 0.

4) In the case of life insurance, may be distributed i

t

fore, the following explanation is als

ution. However, if there are a lot of insur- ed, the binomial distribution form can approximate the normal distri-

bution form. There plicable to

the cas

The Wage Schedul

o ap

a Risk Averse Manag

e of life insurance.

rke

in an Insurance Ma

eo f er

行 の こ 式 を

は 数

段 に 送 る た め、

次 の

ュラー 処理していま す。訂正時注 意字 ド リ が 入 っ て い ま す。訂 正 時注意

イレジ←

In addition, each utility function form is assumed to be specified as follows:

= − exp − , …⑵

where 0is the degree of absolute risk aversion of the manager.

represents the managerʼs wage, and is assumed to be:

= α + β , …⑶

where is the profits of insurance firm before subtracting the managerʼs wage, which is written as:

= −

∑

, …⑷In addition,α is the fixed wage and β is the performance-based wage per , on the assumption that β∈ 0,1 .

Substituting equations⑶ and⑷ into equation⑵, we have:

= − exp − = − exp − α+ β −

∑

. …⑸From equation⑸, the certainty equivalent of the manager in insur- ance firm , which is denoted by , is as follows:

= α+ β − α+ β

2 , …⑹

where ・ and ・ represent the operators of expected value 5) Even ifβ >1, the results from our model, described later, are not essentially changed. In contrast,β < 0does not need to be investigat-

ed because it is unrealistic.

6) For the derivation of equation ⑹, see, for example, Freund(1957), Borch(1968), and Cuthbertson(1985).

保険学雑誌 第 617号

and variance. Then, α + β can be shown as:

α + β = α + β − μ . …⑺

Further, α + β is as follows:

α + β = β . …⑻

In equation⑻, can be computed as:

=

∑

= σ . …⑼Substituting equations⑺,⑻, and⑼ into equation ⑹, the certainty equivalent of the manager in insurance firm can be rewritten as:

= α + β − μ− β σ

2 . …

In contrast, the profit function of the stockholder in insurance firm is:

= 1− β − α. …

Then, the expected profit function of the stockholder in insurance firm can be shown as

= 1− β − μ − α. …

Based on the above settings, the following three-stage game is analyzed. In the first stage, the stockholder proposes to the manager the wage schedule described in equation ⑶. In the second stage, the 7) The expected profit and the certainty equivalent of stockholder are

same because the stockholder is risk neutral.

The Wage Schedule of a Risk Averse Manager in an Insurance Market

manager decides whether to accept this proposed wage schedule. If the manager accepts it, the game proceeds to the third stage. If not, the game ends and the manager receives certain reservation utility, represented by . In the third stage, all managers choose their own insurance premium simultaneously.

3.Monopoly Market

In this section, a monopoly market is considered. That is, =1. In the third stage, from equation , the certainty equivalent of the manager in a monopolistic insurance firm is:

= α + β − μ− β σ

2 − . …

Then, the first-order condition is computed as:

= β −2 + μ+ β σ

2 =0. …

From equation , the equilibrium insurance premium can be derived as follows:

= + μ

2 + β σ

4 . …

Some interesting characteristics are found in equation . Because the insurance market is a monopoly market, the insurance firm can receive maximum profits when it sets monopolistic insurance pre- mium = + μ 2. However, the equilibrium insurance premium is β σ 4higher than the monopolistic one. This implies that the man- ager chooses a higher insurance premium in order to decrease demand and lower the uncertainty about the total insurance money.

保険学雑誌 第 617号

Because the manager is (weakly)risk averse, lowering the uncer- tainty leads to a lower risk premium and raises certainty equivalent.

Actually, it is easy to verify that = + μ 2is realized when the manager is risk neutral =0, uncertainty does not exist σ =0, or the wage schedule is perfectly fixed β=0.

In order to compute the first and second stages, substituting equa- tion into equation , the following certainty equivalent of the manager in the monopolistic insurance firm is as follows:

= α + 1

16β 2 − μ − β σ . … Then, the stockholder in the monopolistic insurance firm chooses a wage schedule that maximizes the stockholderʼ s own expected profits, subject to the managerʼs individual rationality constraint de- scribed in equation .

= 1− β − μ − α, …

subject to = α + 1

16β 2 − μ − β σ . … In this case, the stockholder in the monopolistic insurance firm chooses a wage schedule to satisfy = . Then, we have:

α = − 1

16β 2 − μ − β σ . …

Substituting equation into equation , we can rewrite the above maximization problem as follows:

= 1

16 2 − μ − β σ

2 − μ + 1−2β β σ − . …

The Wage Schedule of a Risk Averse Manager in an Insurance Market

The first-order condition can be computed as:

β = − 1

8β σ 4 − μ + 1−3β σ =0. … From equation ,β=0is derived . Thus, in the monopoly market, the stockholder proposes a perfectly fixed wage. From the assump- tion, the manager is(weakly)risk averse and the stockholder is risk neutral. Thus, whatever uncertainty is taken on by the stock- holder a perfectly fixed wage becomes the optimal uncertainty allo- cation. Further evidence to indicate that β=0is that = + μ is achieved whenβ=0.

4.Duopoly Market

In this section, a duopoly market is considered. That is, =2. In the third stage, from equation , the certainty equivalent of each manager in insurance firm is:

= α + β − μ− β σ

2 − +γ . …

Then, each first-order condition is computed as:

= β + μ+ β σ

2 −2 +γ =0. … From equation , the equilibrium insurance premium can be derived as follows:

= + μ

2−γ+ σ 2β+γβ

2 4−γ . …

Some interesting characteristics are found from equation . First, as 8) Equation has two solutions. However,β =0is the only solution

to satisfy the second-order condition.

保険学雑誌 第 617号

in the monopoly market, managers choose the insurance premium that is σ 2β +γβ 4−γ higher than the duopolistic insur- ance premium = + μ 2−γ . However, unlike the monopoly market, the difference in the insurance premium depends not only on the managerʼs own wage schedule but also on the rivalʼ s wage sched- ule. Thus, the duopolistic insurance premium = + μ 2−γ may not be realized even ifβ =0, and we may find that β β

.

In order to compute the first and second stages, the certainty equivalent of the manager in insurance firm , found by substituting equation into equation , is shown as follows:

= α +β 2 2+γ − −γμ − σ 2−γ β−γβ

4 4−γ .

… Then, the stockholder in insurance firm faces the following maxim- ization problem and constraint:

= 1− β − μ − α, …

subject to

= α +β 2 2+γ − −γμ − σ 2−γ β−γβ 4 4−γ

. …

In this case, insurance firm chooses a wage schedule to satisfy

= .Then, we have:

α = − β 2 2+γ − −γμ − σ 2−γ β−γβ 4 4−γ

… Substituting equation into equation , we can rewrite the above

a Risk Averse Manag

The Wage Schedule of er i n an Insurance Mar ket

レジュラー処 す。訂 正 時 注意理 で

イ

maximization problem as follows:

= σ

4 4−γ 2γ 2+γ − −γμ

− β 4 2−γ 2+γ − 1−γμ

−4 σ 2−γ +3 σβ 8−6γ+γ

+ σγβ γ−2 4−γ β − . … The first-order condition can be represented by using the symmetric conditionβ≡ β= β, as follows:

β = σ

4 2−γ 2+γ 2γ − 1−γμ

−β4 4−γ − 1−γμ

+ σ 4−γ2+γ

− σβ 2−γ 6−γ2+3γ . … From equation , the following derivatives can be derived in the cases where >0andσ >0.

β = σγ − 1−γμ

2 2−γ 2+γ >0, …

β = − σ 8−3γ 2 − 1−γ 2μ+ σ

4 2−γ 2+γ <0. … From equations and , we find that the unique equilibrium β ∈

0,1 always exists.

The reason that β ∈ 0,1 is realized in the duopoly market can 9) In contrast, if =0and/or σ =0, allβbecome the equilibrium because neither the manager nor the stockholder needs to consider un- certainty.

保険学雑誌 第 617号

be explained as follows. A higherβ is not desirable to the manager in insurance firm because the uncertainty about the total insurance money also becomes higher. However, a higher β is associated with an incentive for both managers to choose a higher insurance pre- mium that can realize more expected profits of the stockholder becauseβ andβare strategic complements . For those reasons, β

=0is not the equilibrium in the duopoly market.

5.n Insurance FirmsʼMarket

In this section, there are insurance firms in the market . In the third stage, the certainty equivalent of the manager in insurance firm is:

= α + β − μ− β σ

2 − +γ

∑

. …Then, each first-order condition is computed as follows:

= β + μ+ β σ

2 −2 +γ

∑

=0. …From equation , the equilibrium insurance premium can be derived as follows:

10) Thus, if the strategic variables of the managers are strategic substi- tutes,β=0is also the equilibrium in the duopoly market. This can be confirmed by introducing a quantity competition model instead of an insurance premium (price)competition model. For details, see the Appendix.

11) Thus, of course, the results in Section4are obtained when substitut- ing =2into the following equations in this section.

k Averse Manager in an Insurance Mar

The Wage Schedule of a Ris ket

数式が き

たためイレジュ ラー処理をして い ま す。訂 正 時 注意

文末に

=

2 2+γ + μ + σ 2− −2γβ+ −1γ

∑

β2 2+γ 2− −1γ .

… In order to guarantee a nonnegative equilibrium insurance premium, the following assumption is introduced:

2− −1γ 0 2+γ

γ . …

An interesting characteristic of the insurance firmsʼmarket is as follows. Unlike the situation in the duopoly market, β β

may not be satisfied. In order to realize,β β ,2− − 2γ −1 γ 2+3γ 2γ must be satisfied . In addition, because 2+3γ 2γ< 2+γ/γ for all γ, we find that the number of insurance firms that realizeβ β exist.

In order to compute the first and second stages, the constrained maximization problem is shown as follows:

= 1− β − μ − α. …

subject to

= α + β − μ− β σ

2 − +γ

∑

. …From = , equation is changed as follows:

α = − β − μ− β σ

2 − +γ

∑

. …Substituting equation into equation yields the following expect- 12) Because γ∈ 0,1, this assumption is surely satisfied when =2

and =3.

13) Because γ∈ 0,1, this condition is always satisfied when =2. 保険学雑誌 第 617号

ed profit of the stockholder in insurance firm :

= − μ− β σ

2 − +γ

∑

− . …The first-order condition can be represented as follows:

β =

β− β σ − +γ

∑

+ − μ− β σ

2 −

β+γ −1

β =0.… In addition, from equation , we have:

β= σ 2− −2γ

2 2+γ 2− −1γ , …

β= σ −1 γ

2 2+γ 2− −1γ . …

Substituting equations and into equation , and using the sym- metry condition β≡ β = β =…= β, equation can be rewritten as:

β = σ

4 −γ 2+γ 2γ−2β4−γ

− 1−γμ − σβ4−γ(2+γ

−β2−γ 6−γ2+3γ =0. … Then, we find that β>0is surely chosen in the case where >0 andσ >0because:

β = −1 σγ − μ+ −1γμ

2 2+γ −2+ −1γ >0. …

In contrast, the corner solution β=1may become the equilibrium

The Wage Schedule of a Risk Averse Manager in an Insurance Market

because:

β = σ

4 +γ − −1γ

−2+γ −2+ −1 γ 2 +γ−2 2+γ 1− −1 γμ− σ 2+γ1+γ

− −1+γ + −6+3 −2γ

+2 −1γ 2 2+γ− 1− −1 γ 2 2+γμ+ σ 2+ 3+ −3 γ =0.

… From equation , the equilibrium βcan be derived . However, because the form of the equilibrium βis rather complex and it con- tains several variables, we use the following numerical example to illustrate the characteristics of the equilibrium β.

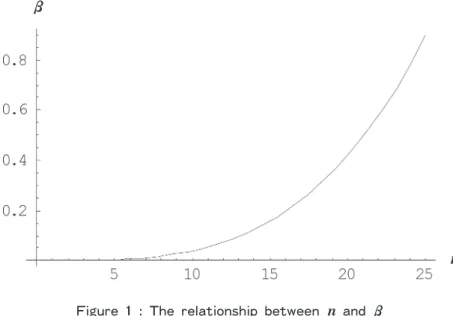

γ=0.02, =1000,μ=100, =2,σ =2.

In the case of these values, the relationship between and βis shown in Figure1.

14) If the case whereβ>1is permitted, of course, the corner solution ofβis changed.

15) Equation has two solutions. However, there is only one solution to satisfy the second-order condition.

保険学雑誌 第 617号

Although this is a sole numerical example, the form of the function in Figure1is almost the same when the given values change . From Figure1, when the number of insurance firms is relatively small, if the number of insurance firms increases, the weight of a performance-based wage rises. In contrast, when the number of insur- ance firms is relatively large, even if the number of insurance firms increases, the weight of a performance-based wage may remain con- stant becauseβ=1has already been realized.

6.Concluding Remarks

This research has investigated the wage schedule of managers in an insurance firm when the manager is risk averse, using a principal ‑ 16) Precisely speaking, a change in γ alters the number of insurance

firms that realizeβ=1.

Figure 1 : The relationship between and

The Wage Schedule of a Risk Averse Manager in an Insurance Market

agent framework. The results of this research are as follows. In the case of a monopoly market, a perfectly fixed wage is the equilib- rium. In contrast, when the market includes more than one insurance firm, a perfectly fixed wage is not the equilibrium. Further, this research concluded that when the number of insurance firms is rela- tively small, if the number of insurance firms increases, there is an increase in the weight of a performance-based wage. In contrast, when the number of insurance firms is relatively large, even if the number of insurance firms increases, the weight of a performance- based wage may remain constant.

The conclusion of this research is very interesting because it reveals a relationship between the wage schedule style and the num- ber of insurance firms without any incentive schemes. However, there are some possible future extensions of the research. First, in this article, all managers have the same degree of absolute risk aversion. If the managersʼdegrees of absolute risk aversion differ, we are interested in whether the wage schedule of the manager who has a higher degree of absolute risk aversion would become more performance-based or fixed. Second, it is important to confirm our conclusion using real-world data. From the conclusion, we predict that emerging new entrants to the insurance market will lead to more performance-based wage schedules.

Appendix

This Appendix proves thatβ=0is the equilibrium in the duopoly market if the strategic variables of managers are strategic substi- tutes. In order to investigate this situation, we introduce a quantity competition model instead of an insurance premium competition

保険学雑誌 第 617号

model. M ore concretely, we change the demand function for the insurance firm as follows:

= − −γ . …(A1)

Using the same computations as in Section 4, the equilibrium insur- ance demand can be derived as follows:

=a+ μ

+γ− σ β−γβ

4−γ . …(A2)

In addition, in the first and second stages, the first-order condition can be represented by using the symmetric condition β≡ β = β as follows:

β = − σ

4 +γ −γ 2γ − μ + β4 4−γ

− μ + σ 4+γ −γ

−2σβ +γ 3−γ …(A3) From equation(A3), the following derivative can be obtained:

β = − σγ − μ

2+γ 2−γ<0. …(A4) From equation(A4), we find that β=0is the equilibrium.

(The author is an associate professor, Faculty of Economics, Nagasaki University)

References

Borch, K., The Economics of Uncertainty, Princeton University Press, Prin-

ceton,1968.

Borch, K.,The Mathematical Theory of Insurance, Lexington Books, M as- sachusetts,1974.

Cuthbertson, K.,The Supply and Demand for Money, Basil Blackwell, Ox-

The Wage Schedule of a Risk Averse Manager in an Insurance Market

ford,1985.

Freund, R. J., “The Introduction of Risk into a Programming M odel,”

Econometrica24,253‑263,1957.

Golubin, A. Y., “Pareto-Optimal Insurance Policies in the M odels with a Premium Based on the Actuarial Value,”Journal of Risk and Insurance

73,469‑487,2006.

Hogarth, R. M . and Kunreuther H., “Pricing Insurance and W arranties:

Ambiguity and Correlated Risks,”Geneva Papers on Risk and Insurance Theory17,35‑60,1992.

Hoy, M., “Risk M anagement and the Value of Symmetric Information in Insurance Markets,”Economica55,355‑364 ,1988.

Kunreuther, H., Hogarth, R. M., and Neszaros, J., “Insurer Ambiguity and Market Failure,”Journal of Risk and Uncertainty 7,71‑87,1993.

Okura, M., “Welfare Effect of Firm Size in Insurance M arket,”Insurance Journal57,113‑124,2006.

Picard, P., “On the Design of Optimal Insurance Policies under M anipula- tion of Audit Cost,”International Economic Review41,1049‑1071,2000. Polborn, M . K., “A M odel of an Oligopoly in an Insurance M arket,”

Geneva Papers on Risk and Insurance Theory23,41‑48,1998.

Shapira, Z., “Ambiguity and Risk Taking in Organizations,”Journal of Risk and Uncertainty7,89‑94,1993.

Stone, J. M ., “A Theory of Capacity and the Insurance of Catastrophe Risks(PartⅠ andⅡ),”Journal of Risk and Insurance 40,231‑243and 339‑355,1973.

保険学雑誌 第 617号