西 南 交 通 大 学 学 报

第 55 卷 第 2 期

2020 年 4 月

JOURNAL OF SOUTHWEST JIAOTONG UNIVERSITY

Vol. 55 No. 2

Apr. 2020

ISSN: 0258-2724 DOI:10.35741/issn.0258-2724.55.2.53

Research articleEconomics

I

S

C

ORPORATE

S

OCIAL

R

ESPONSIBILITY

D

ISCLOSURE

G

OOD FOR

A

CCRUAL

P

ROFIT AND

R

EAL

M

ANIPULATIVE

P

ROFIT

M

ANAGEMENTS

?

企业对纯利润和实际操纵性利润的管理承担社会责任吗?

Suwarno Suwarno a, *, Rahmawati Rahmawati b, Djuminah Djuminah b, Muthmainah Muthmainah b, Widagdo Ari Kuncara b

a Doctoral Program in Economic Sciences, Universitas Sebelas Maret/STIE Purna Graha

Pekanbaru, Indonesia, [email protected]

b

Department of Accounting, Universitas Sebelas Maret

Surakarta, Indonesia, [email protected], [email protected], [email protected],

Received: February 01, 2020 ▪ Review: April 4, 2020 ▪ Accepted: April 24, 2020 This article is an open access article distributed under the terms and conditions of the Creative Commons

Attribution License (http://creativecommons.org/licenses/by/4.0)

Abstract

This study examines the effects of Corporate Social Responsibility disclosure on the profit management of Indonesian mining companies which has rarely been done by previous scholars. This research was conducted on the mining sector in Indonesia. The research period covered was from 2009 until 2017 with 414 sample observations used. The hypothesis was analyzed by using the STATA program. The findings showed that Corporate Social Responsibility has a good relationship with accrual and real manipulative profit managements.

Keywords: Corporate Social Responsibility, Accrual Profit Management, Real Manipulative Profit

Management 摘要 这项研究考察了企业社会责任披露对印尼矿业公司利润管理的影响,这是以前学者很少做的 。这项研究是针对印度尼西亚的采矿业进行的。研究期间为 2009 年至 2017 年,使用了 414 个样 本观测值。通过使用斯塔塔程序分析了假设。调查结果表明,企业社会责任与权责发生制和实际 操纵性利润管理有着良好的关系。 关键词: 企业社会责任,应计利润管理,实际操纵利润管理

I. I

NTRODUCTIONLu et al. [1] states that Corporate Social Responsibility (CSR) is an idea or method of an actual action as realization of social responsibility. CSR has been considered an additionally important matter for business and could be described as the main competitive reason and company performance to survive and it has successfully succeed in business [2]. Although many mining sector companies have been promoting CSR but environmental damages, distance changes/wider natural landscape, such as ex-lead mining in Bangka, gold mining at Newmont Minahasa Raya, Inc, and gold and lead at Freeport, Inc [3]. Cases concerning CSR include PT Meares Soputan mining which contaminated the surrounding environment and nature.

CSR is assumed as the core and unavoidable priority of business ethics. Thus, a company will not only have responsibility for stakeholders but also to other concerned parties [4], [5], [6]. CSR is also described as a connection network which separates the owner, manager, and other stakeholders [7]. When CSR is not promoted well by a company, then consumers in the public will be sensitive to any socially correlated issues which may lead to punishment by keeping off the products or the service [8], [9].

Research on the relationship between management earnings and CSR still shows inconsistent results. Profit management could be categorized into two groups: accrual profit management and real manipulative profit management. Roychowdhury [10], Li [11], and Gunny [12] provided results showing negative differences between the two (earnings management and CSR) In contrast, Prior et al. [13] argues there is a positive relationship between the two variables that tends to result in earnings for management.

This research examines the influence of CSR disclosure on profit management of Indonesian mining companies which was found to have been rarely done by previous scholars. The mining companies were selected because their operating activities were closely related to natural source exploitation and the environmentally damaging effects on surrounding mining environments. Furthermore, the mining sector also had great capacity value compared to other sectors, making it attractive to investors.

Eisenhardt [14] assumes agency theory, namely how human attitudes are related to assumptions. It also reveals how humans have limited rationality. This partition can be minimized by including several individuals who

want to achieve their goals or functions. The role of management in the use of accrual manipulative earnings management is also evident, such as avoiding loan agreements, deviation of conversation costs [15], the existence of motives for opportunities to prioritize themselves or groups, such as promotional gifts, promotions, and honorariums and other shares as options appointed [16].

When stakeholders get an indication of earnings management in the company, the value of the company will experience a significant decline in exchange. This will have an influence on other actors and stakeholders. In other words, the stakeholders will implement a policy that can threaten managers. Something that managers can certainly do is maintain their position by designing and engaging in activities with a goal that can improve the company's relationships with those who have interests in the social environment through CSR. To get support from groups, specific CSR activities include incorporating several social aspects into the production process, or adopting progressive human resource development practices to enhance green concept activities. They make this through recycling, reducing pollution and waste, or by accelerating the overall goals of social organizations [17].

Sial et al. [18] provide evidence that CSR disclosure has a positive influence on profit manipulation. Kim et al. [19] stated that when a company revealed its profit manipulative CSR through the company's operational activities, CSR is revealed as a way of enforcing it in anticipating or preparing for stakeholder dissatisfaction. Then the hypothesis:

H1: Positive CSR disclosures on profit

management.

II. M

ETHODS/M

ATERIALS A. Population and SampleThis research was conducted on a mining sector in Indonesia from 2009 to 2017. 2009 was chosen as the starting point because it represents the year after the global crisis that impacted Indonesia. The data source was secondary data. This research used secondary data from www.idx.co.id, in the form of businesses' financial reports: profit and loss and balance reports of companies within 2009 until 2017. They were gained from annual reports issued by Indonesian Exchange Stock.

GRI Indicator 4 (global reporting initiatives) was obtained from [20] as an introductory index of CSR. This study uses the GRI 4 indicator because it employs international standards used by mining companies. Each item was given a score of 1 if it was disclosed, or a score of 0 if it was not disclosed [21]. Then, the score was added and divided by the item numbers of each company type. The CSRDI formula is [21]:

∑Xij

CSRij = ––––––––– (1) Nj

Remark:

CSRij = Corporate Social

Responsibility

n = company's item numbers

X = dummy variable, 1 if it was disclosed, 0 if it was not.

Disclosed

Therefore 0 < CSR < 1.

Accrual earnings management uses the Discretionary Accrual (DA) proxy and the Modified Jones Model. The real manipulative profit management used Roychowdhury model [10] with real manipulative profit management estimation through selling, reducing discretionary cost, and other exaggerate production.

III. R

ESULTS ANDD

ISCUSSIONTable 1 provides the detail of sample number determination. The sample consisted of 414 companies.

Table 1. Research sample

Table 2 shows the average of DA variable. It is 0.005, indicating that the company committed discretionary accrual profit management to increase the profit (income increasing). The real profit management with the mean of AbnCFO, AbnEXP, and AbnPROD variables respectively scored -0.0002, 0.614, and -1.093. They indicated that the company committed real profit management through operational cash flow, discretion, and discretionary production cost. It showed that there was indication of the company having manipulated the real profit through AbnCFO, AbnEXP, and AbnPROD.

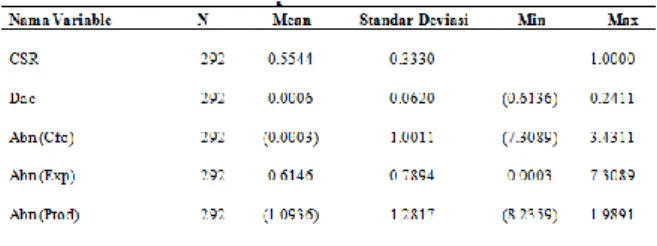

Table 2.

Descriptive statistics 2009-2017

The value of CSR disclosures showed that the disclosing levels of published CSR of the observed companies were found in an annual report. Based on CSR data revealed, the lowest score of the variable is 0.00 (Perdana Karya Perkasa, Inc) with the highest score 0.94 or 94% (Adaro Energy, Inc). As such, higher CSR meant higher CSR disclosing levels of the companies. In this research, the level of CSR is defined as high accountability and transparency of the companies to the stakeholders. The CSR average in this research was 0.55, meaning 55% of CSR disclosure information was disclosed by the observed companies. The deviation value was 0.33, showing that the CSR data variation was also low. When compared to minimum value (0.00), maximum value (0.94) to median (0.59), and mean (0.55), it indicated that the data was no difference from the average.

Meanwhile, CSR group disclosures in several countries [13] showed the highest are: Luxembourg, Taiwan, Finland, Denmark, Norway, Canada, Austria, and the United Kingdom with sequential percentages respectively as follows: (72.64%), (62, 09%), (60.52%), (58.84%), (57.91%), (56.58%), (56.23%), (55.63%). The lowest disclosures were Mexico, Singapore, and Greece (27.08%), (27.95%), (26.64%). Meanwhile, the United States is 45%. The results for CSR disclosure in this study were 58%, which is an improvement. The score showed that CSR disclosure improvement of Indonesian companies, especially mining, was sufficiently excellent.

In order to test the hypothesis, multiple linear regression analysis was used along with the STATA program for the hypothesis. The analysis with panel data needed several determination tests of the best model. The first model was Chow test. Based on the test results, obtained a P-Value higher or greater than 0.05. The better estimation model was the common effect model as opposed to the fixed effect model. The Lagrange Multiplier (LM) using the Breusch-Pagan test was then used to determine the best model. Based on the results, the p-value was higher than 0.05, indicating that the common

effect model performed better than the fixed effect model.

This study also conducted a classic assumption test. The first test was the normality test. The results of that test indicated that residual data were normally distributed, because the significance level 0.137 is greater than 0.05. After that, a regression model tested for multicollinearity. The results showed more values of 0.10 and fewer than 10 VIF values. As a result, it can be concluded that in there was no multicollinearity. The third test was an autocorrelation test. The Durbin-Watson value was 1.907. The Durbin-Watson table at k = 4 and n = 31 shows the value of dL = 1,160 while dU = 1,735. A value of 4-dU = 4-1,739 = 2,265 was obtained. The value of 1.735 < 2.081 < 2.265. From these results, it can be concluded that autocorrelation was not present.

C. Hypothesis Tests

The test aims to study whether CSR disclosure influences the accrual and real manipulative profit managements by multiple regression analysis.

The results of the CSR disclosure hypothesis are positively influenced by the accrual and real earnings management. From the results of the tests carried out in the DAC column in Table 3, the CSR coefficient value of 0.450 is obtained with a significant level of 0.021. The hypothesis can be accepted with a significant score of less than 5%. Therefore, a conclusion can be drawn that the disclosure of the CSR has a positive effect on accrual manipulative profit management. The same results were obtained for real profit management, as the CSR disclosure for the real manipulative profit management also had a positive effect. Column Abn (Cfo) in Table 3 obtained the value of the CSR disclosure coefficient as 0.695 with a significance level of 0.04. Therefore, the hypothesis can be accepted with a significance of less than 5%.

This study describes the CSR disclosures of positive results on two managements: real earnings and accrual. The test results in the DAC column in Table 3 obtained the coefficient score of CSR, which was received with a value of 4.09 and a significance of 0.03. Therefore, the results conclude that CSR disclosure has a positive effect on accrual manipulative profit management. The results were the same for real profit management. In the Abn column (Cfo) in Table 3, the value of the CSR coefficient is 10.47 with a significance level of 0.03. Therefore, this research hypothesis was accepted because the significance was 5% smaller.

Table 3.

Summary of the test result

The results of the study are in accordance with Sial et al. [18], who provide an explanation of the relationship of the CSR disclosure with both accrual and real earnings management. This is reflected in the reports by Prior et al. [13] and Chih et al. [22], which were conducted in European and developed countries. However, these countries differ from the still-developing Indonesia. Completed CSR disclosures can improve the company's image so that it becomes attractive for the investors and other parties who will use the financial statements in the future.

CSR activities in companies have become an interesting topic to discuss. In addition, CSR must have become a basic need for companies so that the benefits can be enjoyed by all parties, therefore CSR is not merely symbolic.

IV. C

ONCLUSIONOverall, the results show that the research carried out today is likely to contribute to the prior research on how CSR disclosures positively influence the accrual and real manipulative profit managements. When the CSR disclosure of a company is high, it will improve the public’s image of the company. This means that their accrual and real manipulative profit managements can be covered. The limitation of this study is that it only uses two earnings managements (accrual and real earnings) and does not refer to the other existing earnings management options. This study also only reviews the mining sector, which means that the results cannot be generalized to the other sectors.