Title

An experimental study of the effect of bidding increments on the

contract price of online auction

Author(s)

Jing FU

Citation

福岡工業大学情報学研究所所報 第28巻 P25-P28

Issue Date

2017-10

URI

http://hdl.handle.net/11478/767

Right

Type

Departmental Bulletin Paper

Textversion publisher

福岡工業大学 機関リポジトリ

FITREPO

An experimental study of the effect of bidding increments

on the contract price of online auction

Jing FU (Department of System Management, Faculty of Information Engineering)

Hideyuki FUJII (Department of System Management, Faculty of Information Engineering)

Abstract

In recent years, online auction has been widely used in a variety of fields. Unlike traditional auctions, it introduces this mechanism to the masses, and provides them with a broad selection of goods to buy or sell. This paper focuses on finding a better bidding increment rule to maximize the contract price from exhibitors’ perspective. The primal method applied here is to compare the effect of fixed and variable bidding increments on the contract price by simulation with C language. The auction is assumed to be first-price and open-bid with installation of automatic bidding system. Our simulation results show that for goods at all market prices, there exists certain fixed bidding increment(s) outperforming the variable one. However, with other fixed bidding increments, variable bidding increments usually perform better.

Keywords: Online auction, Contract price, Fixed bidding increment, Variable bidding increment

1. INTRODUCTION

Nowadays, millions of consumers located on different continents are engaged in competitive exchange via online auction. While there is immense amount of literature that analyzes auction mechanism and bidding strategies, the effects of bidding increments on the contract price are yet to be justified well. Here, we empirically examine how the contract price is influenced by the bidding increments in online auction from exhibitors’ viewpoint.

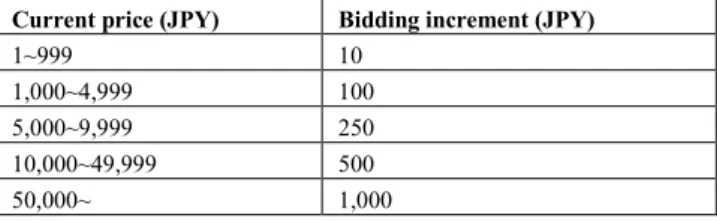

Online auctions come in many different formats, but most popularly in Japan it is first-price and open-bid, i.e., Yahoo auction. It is an ascending-bid auction in which bidding prices are open for all and winners pay what they bid to receive the goods. Yahoo auction has its own rules for bidding increments as shown in Table 1. It is automatically updated by the auction system based on the current bidding price, and cannot be selected by the exhibitor. However, the risk of failed auction due to low demand from exhibitors’ perspective might be increased with this pre-decided bidding increment rule. In order to verify the effect of bidding increments on the contract price, we conduct a simulation for goods with market prices from 250JPY to 100,000JPY and fixed bidding increments from 1JPY to 1,000JPY, and compare the contract prices with that of Yahoo auction.

Table 1. bidding increments in Yahoo auction

Current price (JPY) Bidding increment (JPY)

1~999 10

1,000~4,999 100 5,000~9,999 250 10,000~49,999 500

50,000~ 1,000

2. ONLINE AUCTION MODEL

2.1 AUTOMATIC BIDDING

The simulation is installed with automatic bidding. In other words, a bidder places a bid on the good and enters the max amount she is willing to pay for it. Then the system places bids on her behalf starting with the corresponding bidding increment until the bid is successful or her max bidding price is reached.

2.2 TYPES AND CHARACTERISTICS OF BIDDERS

The bidders are categorized into four types according to their bidding characteristics (Sugawara and Matsuda, 2005), which is summarized in Table 2.

1). Early bidder (EB) places a bid from the first half and continues until her max bidding price is reached, which is often observed in auction beginners.

2). Cheap early bidder (CEB) concerns more about the price, and bids frequently during the first half within her max bidding price.

3). Sniper (SP) places a bid only once within her max bidding price at the last minute, which is often observed in experienced bidders.

4). Sniper by continuation (SPC) bids continuously at the last minute until her max bidding price is reached.

Table 2. types and characteristics of bidders

Type Bidding time Max bidding price (% of market price)

Bidding probability (%)

EB First half 25~75 20~30 CEB First half 20~50 10~20 SP Latter half 50~85 70~80 SPC Latter half 50~80 30~50

Jing FU, Hideyuki FUJII

2.3 ALGORITHM

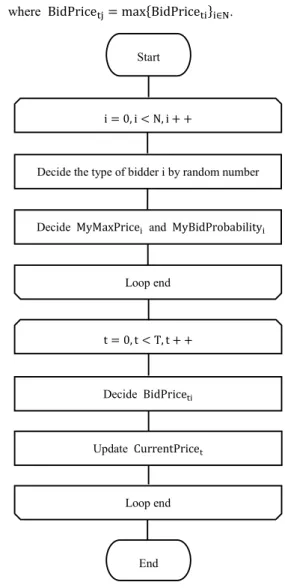

The algorithm is summarized in the flowchart below (Figure 1). 1). Assume that N = {1, … , n} bidders are involved in the auction, and their types are randomly decided. Then their max bidding price and bidding probability are assigned in accordance with bidders’ characteristics.

2). At stage t ∈ {1, … , T}, if the max bidding price for bidder i satisfies the following condition, she will place a bid

MyMaxPricei≥ CurrentPricet−1+ BIt

where BIt is the bidding increment at t. Otherwise bidder i will exit the auction.

3). The bidding price submitted by bidder i is BidPriceti= CurrentPricet−1+ bti

where bti is the bidding increment of bidder i at t

which is decided by bti= randint (1, ⌊

MyMaxPricei− CurrentPricet−1

BIt ⌋) BIt

4). If automatic bidding is applied, current price will be updated to

CurrentPricet= max{BidPriceti}i∈N\{j}

where BidPricetj= max{BidPriceti}i∈N.

3. EXPERIMENTAL RESULTS

Following the algorithm above, contract prices with fixed bidding increments ranging from 1JPY to 1,000JPY are compared with that of Yahoo auction. In this experimental study, there are 50 bidders involved, and 200 iterations are conducted for all market prices and bidding increments.

The differences (average value of 200 iterations) between the contract price with fixed bidding increments and that with yahoo variable bidding increments are summarized in Figures 3 and 4. It suggests that yahoo variable bidding increments are not always the optimal choice for exhibitors, and there exists certain fixed bidding increment(s) outperforming the variable one at all market prices in this experiment, as is shown in Table 3. For example, 50,000JPY goods can be sold at an average contract price of 40,374.87JPY with fixed 250JPY bidding increment, while the contract price with variable bidding increment is 107.15JPY lower in average (Figure 2). Moreover, the best fixed bidding increment at all market prices is lower than the corresponding bidding increment in yahoo auction. The simulation results also indicate that fixed lower bidding increments perform better for goods with lower market prices, while fixed higher bidding increments perform better for goods with higher market prices.

Table 3. market price and its corresponding best fixed bidding increment(s) such that cpfix− cpyahoo is maximized

Market price (JPY) Best fixed bidding increment (JPY)

250 1, 5 500 5 750 5 1,000 5 2,500 10 5,000 50 7,500 50 10,000 50 25,000 100 50,000 250 75,000 500 100,000 500

Figure 2 average contract prices at 50,000JPY with fixed and variable bidding increments

Start

i = 0, i < N, i + +

Decide the type of bidder i by random number

Decide MyMaxPricei and MyBidProbabilityi

Loop end t = 0, t < T, t + + Decide BidPriceti Loop end End Update CurrentPricet

Figure 3 average cpfix− cpyahoo for low market prices Figure 4 average cpfix− cpyahoo for high market prices

4. CONCLUDING REMARKS

Theoretical considerations suggest that variable bidding increment rule in yahoo auction (lower bidding increment for lower price, and higher bidding increment for higher price) can improve the bidding efficiencies. No bidder wishes to compete for goods at 100,000JPY with a bidding increment like 1JPY. However, the clear difference between contract prices with fixed and variable bidding increments is evidence that appropriate selection of fixed bidding increment may increase the contract price and benefit the exhibitors more. This evidence is strengthened by observations for goods with high market prices. It suggests that bidding increment is an important element of the auction design. On the other hand, bidders’ types and characteristics may account a large portion for this difference, and there is still room for controlled experiments to help supply a detailed understanding. Moreover, bidding increments higher than 1,000JPY also remain to be examined furtherly.

Jing FU, Hideyuki FUJII

ACKNOWLEDGMENTS

This work was supported by Start-up Grants from Computer Science Laboratory, Fukuoka Institute of Technology.

(Received on June 30, 2017)

References

(1) K. Sugawara and S. Matsuda: “The proposal and verification of the network auction model which attains successful bid price optimization of exhibitors side”, IPSJ SIG Technical Report, Vol. 32, pp. 41-48 (2005).