◆論 文

A Road to Construct a Valuation Model for Intellectual Properties

KentaroKaneta

SYNOPSIS:Manybusinesspersonsrecognizeanimportanceofintellectualproperty (IP)asavaluedriver.However,thebalancesheetfailstorecognizeIPsbecausethereis novaluationmodelwidelyacceptedsofar.AmaintrendofIPaccountingresearchhas shiftedfromtheDICMtotheNarrativeMethodduringthelatest10years.TheDICM evaluatesanindividualIPasapresentvalue.TheNarrativeMethodevaluateagroup ofIPsfromtheviewpointofbusinessfeasibilityalongwithaplentyofexplanatory wordsandsometimesreferredasthedisclosureofnon-financialinformation.

Notwithstandingsuchatrend,IbelievethattheDCIMcannotbeabandoned.There arethreereasons.First,theamountofIPappearedonthebalancesheetshouldbe,as wellasotherassets,anaggregatedamountofindividualIP.Therefore,anevaluationof individualIPsapartfromgoodwillisafundamentalpremiseforrecognizingIPsonthe balance sheet. Seconds, a recognizing IPs apart from goodwill is indispensable to calculateaproperperiodicprofitbasedonthetraditionalmatchingprinciple.Finally,an evaluationofIPsundertheacquisitionmethodofbusinesscombinationaccounting directlyaffectsanamountofprofit(gainonabargainpurchase).

ThefatalproblemsintheDICMseemtobeinitssubjectivityandvariability(in value-in-use).Ifitistrue,analternativemaybeanestablishmentoftheoreticalbaseto acceptsuchsubjectivityandvariability.Theaccountingforotheritems,suchaspost- retirementliability,interestswap,warrant,andimpairmentloss,perhapsmightbe referenceableforthepurpose.

KEYWORDS:IP valuation; DICM; Narrative Method; Goodwill; Purchase Method;

AcquisitionMethod;FuturePrediction.

Ⅰ.INTRODUCTION

Morethan20yearshavealreadybeenpassingsinceaplentyofheateddebateson the valuation for intellectual property (IP) began around the millennium. Several authoritativearticleswereissuedattheera,includingaseriesofresearchresults conductedbyBrookingsInstitutionsandoneswrittenbyProfessorBaruchLevand others.Theseresearchesapparentlyreflectedadramaticshiftofvaluedriversfrom tangibleassetstoIPs.Thatis,IPssuchaspatents,copyrights,in-processR&Ds,design, brand names, and customer relationships have become a fundamental source of company’sprofitabilitysincearoundthemillennium.Forexample,APECshowsadata thatamarketsharewhichisattributabletoIPshaveincreasedfrom17%in1975and 32%in1985to80%in2005anditfinallyreachedto87%in2015(APEC2018,p.6).

NakamurapointsoutthataninvestmentonIPsbyU.S.economyhasreachedto$1 trillionby2000(Nakamura2003,p.25).

TheIP-intensivebusinesshasalsobeendrivenbythepro-patentpoliciescarriedout byGovernment.TheU.S.Government,apioneerofpro-patentpolicy,implemented manypoliciessuchassimplifyingpatentapplicationprocedures,tax-exemptionforR&D intensivecompaniesandfosteringbusinesspersonswhocanexercisehis/herIPskills.

Asaresultofthesepolicies,thenumberofpatentapplicationhasgrownfrom126,788 in1985to315,015in2000(USPTO2018).Aswith,company’srevenuefromroyaltyhas alsogrownfrom$1.5billionin1990to$50billionin2007(ATG2007).

JapaneseGovernmentalsodevelopedan“IPinfrastructure”asacourseofpro-patent policy.TheIntellectualPropertyBasicLawwaslegislatedin2002andthecabinethas implementedmanypoliciesbasedonthelaw,withpublishing“theIntellectualProperty PromotionPlan”everyyear.

WhathasbeenacrucialpointinthediscussionforderivingatmostvaluefromIP intensivebusinessorforderivingafavorableresultfromthepro-patentpolicy?The answeris,atleastintheaccountingsociety,ameasurementofIPsandanestablishment ofIPvaluationmodel.ProfessorBaruchLevhadthistosayinhis2003articlethat

“current financial statements provide very little information about these assets ...(omitted)...solvingthisproblemwillrequireon-balance-sheetaccountingformanyof theseassets(Lev2003,p.17)”.ProfessorHirosehadthistosaythat“whenimplementing anIPbusinessstrategy,itisimportanttofurtherenhancethevalueofIPsanddevelop

amethodologytoadequatelymeasuresuchvalue(METI2002(Hirosereport),Ⅰ-2)1”.

Have these concernsraised by the prominenttwo professorsbeen successfully clearedduringthelatest20years?IbelievethattheanswerisregrettablyNo!Itissaid thatnoneofthepublishedmethodshasbecomeacommonlyusedmethodworldwide (Pastor2017,p.388)ortherearenotmanystandardizedIPvaluationmodelsorvaluation methodswithacertainlevelofcredibility(APEC2017,p.412).ProfessorLevandhisco- authorsay,intheir2016book,thatweprovedthatintangiblesareamajorcauseof accounting’srelevancelost(Lev=Gu2016,p.91)2.

ThisarticleexamineswhyameasurementofIPandanestablishmentofIPvaluation modelhavenotaccomplishedduringthelatest20years.

Ⅱ.Types of IP valuation

ThesimplesttypeofIPvaluationisbelievedtobeacapitalizinganIPasanasseton thebalancesheet3.Thistypeofvaluationmaybeeasilysupportedbyresearcherswho standonafinancialaccountingperspective,whichissometimesreferredas“Financial ValuationMethodsorDirectIntellectualCapitalMethods(Sveiby2010,p.3)(Pastor2017, p.388)”.IuseaterminologyasDICM,hereinafter,todescribethistypeofvaluation.

As well known, three approaches for capitalizing IP are widely applied; Cost approach,MarketapproachandIncomeapproach.Ibelievethattheincomeapproachis the most appropriate approach for capitalizing IP, and DICM is classified as an applicationofit.Forexample,ifapatenttobevaluedisexpectedtogenerate$100cash flowseachyearforthecoming3yearsandanappropriatediscountrateisestimatedas 4%, the capitalized value of the patent can be calculated as $277 (=$100/1.042 +$100/1.04+$100/1.043).

TheconceptofDICMisverysimpleandisunderstandableintuitively.Infact,several brandvaluationmodelsareconstructedbasedonDICM(METI2002)(Rocha2014).

However,somedifficultproblemscomeoutwhenitturnstovalueapatentbasedon theDICM.Themostdifficultproblemcomesfromthefactthatcashflowsarenot generatedsolelyfromthepatenttobevalued.Forexample,notonlythepatenttobe

1 I use the terminology “Intellectual Property (IP)” interchangeably with “Intangible Asset or Intangibles.”Thereforetheword“intangible”usedintheHirosereporthasbeenalteredtoIPinthis article.

2Theyinsist,throughoutthebook,theaccounting’srelevancelostandtheyrefersuchalostasthe End of Accountingwhichisthetitleofthisbook.Theysaythatthe Death of Accountingwasamong thecandidatesforthetitleofthisbook.

3ThisarticlemainlyfocusesonapatentwhenconsideringthetargetofIPvaluation.

valuedbutalsoseveralperipheralpatentsordefensepatentsareneededtogenerate thecashflows4.Thisisbecausethatiftheexploiterdoesn’thaveperipheralpatentsor defensepatents,itcannotmanufactureand/orsaleapatentedproduct.Ortheexploiter maybedeclaredtohaveinfringedanotherentity’sright.

Inadditiontoperipheralpatentsordefensepatents,severalcorporatecapitalsare indispensabletogeneratecashflows.Theyincludehumancapital,structuralcapitaland relationalcapital(Pastor2017,p.394).Forexample,thecashflowswillvarydepending onwhousethepatentand,therefore,theexistingofexpertsofrelated-technologyfield andtheirtalentedskills(humancapital)areindispensable.Thecashflowswillalsovary dependingonthecapabilityoftheentityasanexploiterand,therefore,anoptimal structureoftheentity(structuralcapital)isindispensable.Furthermore,thecashflows willvarydependingonhowmanypatentedproducttheentityisabletoselland therefore,acontinuouscustomerbase(Relationalcapital)isindispensable.Ofcourse,the cashflowsarealsoaffectedbyanyotherconditionssuchasthenumberofexpected licensees,thepotentialforinvalidationappealandanewtechnologydevelopedbyrival entities.Noonecanlist-upeverycondition.

Thismeansthatapatentcannotbevaluedatstand-alonebasis.ProfessorHirosehad thistosayaboutitthatapatentvaluationrequiresqualitativeevaluationbasedon technologicalfactorsandlegalfactorsinadditiontothequantitativeevaluation(Hirose 2013,p.12).APECalsostatesthat“IPvaluationconsidersfutureconditionsofintangible assets, and IP is examined from various aspects such as technology, rights, marketability,andbusinessfeasibility,soitisdifficulttoprovideanexactcalculation (APEC2017,p.412)”.

Therefore,thismethod(DICM)hasgraduallybecomeatargetoftoughcriticism.For example,APECstatesthatthepurposeofvaluationisnottofindabsoluteandperfect value (APEC 2018, p.27). Furthermore, a researcher states that by translating everythingintofinancialtermstheycanbesuperficial(Pastor2017,p.389).Anotherone insiststhatthepurposeofvaluingintellectualpropertyshouldbelearning(Sveiby2010, p.3).ECalsostatesthat“IncorporatingIPassetsonthebalancesheet,particularlythose assetswhosevaluehasnotbeentestedinthemarket(throughatransactionofsome sort),cangiveafalsepictureofthefinancialviabilityofabusiness(EC2014,p.36).

4Theseassetsthatareusedtosupportthepatenttobevaluedortoenhanceitaregenerally explainedascontributoryassets(ICC2019,p.22).

IbelievethatamainconceptofIPvaluationhasapparentlyshiftedfromDICMto

“NarrativeMethod”mainlyafter2010.Suchashiftseemstohavebeenpromotedby severalinternationalorganizations.EChadthistosaythat“havinganauthoritativeor regulatorybodythatsetsstandardsandprovidedcertificationsonaglobalbasiswould improvethecurrentlimitationswithregardstoIPvaluationwork(EC2014,p.22)”.The followingtablesummarizestheexamplesofNarrativeMethod.

Table1 Narrative Methods

(1)PatentValuationSupportforCommercialization KIPA

(Korea) IPvaluationserviceprovidedforSMEs.

The purpose of valuation includes a valuationofbusinessfeasibility.

(2)IPBusinessValuationReport JPTO

(Japan) It calculates a range of business value, whichleadsIPvalues.

(3)IFRSManagement

Commentary IASB

(2010) Itiscommentaryincludedintoanexisting financialreport,whichshowsmanagement’

viewfortheirbusiness.

(4)EUAccountingDirective

“ManagementReport” EU

(2013) Itrequirescompaniestoreportfinancial andnon-financialinformationtounderstand itsbusiness.

(5)IntegratedReporting IIRC

(2013) Itrequirescompaniestoexplainhowthe company’sbusinesscreatesavalue.

(6)IntangiblesReporting

Framework WICI

(2016) Business sustainability is reported thorough a combination of narrative informationandKPI(number).

(1)ThisserviceisrunbytheKoreaInventionPromotionAssociation(KIPA).KIPA’s homepagestatesthatwe“conductsprofessionalvaluationsofpatentedtechnologies, enhancestheutilityofrelatedpatentedtechnologies,ensureswell-orderedtechnology transfertransactions,providescommercialandtechnologicalsecurity,promotestheuse of patented technologies, and helps cultivate and grow technology markets”. This programisintroducedbyAPECasasupporttoSMEstryingtoconductanIPbusiness.

APECviewsthisserviceincludesavaluationontechnology,rights,businessfeasibility, andtechnologyvalue(APEC2017,p.417).

(2)ThisisrunbyJapanPatentOffice(JPO).Thisprogramisalsointroducedby APECasasupporttoSMEstryingtoconductanIPbusiness.Somesamplesareposted onJPO’shomepage.Thesampleconsistsof59pagesandfollowing5chapters.After Chapter 1 which is a summary, Chapter 2 (Facts regarding the Company and its Business)statesaprofileofthecompanyanditslineupofproductswithpicturesand explanatorysentences.Financialstatementsarealsopostedhere.Chapter3(Facts regardingtheIP)listsupeveryIPsownedbythecompanyandonescurrentlyunder

assessments.ContentsofeachIParebrieflyexplained.Chapter4(Factsregardingthe MarketandCompetition)statesthemarket’sconditionstowhichthecompanybelongs.

Itincludesthemarket’ssizeandaprospectoffuturegrowth.Furthermore,thenumber andconditionsofIPsownedand/orappliedbycompetitorsarestatedhere.Chapter5 (Business Plan) states the business plan for each segments. And based on it, the evaluatorestimateskeyfinancialitems(KPI),suchasworkingcapital,discountrates, interest-bearingliability,salesandcosts.Finallytheevaluatorestimatesthecompany’s businessvalue.Thebusinessvaluehereisestimatedwithsomerange.Intellectual propertyisevaluatedbasedonthebusinessvalue.Thissampleappliestherule-of-sum methodand,therefore,25%orone-thirdofbusinessvalueiscalculatedasarangeof valuegeneratedbyintellectualproperties.Thefinalchapter(GeneralEvaluation:Future Challenge)showsseveralchallengestobemade.

(3)IFRSManagementCommentaryispresentedundertheIFRSpracticestatement No.1.Managementcommentaryisexplainedasanarrativereportthatprovidesa contextwithinwhichtointerpretthefinancialposition,financialperformanceandcash flowsofanentity(IASB2010,par.IN3).Informationprovidedexplainsmanagement’s view not only about what has happened, including both positive and negative circumstances,butalsowhyithashappenedandwhattheimplicationsareforthe entity’sfuture(IASB2010,par.9),whichinclude(a)thenatureofthebusiness, (b) management’sobjectivesanditsstrategiesformeetingthoseobjectives,(c)theentity’s mostsignificantresources,risksandrelationships,(d)theresultsofoperationsand prospectsand(e)thecriticalperformancemeasuresandindicatorsthatmanagement usestoevaluatetheentity’sperformanceagainststatedobjectives(IASB2010,par.24).

(4)EUrequirescompanies,exceptSMEs,initsjurisdictiontoprepareadisclosure documentcalledManagementReport.EUsates“theManagementReportshallinclude (omitted)abalancedandcomprehensiveanalysisofthedevelopmentandperformance oftheundertaking’sbusinessandofitsposition,consistentwiththesizeandcomplexity ofthebusiness.Totheextentnecessaryforanunderstandingoftheundertaking’s development,performanceorposition,theanalysisshallincludebothfinancialand, whereappropriate,non-financialkeyperformanceindicatorsrelevanttotheparticular business,includinginformationrelatingtoenvironmentalandemployeematters.In providing the analysis, the Management Report shall, where appropriate, include referencesto,andadditionalexplanationsof,amountsreportedintheannualfinancial statements. The Management Report shall also give an indication of (a) the

undertaking's likely future development, (b) activities in the field of research and development(EU2013,pars.1-2)”.

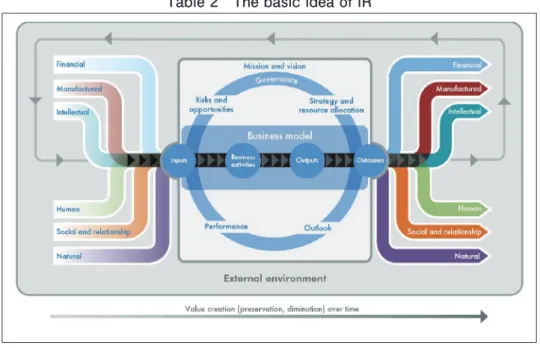

(5)IntegratedReporting(IR)ispromotedbyInternationalIntegratedReporting Council(IIRC).ThepurposeofIRisexplainedas“toexplaintoprovidersoffinancial capitalhowanorganizationcreatesavalueovertime.Itthereforecontainsrelevant information,bothfinancialandother(IIRC2013,par.1.7).”ThebasicconceptofIRisto expresshowthecompanycreatesavaluebyusing6kindsofcapitals.The6capitals comprisefinancialcapital,manufacturedcapital,intellectualcapital,humancapital,social andrelationshipcapitalandnaturalcapital(IIRC2013,par.2.10).Thefollowingcharts wellindicatethebasicideaofIR.

(6)IntangiblesReportingFrameworkisprovidedbyWorldIntellectualCapital/Assets Initiative (WICI). The purpose of the framework is explained as “to provide the definitions,theinterpretationsofthemostrelevantprinciples,andthestructureforthe reportingofintangibleresourcesthatarematerialforanorganization’svaluecreation processandtheircommunication tostakeholders fromtheperspective ofshowing businesssustainabilityovertime(WICI2016,p.8)”andthefeaturesareexplainedas“an integration,totheextentpossible,betweennarrativeinformationandquantitatively expressedinformationrepresentedasKeyPerformanceIndicators:KPI(numerical figures(metrics)relatedtocritical/materialfactorsofvaluecreationandwhichshould

Table 2 The basic idea of IR

(IIRC2013,par.2.20)

provideobjectiveevidenceofperformancetrendsbytrackingthemovertime)(WICI, 2016,p.20)”.

In addition to international efforts to construct a Narrative Method, individual researchersproposeseveralmodels.Lev=GuproposetoprepareaStrategicResource

&ConsequenceReport(Lev=Gu2016,p.135).Asshownitsname,thisreportindicates whatkindofresourceisusedinthebusinesstobevaluedandwhatconsequencesare derived as a result of business activities. IPs are, of course, treated as a part of resources.Thefollowingtable3conciselydepictsastructureofthereport(Lev=Gu 2016,p.143).

Everymodel/reportIcitedaboveasNarrativeMethodshavecommonfeatures.They can beeasily understood bychecking the following keywords. That is“business,”

“businessfeasibility,”“valuecreation,”“narrative,”“management’sview,”“explain,”and soon.Inshort,theseareadevisebywhichthemanagementisabletoexplainhowhis/

herbusinesshascreatedavalue.AlthoughanIPisregardedasaresource,withinthe business,tocreatethevalue,thevalueisbelievedtobegeneratedbyabusinessasa wholenotsolelybytheIP.

Table 3 Strategic Resource & Consequence Report

(Lev=Gu2016,p.143)

Iagreewithacommonideawhichisreflectedintheabovedevises.Tobesure,IP doesn’tautomaticallygeneratecashflowsatstand-alonebasis.IPgeneratescashflows forthefirsttimewhenitisutilizedinthebusinesstogetherwithotherresourcesor capitals.Therefore,weareessentiallynotabletoevaluateanIPatstand-alone-basis.Or

itmightbesaidthatweshouldnotdoso,evenifwecandoso.Thatiswhy,afocusof IPvaluationresearchmighthaveshiftedfromDICMtotheNarrativeMethodsduring thelast10years.

Thefollowingtable4showsacomparisonbetweenDICMandtheNarrativeMethod.

Table 4 A comparison between DICM and the Narrative Method

[DICM] [Narrative Method]

Business as a whole

Tangible

IP

Human Capital

Structural Capital

Relational Capital

Generating Cash Flows IP

Generating Cash Flows

Evaluation

AdisclosureofIPvalueundertheNarrativeMethodmightbeunderstoodasina categoryofso-called“DisclosureofNon-FinancialInformation.”Suchadisclosuresystem maybedeeplystudiedinthefutureandIbelieveaprogresseddisclosuremodelwill provideourbusinesssocietywithveryusefulinformationregardingIPvalue.

However,IPvaluationareahasanurgentproblemthatcannotbesolvedbythe NarrativeMethod.Thenextsectiontreatsthistopic.

Ⅲ.Recognizing IPs on the Balance Sheet

ThemostbasicconcerninfinancialaccountingarearegardingIPsisbelievedtobe recognizingitonthebalancesheet.Afundamentalpremisewehavetoconfirmatfirst, althoughitisextremelyprimitiveone,iswehavetograspthevalueofIPatmonetary amount.Furthermore,theamountshouldbeasoleamount.Inotherwords,several evaluated amounts in a range are not available. For example, JPO’s IP business valuationReport,statedearlier,providesseveralIPvaluesinarange,butsucharange cannotbestatedonthebalancesheet.

Then,theamounthastobespecifiedforeachIP.ManyNarrativeMethods,basedon

thebusinessvalue,evaluateandshowtheIPvaluesasagroup.Inacaseofpatents, suchagroupissometimesreferredas“apatentportfolio,”andinfactthecashflows are being generated by utilize the patent portfolio. Furthermore, some Narrative Methods evaluate the IPvalue with incorporating several surrounding capitals in additiontothepatentportfolio.

However,sucha“groupevaluation”isnotallowedonthebalancesheet,unfortunately.

Onlyitemswhichhavehadbeenidentifiedindividuallycanberecordedonthebalance sheetandtheamountshouldbeanaccumulatedamountofeachassetvaluedatstand- alonebasis.

Assumeacaseofrecordingmachinesasoneoftheaccountswithinthetangibleasset category.Theamountofmachinesappearedonthebalancesheetis,ofcourse,an aggregatedamountofanymachinestheentityowns.Theamountsofeachmachine includingtheirhistoricalcost,accumulateddepreciation,orrecoverableamount,arefully- listedup(recorded)and/orproperlymanagedonaledgerformachines.Theaggregated amountofmachinesis,needlesstosay,separatedfromtheamountsofrelatedassetsor capitalsneededtobeutilizedjointlytogeneratecashflowsfromthemachine.

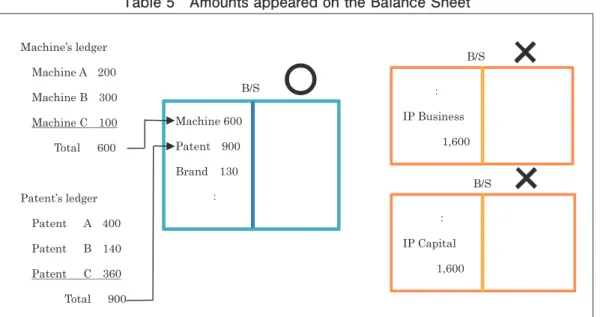

Assameasacaseofmachines,theamountofIPappearedonthebalancesheet shouldbeanaggregatedamountofeachcomprisingIPandtheamountshouldhave beendispatchedfromtherelatedassetsand/orcapitals.Thefollowingtable5showsa relationbetweenamountsinledgersandtheamountofeachassetonthebalancesheet.

Table 5 Amounts appeared on the Balance Sheet

Machine’s ledger Machine A 200 Machine B 300 Machine C 100

Total 600

Patent’s ledger Patent A 400 Patent B 140 Patent C 360 Total 900

B/S B/S B/S

Machine 600 Patent 900 Brand 130

㸸

㸸 IP Business

1,600

㸸 IP Capital

1,600

ࠐ

ࠐ

Whyshouldeachitemonthebalancesheetbebasedontheamountsineachasset’s ledger?Thereasonis,historically,thatmanagement’sassertionsuchasanexistenceof all assets (completeness) and an appropriateness of their evaluation are strictly examinedbyanauditorandeachitemintheledgeristreatedasatargetofthe auditingandvouched(Montgomery1912,pp.82-84).

Asaresultofaboveconsiderations,IbelievethatanevaluationbasedontheDICMis indispensableforallIPs,atleast,fromthefinancialaccountingperspective.Although,as mentionedearlier,afocusofdebatesonIPisshiftingtotheNarrativeMethod,thisfact meanswearecontinuetoberequiredtoseekabettervaluationtechniquesunderthe DICM,evenifsuchastanceisridiculedas“superficial.”

Ⅳ.IPs and Goodwill

AnotherevidenceforanecessityofDICMalsocomesfromtheaccountingforasset acquisition, includinga business combination.Therearebroadlytwocaseswhich requireustorecognizetheIPsasassetsonthebalancesheet.Theformercaseoccurs whenacompanyacquirestheIPsfromanothercompanyasasimplepurchaseor throughabusinesscombination.Inthesimplepurchase,theacquirershouldrecognize theIPsatanamountpaidforthetransaction.Forexample,iftheacquirerpays$100 milliontopurchaseapatent,itisrecognizedonthebalancesheetatsuchamount.This accountingtreatmentisbelievedtobeconsistentwithhistoricalcostprincipleand, therefore,noparticularconcernwouldberaised.

However,severalproblemsoccurwhentheIPsareacquiredthoroughabusiness combination5. A basic accounting method for business combination had been the purchasemethodforalongtimeintheUnitedStates.Thisisstillasurvivingmethod inJapan.

Underthepurchasemethod,aconsiderationpaidisallocatedtoassetsacquiredbased ontheirfairvalues.AlthoughtheIPshadbeenrecognizedattheirfairvalueunderthe purchasemethod,ithadbeenjustaresultofcostallocation.SFAS141(Purchase method)stated“thesameaccountingprinciplesshallapplyindeterminingthecostof assetsacquiredindividually,thoseacquiredinagroup,andthoseacquiredinabusiness combination(FASB2001,par.20)”.

5Formoredetail,Iamverygladifyousee(Kaneta2019).

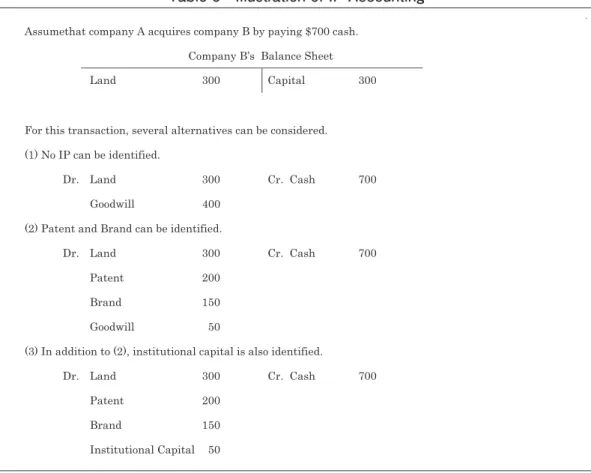

Table 6 Illustration of IP Accounting

Assumethat company A acquires company B by paying $700 cash.

Company B’s Balance Sheet

Land 300 Capital 300

For this transaction, several alternatives can be considered.

(1) No IP can be identified.

Dr. Land 300 Cr. Cash 700

Goodwill 400

(2) Patent and Brand can be identified.

Dr. Land 300 Cr. Cash 700

Patent 200

Brand 150

Goodwill 50

(3) In addition to (2), institutional capital is also identified.

Dr. Land 300 Cr. Cash 700

Patent 200

Brand 150

Institutional Capital 50

Table6aboveshowsseveralalternativesregardingtherecognitionofIPsunderthe purchasemethod.Accountantswhoarepersistenttoconservatismmaypreferthe accountingmethoddescribedin(1).Thosewhobelievetherecognitionofintellectual propertyisnecessarymayprefertheaccountingmethoddescribedin(2).Thosewho believetherecognitionofintellectualcapitalisalsonecessarymayprefertheaccounting methoddescribedin(3).Anyway,thetotalamountsofassetsacquiredhavealready decidedbytheconsideration($700cashinthistable)and,therefore,therecognitionof IPmaybecarriedoutwithinthescopeofconsideration.Consideringfromtheview pointofIPaccounting,itmaybesaidthealternative(2)isbetterthan(1)andalternative (3)isbetterthan(2).Becausethetotalamountofassetsacquirediscoincidewiththe considerationpaidanyway,therecognitionandevaluationofIPisenoughifcarriedout as much as possible within the amount of consideration. Some argue that under historicalaccountingrules,thedistinctionbetweengoodwillandintangibleassetshad beenlessimportantbecausebothassetswereexpensedanyway(Donohue=Vallario

2002,p.75).

However,suchabeliefmaybeturnedoveronceyouencounterintoafollowingcase.

ThatisthecaseofacquisitionofShirebyTakedaPharmaceuticalCompany.Takeda purchasedallsharesissuedbyShireattheamountofaround$60billion.Theamountis thehighestinJapaneseM&Ahistory.ConsideringfromtheIPaccountingperspective, themostcrucialpointinthiscaseishowdidTakedaevaluatenetassetsacquiredfrom Shire(OrhowdidTakedaallocatetheconsiderationintoeachnetassetsacquired).

Thefollowingtable7showsthebookvalueofnetassetsacquiredfromShireand howdidTakedaevaluatethem6.Theamountofcashanditsequivalentsareabout110%

up-appraised((2,271-1,072)/1072 × 100).Assame,receivablesare4.3%down-appraised, inventoriesare112%up-appraised,tangiblesare3.8%down-appraised,IPsare20%up- appraised,Othersare197%up-appraisedandliabilitiesare18%up-appraised.

Table 7 Net assets acquired from Shire.

$ million

Book Value*1 Evaluated*2 Book Value*1 Evaluated*2

Cash and Equiv.

Receivables Inventories Tangibles IPs Others

1,072 3,409 3,882 7,222 32,281 1,939

2,272 3,261 8,240 6,945 38,992 5,771

Liabilities 28,996 34,312

Total 49,809 65,483

*1 This means the book value at Shire before the acquisition. *2 This means the amounts evaluated by Takeda.

WecanunderstandafactthatTakedatriedtodetermineaproperamountforthese assetsandliabilities.Evenso,ahugeamountofgoodwillwaseventuallyrecordedas showninthefollowingjournalentry.

6ThisarticletranslatesanamountatJapaneseyenintoUSDatarateof1$=¥100.

Dr.

CashandEquiv. 2,272

Cr.

Liabilities 34,312

Receivables 3,261 CashandOtherConsiderations7 62,133

Inventories 8,240

Tangibles 6,945

IPs 38,992

Others 5,771

Goodwill 30,964

Howdoyoufeelaboutthegoodwillofover$30billion?Althoughsuchahugeamount itselfissurprising,thisfactisbelievedtoberaisingmanyaccountingconcerns.Ifacost allocationhasbeenproperlycarriedout,thegoodwilldefinitelyrepresentseithera synergyeffectoragoingconcernvalueorboth8.Butdoyoubelievethattheseelements havereachedto$30billion?

ThereisaninterestingfactthatShirehad15candidatedrugsinthethirdphaseof clinicaltrial,immediatebeforetheacquisition.Consideringthisfact,morevaluemight havebeenallocatedtoIPssuchaspatentedornon-patentedtechnologyandin-process R&D.ButTakedacouldnotdoso.ItmeanshowdifficulttheIPvaluationis.Ifthe properallocation,basedonanIPvaluationmodel,hasimplemented,suchvaluesnot onlycanberecognizedandshowedinappropriateaccountsbutalsotobeassociated withthematchingandrealizationprinciples(Jarrett2017,p.2).Becauseoneofthe fundamentalrolesofaccountingiscalculatingproperperiodicearningsbasedonthe matching and realization principles, a proper and complete cost allocation (or an evaluationbasedonfairvalues)isdefinitelyrequired.Ibelievegoodwillof$30billion willnotachieveapropermatchinganyway.

Asubsequentaccountingforgoodwillisalsorelatedtothistopic.UndertheU.S.

GAAPandIFRS,goodwillissubsequentlyaccountedforbyapplyingtheimpairment methodnotthesystematicamortizationmethod(FASB2015,Topic350-20-35;IASC 1998,par.80).Anexpenseisrecognizedonlywhenthevalueofgoodwilldeclinesunder theimpairmentmethod,whichistheoreticallysupportedbecauseasynergyeffectand/

oragoingconcernvaluewillbemaintainedunlesssomeunexpectedeventtriggersa declineofthevalue.Itmeansthatanevaluatingeveryidentifiableassetandliabilities basedonapropercostallocation(oraproperevaluationattheirfairvalues)isthe decisivepremisefortheimpairmentmethod.Ifsomevalueswhichshouldhavebeen

7Considerationsinthiscasewerecashandshares.

8 As you know,accountingstandardrequiresan analysisfor componentswithinthe difference betweennetassetsacquiredandtheconsiderationspaid.Asaresultoftheanalysis,severalassetsand liabilitiesarerecognizedasappropriateaccountsandtheremainingamountisrecognizedasgoodwill, whichrepresentssynergyeffectandgoingconcernvalue(FASB2001,par.B102).

identifiedasaspecificassetareincorporatedintheamountofgoodwill,thepremiseof impairmentmethodwillbeblownaway.Therefore,Ibelievethatwehavetoestablish avaluationmodelforIPsbasedontheDICM.

Ⅴ.IPs and a Gain on a Bargain Purchase

Asyouknow,theacquisitionmethodforbusinesscombinationswasintroducedby SFAS141(R)issuedbytheFinancialAccountingStandardBoard(FASB)in2007.It replacedthepurchasemethodofaccountingforbusinesscombinations.Thisstatement hadbeencodifiedlaterastheASC805andhadbeenineffectsincethefiscalyear beginningafterDecember15,2008.Ibelievethattheacquisitionmethodhasbrought severaldramaticchangesintherecognitionofIPs9.

Undertheacquisitionmethod,“Theacquirershallmeasuretheidentifiableassets acquiredandliabilitiesassumed,andanynon-controllinginterestsintheacquireeat theiracquisition-datefairvalues(FASB2007,par.20)”.Itmeansthatidentifiableassets andliabilitieshavetobemeasuredindependently.Inotherwords,theconsideration involved is irrelevant to measure and record the identifiable assets. Therefore, researchersfrequentlyregardtheacquisitionmethodasafull-fair-valueapproach(i.e.

Davis = Largay2008,p.27).

Suchfairvaluesshouldbemeasuredbasedonamarketparticipantperspective(exit values). This means that the fair value should not reflect the intent or plans the acquirerhasatthedateofacquisition.Theexitvaluesmeasuredundertheacquisition methodhaveameritthatthesevaluesindicatethefairvaluesforpublic.Someargue, however,thatthistreatmentallowstheassetswhichwillbeabandonedafterthe combinationtobecapitalizedattheiracquisitiondatefairvaluesanditprovidessome misleadinginformationtoinvestors(John2007,p.2).

So-callednegativegoodwillshouldberecognizedasanextraordinarygainatthedate ofacquisition.Thismaybeacceptablebecausesuchagainisaresultofrecordingthe net assets at their fair values. However, the many comment letters to the FASB expressedsomeopposition,becausethistreatmentleadsaresultofrecordingaprofit oragainwhenthecompanyimplementedapurchasetransaction(FASB2006,par.46).

Anyway,itcanbesaidthattheimportanceand/orconsequencesofvaluingtheIPs aredramaticallyincreasedcomparedwiththeeraofpurchasemethod.

9Formoredetail,Iamverygladifyousee(Kaneta2020).

Assumethatthefairvalueofacquiredassetsintable6areland$320,patent$240, andbrand280.Theseamountsaredeterminedseparatelyfromtheconsiderationof

$700.Ajournalentryforthistransactionisasfollows.

Dr. Land 320

Cr. Cash 700

Patent 240 Gainonabargainpurchase 140

Brand 280

ThisindicatesthattheIPvaluationisveryimportantundertheacquisitionmethod becausearesultofvaluationdeterminesanearningorloss.Needlesstosay,theamount ofearningsorlossaffecttoavarietyofstakeholders,weshouldpaycloseattentionto thispattern.Thefollowingtable8showsalistofcasesinwhichagainonabargain purchasehasbeenrecognizedinForm10-KssubmittedintheperiodofSeptember throughDecemberin2019.

Ifound5casesinwhichagainonabargainpurchasewasrecognizedintheirincome statements. Percentages of the gain on a bargain purchase to the amount of considerationsforeachcaseare23%(Case(1)),40%(Case(2)),1,191%(Case(3)),18%

(Case(4)),and66%(Case(5)),respectively.Thepercentagesaregenerallynotlowand thenumberincase(3)isextremelyhigh.Itmeansanimpactofthegainonabargain purchaseisconsiderable.

SeveralIPsarerecognizedineachcase.Item(f)representsthesentencesappearedin eachform10-KrelatedtoIPvaluation.Wecanunderstandfromthesentencesthat eachacquirerhavemanagedtoevaluatethem.Item(e)representsanimportanceofIP valuationagainstthegainonabargainpurchase.Althoughthereisvariationamongthe numberofpercentage,IPvaluationisbelievedtohaveconsiderableimportanceatleast incaseof(1),(2),and(4).

Therefore,IbelievethatconstructingareasonableIPvaluationmodelunderthe DICMisurgentintheeraofacquisitionmethod.

Table 8 Cases a gain on bargain purchase is recognized

Case(1)GeneralFinance(Sep.12)(a)Considerations:$7,695,000 (b)Fairvalueofnetassetsacquired:$9,462,000

(c)IPsamongthem:Non-CompeteAgreement$74,000,CustomerList/Relationship$734,000 (d)Gainonbargainpurchase:$1,767,000 (e)(c)IPvalue/(d)Gain:46%

(f)HowtoevaluatetheIPs:

Determiningthefairvalueofintangibleassetsinvolvestheuseofsignificantestimatesand assumptions,whichtheCompanybelievesarereasonable,butareuncertainandsubjectto changesinmarketconditions.

Case(2)PredictiveTechnology(Sep.30)

(a)Considerations:$917,511 (b)Fairvalueofnetassetsacquired:$1,281,187 (c)IPsamongthem:CLIARegulatoryLicenses$295,000,CustomerRelationships$16,000 (d)Gainonbargainpurchase:$363,676 (e)(c)IPvalue/(d)Gain:86%

(f)HowtoevaluatetheIPs:

CLIAlicenseswereestimatedusingtheexcessearningsmethod,usingadiscountrateof 22%,whichisbasedontheestimatedinternalrateofreturn.Theprojectedcashflowswere basedonkeyassumptionssuchasestimatesofrevenuesandoperatingprofits.

Case(3)RennovaHealth(Oct.21)

(a)Considerations:$635,096 (b)Fairvalueofnetassetsacquired:$8,201,766 (c)IPsamongthem:CertificateofNeed$259,443,Non-Compete$245,363 (d)Gainonbargainpurchase:$7,566,670 (e)(c)IPvalue/(d)Gain:7%

(f)HowtoevaluatetheIPs:

Considerablemanagementjudgmentisnecessarytoestimatediscountedfuturecashflows.

Accordingly,actualresultscouldvarysignificantlyfromsuchestimates.

Case(4)Atkone(Nov.22)

(a)Considerations:$43,041,000 (b)Fairvalueofnetassetsacquired:$50,425,000 (c)IPsamongthem:CustomerRelationship$15,400,000,others$1,000,000

(d)Gainonbargainpurchase:$7,384,000 (e)(c)IPvalue/(d)Gain:222%

(f)HowtoevaluatetheIPs:Notmentioned.

Case(5)INTLFCStone(Dec.12)

(a)Considerations:$8,200,000 (b)Fairvalueofnetassetsacquired:$13,600,000 (c)IPsamongthem:IPisincludedamongothers$700,000

(d)Gainonbargainpurchase:$5,400,000 (e)(c)IPvalue/(d)Gain:13%

(f)HowtoevaluatetheIPs:

TheCompanyacquiredcertainidentifiableintangibleassets,includingwebsitedomainnames andinternallydevelopedsoftware.TheCompanyhasengagedathird-partyvaluationspecialist toassistwiththevaluationoftheseacquiredintangibleassets.

Ⅵ.What is a fatal problem in the DICM?

ManyIPvaluationmodelshavebeenadvocatedsofar.Sveibysaysthereare42 modelsasof2010and13modelsamongthemarebasedontheDICM(Sveiby2010, pp.1-8).However,itisfrequentlysaidthatnoneofthepublishedmethodshasbecomea commonlyusedmethodworldwide(Pastor2017,p.388).

Themethodswell-knownaswithinacategoryofDICMincludemulti-periodexcess earing method, relief fromroyalty method, simulation method, sensitivity method, technologyfactormethodandrealoptionmethod.Thefollowingtable9summarizesthe featuresofthesemethods.

Table 9 several methods within a DICM category

(1)Multi-PeriodExcessEaringmethod(MPEE)ThismethodstartswithderivingrevenuesforsubjectIP.Then,allrelatedexpensesarededucted fromtheexpectedrevenuestograspaprofitgeneratedfromtheIP.Bysubtracting,fromthatprofit, returnsonfixedassets,workingcapital,assembledworkforceandotherIPs,wecangraspthe excessearningsfromexistingtechnology.

(APEC2018,pp.20-21)(Radu2014,pp.355-356)

(2)RelieffromRoyaltymethod(RfR)

Thismethoddiscountshypotheticalfutureroyaltypayments.Ifacompanydidn’tpossessthe subjectIP,thecompanymustmakearoyaltypayment.Apresentvalueofcashflowsgenerated fromsuchapaymentisseemedequivalentwithavalueofsubjectIP.Thehypotheticalfuture royaltywillvarydependingonfuturesalesthecompanycanachieve.Therefore,aprojectionof futurerevenuesandcostsisindispensableassameasthemethodin(1).

(ICC2019,pp.15-16)

(3)Simulationmethod

Thismethodappliedasimulationanalysistoremoveuncertaintiesintheprojectedfuturerevenue andanyotherinputs.Inthesimulationmethodincludingthefamous“MonteCarlosimulation,”all variablesinavaluationmodelareadjustedatonceaccordingtoindividualprobabilitydistributions toproduceanoveralldistributionofpossiblevaluations.

(Pitkethly1997,p.9)

(4)Sensitivitymethod

Thismethodisappliedtoincorporatetheseveralprobabilitiesrelatedtofuturerevenuesand expensesintoavaluationmodel.Forexample,whentwovariablessuchasfuturesalesandmarket shareareestimated,severalpossibilitiesinbothvariablesaremultipliedandanaveragednumber resultingfromthiscalculationisadoptedasasingleestimation.

(Amram2005,p.70)。

(5)TechnologyFactormethod

This method evaluates the technology factor at first. The factor is set between 0 ~ 100%

consideringtheattributesofindividualtechnologycalculatedaccordingtoindustrialfeaturesand qualitativevaluations.Thefactorismultipliedbyrevenuesprojected.Elementstakenintoaccount forevaluatethetechnologyfactorincludecompletenessoftechnologydevelopment,extentofthe efforts needed for additional development (for commercialization), originality, probability of a replacement technology being developed, level of difficulty to create imitations, the phase of technologylifecycleandtechnologyexpandability. (APEC2017,pp.431-434)

(6)RealOptionmethods

Thismethodtreatsapatentasacalloptionandevaluatingitsvaluethoroughanoptionpricing model(Black=Sholesmodel).Theoptionpriceinjectedintotheblack=Scholesmodelisreplacedby thecosttoinitiateR&Dintherealoptionmethodhere,and,aswell,strikedateisreplacedbythe dayofproductlaunch,strikepriceisreplacedbyR&Dcostsincurredbyproductlaunchdate, respectively.Inadditiontosuchreplacements,thediscountedvalueoftotalpotentialearningsfrom

salesofthenewproductisneeded. (Stiroh1998,pp.21-25)

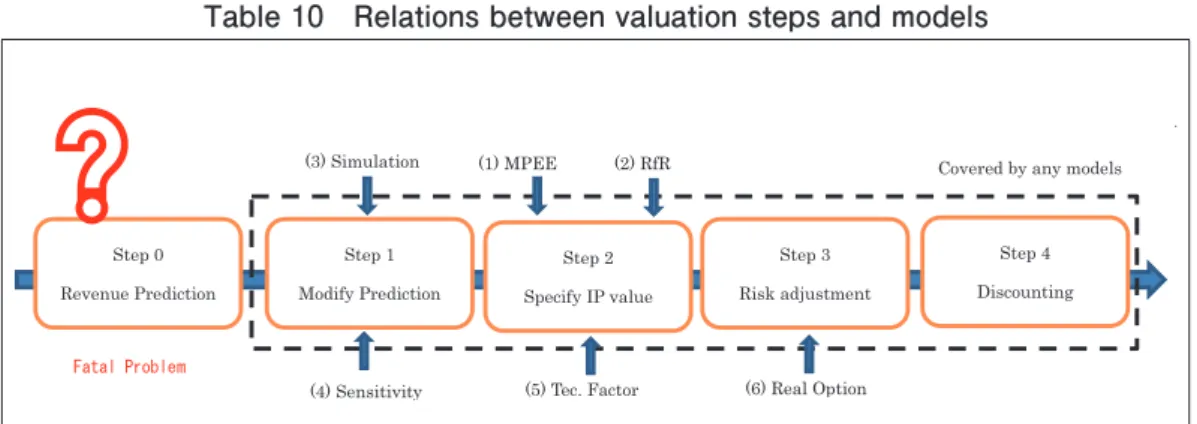

Asshownintable9,severalmethodshavebeendiscussedundertheDICM.Ibelieve thatthereisafundamentalandanabsolutepremiseregardinganymethods.Thatisa fact that future sales of products to which the subject IP is utilized have to be projected,anyway.Itisimportanttorecognizethatanymethodsabovedon’tgenerate thepredictionoffuturesalesitself,butsoleamendstheprediction.

IbelievethatthefollowingstepsaregenerallyrequiredtoevaluateanIPunderthe DICM.Thestep0predictsfuturesalesandexpensesgeneratedbyaproductinwhich the subject IP is applied.Step 1 modifiesthe amount predictedat step 1. Step 2 specifiesthepartthesubjectIPcontributes.Asaresultofstep2,tentativecashflows generatedbythesubjectIParedetermined.Step3adjuststhetentativecashflowsby reflectingrisksintothecashflows(oranappropriatediscountrateisdeterminedatthe step3).Asaresultofstep3,thecashflowsgeneratedbythesubjectIParedetermined.

Finallystep4discountsthecashflowsintoapresentvalue.Suchadiscountedvalueis theIPvalue,whichcanberecognizedasanassetonthebalancesheet.

Ibelievethatanymodelsabovestartsfromstep1.Nomodelprovidesatechniqueor aninsightrelatedtostep0thatseemstobethemostfundamentalandimportantstep inavaluationprocess.Table10belowshowstherelationsbetweenvaluationstepsand models.

Ibelievethefatalproblemlaysinthestep0.Manyinsistthesamethingssuchas“as with all income valuations the need to accurately forecast future cash flow is of paramountimportance(Chaplinsky2002,p.3),”“Projectingincomestream(CashFlow)is afundamentalrequirementinDCF(WIPO2004-2007,p.28),”and“”amajortaskin connectionwiththevaluationofsingleassetsisisolatingthespecificcashflowsthatcan becreditedtotheassettobeevaluated(Bader=Ruether2009,p.123)”.Notwithstanding thesefacts,itissurprisingthatnomodelprovidesanyanswertostep0.Whystep0is sodifficulttosolve?

Table 10 Relations between valuation steps and models

Step 0 Revenue Prediction

Step 1 Modify Prediction

Step 2 Specify IP value

Step 3 Risk adjustment

Step 4 Discounting (1) MPEE (2) RfR

(3) Simulation

(4) Sensitivity (5) Tec. Factor (6) Real Option

Covered by any models

❓

)DWDO3UREOHP

The answer may exist in a difficulty of future projection. Generally, the future projectioniscarriedoutbasedonhistoricalinformation.Assumeaweatherforecast.

Themeteorologicalagencydoesn’tforecasttomorrow’schanceofrainwithoutany evidences.Theyforecastitbasedonhowmanytimesweexperiencedraininthepast inacaseofsameairpressurepatternwithtomorrow.Asotherexamples,aprediction ofsharepricewouldbemadebasedonthesharepriceoftargetsharesinthepast.

Beforepurchasingahorsevotingticket,wearesupposedtoanalyzethepastrace recordsindetailforthetargethorse.

IsthereahistoryforIPs?TheanswermaybeYESforsomeIPsandmaybeNOfor others.Ibelievebrandsandcustomerlists/relationareexamplesofYESandpatents andtechnologyareexamplesofNO.Brandsare,forexample,constructedasaresultof providinghighqualityproducts/servicesforalongtime.Thatiswhyithasahistory.

Incontrast,apatentnewlydeveloped,forexample,isissuedsolelyfornewtechnologies which are qualified ashaving anovelty and progressiveness. Although there isa historyasR&Dactivities,thepatentasanassethasjustborne.Thatiswhyitdoesn’t haveahistory.ProjectionoffuturecanbecarriedoutforIPsofYESbasedonits history10.ButwecannotdosoforIPsofNO.

Anyway,wehavetoprojectfuturesalesofproducttoevaluateanIP.Forthat,aunit priceandsalesvolumehavetobeprojected.However,suchaprojectioncannotbe madeifwedon’thavesalesdataforpastperiod11.Itwillbecomehighlysubjectiveifwe

10JPOindicatesthescenariomethodwhichtranslateshistoricaldatatofutureprojection(JPO2017, p.45).

11Medicaldrugpatentsownedbypharmaceuticalcompaniesareexceptions.Futuresalesofmedical drugscanbeprojectedbyreferencetothedrugprice(InJapan,itisdeterminedbyGovernment)and thenumberofpatients.Thereforeseveralvaluationmodelsformedicaldrugpatentsarefrequently discussed.Amrammodel,KurumeUniversitymodel,andCrane=Dysonmodelareitsrepresentatives (Amarm2005),(Kaneta2011,pp.35-38)and(Crane=Dyson2009).

areforcedtoprojectthefuturesaleswithoutanyhistoricalsalesdata.Ibelievethat thisisareasonthatmanymodelsdon'tmentiontostep0.Andthisisthefatalproblem intheDICM.

Ⅶ.Conclusion

ThefocusofIPResearchhasbeensiftedfromtheDICMtotheNarrativeMethod especiallysince2010.AbackgroundoftheshiftisbelievedtobeinthefactthatanIP cannot be evaluated at stand-alone basis and many surrounding factors and supplementalassetsshouldbetakenintoaccount.ThestudyontheNarrativeMethod willprogressmoreinthefutureunderthebannerofthedisclosureofnon-financial information.

Evenso,IbelievethatweshouldneverabandonanefforttocapitalizetheIPsonthe balancesheetundertheDICM.Iamnotsayingitbasedonspiritualism.Rather,a capitalizationofanindividualIPundertheDICMisindispensabletocalculatethe properperiodicearningbasedonthematchingprinciple.Furthermore,anIPvalue capitalizedundertheacquisitionmethoddirectlyeffectsonthegainonabargain purchase.Thatiswhy,theDICMhastocontinuetobepursuedbyresearchers.

Anyway,theDICMhasbeensomuchcriticizedrecentlybecausenotonlyalackof reliablevaluationmodel,butalsothesubjectivityofamountcalculatedbyamodel.For example,“DisadvantagesoftheDCFmethodincluderelianceonsubjectivecashflow projectionswhich,particularlyinthecaseofindividualIPassets(ICC2019,p.17),”“The factremainsthattheresultsofitachievesarecompletelysubjectiveandunreliable (Mrsa2018,p.189),”“IncorporatingIPassetsonthebalancesheet,particularlythose assetswhosevaluehasnotbeentestedinthemarket(throughatransactionofsome sort),cangiveafalsepictureofthefinancialviabilityofabusiness(EC2014,p.36),”

“DependingonwhoisusingtheIP,thevaluemayvarysuchasfairmarketvaluefrom thestandpointofafinancialinvestor;acquisitionvalueforastrategicbuyer;fairvalue foranauditor;marketvalueforacompetitor;liquidationvalueforthebanker;andthe currentvaluefortheowner(APEC2018,p.25),”and“thevalueofIPassetsishighly contextual.Thevalue-in-usetooneownermaybeverydifferenttothevalue-in-useofa differentowner(EC2014,p.37)”.TheDICMissurroundedbytoughcriticismslikethis.

Asyoucansee,therearetwokeywordsinthecriticisms:subjectivityandvariability.

Themostidealanswerforthecriticismsistoconstructaperfectmodelunderthe DICMwhichenablestopredictfuturesaleswithobjectiveevidences.However,sucha

thingmaybeimpossible.Becauseeachmarketparticipanthashis/herownexpectations forthefuture,andthebusinessactivityismadebasedonsuchavarietyofexpectations, therecanneverbeasinglemodeltopredictfuturesalesofacompany.

Ifitistrue,analternativemaybeanestablishmentoftheoreticalbasetoacceptsuch subjectivity and variability. The accounting for other assets perhaps might be referenceableforthepurpose.

Forexample,apensionliabilityiscapitalizedonthebalancesheet.Theamountof pensionliabilityisdeterminedbasedonactuary’spredictions(Kiesoet.al2001,p.1127).

The prediction of the pension liability is heavily reliant upon a number of key assumptionsaboutthefuture(FRC2018,p.11).FRCshowsonepracticalcaseinwhich auditorstacklewithsubjectiveamount,saying“inmostcasestheauditorconsidered whethertheassumptionswerewithintheacceptablerangeandassessedwhetherthey wereattheoptimisticorpessimisticendofthisrange.Iftheassumptionswereoutside therange,theauditorwouldberequiredtochallengemanagementtobringtheir assumptionswithintherange(FRC2018,p.11)”.

Asfarasvariability,thebiggestproblemintheDICMisseemedtobeafactthatan IPdoesn’thaveafairvaluebuthaveavarietyofValue-in-Use.Tobesure,avalue-in- useofIPwillsomuchvarydependingonwhouseit.Butthesamethingcanbesaid fortangibleassetsthoughthedegreeofvariabilityissmall.Indetail,thevalue-in-useis differentfromthefairvalueforbothtangibleassetsandIPs.Becausethedifference betweentangibleassetsandIPsregardingthevariabilityisamatterofdegree,it shouldnotbeensomuchemphasized.And,infact,weapplyavalue-in-usefortangibles intheimpairmentaccounting(IASC1998(Revisedin2013),par.30).Needlesstosay,the value-in-useappliedforundertheimpairmentaccountingisatargetofauditing.

Anyway,thenextarticlewilldiscussit.

References

AcaciaTechnologyGroup(ATG),Acacia Research,initswebsite,2007.

Amram,M.,“TheChallengeofValuingPatentsandEarly-StageTechnologies,”Journal of Applied Corporate Finance,Vol.17No.2,2005.

APEC-Guide(IntellectualPropertyExpertsGroup:IPEG),TheGuidebookforSMEs’IP -BusinessCycle,APEC(Asia-PacificEconomicCooperation),2017.

APEC-Manual(IntellectualPropertyExpertsGroup:IPEG),Intellectual Property (IP) Valuation Manual: A Preliminary Guide, APEC (Asia-Pacific Economic

Cooperation),2018.

Bader,M.A.andF.Ruether,“StillaLongWaytoValue-BasedPatentValuation-the PatentValuationPracticesofErope’sTop500,”Les Nouvelles,June2009.

Blair,M.M.,andS.M.H.Wallman,Unseen Wealth, Report of the Brookings Task Force on Intangibles,BrookingsInstitutionPress,2001.

Chaplinsky, S., Methods of Intellectual Property Valuation, University of Virginia (UVA-F-1401),2002.

Crane,M.andR.A.Dyson“RisksinApplyingtheNewBusinessCombinationGuidance toIntangibleAssets,”The CPA Journal,January2009.

Davis, M. and J.A. LargayⅢ, “Consolidated Financial Statements-Major Changes Coming !,”The CPA Journal,February2008.

Donohue,J.J.andC.W.Vallario,“ANewScorecardforIntellectualProperty,”Journal of Accountancy,April2002.

EuropeanCommission(EC),Final Report from the Expert Group on Intellectual Property Valuation,EuropeanUnion(EU),2014.

EuropeanUnion(EU),“Directive2013/34/EUoftheEuropeanParliamentandofthe Councilof26June2013,”Official Journal of the European Union,2013.

FinancialAccountingStandardsBoard(FASB),Statements of Financial Accounting Standards No.141:Business Combinations,FASB,2001.

FinancialAccountingStandardsBoard(FASB),“ProposalforanewagendaProject:

DisclosureofInformationaboutIntangibleAssetsNotrecognizedinFinancial Statements,”FASB,2002.

FinancialAccountingStandardsBoard(FASB),Exposure Draft, Business Combinations Comment Letter Summary,FASB-IASB,2006.

FinancialAccountingStandardsBoard(FASB),Statements of Financial Accounting Standards No.141(Revised 2007): Business Combinations,FASB,2007.

FinancialAccountingStandardsBoard(FASB),Accounting Standards Codification (ASC),FASB2015.

FinancialReportingCouncil(FRC),The audit of defined benefit pension obligations:

Findings from 2017/18 audit quality reviews,FRC,2018.

Hirose,Y.ed.,Revolution of Financial Reporting,Chuokeizaisya,Inc.,2013.

International Accounting Standards Board (IASB), IFRS Practice Statement 1:

Management Commentary,IASB,2010.

International Accounting Standard Committee (IASC), International Accounting

Standard 36: Impairment of Assets,IASC,1998(Revisedin2013).

International Chamber of Commerce (ICC), Handbook on Valuation of Intellectual Property Assets,ICC,2019.

InternationalIntegratedReportingCouncil(IIRC),The international IR framwork, Integrated Reporting,InternationalIntegratedReportingCouncil,2013.

JapanPatentOffice(JPO),Valuation on Intellectual Property,JPO,2017.

Jarrett,J.E.,“IntellectualPropertyValuationandAccounting,”Intel Prop Rights,Vol.5 No.1,2017.

John,B.,“ChangingtheRules,”ELT (Powered by BNET.com),October2007.

Kaneta,K.,“AStudyonthePatentValuation(1)‐ AnalyzingSeveralFrameworks,”

Journal of Commerce Kurume University,Vol.17No.3,2011.

Kaneta, K., “Accounting for Intangible Assets: Widening Inconsistency in the Accounting Recognition between Acquired Intangible Assets and Internally- GeneratedIntangibleAssets,”Kurume University Business Research,No.4,2019.

Kaneta, K., “Caution against a Gain from Bargain Purchase,” Kurume University Business Research,No.5,2020.

Kieso,D.E.,Weygrandt,J.J.andT.D.Warfield,IntermediateAccountingTenthEdition, Wiley,2001.

Lev,B.,Intangible, Management, Measurement, and Reporting, BrookingsInstitution Press,2001.

Lev,B.,“RemarksontheMeasurement,Valuation,andReportingofIntangibleAssets,”

FRBNY Economic Policy Review,September,2003.

Lev,B.,andF.Gu,The End of Accounting and the path Forward for Investors and Managers,Wiley,2016.

METI,the Report of the Committee on Brand Valuation (Hirose Report),theMinistryof Economy,TradeandIndustrytheGovernmentofJapan,June,2002.

Montgomery,R.H.,Auditing Theory and Practice,RonaldPress,1912.

Rocha, M., Financial applications for brand valuation- Delivering value beyond the number,Interbrand,2014.

MrsaJ.,“ValuationofInternallyGeneratedIntangibleAssetsinAccounting,”Acta Economica Et Turistica,Vo.4No.2,2018.

Nakamura, L., “A Trillion Dollars a Year in Intangible Investment and the New Economy,”inHand=Lev ed. Intangible Assets, Values, Measures and Risks,Oxford UniversityPress,2003.

Pastor, D. et al., “Intangibles and methods for their valuation in financial terms:

Literaturereview,”Intangible Capital,Vol.13No.2,2017.

Pitkethly,R.,The Valuation of Patents: A review of patent valuation methods with consideration of option based methods and the potential for further research, Availableonlineathttp://users.ox.ac.uk(updatedon1997).

Radu,R.I.,Patent Evaluation for Accounting Registration- Strategic Tool for Business Development, a handout at International Conference “Risk in Contemporary Economy”on2014inGalati,Romania.

Stiroh,L.J.andR.T.Rapp,ModernMethodsfortheValuationofIntellectualProperty, (PLIPats.Copyrights,Trademarks,andLiteraryProp.Course,HandbookSeriesNo.

526),1998.

Sveiby,K.E.,Methods for Measuring Intangible Assets,Availableonlineathttp://sveiby.

com(updatedonApril2010).

U.S.PatentandTrademarkOffice(USPTO),Patent Statistics Chart 2018,USPTO,2018.

World Intellectual Capital/Assets Initiative (WICI), WICI Intangibles Reporting Framework,WICI,2016.

World Intellectual Property Organization (WIPO), IP Panorama- module11, IP Valuation,WIPO,2004-2007(CurrentlyavailableatwebsiteofWIPO).