DP RIETI Discussion Paper Series 03-E-002

Price Level Dynamics in a Liquidity Trap

WATANABE Tsutomu

RIETI

IWAMURA Mitsuru

Waseda University

The Research Institute of Economy, Trade and Industry

http://www.rieti.go.jp/en/

RIETI Discussion Paper Series 03-E-002

Price Level Dynamics in a Liquidity Trap

Mitsuru Iwamura and Tsutomu Watanabe

December 2002

Abstract

This paper studies the dynamic behavior of the general price level when the natural rate of interest declines substantially. Particular attention is paid to two constraints: the non-negativity constraint of nominal interest rates, and the government's intertemporal budget constraint. In a normal situation, nominal bond prices rise in response to the shock, which restores equilibrium. However, if the non-negativity constraint is binding, nominal bond prices cannot rise sufficiently. Equilibrium can then be restored only by a sufficient fall in the current price level. The required fall is greater when the maturity of government debt is shorter. To avoid deflation, the government must coordinate with the central bank by committing itself to reducing the current and future primary surplus.

P r ice L evel D y nam ics in a L iqui dit y Tr ap

not

not

any

not

, , ,

,

t

not

© ª £ ¤

and

real

,

NB NB NB NB NB NB

NB NB

NB NB NB NB NB

NB

0.000 0.002 0.004 0.006 0.008 0.010

-10 0 10 20 30 40 50 60 70 80 90 100

0.000 0.002 0.004 0.006 0.008 0.010 0.012

-10 0 10 20 30 40 50 60 70 80 90 100

Optimal path Taylor rule

-0.060 -0.050 -0.040 -0.030 -0.020 -0.010 0.000 0.010

-10 0 10 20 30 40 50 60 70 80 90 100

Optimal path Taylor rule

Figure 1

Optimal responses when the natural rate of interest stays above zero

ˆ 1

ˆ − −

j

j P

P 1

ˆ , + j

Qj 1

ˆ , + j

Dj

0.000 0.002 0.004 0.006 0.008 0.010 0.012 0.014 0.016

-10 0 10 20 30 40 50 60 70 80 90 100

0.000 0.002 0.004 0.006 0.008 0.010 0.012

-10 0 10 20 30 40 50 60 70 80 90 100

Optimal path Taylor rule

-0.110 -0.090 -0.070 -0.050 -0.030 -0.010 0.010

-10 0 10 20 30 40 50 60 70 80 90 100

Optimal path Taylor rule

Figure 2

Optimal responses when the natural rate of interest falls below zero

ˆ 1

ˆ − −

j

j P

P 1

ˆ , + j

Qj 1

ˆ , + j

Dj

0.000 0.002 0.004 0.006 0.008 0.010 0.012

-10 0 10 20 30 40 50 60 70 80 90 100

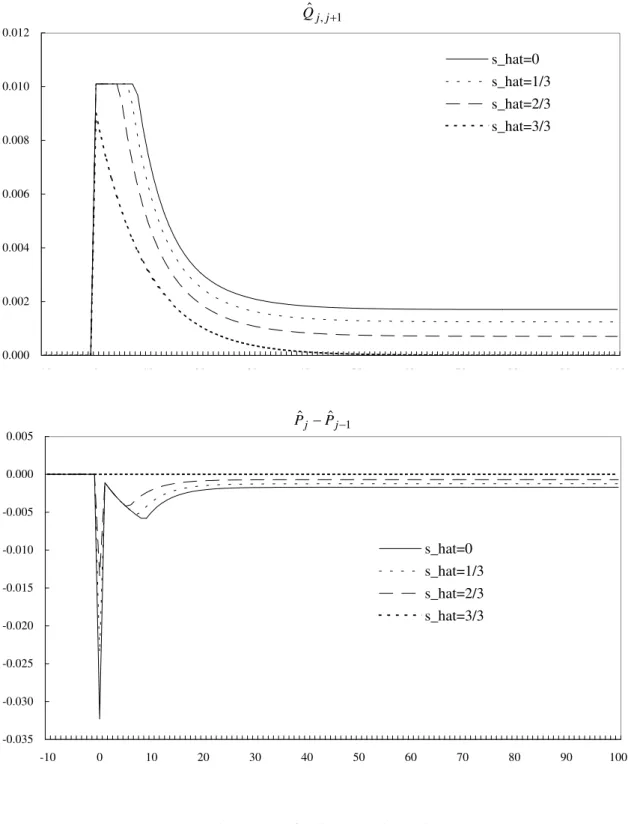

s_hat=0 s_hat=1/3 s_hat=2/3 s_hat=3/3

Figure 3 Optimal policy mix

-0.035 -0.030 -0.025 -0.020 -0.015 -0.010 -0.005 0.000 0.005

-10 0 10 20 30 40 50 60 70 80 90 100

s_hat=0 s_hat=1/3 s_hat=2/3 s_hat=3/3 ˆ 1

ˆj −Pj−

P 1

ˆ , + j

Qj