This study examined the cross-regional impacts of renewable energy production in Tohoku on the Tokyo electricity spot market. Specifically, our results confirm the cross-regional impact of the price stabilization of renewable energy generation in Tohoku. Our objective is to examine the indirect impact of solar and wind power generation in Tohoku on domestic price and volatility in the Tokyo electricity spot market.

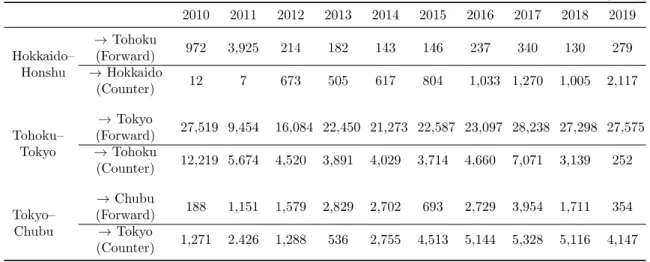

For this reason, we focus on these areas to study the inter-regional impacts of renewable energy generation on the electricity market. A traditional two-stage least squares (2SLS) framework was used to investigate the cross-regional impact of Tohoku's renewable energy generation on Tokyo's spot market. The second phase estimates the inter-regional impact of Tohoku's renewable energy generation on the spot price in Tokyo through its impact on electricity transmission between the two regions.

Sun(Tohoku)t and Wind(Tohoku)t are positive and statistically significant in columns (2)–(3), meaning that increasing renewable power generation in Tohoku also increases electricity transmission from Tohoku to Tokyo. The regression results on the impact of renewable power generation on the electricity pot market in Tokyo are presented in Table 4. 𝑛𝑠𝑚𝑖𝑠𝑠𝑖𝑜𝑛(𝑊𝑖𝑛𝑑)̂ 𝑡 is negative and statistically significant in columns (2) and (3) , which means that increasing renewable power generation in Tohoku can also help lower the electricity spot price in Tokyo's spot market.

The results suggest that a 1% increase in the inter-regional impacts of solar and wind power generation in Tohoku leads to an increase of 0.013% and 0.003%.

Realized Volatility

In summary, the estimation results of the second stage model suggest that both local renewable energy generation and renewable energy transmitted from Tohoku through the inter-regional interconnection lines can help reduce the spot electricity price in Tokyo. Furthermore, the results indicate that the cross-regional impact of wind power generation on price decline was greater than that of solar power generation during peak hours, while opposite effects were found during off-peak hours. The coefficients of 𝑆𝑜𝑙𝑎𝑟(𝑇𝑜𝑘𝑦𝑜)𝑑 are positive and statistically significant in columns (2) and (3), suggesting that local solar power generation leads to an increase in realized volatility in the Tokyo market.

For example, the coefficient is 0.044 for Solar(Tokyo)d in column (3), suggesting that a 1% increase in local solar production leads to a 0.044% increase in realized volatility. This result is consistent with Rintamäki et al. 2019), namely that renewable electricity production increases the realized volatility on the local electricity spot market. These results show that increasing the renewable energy transmitted from Tohoku reduces the realized volatility in the Tokyo spot market.

In particular, a 1% increase in the indirect impacts of Tohoku's solar and wind power generation induces a decrease of 0.034% and 0.019%, respectively, in the change in realized volatility13. TransImpactd is positive and statistically significant in columns (3), suggesting that the non-renewable electricity transmission from Tohoku to Tokyo leads to an increase in realized volatility in the Tokyo spot market. Our results show opposite effects of local and transmitted renewable energy on realized volatility in Tokyo.

The coefficients of solar (Tohoku)d and wind(Tohoku)d in Table 7 suggest that the transmitted energy generation by Tohoku can be varied with changes in electricity demand in Tokyo. The results suggest that local renewable energy generation increases realized volatility during the day and off-peak periods. Specifically, a 1% increase in solar and wind power generation leads to a 0.034% and 0.012% increase in realized volatility in the Tokyo spot electricity market, respectively.

For example, a 1% increase in solar and wind power transmitted from Tohoku leads to a 0.018% and 0.010% decrease in realized off-peak volatility, respectively15. Conversely, the insignificant coefficients of the renewable energy production indicators presented in column (4) in Table 8 show that both local and transmitted renewable energy do not exert an impact on the long-run volatility. These results on the realized volatility in different periods show that both the local production of renewable energy and the transmitted one affect the realized volatility during the period with lower electricity demand17.

Conclusions

The renewable power suppliers were not incentivized by the FIT scheme to increase production during the period with higher electricity demand (METI, 2020b). This result complements the findings of Schmidt et al. 2013) that FIT does not provide an incentive to match electricity production with the marginal cost of electricity production. The actual marginal cost during off-peak times was higher, and during off-peak times it was below average.

High marginal cost power plants are built to operate only during peak periods, while there is significant unused capacity during off-peak periods (Pikk and Viiding, 2013). Suppliers of renewable electricity tend to trade during periods of lower demand to avoid the higher marginal costs and therefore higher financial risk during peak times. Implementing the feed-in premiums (FIP) scheme can help facilitate demand-driven power supply, as the premium that producers receive is based on the market price (Marques et al., 2019).

Furthermore, the FIP is considered to provide an incentive to better match renewable power generation with marginal production costs. In fact, to achieve the carbon neutral goal for 2050, the sliding FIP system will be implemented in the Japanese market from April 2022 (METI, 2021). The government expects that renewable power producers will be incentivized to respond based on market price signals once the FIT is replaced with the FIP.

However, the government must also be careful that the FIP inhibits investment in renewable energy technologies18. In addition, we suggest that increased use of aggregator services may increase the stability of renewable energy production and thus lead to further price reduction effects during peak periods. 18 Du and Ma (2021) discuss the implementation of the FIP in Germany and state that the FIP has achieved its goal of promoting market integration of wind energy, but inhibits investment in solar energy technologies in Germany.

Acknowledgement

An Empirical Study on Japan’s Electricity Spot Market”, Discussion Paper No.17, Research Project on Renewable Energy Economics, Kyoto University. The impact of feed-in and capacity policies on electricity generation from renewable energy sources in Spain. Home, Council, Expanded Resources and Energy Research, Electricity and Gas Sector, Renewable Energy Promotion and Electricity Network.https://www.meti.go.jp/shingikai/enecho/denryoku_gas/saisei_kano/pdf/022_02_00.

Electricity Supply Outlook - Demand and Interregional Connections: Actuals for Fiscal Year 2019. Organization for the Interregional Coordination of Transmission Operators, English, Information Disclosure, Forecast for Electricity Supply - Demand and Interregional Connections. Where the Wind Blows: Assessing the Effect of Fixed and Premium Purchase Prices on the Spatial Diversification of Wind Turbines.

Trend analyzes of small and medium hydropower development after the FIT scheme introduced in Japan. The merit-order effect: a detailed analysis of the price effect of renewable electricity generation on spot market prices in Germany. The Impact of Wind Generation on Spot Electricity Market Price Levels and Variance: The Texas Experience.