西 南 交 通 大 学 学 报

第 55 卷 第 5 期

2020 年 10 月

JOURNAL OF SOUTHWEST JIAOTONG UNIVERSITY

Vol. 55 No. 5

Oct. 2020

ISSN: 0258-2724 DOI:10.35741/issn.0258-2724.55.5.32

Research article Economics

T

HE

A

PPLICATION OF

A

CTIVITY

-B

ASED

C

OSTING FOR

P

UBLIC

H

OSPITAL

S

ECTOR

S

USTAINABILITY

基于活动的成本在公共医院可持续性中的应用

Somnuk Aujirapongpan a, *, Watcharawat Promma a, *, Pornpun Theinsathid a, Sirichai Deelers b, Suchavadee Meechai a

a School of Management, Walailak University

Nakhon Si Thammarat,Thailand, asomnuk@wu.ac.th, pwatcha@wu.ac.th

b Faculty of Management Science, Silpakorn University

Petchaburi, Thailand

Received: June 6, 2020 ▪ Review: September 14, 2020 ▪ Accepted: October 9, 2020

This article is an open-access article distributed under the terms and conditions of the Creative Commons Attribution License (http://creativecommons.org/licenses/by/4.0)

Abstract

The research objective is to analyse the cost by the application of Activity-Based Costing of the cancer treatment process at a Thai public hospital by comparing the cost of cancer treatment with the compensation received from the National Health Security Office to set sustainability policy. Historical data were collected from 698, 295 and 348 cases of patients with breast cancer, liver cancer and colorectal cancer, respectively, from 1 October 2017 to 30 September 2018 by creating a matrix of coefficients and constants.The results showed that the cost of breast cancer treatment included the costs of 5 activities: breast cancer surgery, radiation, chemotherapy, the use of anti-hormone drugs and the treatment at the targeted cancer. The costs for the treatment of liver cancer included the costs of 5 activities: liver cancer surgery, TACE, radiation, chemotherapy and the treatment at the targeted cancer.And the cost of the treatment of colorectal cancer included the costs of 3 activities: colon cancer surgery, radiation and the use of chemotherapy.The treatments were found that the cost calculated from the activity-based were higher than the compensation received from the National Health Security Office. The research data constitute useful information for executives involved in policy makingabout managing and resources allocation to be the most appropriate and cost-effectiveness for sustainability of public hospitals in Thailand.

Keywords: Thailand, Activity-Based Costing, Cancer Treatment Cost, Public Hospital, Healthcare

摘要 该研究目标是通过将癌症治疗的成本与国家卫生安全局制定的可持续性政策获得的赔偿金进

行比较,通过在泰国公立医院采用基于活动的成本进行癌症治疗过程的成本分析。通过建立系数 和常数矩阵,从 2017 年 10 月 1 日至 2018 年 9 月 30 日分别收集了 698 例 295、295 例和 348 例乳

腺癌,肝癌和大肠癌患者的历史数据,结果表明乳腺癌的成本癌症治疗包括五项活动的费用:乳 腺癌手术,放射线,化学疗法,抗激素药物的使用以及针对性癌症的治疗。肝癌的治疗费用包括 5 个活动的费用:肝癌手术,泰斯,放射线,化学疗法和针对性癌症的治疗;大肠癌的治疗费用包 括 3 个活动的费用:结肠癌手术,放射线和化学疗法的使用。治疗被发现,以活动为基础计算出 的费用要比国家卫生局收取的费用高。研究数据为参与管理和资源分配决策的高管提供了有用的 信息,这对于泰国公立医院的可持续发展是最合适和最具成本效益的。 关键词: 泰国,基于活动的成本核算,癌症治疗费用,公立医院,医疗保健

I.

I

NTRODUCTIONHealth care spending has risen steadily in most countries, and the situation will become more challenging for public health financing and state budget expenditure [1]. Medical technology is a key driver of rising health expenditures [2], [3]. The Ministry of Public Health, Strategy and Planning Division, of Thailand, in 2018, reported the death rates classified according to major causes of 100,000 people and found that cancer was the leading cause of death among public health issues, followed by cerebrovascular disease and pneumonia [4]. In Thailand in 2016, there were 26,338 new patients, among whom 3,610 people, 1,475 males and 2,135 females, respectively, were diagnosed with cancer. The top 5 most common cancers are breast cancer, liver cancer, colorectal cancer, lung cancer and cervical cancer [5]. In addition, in the year 2017, there were approximately 78,540 cancer deaths, including deaths of 45,016 males and 33,524 females. The number of patients has increased since 2013 [6] due to the leading causes of death and the increasing trend of new patients, affecting the economy, society, quality of life and security of the people.

Surat Thani Hospital is a Thai central public hospital that is a specialized centre with 7 branches as follows: Heart Disease Centre, Cancer Centre, Accidental Centre, Newborn Centre, Kidney Transplant Centre, Haemodialysis Centre and Gallstone Centre. The centre hospital requires advanced and expensive technology, including both pharmaceuticals and medicines, to support the referral of patients in the health zone [7], [8]. It was found that in the fiscal year 2016, there were 1,466 cancer patients, both old and new, who were admitted to the service, with 245 patient deaths, making cancer 1st among all causes of patient deaths, withpneumonia and cerebrovascular disease being the 2nd and 3rd most common causes of death, respectively [9]. The number of patients has continued to increase, affecting the cost of treatment accordingly. Cancer treatment

approaches require advanced and sophisticated technology, such as surgery, radiation and chemotherapy or specific medications for cancer cells, such as targeted cell therapy. These technologies come at a high cost, and the government wants to control the cost of medical treatment [10]. The National Health Security Office requires the payment of medical services for the treatment of inpatients with relative weight (Relative Weight; RW) of the Diagnosis Related Groups (DRGs) as for outpatients, and the service fee is paid per eligible person. These are the main issues to be addressed and a circumstance to be improved upon. Thus, the objective of this research is to analyse the cost of the cancer treatment process of Surat Thani Hospital by comparing the cost of cancer treatment and creating a matrix of coefficients and constantswith compensation received from the National Health Security Office to set the policy for sustainable resource management to be the most appropriate and cost-effectiveness and sustainability in Thailand healthcare system.

II.

L

ITERATURER

EVIEWAccording to a cancer guidelines review from the National Comprehensive Cancer Network 2018 [4], the Guideline for Screening and Diagnosing Breast Cancer Treatment Thailand [11], the Liver Cancer Patient Care Guideline Thailand [12] and the Guideline for Screening and Diagnosing Colorectal Cancer Treatment Thailand [11], each cancer therapy activity can be considered as one of 6 activities as follows: 1. Operation, 2. Radiation, 3. Chemotherapy, 4. Hormonal therapy, 5. Targeted therapy and 6. TACE (Transarterial Chemoembolization for Liver Cancer). Referring to the literature reviews by researchers from both Thailand and internationally, there has been no research studying the cost of breast cancer, liver cancer and colorectal cancer. However, an international literature review found research from Mohd, et al. [13], who studied the cost of colorectal cancer, but it was in a different context, and due to the

progression of therapy technology, only some information can be used as reference. Additionally, most studies references the Activity-Based Costing method [14], [15], [16]. Hence, researchers only use it as a reference in the theoretical concepts analysis of activity cost to create a conceptual framework of such a study but cannot use it as a comparative study of the cost difference in each activity therapy for breast cancer, liver cancer and colorectal cancer.

Most studies using the Activity-Based Costing (ABC) approach in public health are described in the reference section [17], [18], [19], [20], [21], [22], [23], [24], [25]. However, there have been no studies on breast cancer, liver cancer, and colorectal cancer. The researcher is interested in studying the cost of treating cancer patients. Using ABC, which is a method for estimating service costs by finding the cost of the sub-activities that result in the final service, enables each resource to be identified, and the cost calculation is more accurate. The researcher conducted the study in patients with the three most prevalent cancer types: breast cancer, liver cancer, and colorectal cancer. According to the literature reviews both in Thailand and abroad, there has been no research on the cost of activities in all three cancers [5], [26].

The cost centres are organized into main and supporting cost centres. The supporting cost centre consists of 5 departments as follows: General Administrative, Group Human Resources Section, Financial Group, Accounting Group Inventory and Maintenance Section and the Strategy and Information Group. The main cost centres consist of 8 departments as follows: the organization of medical surgery, anaesthetist work, operating room surgery, radiology, pharmaceutical, outpatient jobs, nutrition and chemotherapy wards [9], [25]. The supporting cost centre consists of 5 departments as follows: General Administrative, Group Human Resources Section, Financial Group & Accounting Group, Inventory Maintenance Section and the Strategy & Information Group. Information obtained from the activity-based costing method can be used to plan, manage, and allocate resources for suitability and to create the best value for money. In addition, the researcher has also studied the total cost compared to compensation received from the National Health

Security Office. Therefore, the actual cost can be reflected back to the National Health Security Office (NHSO) to allocate expenses appropriately.

III.

R

ESEARCHM

ETHODSThe researcher used a descriptive statistics method by studying of the cost of cancer treatment activities. Surat Thani Hospital collected historical data for all breast cancer, liver cancer [25], and colorectal cancer patients all stages of the disease who were admitted to Surat Thani Hospital From 1 October 2017 to 30 September 2018 using the following steps: 1) To collect general data for breast cancer, liver cancer and bowel cancer; 2)To collect and summary data on all 5 supporting cost centres and 8 major cost centres as follows: labour cost, material cost and i nvestment cost; 3) To calculate costs of sub-activ ities in the activity-based costing system, which c an specify the cost of cancer treatment activities a ccording to the conceptual framework; and 4) To collect data for compensation received from the National Health Security Office. The data were divided into 2 parts by using descriptive statistics, such as frequency distribution, percentage, mean and standard deviation: 1. Analyse general information of patients and 2. Analyse the cost data as a framework as shown in Figure 1 [25], by collect cost data such as labour cost, material cost and investment cost from 8 major cost centres and 5 supporting cost centres to find the Total Direct Cost (TDC) in each cost unit. And allocate costs from all 5 support cost centres to 8 main cost centres. This is a Full Cost (FC) calculation using the Simultaneous Equation as follows: Arrange straight line equations and strip the image into a matrix equation to find the total cost of the agencies that sent the costs to one another (full cost of the transient cost centre) to get the equation:

[B] = [A].[X] (1) where: B is the direct total cost of the temporary cost unit.

A is a coefficient that sends costs to one another, and

X is the total cost of the temporary cost unit that distributed or sent the cost to each other.

By using Microsoft Excel for calculation by creating a matrix of coefficients [A] and constants [B], the coefficient A value is brought into the Inverse matrix by using Microsoft Excel to get the equation:

[X] = [A]-1.[B] (2)

Finally, multiply the Inverse matrix by [B], and the total cost of the cost units that are used together will be generated. Once we received the total full cost (FC) in the main cost centre of each department, we distributed the costs to related activities by using capital to help calculate the cost. After that, the activity cost in each activity was obtained.

IV.

R

ESULTS ANDD

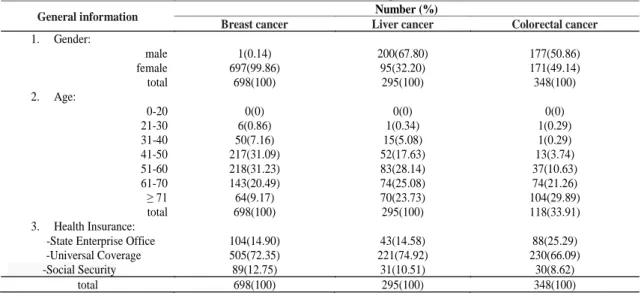

ISCUSSIONA. General Information for Cancer Patients The population studied included patients with breast cancer, liver cancer and colorectal cancer. Most breast cancer patients are female, and there

were 697 patients, accounting for 99.86 percent; patients aged between 51-60 years included 218 persons, accounting for 31.23 percent; and most had treatment rights because they had the National Health Insurance Card (Gold Card), including 505 patients, representing 72.35 percent.

The majority of liver cancer patients are male, 200 cases, 67.80%; those aged between 51-60 years included 83 persons, accounting for 28.14; and the majority had treatment rights from the National Health Insurance Card (Gold Cards), 221 patients, representing 74.92%. For patients with colorectal cancer, males and females were no different. There were 177 males or 50.86%, and 171 females or 49.14%; most of them aged over 70 years, with 104 males or 29.89%; and the majority had treatment rights from the National Health Insurance Card (Gold card), including 230 members, equivalent to 66.09%. The details are shown in Table 1.

Table 1: General information for breast cancer, liver cancer, and colorectal cancer patients

General information Number (%)

Breast cancer Liver cancer Colorectal cancer

1. Gender: male 1(0.14) 200(67.80) 177(50.86) female 697(99.86) 95(32.20) 171(49.14) total 698(100) 295(100) 348(100) 2. Age: 0-20 0(0) 0(0) 0(0) 21-30 6(0.86) 1(0.34) 1(0.29) 31-40 50(7.16) 15(5.08) 1(0.29) 41-50 217(31.09) 52(17.63) 13(3.74) 51-60 218(31.23) 83(28.14) 37(10.63) 61-70 143(20.49) 74(25.08) 74(21.26) ≥ 71 64(9.17) 70(23.73) 104(29.89) total 698(100) 295(100) 118(33.91) 3. Health Insurance:

-State Enterprise Office 104(14.90) 43(14.58) 88(25.29)

-Universal Coverage 505(72.35) 221(74.92) 230(66.09)

-Social Security 89(12.75) 31(10.51) 30(8.62)

total 698(100) 295(100) 348(100)

B. Labour Cost, Material Cost, Investment Cost, and Total Direct Cost

The total direct cost (TDC) of the primary cost centre is higher than the supporting cost centre, in which the total direct cost is 491.35 million baht, which has the highest component of the labour cost (LC), 51.92%, followed by the cost of materials (MC), 24.19%, and the cost of investment (CC), 23.89%. The details are shown in Table 2, which can be separated in each cost centre as follows.

In the support cost centre, the total direct cost (TDC) is 87.47 million baht, representing 17.80 percent of the total cost. The composition of the cost is labour cost (LC), 24.53%, material cost (MC), 1.49%, and cost of investment (CC), 19.70%. In major cost centres, the total direct cost (TDC) is 403.87 million baht, accounting for 82.20 %, representing labour cost (LC), 75.47%, material cost (MC), 98.51 %, and investment cost (CC), 80.30 percent. The details are shown in Table 2.

Table 2: The labour cost, material cost, investment cost, and total direct costs classified by major cost centre unit and supporting cost centre (million baht and percentages)

Cost centres Labour cost (LC) Material cost (MC) Investment cost (CC) Total cost

1 supporting cost centres 62.58 71.55% 1.76 2.02% 23.12 26.43% 87.47 100% 24.53% 1.49% 19.70% 17.80% 2 major cost centres 192.52 47.67% 117.09 28.99% 94.25 23.34% 403.87 100% 75.47% 98.51% 80.30% 82.20% total 255.10 51.92% 118.86 24.19% 117.37 23.89% 491.35 100% 100% 100% 100% 100%

C. Full Cost of the Cost Centres

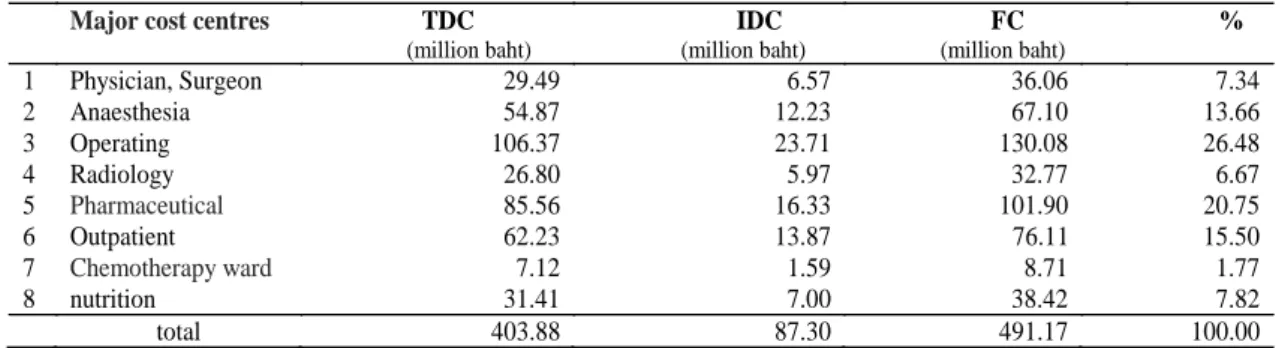

The total full cost (FC) of the 8 major cost centres was calculated from the total direct cost (TDC) combined with the indirect cost (IDC). From the cost allocation from the cost centre supported by the Simultaneous Equation method, it was found that the total full cost (FC) of the 8 main cost centres was 491.17 million baht, which was divided into total direct cost (TDC) of 403.87 million baht and the indirect cost (IDC)

from the allocation, equal to 87.29 million baht. The operating room had the highest total full cost (FC), equal to 130.08 million baht or 26.48 %, followed by the pharmaceutical work, which had a total full cost (FC) equal to 101.90 million baht, or 20.75 %. The lowest was the chemotherapy ward, which had a total full cost (FC) of 8.71 million baht, or 1.77 %. The details are shown in Table 3.

Table 3: The cost and percentage of total cost classified by main cost centre unit

Major cost centres TDC (million baht) IDC (million baht) FC (million baht) % 1 Physician, Surgeon 29.49 6.57 36.06 7.34 2 Anaesthesia 54.87 12.23 67.10 13.66 3 Operating 106.37 23.71 130.08 26.48 4 Radiology 26.80 5.97 32.77 6.67 5 Pharmaceutical 85.56 16.33 101.90 20.75 6 Outpatient 62.23 13.87 76.11 15.50 7 Chemotherapy ward 7.12 1.59 8.71 1.77 8 nutrition 31.41 7.00 38.42 7.82 total 403.88 87.30 491.17 100.00

D. Activity Costs in the Treatment of Breast Cancer, Liver Cancer and Colorectal Cancer

Activity costs in the treatment of breast cancer were divided according to the guidelines for treating 5 cancer-targeted activities (Targeted therapy), with costs per visit equal to 17,395.03, 2,452.11, 1,102.15, 976.33 and 1,170.56 baht, respectively. The details are shown in Table 4. Activity costs in the treatment of liver cancer were divided into 5 treatment activities [4] as follows: surgical, TACE, radiotherapy (RFA), chemotherapy and targeted therapy. Activity costs

in the treatment of liver cancer were divided into 5 treatment activities [4] as follows: surgical, TACE, radiotherapy (RFA), chemotherapy and cancer treatment (targeted therapy), with costs per session of 17,850.37, 17,850.37, 2,452.11, 1,736.19 and 933.87 baht, respectively [25]. The details are shown in Table 4. Activity costs in the treatment of colorectal cancer were divided into 3 treatment activities [4] as follows: surgical, radiotherapy (RFA) and chemotherapy, with costs each time equal to 18,305.71, 2,452.11 and 2,167.80 baht, respectively. The details are shown in Table 4.

Table 4: Activity costs for the treatment of breast cancer, liver cancer and colorectal cancer

Activity Unit cost (baht)

Breast cancer Liver cancer Colorectal cancer

1. Surgical 17,395.03 17,850.37 18,305.71 2. Radiation therapy 2,452.11 2,452.11 2,452.11 3. Chemotherapy 1,102.15 1,736.19 2,167.80 4. Hormonal therapy 976.33 - - 5. Targeted therapy 1,170.56 933.87 - 6. TACE - 17,850.37 -

E. Comparing the Cost Analysis by Activity-Based Costing and NHSO Compensation According to the guidelines for requesting expenses for public health services, fiscal year 2018, the disbursement of eligible rights in outpatients was 1,167.41 baht/eligible person. For inpatients, the reimbursement can be made equal to 1,113.93 baht, while for the reimbursement for chemotherapy, hormones or radiotherapy for cancer patients, the NHSO will pay for chemotherapy and hormonal drugs on a case-by-case basis, but not more than the specified threshold.

For the patients were treated by surgical procedures with a reimbursement of 8,050baht multiply adjRW (Relative weight is defined by NHSO which is calculated by divide an average charge of each DRG group by average charge of allpatients), it was found that the compensation received from the National Health Security Office was less than the total cost calculated from the research, with the following respective differences in breast cancer, liver cancer, colorectal cancer: -1.71, -4.80 and -2.71 million baht, as shown in Table 5.

Table 5: Comparison of the total cost of cancer treatment calculated from this research and compensation from the National Health

Security Office, fiscal year 2018

Cancer Total cost/year

(million baht) Compensation/Year (million baht) Difference (million baht) breast 3.48 1.77 -1.71 liver 5.56 0.76 -4.80 colorectal 3.60 0.89 -2.71

The results of the research, when considering the proportions of labour cost (LC): material cost (MC): investment cost (CC) of the total cost,

found the highest labour cost ratio for all primary cost centres and cost centres for support materials because they need to use medical materials that

are specific, sterile, and specialized, and the staff need to work together as a multidisciplinary team. The cost of labour varies according to the work force, civil servant and the service life, which can be divided according to the cost centres as follows: major cost centres 47.67: 28.9: 23.34, supporting cost centres 71.55:2.02: 26.43 respectively.

In addition, from the aforementioned proportions, it can be seen that the cost of materials in the support centre is relatively low. Since most materials used in offices involve general document work, which is different from the main cost centre which requires medical supplies, for the total full cost (FC), it was found that the operating room had the highest total cost, particularly the cost of materials, because the surgeries require medical supplies that are specific, sterile and sufficient. Next, pharmaceutical costs also account for a high material cost due to the high cost of medicines. In addition, in terms of activity costs, in treating all 3 cancers, surgical methods and treatment with TACE had higher costs than other methods. These results provide a step-by-step conduct to what to do. Nevertheless, these activities also received lower compensation from the National Health Security Office than the calculated activity since surgical patients must recuperate at the hospital as an inpatient, while treatments with radiation therapy, chemotherapy, hormonal therapy and targeted therapy are outpatient treatments.

Comparing compensation costs with calculated costs found that the compensation received from the National Health Security Office was less than the total full cost for breast cancer, liver cancer, and colorectal cancer, which creates the burden for the hospital to allocate funds to support such activities, such as opening a special clinic outside office hours, requesting donations through thehospital's foundation, and privatepayment for non-National List of Essential Medicine (NLEM) patients from the National Health Insurance Card (Gold card). If the compensation is not needed for an activity, the cash balance can be used to procure scarce medical equipment or modern medical equipment or even pay wages to staff and officers who still keep waiting for late payments from the government.

V.

C

ONCLUSIONThis research analyses the activity costs of cancer treatment under activity-based costing for breast cancer, liver cancer, and colorectal cancer, consisting of labour costs, material costs,

investment costs and total cost. The activity costs per service unit or process costs were calculated, and the cost was made known for each unit cost. It defines the gap between the current state of a process. Therefore, the organization can be allocated, and costs can be controlled to be suitable for each unit since the total cost calculated by this research was higher than the actual compensation received from the National Health Security Office. The research data constitute useful information for executives involved in policy making. In addition, the limited resources can be managed for maximum efficiency by making a budget plan to drive the organization strategy toward better execution for each unit cost. And the cost analysis of a matrix of coefficients and constants in this research also can be used to plan, manage and allocate resources to be the most appropriate and cost-effective for sustainability.

A

CKNOWLEDGMENTSThis research was partially supported by the new strategic research (P2P) project, Walailak University, Thailand. And it also was supported by Surat Thani Hospital.