西 南 交 通 大 学 学 报

第 56 卷 第 2 期

2021 年 4 月

JOURNAL OF SOUTHWEST JIAOTONG UNIVERSITY

Vol. 56 No. 2

Apr. 2021

ISSN: 0258-2724 DOI:10.35741/issn.0258-2724.56.2.13

Research articleEconomics

T

HE

I

NFLUENCE OF

E

NTERPRISE

R

ISK

M

ANAGEMENT

I

MPLEMENTATION AND

I

NTERNAL

A

UDIT

Q

UALITY ON

U

NIVERSITIES

’

P

ERFORMANCE IN

I

NDONESIA

企业风险管理的实施和内部审计质量对印度尼西亚大学绩效的影响

Ivan Yudianto a, Sri Mulyani a, b, Mohamad Fahmi c, Srihadi Winarningsih a a Department of Accounting, Faculty of Economics and Business, Universitas Padjadjaran

Bandung, Jawa Barat, Indonesia, ivаn.yudiа[email protected], sri.mulyаni@unpаd.ac.id,

srihаdi.winа[email protected]

b Universitas Singaperbangsa Karawang

Karawang, West Java, Indonesia, sri.mulyаni@unsikа.ac.id

c Department of Economics and Development Studies, Faculty of Economics and Business, Universitas Padjadjaran

Bandung, Jawa Barat, Indonesia, mohаmad.fа[email protected]

Received: January 27, 2021 ▪ Review: February 26, 2021 ▪ Accepted: April 14, 2021 ▪ Published: April 30, 2021

This article is an open-access article distributed under the terms and conditions of the Creative Commons Attribution License (http://creativecommons.org/licenses/by/4.0)

Abstract

Universities obtain a lot of pressure from stakeholders to manage risk to achieve better performance. The enterprise risk management implementation and internal audit quality conditions are not optimal to help the university reach the performance target. This study aims to examine the influence of the enterprise risk management implementation and internal audit quality toward the performance of State-Owned Universities-Legal Entity and State-Owned Universities-Public Service Agency in Indonesia. Researchers use explanatory study and questionnaire instruments to collect data. The study concludes that the enterprise risk management implementation and the internal audit quality have a positive and significant influence on the Performance of State-Owned Universities-Legal Entity and State-Owned Universities-Public Service Agency in Indonesia. Improving university performance requires an effective enterprise risk management implementation and internal audit quality.

Keywords:Enterprise Risk Management, Internal Audit Quality, University Performance

理的实施和内部审计质量条件并不是帮助大学达到绩效目标的最佳方法。本研究旨在考察企业风险管 理实施和内部审计质量对印度尼西亚国立大学-法律实体和国立大学-公共服务机构绩效的影响。研究人员使用解释性研究和问卷调查工具来收集数据。研究得出结论,企 业风险管理的实施和内部审计质量对印度尼西亚国立大学-法律实体和国立大学-公共服务机构的绩效具有积极而显着的影响。提高大学绩效需要有效的企业风险管理实施和内部审核 质量。 关键词: 企业风险管理,内部审计质量,大学绩效

I. I

NTRODUCTIONHigher education has the main task of developing science and technology to increase Indonesian competitiveness in the world [1]. Accordingly, higher education must continue to improve graduates' innovation and quality [2].

Increasing competitiveness and innovation requires talent entrepreneurship. Based on the Global Talent Competitiveness Index [3], Indonesia's talent competitiveness is ranked 77th out of 125 countries. Besides, The Global Entrepreneurship Index [4] reports that Indonesia's entrepreneurial sector is still lagging compared to other ASEAN countries. The government, companies, universities, and various levels of society contribute to increasing the potential for growth and entrepreneurial competitiveness [5]. In 2018, Indonesia's unemployment rate was relatively high, of which 3.16 percent unemployed from undergraduates and 10.42 percent from diploma graduates [6].

Based on the PR [2], Indonesia has fewer universities in the top 500 world-class universities (WCU) ranking than Malaysia, Hong Kong, Taiwan, South Korea, and China. Some performance indicators that still need to be improved are international publications, lecture quality, and the number of international students.

Universities operate in a complex, dynamic environment and under pressure to change business practices such as fierce competition to obtain fund and students, increasing efficiency and accountability, increasing supervision by the government and the public, the need for new technologies that require large investment costs, increasing entrepreneurial activities with private sector partners, expanding market competition, and proliferation of litigation [7]. Abraham [8] identifies the main risks in universities: economic conditions, political change, financial stability, student input, information technology, physical infrastructure, developing student talent,

compliance to regulations, and growing institutional reputation. The increasingly turbulent and complex organizational environment causes risk management to be an essential function for its leadership [9]. So it is necessary to develop an enterprise risk management (ERM) program to manage the problems within these institutions [10]. ERM is a means to manage risk comprehensively and strategically, but business sector practitioners develop the current ERM model from the fields of auditing, accounting, and insurance [11]. Risk management practices in universities and other non-profit organizations are less developed than in most companies [12]. There are several obstacles to implementing ERM in higher education, such as ambiguity of university goals, shared governance, and decentralized decision making [13]. In the Netherlands, higher education institutions still do not have an integrated policy related to risk management [14]. In 2003, The National Association of College and University Business Officers (NACUBO) published a risk management report on higher education, thus encouraging higher education leaders to implement and promote an effective risk management program [12]. ERM helps universities maintain competitive advantage, protect their reputation, respond effectively to adverse events, limit financial shocks, and improve resource management [7].

Organizations need an ERM program in line with various strategic levels within the organization [15]. The ERM implementation outcome provides information to determine the appropriate organizational strategic formulation [16]. If ERM is a control system, ERM performance should provide feedback for cognitive learning processes and behavior in organizations to add value to the organization [17].

However, Pagach & Warr [18] revealed that ERM implementation had not influenced improving company performance in the long-run

period. Other studies also showed that ERM had no significant effect on firm value [19], [20], [21]. McShane et al. [22] found a positive relationship between ERM rating and Tobin's Q, but the results showed that ERM implementation did not cause an increase in firm value.

Indonesia has Government Regulation of Republic Indonesia Number 60 of 2008 concerning the Internal Control System for Government Agencies [23], and Ministry of Education and Culture Regulation of Republic Indonesia Number 66 of 2015 concerning the Risk Management [24] as legal guidance for state universities in Indonesia to implement risk management. Still, the ERM has not been implemented optimally.

Besides, internal audit also contributes to ensuring organizational goals using efficient and effective resources [25]. Allegrini & D'Onza [26] reveal that internal auditors and risk management simultaneously increase the organization's value. Management uses an internal audit to ensure organizational adherence to relevant statutory regulations and ensure organizational goals [27]. Internal auditors can assist the administration at all organizational levels in universities by providing more efficient and effective use of human resources and improving their quality to achieve the goals [28]. Further, Mihret & Yismaw [29] reveal that the internal audit quality (IAQ) and management support significantly influence internal audit effectiveness by increasing grades, improving operations, and helping universities achieve their goals. Thus there is a close relationship between internal audit and company performance [30].

However, Internal Audit Department's contribution in the state-owned universities is still not optimal because the number of auditors, budget, facilities, and infrastructures in several universities is still inadequate [31]. Griffiths [32] revealed no relationship between internal audit and performance due to a negative attitude towards internal audit and the lack of appropriate skills and training for internal auditors. Also, Kiabel [33] also concluded that there was no strong relationship between internal audit practices and financial performance due to poor internal audit practices.

Researchers conduct the study at State-Owned Universities-Legal Entity (SU-LE) and State-Owned Universities-Public Service Agency (SU-PSA) in Indonesia due to wider academic and non-academic autonomy and financial support from the

government to achieve the top 500 WCU ranking than other universities in Indonesia.

The factual phenomena and empirical research results above show inconsistencies with the underlying theory. So researchers suspect that there are factors that cause inconsistencies (contingency factors). The contingency approach provides the idea that the ERM implementation and the IAQ influence state university' performance. Based on the literature, the research topic is one new study that discusses the ERM implementation, the IAQ, and its influence on the SU-LE and SU-PSA performance in Indonesia. It is expected to add insight into university performance (UP) in Indonesia.

A. Problem Formulations

Based on the research background above, the research problems that can be formulated are:

• Does ERM implementation affect universities' performance?

• Does IAQ affect universities' performance?

B. Contribution of This Paper to the Literature

• This study statistically proves that performance can be improved by ERM implementation and IAQ for public sector organizations.

• Empirically, this study proves that universities' performance is influenced by ERM implementation and IAQ.

• The model in this study can be used in the public sector organizations in Indonesia to measure performance in universities from the perspective of ERM implementation and IAQ.

II. L

ITERATURER

EVIEWA. ERM Implementation

ERM is the culture, capabilities, and practices, integrated with strategy-setting and performance, that organizations rely on to manage risk in creating, preserving, and realizing value [34]. Moreover, ISO 31000 [35] states that ERM is coordinated activity to direct and control an organization concerning risk. Maurer [36] states that the effective implementation of ERM covers all lines of business (integrated), all types of risk (comprehensive), and is in line with business strategy (strategic).

CRMS Indonesia [37] concludes that the companies in Indonesia generally use ISO31000 (67.5%) more than COSO (15%) and other

standards (17.5%) as risk management standards. The dimensions and indicators in this study use ISO31000. According to ISO 31000 [35], the risk management process includes communication and consultation, determining the context, identifying risks, analyzing risks, evaluating risks, and monitoring and review.

B. Internal Audit Quality

Pitt [38] states that quality is relative, where comparing two products or services or assessing a product or service against a series of accepted standards determine the existence of quality. Providing quality products or services can increase customer satisfaction, supporting organizational success [38].

Mihret & Yismaw [29] reveal that IAQ is determined by the internal audit department's capacity to provide useful recommendations on the organization's audit findings. According to the Institute of Internal Auditors [39], the definition of internal audit is an independent, objective assurance and consulting activity designed to add value and improve an organization's operations. Internal auditors plan and perform audit work to produce useful audit findings and provide organizational improvement recommendations [39].

Based on the Institute of Internal Auditors [39], IAQ has dimensions of independence and objectivity, expertise and professional accuracy, work scope, implementation of inspection activities, managing internal audit activity, and quality assurance requirements and improvement programs.

C. University Performance

Performance is the output of activities or programs intended to be achieved in connection with the budget realization with measured quantity and quality [40]. Ghobadian & Ashworth [41] state that performance measurements can help the organization improve resource allocation and management decisions, increase accountability and provide a systematic basis for staff assessment and motivation. University management requires a balance in economic, efficiency, and effectiveness to ensure universities' sustainability in the long run period [42].

The universities have many experiences with significant changes, including applying the concepts of managerialism and entrepreneurship to organizational management [43]. The government

has reduced funding significantly for state universities. Consequently, state universities find other income sources to finance their programs and activities [44]. Accordingly, universities are increasingly required to increase collaboration with industries to increase revenue. Fielden [45], Kassahun [46], and Wang [47] reveal that the income earned apart from the government and tuition fees are indicators of the financial performance of universities.

One of the higher education tasks is to create superior human resources through a good learning process. The learning performance can be measured using the graduate level that directly works indicator [45], [47]. Universities contribute significantly to develop and enhance growth potential and entrepreneurial competitiveness [5]. As a result, the level of graduates with entrepreneurship is one of the relevant performance indicators for universities.

Besides, innovation performance is one of the performance indicators that universities must achieve. Nelson [48] states that universities have an essential role in the national innovation system because it is a place for innovative research. Science-based industries are necessary to enhance international competitiveness. Academic research is a driving force for creating innovations that can be used in industries [49].

Fielden [45] and Wang [47] use citations to assess the research and publications performance. The more the number of citations, the greater the usefulness of scientific work for the community. Thus the number of citations very relevant is used as an indicator of university performance.

The Indonesia Government determines universities performance based on the Ministry of Research, Technology, and Higher Education Decree of the Republic of Indonesia Number 14 of 2019 for SU-LE and SU-PSA [50], including the number of citations, registered intellectual property, innovative products, entrepreneurial students, and the percentage of graduates who work immediately.

D. ERM Implementation and University Performance

ERM implementation is a useful technique for managing risk. The companies that implement it will benefit from business performance [51], [52] and enhance the reputation [53]. Moreover, Pagach & Warr [18] explain that companies that adopt ERM are motivated by economic benefits.

Integrated risk management implementation can help the organization reduce risks that hinder organizational goals [54] and create organizational value [55], [56]. Acharyya [16] concludes that a strong ERM will balance the performance of a single dimension company such as Economic Value Added with performance dimensions compound such as the Balanced Scorecard. Hoyt & Liebenberg [57] explain a positive relationship between ERM implementation and organizational values.

Complex and dynamic environments with high uncertainties encourage universities to implement ERM [58]. ERM helps universities maintain competitive advantage, respond to significant events, avoid financial shocks, and manage the resources effectively [59]. Further, ERM contributes to overcoming problems and managing risks that hinder the achievement of UP [12], [14]. Implementation of ERM supported by the chief of the risk management unit, top management, and good training and education has a significant and positive effect on management, finance, and marketing in PU in Malaysia [60]. Risk management is carried out by identifying, classifying, analyzing, and mitigating risks to improve the UP [61]. Based on these reviews, a hypothesis is stated as follows:

H1: There is a positive and significant influence

of ERM implementation on the UP.

E. Internal Audit Quality and University Performance

Institute of Internal Auditors [39] states that internal audit helps organizations achieve their goals. An internal audit is a management tool used to provide evidence regarding reducing and eliminating problem areas to improve overall organizational performance [62]. The internal audit seeks to add organizational value through risk management at different organization levels and align the internal audit objectives with the

organization's strategic goals [26]. Besides, Dahir & Omar [63] and Al-Matari et al. [30] reveal that IAQ has a significant effect on company performance.

Internal auditors can assist the administration at all levels of the organization by ensuring more efficient and effective use of human resources and improving quality to achieve the universities' stated goals [28]. Mulyani et al. [64] state that internal audits can prevent fraudulent financial reporting. Moreover, Mihret & Yismaw [29] reveal that the IAQ and management support significantly influence internal audits' effectiveness by increasing grades, improving operations, and helping universities achieve their goals. Based on these reviews, a hypothesis is stated as follows:

H2: There is a positive and significant influence

of IAQ on UP.

III. M

ATERIALS ANDM

ETHODSA. Research Methods

The objects in this research are the ERM Implementation, IAQ, and UP. Based on its purpose, this is explanatory research that aims to test the hypothesis based on a particular theory [65]. The data are distributed by respondents using a questionnaire given to the chief/auditor of the Internal Audit Department in universities. The time horizon of this study is cross-sectional, that is, research at a specific period. The analysis units examined are 41 of SU-LE and SU-PSA in Indonesia.

B. Variable Operationalization

Variables are research objects with different values at various times for the same object or at the same time for other objects [66]. The operationalization of variables is the act of formulating variables to determine the indicators attached to these variables.

Table 1.

Variable operationalization

Variables Dimensions Indicators

ERM Implementation [35]

Mandate and Commitment (ERM1) • Risk management training. • Continous communication.

• Risk management is part of decision-making. Risk Management Framework

Planning (ERM2)

• Resources to perform risk management. • Integrating risk management in organizational processes.

Risk Management Process (ERM3) • Communication and consultation. • Determine the context.

Variables Dimensions Indicators

• Risk identification. • Risk analysis. • Risk evaluation. • Risk response.

• Monitoring and review.

IAQ [29], [39]

Purpose, Authority, and Responsibility (IAQ1)

• Internal Audit Charter review. • Internal Audit Charter discussion. Independence and Objectivity

(IAQ2)

• Organizational independence. • Individual objectivity.

• Impairment to independence or objectivity. Proficiency and Due Professional

Care (IAQ3)

• Proficiency.

• Due to professional care. Nature of Work

(IAQ4)

• Risk management • Governance. • Control. Performing the Audit Activities

(IQA5)

• Engagement planning. • Performing the engagement. • Communicating results. • Monitoring progress. Managing the Internal Audit Activity

(IAQ6)

• Planning.

• Communication and approval. • Resource management. • Policies and procedures. • Coordination and reliance.

• Reporting to senior management and the board of trustees.

• External service provider and organizational responsibility for internal auditing.

Requirements of the Quality

Assurance and Improvement Program (IAQ7)

• Internal assessments. • External assessments. Management Support

(IAQ8)

• Management response to audit findings and follow-up.

• Management's commitment to strengthen internal audit.

UP [45], [46], [47], [50]

Financial Performance (UP1)

• The percentage of non-tuition fee income from total universities income.

• Ability to finance programs and activities. • Ability to meet short obligations. • Research income from industry. Quality of Learning and Student

Affairs (UP2)

• Percentage of graduates with entrepreneurship. • Percentage of graduates directly employed. Research, Development, Innovation

and Community Service Performance (UP3)

• The number of citation papers published in an international journal indexed by Scopus.

• The number of citation papers published in the national journal is indexed by Sinta.

• The number of patents per a lecturer. • The number of innovative research and development products that have been produced and utilized by users.

• Community service performance.

Note: All indicators used in the table above are 1-5 ordinal scale

IV. R

ESULT ANDD

ISCUSSIONA. Descriptive Analysis

The respondents' responses to each statement item are categorized into 5 categories: very good, good, fair, poor, and very poor with the following

calculation: Interval Distance = [maximum value - minimum value]: 5 = (5-1): 5 = 0.8.

Table 2.

Guidelines for respondent response score categorization

Average Index Category

4,21 - 5,00 Very Good 3,41 - 4,20 Good 2,61 - 3,40 Fair 1,81 - 2,60 Poor 1 - 1,80 Very Poor

The table below presents the calculation of each variable's scores and summary scores of respondents' answers obtained from SU-LE and SU-PSA.

Table 3.

Descriptive statistics of ERM implementation variable

Variable and Dimension Average Score Category

ERM Variable 2,43 Poor 1 ERM1 2,78 Fair 2 ERM2 2,55 Poor 3 ERM3 2,25 Poor

Based on Table 3 above, the average value of respondents' answers to the ERM Implementation construct is 2.43 with the poor category. The result means that, on average, SU-LE and SU-PSA have not implemented ERM properly. The ERM implementation requires the university leader's strong commitment by developing programs and activities to increase risk awareness and ongoing communication to employees about the importance of risk management. University leaders must prepare resources that support the risk management function and develop risk management regulations and guidelines. Integrating the risk management process in the organization's business processes is essential for effective ERM implementation.

Table 4.

Descriptive statistics of IAQ variable

Variable and Dimension Average Score Category

IAQ Variable 3,06 Fair 1 IAQ1 2,99 Fair 2 IAQ2 3,59 Good 3 IAQ3 3,28 Fair 4 IAQ4 3,07 Fair 5 IAQ5 3,71 Good 6 IAQ6 3,59 Good 7 IAQ7 2,63 Fair 8 IAQ8 3,76 Good

Further, respondents' average value to the IAQ construct is 3.09, with a good category. The result means that, in general, internal audits at SU-LE and SU-PSA have a good internal audit quality, but there is still a gap of 39 percent, so needs improvement in internal audit quality. IAQ indicators that need to be improved are the internal audit charter review, disclosure of the independence or objectivity impairment, internal auditors proficiency, performing the engagement, communicating results, internal assessment, and external assessments.

Table 5.

Descriptive statistics of UP variable

Variable and Dimension Average Score Category

UP Variable 2,67 Fair 1 UP1 3,41 Good 2 UP2 2,4 Poor 3 UP3 2,05 Poor

The average value of respondents' answers to the UP construct is 2.67 with a fair category. The UP needs to be improved further, considering that there is still a sizeable gap of 47 percent. Financial performance obtains a good category, but the quality of learning and student affairs get a poor category. Besides, research, development, innovation, and community service performance also get the poor category.

B. Structural Equation Model (SEM) PLS Analysis

The CFA test results for all indicators are valid as a measurement tool for each latent variable. Further, the convergent validity test results for all dimensions and indicators are valid as a measurement tool. Moreover, the discriminant validity test result for all dimensions and indicators have good discriminant validity.

Moreover, the measurement results with composite reliability are that each indicator has consistency in measuring the construct.

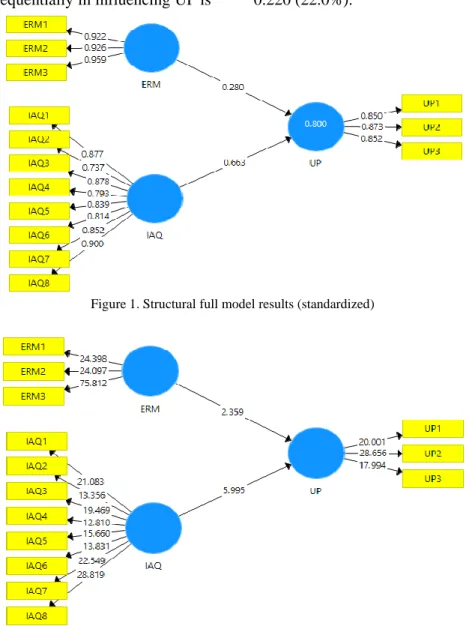

The following Figure 1 presents the full structural model's estimation results using the latent variable score. Based on the test results in the picture above, each standardized coefficient (path) between variables shows positive results. Then, find out the significance of the relationship between variables obtained by the bootstrapping method with the following Figure 2.

Based on the results of the structural model estimation of the relationship between latent variables through the path coefficient test, the ERM

Implementation and IAQ have an effect of 80.00% on the UP simultaneously. Moreover, the most dominant variable sequentially in influencing UP is

IAQ with a path coefficient of 0.580 (58.0%), then ERM implementation with a path coefficient of 0.220 (22.0%).

Figure 1. Structural full model results (standardized)

Figure 2. Structural full model results (bootstrapping)

C. Hypothesis Test

The structural model evaluation results show that the path coefficient between the ERM implementation and UP is 0.220 positively. Further, the t-statistic value (2.359) is greater than t-table (1.65) and the p-value (0.008) < 0.05, then at a 5% error rate (one-tail) so it is decided to reject H0 and accept H1. In conclusion, the ERM

implementation has a positive and significant effect on UP.

The structural model evaluation results show that the IAQ and UP's path coefficient is 0.663 in a positive direction. Moreover, the t-statistics value (5.995) is greater than the t-table (1.65) and p-value (0,000) < 0.05, then at a 5% error rate (one-tail) so it is decided to reject H0 and accept H2. In

conclusion, the IAQ has a positive and significant effect on UP.

D. Discussion

The result of hypothesis testing concludes that the ERM implementation has a positive and significant effect on UP. The result of this study is consistent with the results of previous studies conducted by Acharyya [16], Obalola et al. [53], Gates et al. [56], and Hoyt & Liebenberg [57]. They conclude that the ERM implementation can improve organizational performance. Organizations that adopt ERM are motivated by economic benefits [18]. The integrated ERM implementation into all organization levels can help reduce risks that hamper organizational goals [54]. It will have

implications for improving the organization's performance and value [51], [52], [55].

ERM helps universities maintain competitive advantage, respond effectively when significant events occur, avoid financial shocks, manage the resources available at universities effectively [59]. Further, ERM can help universities address the main areas of risk faced and managing risks that lead to key performance indicators [12], [14]. Besides, Setapa & Zakwan [60] conclude that ERM's implementation supported by the chief of a risk management unit and top management, good training and education has a significant and positive influence on management's performance finance and marketing at PU in Malaysia.

Based on study results, ERM implementation at the SU-LE and SU-PSA is still not optimal, such as the low frequency of risk management training at universities to increase risk awareness and risk management. However, universities have sufficient resources to implement risk management, such as facilities and infrastructure, and the number of human resources. Nevertheless, the ERM implementation has an influence of 22% on UP; other factors influence the rest.

The hypothesis testing results reveal that IAQ has a positive and significant effect on UP. The results are consistent with the previous studies conducted by Mihret & Yismaw [29], who revealed that the IAQ and management support significantly influenced universities' internal audit effectiveness. Dahir & Omar [63] and Farouk & Hassan [67] also concluded that internal audit quality affects company performance. Allegrini & D'Onza [26], Al-Matari et al. [30], IIA [39], and Mahzan & Hassan [62] state that internal audit can help the organization achieve the goals.

The study results stated that the IAQ had an effect of 58% on UP; other factors influenced the rest. Internal auditors can help universities to evaluate the adequacy and effectiveness of controls. As a result, universities can economically, efficiently, and effectively conduct the programs and activities and comply with applicable laws and regulations.

SU-LE and SU-PSA have broad financial management autonomy. Internal audit contributes to ensuring that finance is managed in a transparent, accountable manner and allocated to programs and activities that support the universities' vision and ensure the fulfillment of liabilities. SU-LE and SU-PSA have revenues from various sources such as tuition cost, cooperation

revenue with industry and public sector organizations, income from business units, income from community grants, etc. Internal audits contribute to ensuring that revenue realization, according to targets.

V. C

ONCLUSIONBased on the study results, ERM implementation has a positive and significant influence on UP. ERM implementation helps universities to identify risk factors that might hamper the achievement of goals and provide strategies to overcome these risks.

Also, ERM implementation helps to find opportunities in the context of achieving the expected UP. Universities leaders must arrange programs and activities to increase employee risk awareness and risk management competencies periodically, ongoing communication to employees regarding the importance of considering risk in every decision making, formulate regulations and guidelines for implementing risk management, integrating risk management in organizational processes is required to accomplish effective ERM implementation.

Moreover, the IAQ has a positive and significant effect on the UP. The internal audit provides an objective assurance and consulting services designed to add value and helps a university accomplish its objectives.

VI. L

IMITATIONS ANDS

UGGESTIONSThis research was only conducted at SU-LE and SU-PSA in Indonesia. For further research, it is recommended to conduct research in private universities throughout Indonesia.

A

CKNOWLEDGMENTSThe authors would like to thank the Internal Audit Department in SU-LE and SU-PSA for helping carry out this research.