Tax Legislation as Instrument to Support Private

Patronage of the Arts and Cultural Heritage

prof. dr. Sigrid J.C. Hemels

1and dr. Yuka Shiba

1 Introduction

Historically, the private initiative has always been of great significance for the arts. Emperors, kings and wealthy citizens were important patrons of the arts both in Europe and Asia. In most European countries the government took over from the private initiative after World War II. However, the private initiative was never completely gone, also not in the second half of the 20th century in which government subsidies were the dominant factor in the funding of the arts and cultural heritage. The private initiative remained very important for cultural heritage such as monuments: it would be impossible for the government to take responsibility for all monuments. Another reason why the private initiative never fully disappeared was that individuals and companies still collected art. Some of these collections became so important, that they were given on loan or were

1 Professor of Tax Law at the School of Law of Erasmus University Rotterdam,

the Netherlands. This paper was inspired by a Japan Society for the Promotion of Science (JSPS) Invitation Fellowship for Research in Japan (Short-term) in November 2014 during which fellowship I gave a lecture on the topic of this paper at Tokoha University in Shizuoka at the conference organized by dr. Yuka Shiba: ‘Cultural heritage and landscapes as local resources’.

even donated to museums or became the basis of a new museum. A good example of a private museum in the Netherlands is Museum

Beelden aan Zee [Sculptures at Sea] in Scheveningen which is founded by Theo and Lida Scholten who started their collection in 1969. Also other individuals donated funds for a new wing of this museum.2

Furthermore, many volunteers are active in the museum. Another interesting example is the Nihon No Hanga Museum in Amsterdam with a beautiful collection of Japanese prints of which 90% dates from the 20th century (mostly before World War II) and which hosts two exhibitions every year.3 In Japan, a lot of historical and cultural

heritage is privately owned.

At the end of the 20th and the beginning of the 21th century, budget constraints of national and local governments obliged cultural and heritage institutions to look for alternative sources of funding. This brought companies and private individuals who might have operated in the shadow until then, in the spotlight again as an important source of funds for the arts and cultural heritage. In the Netherlands at the end of the 1990s, the economist Rick van der Ploeg introduced the term ‘cultural entrepreneurship’ when he was State Secretary of Culture.4

Cultural entrepreneurship required more focus on the audience and private support and less focus on governmental support. Tax legislation was mentioned as a possible instrument to support cultural

2 For more information on the museum and its collection I refer to www.

beeldenaanzee.nl/engels/110-2/ (accessed on 24 November 2014).

3 http://www.nihon-no-hanga.nl/ (accessed on 9 December 2014).

4 Cultuur als Confrontatie, Nota Cultuurbeleid 2001-2004 Kamerstukken II,

1998-1999, 26591, nr. 2. https://zoek.officielebekendmakingen.nl/kst-26591-2. html (accessed on 24 November 2014).

entrepreneurship.5 Several countries, such as Spain, France and the

Netherlands introduced special legislation on cultural patronage, which included tax incentives, in 2002, 2003 and 2012 respectively.6 In

Japan, a special income tax treatment for the contributions to institutions officially recognized as contributing to the public welfare was introduced in 1962 (charitable contribution deduction).7 Tax payers

can deduct donations given to the national or a local government or to the officially recognized institutions.8 In 2008, the government

introduced a“hometown tax” that would let taxpayers allocate some of their residence tax (local income tax) to hometowns they no longer reside in.9 Donations to local governments via a tax incentive that

encourages people to contribute to their hometowns while living elsewhere have soared. A tax payer can deduct donations not only from his income tax but also from residence tax. However, no specific legislation on incentives for cultural patronage has been introduced in

5 Cultuur als Confrontatie, Nota Cultuurbeleid 2001-2004 Kamerstukken II, 1998-1999,

26591, nr. 2.

https://zoek.officielebekendmakingen.nl/kst-26591-2.html (accessed on 24 November 2014).

6 Ley 49/2002 de 23 de diciembre, de régimen fiscal de las entidades sin fines

lucrativos y de los incentivos fiscales al mecenazgo, Loi du 1er Août 2003 relative au mécénat aux associations et aux foundations and Wet van 22 december 2011 tot wijziging van enkele belastingwetten (Geefwet).

7 Article78 Income Tax Act, Article37 (3) Corporate Income Tax Act.

8 Yoshihiro Masui, Governmental and Non-governmental Organizations in Japan:

a Tax Perspective, in Kenjiro Egashira et al. ed., Markets and Organizations, University of Tokyo Press 2005, pp.33-57. Prof. Masui points out that it is important to decide which organizations are desirable as providers of public goods because the existence of the organizations is a prerequisite for charitable contribution deduction.

Japan with the exception of an exemption in the property tax10 and an

exemption in the capital gain tax for important cultural property.11

In this paper we will analyse how tax legislation can be used to support private patronage of the arts and cultural heritage. We will discuss best practices in several European countries. However, first we will introduce the notion of a ‘tax incentive’ and how it functions in comparison to direct subsidies.

2 Tax as a policy instrument

A government has several instruments to achieve policy goals, including cultural policy goals. These instruments include:

1. Legislation, for example the requirement of a permit to export important works of art;

2. Information campaigns, for example the Dutch campaign Cultuur daar geef je om [Culture that is what you give for (with the double meaning in Dutch of ‘what you care about’] in order to promote giving to art and cultural heritage;12

3. Subsidies:

a) Direct subsidies, for example government subsidies for orchestras; b) Tax incentives, for example deductibility of gifts for income tax

purposes.

The primary function of tax legislation is to raise a budget for government expenditure. Some Japanese municipalities (Kyoto city,

10 Article 348 (2) (i) Local Tax Act.

11 Article 40-2 Act on Special Measures Concerning Taxation. 12 http://www.daargeefjeom.nl/ (accessed on 24 November 2014).

Nara prefecture, Dazaifu city) have introduced special taxes to raise a budget for the maintenance of historical monuments. Here taxes are not used as a policy instrument, but as a means to obtain the budget for direct expenditures (category 3a above). Kyoto city introduced the Kyoto Old Capital Preservation Cooperation Tax, which was once levied in accordance with a tax ordinance in 1985. This tax was used only for the maintenance costs of historical and cultural monuments. The tax was imposed on visitors of cultural property in temples. As the temples were obliged to collect the tax, they were against the tax.13 It

was abolished in 1988.

However, tax can also be used to achieve certain policy goals (secondary function). If tax legislation is used to give rewards for desired behavior, this is called a tax incentive. Other words for the same phenomena are tax subsidy or tax expenditure. According to Surrey, he was the first to use the word ‘tax expenditure’ in 1967 when he was Assistant Secretary of the Treasury for Tax Policy of the USA.14 Based on his definition, the

Netherlands now uses the following, general, definition of a tax incentive: “a government expenditure in the form of a loss of tax income or postponement of tax income caused by a provision in the legislation insofar as this provision is not in accordance with the primary structure of that legislation”.15 The problem is, of course, what the

13 Takemichi Hatakeyama, Kyoto Old Capital Preservation Cooperation Tax,

Jurist 786 1983 p. 27.

14 S.S. Surrey, Pathways to Tax Reform, Cambridge Massachusetts: Harvard

University Press 1973, p.vii.

15 Annexes to the Miljoenennota 2015 [Budget 2015], Kamerstukken II [Official

documents of the Second Chamber of Parliament], 2014-2015, 34000, no. 2, p. 24 http://www.rijksbegroting.nl/2015/voorbereiding/miljoenennota,kst199383_6. html (accessed on 24 November 2014). This definition was first used in the report Belastinguitgaven in de Nederlandse inkomstenbelasting en de

‘primary structure’ of tax legislation is. This has been a politically sensitive discussion in the Netherlands on which we will not elaborate in this paper. Tax incentives can take several forms such as a deduction from taxable income, a tax credit, a deferral of tax, a reduced tax rate or a tax exemption. In Japan a similar though differently defined concept is used: ‘Special Tax Measures’. These are defined as ‘provisions that take exception to Japan’s fundamental tax principles (equity, neutrality, and simplicity) to pursue some other policy objective.’16 An

important difference with the definition of tax incentives is that Japan defines its Special Tax Measures by comparison to fundamental tax principles, rather than relative to a benchmark or primary tax system. Whether tax incentives should be used to achieve a certain policy goal, should be based on the answers to the following questions:

Why is government interference necessary? What is the policy objective?

What is the most effective and efficient instrument to reach this policy objective?

Only if these questions can be answered in a duly motivated way and lead to the conclusion that tax incentives are the most effective and efficient instrument for a certain policy objective, these should be used. Unfortunately, in reality these questions are not always decisive. Lobby

loonbelasting, The Hague: Staatsuitgeverij 1987, p. 16.

16 OECD, Tax Expenditures in OECD Countries, Paris: OECD 2010, p. 93, http://

www.oecd.org/gov/budgeting/taxexpendituresinoecdcountries-oecdpublication. htm (accessed on 24 November 2014).

groups can have a strong political influence when pleading for tax incentives. The benefit of such incentive is big for the small group who benefits from it and the costs are born by a large group of anonymous tax payers whose interests are not always duly taken into account by Members of Parliament. Tax incentives may be perceived as free lunches, but they are not. A tax incentive reduces the tax income of government, for which reason the government must either increase the tax burden of other tax payers and/or increase other taxes to maintain the same budget or reduce spending. Just as direct subsidies, tax incentives are a cost for the government. Ministries other than the Ministry of Finance often prefer a tax incentive over a direct subsidy as these do not reduce their budget, but only affect the income of the Ministry of Finance. For the Ministry of Culture an ineffective tax incentive might, therefore, be more attractive than a more effective direct subsidy which reduces its budget. For the government as a whole this is, of course, not desirable. In our view, tax incentives should, therefore, be accounted for and controlled in the same way as direct subsidies to ensure an efficient and effective use.17 Unfortunately,

currently this is not the case in many countries. For example, in Japan, tax expenditures were not disclosed in a yearly budget.18 In 2010, the

17 In the same way: OECD, Tax Expenditures in OECD Countries, Paris: OECD

2010, p. 45, http://www.oecd.org/gov/budgeting/taxexpendituresinoecdcountries-oecdpublication.htm (accessed on 24 November 2014).

18 Toshiyuki Uemura, An Estimation of Tax Expenditure in Japanese Income Tax

from the Viewpoint of the Fiscal Transparency, Government Auditing Review Volume 16 2009.3, p. 1 http://www.jbaudit.go.jp/english/exchange/pdf/e16d01. pdf (accessed on 24 November 2014). Uemura (p. 16) is of the opinion that “Creation of a tax expenditure budget and its disclosure are essential to increase fiscal transparency of Japan, to recover reliability on finance, and to openly discuss tax expenditures as policies.”

Special Taxation Measures Transparent Act was enacted. A review was made targeting all of the special taxation measures and rules provided for in the Act on Special Measures Concerning Taxation, which are intended to reduce the tax burden for industry policy and other specific policy purposes.19 The Minister of Finance creates a report that

describes the applicability of the Special Taxation Measures each fiscal year, and Cabinet submits it to the Diet. This act is not enough for the special measures to be accounted for and controlled by Parliament. Even though many other industrialized countries, such as the USA since 1967/197420 and the Netherlands since 1999 prepare so called ‘Tax

expenditure budgets’ in which tax expenditures are accounted for, these do not have the same status as budgets for direct expenditures.

Because of this, several tax experts are not in favor of tax incentives as a policy instrument. In Japan, some tax experts regard tax incentives (special taxation measures) as hidden subsidies which violate the fairness principle of the Japanese Constitution.21

The OECD identified the following theoretical and practical allegations

19 Ministry of Finance, Report on the result of the application of the Survey of

Special Taxation Measures http://www.mof.go.jp/tax_policy/reference/stm_ report/index.htm (accessed on 6 December 2014).

20 In 1967, the first US list of tax expenditures was produced. The Congressional

Budget Act of 1974 required the Administration to publish a tabulation of tax expenditures as part of its annual budget submission. Leonard E. Burman and Marvin Phaup, Tax expenditures, the size and efficiency of government, and implications for budget reform, NBER working paper series, Working Paper 17268, Cambridge Massachusetts: National Bureau of Economic Research, 2011, p. 4, http://www.nber.org/papers/w17268 (accessed on 24 November 2014).

21 Article 14. All of the people are equal under the law and there shall be no

discrimination in political, economic or social relations because of race, creed, sex, social status or family origin.

against tax expenditures:22

1. Fairness: the issue of the lobby groups mentioned before;

2. Efficiency and effectiveness: difficulty to evaluate existing tax expenditures and weaknesses in tax expenditure reporting in the budget;

3. Complexity: tax incentives can increase complexity of the tax system;

4. Revenue sufficiency: difficulty to estimate the costs of tax incentives;

5. Growth of tax incentives: Tax expenditures tend to evade systematic and critical review. As a result, they can grow over time and avoid reform, reduction or repeal.

However, if the choice for the instrument of a tax incentive is based on the three questions mentioned before and if these are duly accounted for and evaluated, tax incentives can, in our view, be a valuable instrument to reach certain cultural policy objects in a more efficient and effective way than with the other policy instruments. We will substantiate this statement below.

3 Effective and efficient tax incentives for cultural policy goals

In 2010 the OECD identified several conditions under which tax expenditures are most likely to be successful, or even the best, policy

22 OECD, Tax Expenditures in OECD Countries, Paris: OECD 2010, p. 25-34,

http://www.oecd.org/gov/budgeting/taxexpendituresinoecdcountries-oecdpublication.htm (accessed on 24 November 2014).

tools to achieve their objectives.23 This was under the assumption that

there are valid reasons for government involvement (such as market failures or merit goods). These OECD conditions are listed below. We have added some examples from the cultural policy field:

1. Administrative economies of scale and scope: tax incentives might lead to less administrative costs than direct subsidies. For example: given a cultural policy goal of private ownership of art, an exemption of privately owned art from wealth tax is more cost efficient than taxing (and to assess the value of) these objects on a yearly basis and give a direct subsidy for private ownership of art. 2. Limited probability of abuse or fraud: where detailed verification is

not necessary, a tax benefit can be cost-effective, especially as information from third sources is available which can be used to check the claim of the tax payer. An example is the deduction of gifts in case charities are obliged to report the gifts they have received to the Tax Agency.

3. A proper wide range of taxpayer choice: in case of wide ranges of private preferences the distinctions among different activities that properly qualify for governmental support may not be considered important in which case a simpler reporting and verification process through the tax system might be thought to be more efficient than a direct subsidy. An example can be an exemption of museums form gift and inheritance tax.

4. Measurement of taxpaying capacity: deductions or exclusions from

23 OECD, Tax Expenditures in OECD Countries, Paris: OECD 2010, p. 24-25,

http://www.oecd.org/gov/budgeting/taxexpendituresinoecdcountries-oecdpublication.htm (accessed on 24 November 2014).

income can be justified as proper measurements of the ability to pay tax, or as essential to measure income accurately. An example can be the deduction of maintenance costs for privately owned monuments. However, the OECD acknowledges that this criterion might be problematical as under many applications of the tax expenditure concept, such deductions or exclusions could be considered structural features of the tax system rather than tax expenditures. This brings us back to the discussion on the ‘primary structure’ of a tax.

Taking into account the criterions mentioned above and provided the requirements regarding accountability and evaluations are met, tax incentives can be an efficient and effective instrument to achieve the following cultural policy goals:

a) Creating a bond between the public and cultural institutions; b) Raising funds quickly to preserve cultural heritage;

c) Preserving privately owned cultural heritage;

d) Ensure access to privately owned cultural and natural heritage. Below we will argue why this is the case, using examples of tax incentives for each policy goal.

4 Create a bond between the public and cultural institutions

4.1 Tax incentives for private giving

In Europe, cultural institutions are often mainly funded by direct subsidies of local or national governments. However, many national

6

figure 2: tax incentive

(2b) 50 tax

(2a) 50 deduction

(1) 100 donation

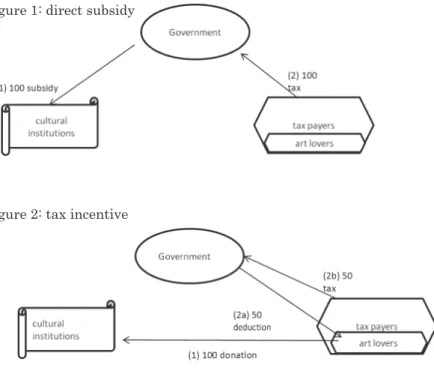

An important difference between the two graphs is that in figure 1 there is no direct financial relation between the cultural institutions and the art lovers, the public. The government (or a governmental agency or committee) decides which cultural institutions get which amount of money and all tax payers have to fund this. The art lovers are not given any responsibility for sustaining the arts. This might have the effect that cultural institutions focus on the government and their advisory bodies and forget about the preferences of their public. In the Netherlands this had the effect of populist parties claiming that the arts were merely ‘hobbies of left wing politicians’ for which general tax payers were no longer willing to pay, resulting in huge cuts on subsidies for the arts when this populist party became part of the government.

Tax incentives, however, do create a bond between art lovers and cultural institutions and reduce the costs of all tax payers. The starting point is the decision of the art lover to make a donation. The result is a deduction for income tax purposes. As an example weI have chosen an income deduction against a tax rate of 50%, but a lower deduction, for example by using a fixed tax credit, is of course possible as well. Only this deduction and not the whole gift have to be funded by all tax payers. The result is, therefore, not only that cultural institutions have to take into account the preferences of their public and create a bond with them in order to attract donations, but also that all tax payers only have to pay part of the costs. The other part is financed by the art lovers. We do not claim that all direct subsidies for cultural institutions must be replaced by tax incentives.

figure 1: direct subsidy

(1) 100 subsidy (2) 100 tax 書式変更: フォントの色 : 自動, 上付き/下 付き(なし) 書式変更: フォントの色 : 自動, 上付き/下 付き(なし)

governments also fund cultural institutions indirectly, by granting tax incentives for cultural giving. An example is the deductibility of gifts to museums, theatres and other cultural institutions. The graphs below show the difference between these two ways of funding the arts:24

figure 1: direct subsidy

figure 2: tax incentive

An important difference between the two graphs is that in figure 1 there is no direct financial relation between the cultural institutions and the art lovers, the public. The government (or a governmental agency or committee) decides which cultural institutions get which amount of money and all tax payers have to fund this. The art lovers

24 S.J.C. Hemels, Giftenaftrek afschaffen ten bate van vooringevulde aangifte?

are not given any responsibility for sustaining the arts. This might have the effect that cultural institutions focus on the government and their advisory bodies and forget about the preferences of their public. In the Netherlands this had the effect of populist parties claiming that the arts were merely ‘hobbies of left wing politicians’ for which general tax payers were no longer willing to pay, resulting in huge cuts on subsidies for the arts when this populist party became part of the government.

Tax incentives, however, do create a bond between art lovers and cultural institutions and reduce the costs of all tax payers. The starting point is the decision of the art lover to make a donation. The result is a deduction for income tax purposes. As an example we have chosen an income deduction against a tax rate of 50%, but a lower deduction, for example by using a fixed tax credit, is of course possible as well. Only this deduction and not the whole gift have to be funded by all tax payers. The result is, therefore, not only that cultural institutions have to take into account the preferences of their public and create a bond with them in order to attract donations, but also that all tax payers only have to pay part of the costs. The other part is financed by the art lovers.

We do not claim that all direct subsidies for cultural institutions must be replaced by tax incentives. For certain costs, such as security, heating, accounts and other exploitation costs, it can be difficult to attract private funds. Such base costs could still be funded by direct subsidies. Nevertheless, private gifts are for several reasons very important for cultural institutions:

an additional source of income next to government subsidies, leading to more funding.

b) Strengthening the financial base of cultural institutions: gifts of private individuals are less sensitive to political and economic changes provided cultural institutions have created a bond with the art lovers;

c) Strengthening the social base of cultural institutions: private gifts provide an opportunity to create and foster a bond with the public. Tax incentives can promote these private gifts and contribute to achieving these possible objectives of cultural policy.

4.2 Tax incentives for volunteers

Not only gifts in the form of money and objects are important means to create a bond between cultural institutions and the public. Also a donation of time, volunteering, can achieve this object. Also, volunteers can reduce costs of cultural institutions and make activities possible which could otherwise not take place. Donation of time is not limited to rich people. In fact, it enables lower income groups, such as unemployed and retired people to become engaged in cultural institutions. Activities of volunteers can take many forms, for example providing guided tours in a museum (this can be seen in many Japanese museums, an example is the Edo-Tokyo Museum in Tokyo25),

helping with the indexation and maintenance of museum objects (for example, in the Amsterdam Museum volunteers help out in indexing

25 http://edo-tokyo-museum.or.jp/english/information/index.html (accessed on 24

and restoring the collection of costumes26) and providing information at

information desks.

In the Netherlands, volunteer activities are stimulated by a tax incentive in the wage and income tax. A reimbursement for volunteers is not taxed if this does not exceed EUR 1500 (approximately JPY 220 000) per year, EUR 150 (approximately JPY 22 000) per month and EUR 4. 50 (approximately JPY 660) per hour.27 Furthermore, if a

volunteer has a right to receive such reimbursement and the cultural institution is able and willing to pay out this reimbursement, but the volunteer refuses the reimbursement, he can deduct the reimbursement which he did not want to receive as a gift for personal income tax purposes.28 Next to these incentives for volunteers,

charities, including cultural institutions, which are liable to corporate income tax (this is a minority as most Dutch charities are exempt from this tax) with volunteers can get a special corporate income tax deduction.29 These institutions can deduct the net costs (after real

costs) which they would have had if they would have had to pay the volunteers the minimum wage for their activities. Through these tax incentives the Netherlands makes volunteering more attractive. This does not only serve cultural policy goals, but also social policy goals such as providing work experience for the unemployed and making sure that people without work (including housewives and pensioners)

26 http://hart.amsterdammuseum.nl/31611/nl/vrijwilligers (accessed on 24

November 2014).

27 Article 2(6) Wet op de loonbelasting 1964 [Dutch Wage tax Act 1964] and article

3.96(c) Wet inkomstenbelasting 2001 [Dutch Personal income tax Act 2001].

28 Article 6.36(1) Wet inkomstenbelasting 2001 [Dutch Personal income tax Act

2001].

29 Article 9(1) (h) Wet op de vennootschapsbelasting 1969 [Dutch corporate income

feel part of the society.

In Japan, there is no special income tax treatment for volunteer activities.30

5 Raising funds quickly to preserve cultural heritage

Not all works of art which are regarded as having great importance for a country are owned by the government. Some of these works of art are still privately owned. When the owner dies, the heirs will have to pay inheritance tax over these works of art. This might be an additional incentive for the heirs to sell the works of art on a (foreign) auction. Museums or the government will not always be able to acquire the necessary funds in time to buy the works of art. By the time they have gone through all the bureaucratic procedures, the particular work of art may already have been sold. This means that after an auction the art may be lost to the public, or even to the country if it is bought by a foreigner. In the case of heritage buildings, in some circumstances such a sale might lead to their demolition.

In order to prevent this and to preserve important national heritage, many European countries have introduced the option of paying inheritance tax, and in some countries other taxes, by transferring such cultural heritage to the state. The tax incentive has the advantage that the budget is already there, which enables the government to act quickly. It is important to note that not every work of art can be used to pay taxes: the cultural heritage has to be of significant cultural or

30 Yoshihiro Masui, Volunteer activities and charitable contribution deduction,

historical value to the country in question and most countries have special committees that advise on the acceptance (or rejection) of cultural heritage. Such cultural heritage might include works of art, manuscripts, archives, heritage objects and historic documents.

In England this tax incentive is referred to as “acceptance in lieu of tax” and in France as “dation”. England and France have a relatively long and successful tradition of using this tax incentive: in England it was first introduced in 1910 for historic buildings and over time it was offered for other cultural heritage, such as works of art. English and French governments and museums give a lot of publicity to the incentive and its successes.31

Other European countries with similar tax incentives are the Netherlands, Ireland, Italy, Belgium and Spain. In most countries 100% of the value of the work of art is taken into account to establish the amount of tax which should be paid. However, in the Netherlands, 120% of the value is taken into account. This means that for a work of art with a value of €100,000, an inheritance tax assessment of 120,000 Euro may be paid.

In various countries this tax incentive has been important in acquiring major works of art which are now on public display. The Musée Picasso in Paris is a good example of the success of the French incentive, as its existence is a direct result of the use of the dation after the death of Picasso and later of his wife, Jacqueline.32 It might not have been

31 For example in England:

http://www.artscouncil.org.uk/what-we-do/supporting-museums/cultural-property/tax-incentives/acceptance-lieu/ (accessed on 24 November 2014).

32 http://www.museepicassoparis.fr/collections/presentation/ (accessed on 24

possible to acquire these important works of art through direct subsidies.

Most countries only allow the paying of inheritance tax with art. However, some countries, such as Ireland, Spain and Italy also allow other taxes to be paid for through cultural heritage. These tax incentives may benefit companies and so offer governments other opportunities to retain important cultural heritage. In Ireland, for example, this can be used to deduct a tax credit from income tax, corporation tax, capital gains tax, gift tax or inheritance tax liabilities (including interest and penalties).33 Through this tax incentive, the

National Library of Ireland managed to acquire a previously unknown six-page James Joyce manuscript in spring 2006. The Allied Irish Bank bought this manuscript for EUR 1.17 million (approximately JPY 171 million) at auction with the purpose of donating it to the National Library and crediting the value against its corporation tax liabilities. It would probably not have been possible for the National Library itself to raise the funds in time to buy this important manuscript at auction. Therefore, the incentive made it possible to preserve the manuscript for Ireland and make it available to the public and researchers.

These examples show that the possibility to pay inheritance- and other taxes with important works of art can be an effective and efficient way to achieve the cultural policy goal of preserving important cultural heritage for the nation.

In Japan it is also possible to pay inheritance tax with land, buildings or art. However, as the government must sell the property on an auction to obtain a budget, this system is not an incentive for the

33 Section 1003, Taxes Consolidation Act, 1997, http://www.irishstatutebook.

preservation of historical or cultural heritage. An example is the historic building where Empress Michiko was born. After her father died in 1999, it was offered to the Government in lieu of inheritance tax. Officials decided to demolish the house and auction off the land. It is regrettable that the incentive is only used to obtain a budget and is not used as an instrument to preserve important cultural heritage for the country and future generations.

6 Preserving privately owned cultural heritage: tax

incentives for monuments

It is impossible for the government to own all monuments in a country and maintain them. An example is Amsterdam’s 17th century Canal Ring which was added to the UNESCO World Heritage List in 2010. The canal houses which line these canals and are an important characteristic of the Canal Ring. Many canal houses are registered monuments. These houses were built by individuals and the majority of these houses is still privately owned, both by individuals and companies. The maintenance of this important characteristic of the Canal Ring has, therefore, mainly been a private affair. The government wants to make sure that these monuments are preserved. A special tax incentive is one of the means to pursue this cultural policy goal.

Where maintenance costs of houses are, in general not deductible in the Netherlands, individuals owning a registered building of historical interest can deduct 80% of certain maintenance and restoration costs

from their taxable income.34 The reason behind this is that the

government cannot afford to subsidise the maintenance of all such buildings in the Netherlands but by providing for a tax incentive, the government can reduce the costs for private owners of these heritage buildings. Furthermore, it is expected that private owners will take good care of the buildings given that they are a close concern of theirs. Therefore, society as a whole benefits from this private preservation as it is a way to maintain buildings of historical interest.

In Japan, it is not possible to deduct the maintenance cost of historical buildings from income. Only, if a tax payer obtains income from property, he can deduct the costs. Otherwise, the maintenance costs cannot be deducted. However, in some municipalities special measures are included in the local property tax. For example, important cultural property, such as certain traditional and historic buildings, is exempt from property tax or taxed at a reduced rate.

In Japan, in order to support privately owned important cultural property, some special rules of inheritance tax valuation apply. For example, the value of houses which are important cultural property is set at 30% of the fair market value.35 The owner is not obliged to open

the house to the public.

7 Ensure public access to privately owned cultural and

natural heritage

Private collections may be very interesting for a broader audience.

34 Article 6.31 Wet inkomstenbelasting 2001 [Dutch Personal income tax Act

2001].

However, for the private owner of art, giving a work on loan to a museum or making a collection accessible for the public has many disadvantages. It leads to additional costs, for example for security, transport and insurance, risks, for example of damage and hassle. To stimulate private owners of art to open their collection or cultural heritage to the public notwithstanding these disadvantages, countries have introduced various tax incentives.

For example, under the French Patronage Act France has introduced a tax incentive to retain significant cultural heritage (“tremors nationaux”) for the country. If the owner of cultural heritage wants to export it, he must acquire an export license, which the French state might choose to temporarily refuse whilst it tries to find the funds to buy the object. However, this will not always be possible, in which case companies resident in France may request approval of the French State to buy the object by taking advantage of a specially designed tax incentive. If the approval is granted, the company may deduct 40% of the purchase price from its taxable profit and is obliged to give the object on loan to a French museum, public archive or state library for a period of at least 10 years. During this 10 year period the company is not allowed to transfer ownership of the cultural heritage. Another tax incentive provision of the French Patronage Act grants companies a deduction if they acquire works from living artists and put them on permanent display at a location accessible to the public. This location may be a museum but also a company’s entrance foyer to which the general public is granted access. If all requirements are met, the company may for tax purposes deduct one-fifth of the purchase price over a period five years, with the maximum yearly tax deduction set at 0.5% of the annual turnover of the company. This tax incentive not only

gives artists the opportunity to sell their works, but also enables them to build a reputation. Furthermore, it enables the public to get acquainted with modern art. France grants a similar tax incentive to companies that buy musical instruments and, upon request, give them on loan to musicians. This tax incentive enables talented artists to play valuable instruments, from which not only the musician, but also his audience benefits.

The Netherlands applies several tax incentives on privately owned registered estates of natural beauty. Such estates of natural beauty are defined as estates in the Netherlands with nature and forests which may include a building as long as the building (for example a monumental house) adds to the natural beauty.36 The owner has the

obligation to preserve the estate and to further the natural beauty. In 1928 the first tax incentive for such estates of natural beauty was introduced in the Netherlands to prevent that the heirs had to sell or divide the estate to pay the inheritance tax. Still, an important tax incentive for such estates is the full exemption of gift and inheritance tax if the estate (not necessarily the house) is open to the public and is maintained for at least 25 years.37 Other tax incentives apply as well:

no real estate transfer tax upon the transfer of such estates,38 no

municipal real estate tax over the grounds,39 no wealth tax over the

grounds40 and an exemption of corporate income tax for incorporated

36 Article 1(a) Natuurschoonwet 1928 [Dutch Natural beauty Act 1928]. 37 Article 7 Natuurschoonwet 1928 [Dutch Natural beauty Act 1928]. 38 Article 9a Natuurschoonwet 1928 [Dutch Natural beauty Act 1928]. 39 Article 220d (d) Gemeentewet [Dutch Municipal Act].

40 Article 5.7(1) (c) Wet inkomstenbelasting 2001 [Dutch Personal income tax Act

estates of natural beauty.41 These tax incentives may be a reason not to

build on the land but to preserve it. Such estates are often also supported with private gifts.

In Japan, the Act on Public Display of Art at Museums was introduced in order to promote the public display of important art works in 2000. The Agency for Cultural Affairs registers art works according to the act. The act makes it easy to pay inheritance tax for the owners of the registered art works.42 This may be an incentive for the owners of the

registered art works. Because priority of payment in kind is defined in the inheritance tax law.

First: government bonds, municipal bonds, real estate and ships Second: commercial bonds, shares

Third: movable property

Art works are included in the movable property. However, if the art works are registered, priority of payment in kind rises from third to first by special measures.

8 Conclusion

Before opting for a tax incentive, it must be made clear that a tax incentive is indeed the most effective and efficient option to achieve the policy goal and its accountability and evaluation must be ensured. If these requirements are met, tax incentives can play an important role in achieving goals of cultural policy. Best practices of other countries can be an inspiration, also for Japan, in applying tax incentives to

41 Article 5(1) (a) Wet op de vennootschapsbelasting 1969 [Dutch corporate income

tax Act1964].

achieve certain policy goals. 執筆者

Sigrid J.C. Hemels

Professor of Tax Law at the School of Law of Erasmus University Rotterdam, the Netherlands

(エラスムス大学ロッテルダム 法学部 教授)

柴 由花(常葉大学 法学部 准教授)

英文タイトル

Tax legislation as instrument to support private patronage of the arts and cultural heritage