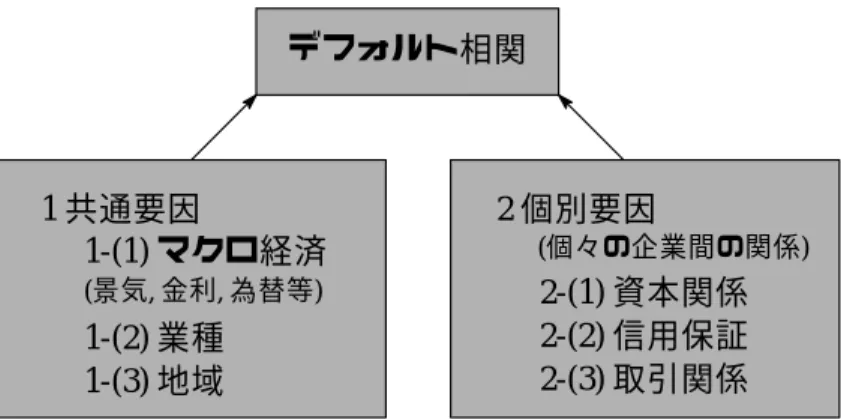

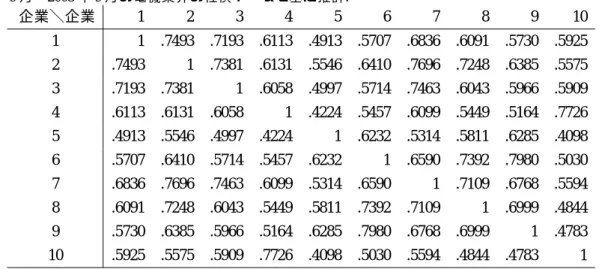

デフォルト相関係数のインプライド推計( )

全文

図

![表 3: 電機ポートフォリオのハザード過程の推定結果 Bloomberg より取得した 1998 年 9 月〜2003 年 9 月までの日次社債データを元に推定. 企業\項目 長期平均 (h) 平均回帰係数 (b) ボラティリティ (σ) デフォルト確率 (P [τ ≤ 1]) 1 .0106 .4572 .0050 .0178 2 .0060 1.0624 .0046 .0101 3 .0110 -1.1132 .0052 .0272 4 .0093 .0768 .0050 .0171 5 .0091 1](https://thumb-ap.123doks.com/thumbv2/123deta/8084341.850788/15.892.117.772.229.518/ポートフォリオハザード日次データ長期ボラティリティデフォルト.webp)

関連したドキュメント

We generalized Definition 5 of close-to-convex univalent functions so that the new class CC) includes p-valent functions.. close-to-convex) and hence any theorem about

In the previous section we have established a sample-path large deviation principle on a finite time grid; this LDP provides us with logarithmic asymptotics of the probability that

Since the copula (4.9) is a convex combination of elementary copulas of the type (4.4) and the operation of building dependent sums from random vector with such copulas is

Since the copula (4.9) is a convex combination of elementary copulas of the type (4.4) and the operation of building dependent sums from random vector with such copulas is

As the number of firms in the triangular network increases, the Kolmogorov statistic D increases, thus allowing us to reject the null hypothesis that the copula of the counterparty

To overcome the drawbacks associated with current MSVM in credit rating prediction, a novel model based on support vector domain combined with kernel-based fuzzy clustering is

Vovelle, “Existence and uniqueness of entropy solution of scalar conservation laws with a flux function involving discontinuous coefficients,” Communications in Partial

TANK MIXTURES: Up to 48 fluid ounces of this product per acre may be applied postemergence (in-crop) over the top of Roundup Ready alfalfa in the seeding year in a tank-mix with