How is the trading volume of Bitcoin determined?

著者(英) Yutaka Kurihara

journal or

publication title

Doshisha Shogaku (The Doshisha Business Review)

volume 70

number 6

page range 747‑755

year 2019‑03‑15

権利(英) Doshisha Daigaku Shogakkai

The Association of Commerce Doshisha University

URL http://doi.org/10.14988/pa.2019.0000000045

How Is the Trading Volume of Bitcoin Determined?

Yutaka Kurihara

Introduction Theoretical Analysis Data

Empirical Analysis Conclusions

Abstract

Bitcoin, which is a cryptocurrency, is not a legal currency but a privately managed monetary system. It does not depend on central banks or governments. Since the introduction of Bitcoin, its trading volume has rapidly increased. This paper aims to examine whether or not the trading volume of Bitcoin are significant drivers. The determinant elements of Bitcoin prices have been discussed and studied a lot, but the relationship between the volume and the prices has not been analyzed much. This paper focuses on this issue. The empirical results show that the volume of Bitcoin is determined by the prices. However, the relation has appeared since the introduction of the Bitcoin. Bitcoin’s transactions seem to be becoming efficient.

JEL classification numbers: E42, E44, E51

Key words: Bitcoin, efficient market, price of Bitcoin, volume of Bitcoin

Introduction

Bitcoin is a typical cryptocurrency, which is not a legal currency but a private managed monetary system. Bitcoin does not depend on central banks or governments. Since the starting of the transaction, it has received much attention. The volume of this currency has been increasing largely and rapidly. Some serious incidents have occurred all over the world again and again, however, Bitcoin may have overcome such serious conditions by now.

Bitcoin is a new and different kind of currency from other existing currencies. One characteristic is that Bitcoin is not a simple digital cash, which has been used all over the world. Unlike central bankand governmentissued currencies, Bitcoin can be inflated at will, and the supply of Bitcoin is limited to a certain volume, which cannot be changed. Instead, the usage of Bitcoin allows users to send or receive any amount of money to anyone at a very cheap cost compared to other traditional financial instruments. Payments can be performed efficiently. Bitcoin payments are impossible to block, and Bitcoin wallets cannot be closed.

(747)141

Short of turning off the Internet and keeping it turned off, the Bitcoin network can be unstoppable. Although Bitcoin confers much freedom, it also demands user responsibility, but the rewards are well worth the user’s time (Bitcoin homepage, retrieved on August 16, 2018).

These new and drastic characteristics attract users, and Bitcoin has been accepted all over the world. From the introduction, most people believed that Bitcoin is too risky for transactions to use. However, Bitcoin has been used for many kinds of transactions and by many users.

Bitcoin has received much attention from the real world and from the academic field. Brѐre, Oosterinck, and Szafarz (2015) indicated that Bitcoin confers diversification of financial instruments. Dyhrberg (2016) showed that Bitcoin can hedge risks arising from financial transactions. However, as indicated by Seigh (2015), Bitcoin has also been employed for speculation. Cheah and Fry (2015) showed that the fundamental price of the Bitcoin is zero, and Bitcoin has exhibited speculative bubble elements.

At this point, the price stability of Bitcoin is important because it relates directly to economic activity. For this paper’s theme, the volume seems to be related with the prices. If Bitcoin prices fluctuate largely or suddenly lose value, market participants do not use them, which can damage efficient allocation of resources in the economy. As the liquidity of Bitcoin is quite large, the effect of the price on its volume could be large. Bitcoin users consider measures to avoid or reduce systemic risks, and the influence from a failure of only one participant in a payment or settlement system will spread. A sound and stable payment system is necessary to maintain and boost the Bitcoin market economy. A stable currency and financial system promote economic growth; on the other hand, instability may cause serious economic turmoil and damage to the economies. It is necessary to examine the prices of Bitcoin, but few studies have tackled this problem yet.

This paper examines the price efficiency of Bitcoin. Jakub (2015) and Kurihara and Fukushima (2017) showed that Bitcoin follows the hypothesis of efficient markets. Khuntia and Pattanayak (2018) indicated that market efficiency evolves with time and validates the adaptive market hypothesis. Tiwari, Jana, Das, and Roubad (2018) also found the Bitcoin market to be informationally efficient. On the other hand, Urquhart (2016) showed that the Bitcoin market has been inefficient.

Many studies have examined foreign exchange markets and exchange rates such as the same or substitute asset prices from the views of theoretical aspects and empirical aspects. Yamori and Kurihara (2004) is this one. Among them, market efficiency with Bitcoin has also received much attention, and many analyses have been conducted. Whether or not covered interest parity (CIP) or uncovered interest parity (UIP) holds has been thoroughly analyzed

同志社商学 第70巻 第6号(2019年3月)

142(748)

(see, e.g., Fama (1984), Sarno, Valente, and Leon (2006), and Batten and Szilagyi (2010)).

Ciaian, Rajcaniove, and Kancs (2016) found that as long as Bitcoin prices are not moved by speculative investments, Bitcoin will not be able to compete with traditional currencies.

Almudfaf (2018) discovered that there is a significant and persistent premium with an average 44% in Bitcoin. Su. Li, Tao, and Si (2018) showed that there have been four explosive bubbles in China and the U.S. Bitcoin markets. Brauneis and Mestel (2018) indicated that cryptocurrency prices became less predictable. Phillip, Chan, and Peris (2018) suggested that cryptocurrencies have unique characteristics including leverage effects and studentt error distributions. Bouri, Azzi, and Drhrberg (2017) showed no evidence of an asymmetric return

volatility relationship in Bitcoin markets. Stavroyiannis (2017) found that Bitcoin is a highly volatile price currency violating the valueatrisk measures more than the other assets. Zhu, Dickinson, and Li (2017) discovered that Custom price index, U.S. dollar index, Dow jones industry average, Federal Funds Rate, and gold price influence Bitcoin price. Delikanli and Vogiazas (2018) demonstrated that Bitcoin returns are significantly linked with in the short

run with the CBOE Volatility Index, the CBOE S&P 500, and the 12month Euribor rate.

Sukamulja and Sikora (2018) indicated that the macroeconomic indicator is the demand for Bitcoin, and the gold price influences Bitcoin’s price fluctuations in the shortand longrun.

Polasik, Piotrowska, Wisniewski, Kotkowski, and Lightfoot (2015) found that Bitcoin’s return is influenced by Bitcoin’s popularity, the sentiment expressed in newspaper reports on cryptocurrency, and total number of transactions. Gandai, Hamrick, Moore, and Oberman (2018) discovered that suspicious trading activities caused the unprecedented change in the USDBitcoin exchange rate in late 2013. Kj, Meland, and Qust (2018) indicated that the volumes of Bitcoin and Bitcoins’ prices have negative relationships.

This study is related with this subject. Many papers about Bitcoin examine the prices, however, unique among these studies, this paper examines how the trading volume of the Bitcoin is determined.

This article is structured as follows : Section 2 provides a model for Bitcoin volume determinants. Section 3 explains the data employed here. Section 4 reveals the empirical results and provides the analyses. Finally, section 5 gives a brief conclusion.

Theoretical Analysis

This paper examines how the trading volume of Bitcoin is determined. To study the dynamics of the Bitcoin’s trading volume, regression analyses and vector autoregressive

How Is the Trading Volume of Bitcoin Determined?(Kurihara) (749)143

(VAR) models are used for estimations. Let %$be a vector that contains the variables, so a VAR reads as follows the equation (1).

%$#!"!

"#!

# !"%$!"""$ (1)

where c is a vector of constants and"is a vector of independent white noise innovation. The laglength is determined using the Schwartz Bayesian information criterion. This model investigates the dynamics between the trading volume of Bitcoin and the prices. Whether or not the prices influence the trading volume of Bitcoin is examined empirically.

Data

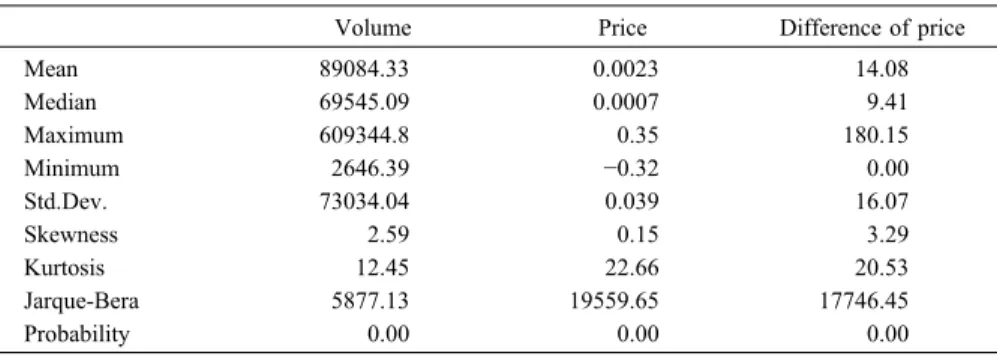

The Bitcoin data are from www.bitcoinaverage.com, which is the aggregated Bitcoin indexes that include daily prices, highest/lowest prices, and trading volume after the data are converted from all available Bitcoin markets. First, data that are converted level into rate are used for estimation. All of the data are stationary according to an augmented DickeyFuller (ADF) test. The change rate of the Bitcoin prices is integrated at order one and becomes stationary (price), and the difference of the highest one and the lowest one is also employed (difference of price). The sample period is from 7/17/2010 to 12/29/2016. The descriptive statistics of Bitcoin for the whole period are shown in Table 1.

There appears to be more than small differences among the days. The mean, skewness, and kurtosis are all positive.

Table 1 Descriptive Statistics of Bitcoin

Volume Price Difference of price

Mean Median Maximum Minimum Std.Dev.

Skewness Kurtosis JarqueBera Probability

89084.33 69545.09 609344.8 2646.39 73034.04 2.59 12.45 5877.13 0.00

0.0023 0.0007 0.35

−0.32 0.039 0.15 22.66 19559.65 0.00

14.08 9.41 180.15 0.00 16.07 3.29 20.53 17746.45 0.00 同志社商学 第70巻 第6号(2019年3月)

144(750)

Empirical Analysis

Using the data in the previous section 3, empirical analyses are conducted to examine how the trading volume of Bitcoin is determined. The sample period from the start to the end of the year of 2016 is divided into two time periods (first and second). The empirical results are in shown in Table 2 a and 2 b.

The results are almost expected. The rising prices of Bitcoin causes the increase in trading volume of Bitcoin. However, the coefficients in the first part are not significant, so it seems that the Bitcoin market is becoming efficient.

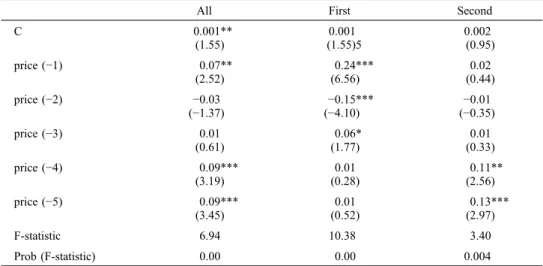

The VAR model is estimated according to equation (1). The volume and price of Bitcoin are estimated, and the lag of the equation is selected Schwarz Bayesian information criterion.

The results are in Table 3 a and 3 b.

Table 2 a Regression Analysis for Trading Volume

All First Second All First Second

C 88692.67***

(42.36) 92669.07***

(40.30) 82905.96***

(21.08) 60020.50***

(24.14) 50748.09***

(26.07) 66459.93***

(12.76)

Price 164691.8***

(3.07) 41198.04

(0.45) 209041.8***

(2.84)

Difference of price 2063.047***

(28.56) 3386.75***

(32.63) 1028.92***

(4.89)

Fstatistic 9.44 0.20 8.07 314.60 1065.35 23.98

Prob (Fstatistic) 0.002 0.64 0.004 0.00 0.00 0.00

Note.***denotes significance at 1%, **at 5%, and *at the 10% level. Figures in parentheses are tstatistics.

Table 2 b Regression Analysis for Anomaly

All First Second

C 59653.24***

(24.07) 50775.15***

(26.05) 65547.03***

(12.67)

Price 163979.4***

(3.43) −25529.31

(−0.44) 216732.6***

(3.01)

Difference of price 2062.71***

(17.81) 3388.37***

(32.61) 1042.39***

(5.00)

Fstatistic 164.60 532.18 16.75

Prob (Fstatistic) 0.00 0.00 0.00

Note.***denotes significance at 1%, **at 5%, and *at the 10% level. Figures in parentheses are tstatistics.

How Is the Trading Volume of Bitcoin Determined?(Kurihara) (751)145

The results are not so clear. However, before or after prices can sometimes have effects on the trading volumes and prices. On the other hand, it is quite difficult to find robust patterns.

Finally, the impulse response of the volume of Bitcoin is estimated as the regression results are not so clear. Figure 1 is the result, and it is almost clear. The shock disappears gradually in a few days.

Table 3 a VAR analysis(volume)

All First Second

C 13826.70***

(5.73) 21877.15***

(5.78) 9343.45***

(2.85)

Volume (−1) 0.65***

(22.76) 0.61***

(16.58) 0.68***

(14.94)

Volume (−2) 0.02

(0.68) 0.008

(0.20) 0.03

(0.66)

Volume (−3) −0.02

(−0.59) −0.06

(−1.41) 0.02

(0.52)

Volume (−4) 0.04

(1.38) 0.04

(1.11) 0.03

(0.57)

Volume (−5) 0.14***

(5.05) 0.15***

(4.25) 0.10**

(2.41)

Fstatistic 339.24 119.90 211.92

Prob (Fstatistic) 0.00 0.00 0.00

Note.***denotes significance at 1%, **at 5%, and *at the 10% level. Figures in parentheses are tstatistics.

Table 3 b VAR analysis(price)

All First Second

C 0.001**

(1.55)

0.001 (1.55)5

0.002 (0.95)

price (−1) 0.07**

(2.52)

0.24***

(6.56)

0.02 (0.44)

price (−2) −0.03

(−1.37)

−0.15***

(−4.10)

−0.01 (−0.35)

price (−3) 0.01

(0.61)

0.06*

(1.77)

0.01 (0.33)

price (−4) 0.09***

(3.19)

0.01 (0.28)

0.11**

(2.56)

price (−5) 0.09***

(3.45)

0.01 (0.52)

0.13***

(2.97)

Fstatistic 6.94 10.38 3.40

Prob (Fstatistic) 0.00 0.00 0.004

Note.***denotes significance at 1%, **at 5%, and *at the 10% level. Figures in parentheses are tstatistics.

同志社商学 第70巻 第6号(2019年3月)

146(752)

Conclusions

This paper examined how volumes of Bitcoin are determined. The results show that volumes of Bitcoin are affected by the prices of Bitcoin. It is interesting to note that the prices of Bitcoin are not deterministic elements for the first of the half period from the beginning.

There seems some possibility that market efficiency has been gradually accomplished. Also, the shock of volume disappears gradually. It seems that Bitcoin has been gaining stability

Table 3 c VAR analysis(price difference in a day)

All First Second

C 0.001

(0.66) −0.001

(−0.85) 0.005

(1.32)

dprice (−1) 5.12 E−05

(0.60) −8.51 E−06

(−0.09) 7.87 E−05

(0.53)

dprice (−2) 0.0001**

(2.13) 0.0002**

(2.09) 0.0001

(1.03)

dprice (−3) −7.83 E−05

(−0.87) 2.36 E−05

(0.23) −0.0001

(−1.11)

dprice (−4) −0.0002***

(−2.93) −0.0001

(−1.62) −0.0003**

(−2.32)

dprice (−5) 0.0001**

(2.17) 0.001**

(1.97) 0.0001

(1.05)

Fstatistic 3.35 2.96 1.73

Prob (Fstatistic) 0.005 0.011 0.12

Note.***denotes significance at 1%, **at 5%, and *at the 10% level. Figures in parentheses are tstatistics.

Figure 1 Impulse response of the volume of Bitcoin

How Is the Trading Volume of Bitcoin Determined?(Kurihara) (753)147

through transaction.

Bitcoin is surely related to other kinds of financial assets. For example, coordination channeled through foreign exchange market interventions may be effective because they attract the fundamentals if the original prices of Bitcoin are efficient. Some studies have shown that central bank interventions tend to increase exchange rate volatility. There may be some room for further research on Bitcoin.

Beer and Weber (2014) suggested that the network and financial services related to Bitcoin are not regulated and that customers should take appropriate measures to protect their holding Bitcoin. On the other hand, as found by William (2016), Bitcoin should overcome reduced regulatory issues as they contain some legal or regulatory problems. McCallum (2015) stated,

“There exists a rather prominent possibility that the U.S. government will take legal measures to constrain or banish the Bitcoin system (p.347)”. Maftei (2014) discovered that Bitcoin transactions have grown rapidly, which may catalyze regulation measures or legal approval of governments. However, Bitcoin could provide new hopes for greater freedom in terms of volume, payment instruments, anonymity, and so on. For the various kinds of information, the share will be dynamic and evolves significantly over time (Brandvold, Molnar, Vagstad, Andreas, & Ole, 2015). Sound trading and boosting economies via Bitcoin is expected.

Acknowledgments

I appreciate Dr. Fujiwara for his great contribution to the Japanese academic fields. This work was supported by the Nitto Foundation.

References

Almudfaf, F. (2018). Pricing efficiency of Bitcoin trusts.Applied Economics Letters, 25,504508.

Batten, J. A., & Szilagyi, P. G. (2010). Is covered interest parity arbitrage extinct? Evidence from the Spot USD/

Yen.Applied Economics Letters, 17(3), 283287.

Beer, C., & Weber, B., (2014) Bitcoin : The promise and limits of private innovation in monetary and payment systems.Monetary Policy and the Economy,Q 4/14.

Brѐre, M., Oosterinck, K., & Szafarz, L. (2015). Virtual currency, tangible return : Portfolio diversification with Bitcoin.Journal of Asset Management, 16(6), 365373.

Bouri, E., Azzi, G., & Drhrberg, A. H. (2017). On the returnvolatility relationship in the Bitcoin market around the price crash of 2013,Economics, 11(2), 117.

Brandvold, M., Molnar, P., Vagstad, K., Andreas, V., & Ole, C. (2015). Price discovery on Bitcoin exchange.

Journal of International Financial Markets, Institutions and Money, 36,1835.

Brauneis, A. & Mestel, R. (2018). Price discovery of cryptocurrencies : Bitcoin and beyond.Economics Letters, 165,5861.

Cheah, E. T., & Fry, J. (2015). Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin.Economic Letters, 130,3236.

Ciaian, P., Rajcaniove, M., & Kancs, D. (2016). The digital agenda of virtual currencies : Can Bitcoin become a 同志社商学 第70巻 第6号(2019年3月)

148(754)

global currency?Information Systems and eBusiness Management, 14(4), 883919.

Delikanli, I. U., & Vogiazas, S. (2018). Testing for the presence of speculative price bubbles in Bitcoin.Istanbul Ticaret Universitesi Sosyal Bilimler Dergisi, 17,511523

Dyhrberg, A. H. (2016). Bitcoin, gold and the dollar : A GARCH volatility analysis.Finance Research Letters, 16,8592.

Fama, E. (1984). Forward and spot exchange rates.Journal of Monetary Economics, 14,319338.

Gandai, N., Hamrick, J. T., Moore, T., & Oberman, T. (2018). Price manipulation in the Bitcoin ecosystem.

Journal of Monetary Economics, 95,8696.

Jakub, B. (2015). Does Bitcoin follow the hypothesis of efficient market? International Journal of Economic Sciences, 4(2), 1023.

Khuntia, S., & Pattanayak, J. K. (2018). Adaptive market hypothesis and evolving predictability of Bitcoin.

Economics Letters, 167,2629.

Kj, F., Meland, M., & Qust, A. (2018). How can bitcoin price fluctuations be explained?International Journal of Economics and Financial Issues, 8(3), 323332.

Kurihara, Y., & Fukushima, A. (2017). The market efficiency of Bitcoin : A weekly anomaly perspective.

Journal of Applied Finance & Banking, 7(3), 5764

Maftei, L. (2014). Bitcoin : Between legal and informal.CES WorkingPapers, 6(3), 5359.

McCallum, B. T. (2015). The Bitcoin revolution.Cato Journal, 35(2), 347356.

Phillip, A., Chan, J. S. K., & Peris, S., (2018) A new look at cryptocurrencies.Economics Letters, 163,69.

Polasik, M., Piotrowska, A. I., Wisniewski, T. P., Kotkowski, R., & Lightfoot, G. (2015). Price fluctuations and the use of Bitcoin : An empirical inquiry.International Journal of Electronic Commerce, 20(1), 19.

Sarno, L., Valente, G., & Leon, H. (2006). Nonlinearity in deviations from uncovered interest parity : An explanation of the forward bias puzzle.Review of Finance, 10,443482.

Seigh, G. (2015). Synthetic commodity money.Journal of Financial Stability, 17,9299.

Stavroyiannis, S. (2018). Valueatrisk and related measures for the Bitcoin.The Journal of Risk Finance, 19(2), 127136.

Su, C. W., Li, Z. Z., Tao, R., & Si, D. K. (2018). Testing for multiple bubbles in bitcoin markets : a generalized sup ADF test.Japan and the World Economy, 46,5663.

Sukamulja, S., and Sikora. C. O. (2018). The new era of financial innovation : The determinants of Bitcoin’s price.Journal of Indonesian Economy and Business, 33(1), 4664.

Tiwari, A. K., Jana, R. K., Das, D., & Roubaud, D. (2018). Informational efficiency of Bitcoin−An extension.

Economics Letters, 163,106109.

Urquhart, A. (2016). The inefficiency of Bitcoin.EconomicsLetters,148,8082.

William, L. J. (2006). Bitcoin and future of digital payments,Independent Review,20(3), 397404.

Yamori, N., & Kurihara, Y. (2004). The dayoftheweek effect in foreign exchange markets : Multicurrency evidence.Research in International Business and Finance, 18(1), 5157.

Zhu, Y., Dickinson, D., & Li, J. (2017). Analysis on the influence factors of Bitcoin’s price based on VEC model.Financial Innovation, 3(1), 113.

How Is the Trading Volume of Bitcoin Determined?(Kurihara) (755)149