Credit guarantee schemes in emerging market economies : evidence from Thailand

journal or

publication title

Doshisha Shogaku (The Doshisha Business Review)

volume 66

number 5

page range 725‑753

year 2015‑03‑15

権利(英) Doshisha Daigaku Shogakkai

The Association of Commerce Doshisha University

URL http://doi.org/10.14988/pa.2017.0000013938

Credit Guarantee Schemes in Emerging Market Economies :

Evidence from Thailand

Jittima Tongurai

Abstract

This study examines credit guarantee schemes in one of important emerging market economies in the Southeast Asian region, Thailand. We find that SMEs in Thailand face greater barriers to obtain bank credits compared to large established firms. The role of Thai Credit Guarantee Corporation (TCG) in the Thailand’s credit market has increased but it is still limited compared to the role of credit guarantee institutions in other countries. There is a sign of vulnerability of the credit guarantee schemes in Thailand. More specifically, the leverage level of TCG exceeds the best practice level of 5 times the capital amount. However, the default rate of guaranteed loans is close to the sustainable level. Although the operation of Thai Credit Guarantee Corporation, at this point, shows indication of sustainability, periodical review of the scheme is necessary to prevent the vulnerability to become materialized. The challenge for policy makers is to strengthen the operation of Thai Credit Guarantee Corporation so as to increasingly facilitate SMEs access to bank credits. New methods of risk management (e.g., a risk-adjusted guarantee fee structure) can be adopted. Through the credit guarantee mechanism, banks will gain more experience with lending to SMEs. When a longer bank-customer relationship is established, better risk perception of SME lending will lead to reduction in interest rates and less collateral requirements on SME loans.

Key words: SMEs, Credit Guarantee Scheme, emerging market economies, Thailand

Ⅰ Introduction

Small- and medium-sized enterprises (SMEs) play a pivotal role in economic growth, job creation and poverty reduction of emerging market economies as well as in other developing and developed economies (e.g., Hallberg, 2000 ; Riding and Haines, 2001 ; Wagenvoort, 2003 ; Beck et al., 2005 a ; Bass and Schrooten, 2006). Nonetheless, SMEs usually face disproportionately less access to external financial resources compared with large firms (e.g., Riding and Haines, 2001 ; Beck et al., 2005 a ; Bass and Schrooten, 2006 ; Beck et al., 2008 ; ADB, 2013). The financial constraint, particularly limited access to debt financing, is an important factor that limits the start-up, growth, and survival of SMEs (Riding and Haines, 2001). Because SMEs are the engine of economic growth, governments often intervene in the financial markets to lessen the credit constraints faced by SMEs.

(725)175

During the last two decades credit guarantee schemes as a tool to promote private sector growth in general and growth of the SME sector in particular have attracted greater attention (Riding and Haines, 2001 ; Becket al., 2008 ; Centre for Entrepreneurship, SMEs and Local Development, 2013). The schemes have been widely implemented in both developed and developing countries to facilitate the flow of funds to

1

SMEs. For example, the Small Business Administration in the United States provides loan guarantees to qualifying small firms. Similar schemes are in effect in Canada, Japan, the UK and Germany (Riding and Haines, 2001). In many Asian countries (e.g., Indonesia, Korea, Malaysia, Taiwan and Thailand), government credit guarantee is an important part of corporate financing for SMEs (Shim, 2006). In Thailand, credit guarantee is operated by Thai Credit Guarantee Corporation (TCG), a state- owned specialized financial

2

institution that was established in 1991 under the supervision of the Ministry of Finance.

Taking on the experience of Thailand, this paper focuses on the government intervention in credit markets by means of credit guarantee on loans that commercial banks grant to SMEs.

More specifically, this paper examines the performance and contribution of Thai Credit Guarantee Corporation to the Thai economy in the past 20 years of its operation. The objectives of this paper are twofold ; (i) to examine the operation of TCG in the past years, and (ii) to assess the impact of its operation on the Thailand’s economy. A thorough analysis of the credit guarantee schemes in Thailand will help identify major challenges to the development of a more effective and sustainable credit guarantee system in the country.

Empirical findings in this study suggest that SMEs have faced higher financing obstacles than larger firms. By promising that a guarantor will pay all or part of the loan if the borrower defaults, a credit guarantee scheme help SMEs access to debt financing. The role of Thai Credit Guarantee Corporation in the country’s credit market has been increasingly important but it is still limited compared to the role of guarantee institutions in other Asian countries.

The vulnerability in the operation of Thai Credit Guarantee Corporation should be tracked periodically. More specifically, the sustainability of credit guarantee schemes depend largely on revenue from guarantee fees and the levels of leverage and non-performing guarantee (NPGs).

────────────

1 Credit guarantee schemes have existed in many countries since the beginning of the 20thcentury. During the 2008−2009 global financial crisis, credit guarantee schemes have been used as a policy instrument to improve access to finance by SMEs and young firms (Center for Entrepreneurship, SMEs and Local Development, 2013).

2 As of December 2014, the Ministry of Finance holds a 95.49 percent share and Thai financial institutions hold the rest of shares (Thai Credit Guarantee Corporation, 2014).

同志社商学 第66巻 第5号(2015年3月)

176(726)

The rest of the paper is organized as follows. Section 2 reviews theoretical concepts and the development of credit guarantee schemes in developed and developing countries. Rationale for the use of guarantee, particularly government credit guarantee, is investigated. The development of credit guarantee schemes in Thailand are also discussed in this section.

Section 3 discusses the results of empirical analysis and Section 4 concludes the paper.

Ⅱ Credit Guarantee Schemes

2.1 Rationale for the Use of Guarantees

SMEs usually suffer from the what-so-called credit rationing as stated by Stiglitz and Weiss (1981). In theory, credit rationing is the circumstances in which either (i) among loan applicants who appear to be identical some receive a loan and others do not, and the rejected applicants would not receive a loan even if they offered to pay a higher interest rate ; or (ii) there are identifiable groups of individuals in the population who, with a given supply of credit, are unable to obtain loans at any interest rate, even though with a larger supply of credit (Stiglitz and Weiss, 1981). Information asymmetry is seen as the main explanation of credit rationing (Gittell and Kaen, 2003 ; Craig et al. 2008 ; ADB, 2013). That is, commercial banks never have full information about their potential clients’ capacity and willingness to repay. As a consequence, the amount of credit allocated to small firms is relatively low even though they may represent a healthy economic sector. Credit rationing to SMEs can also occur because of other reasons such as relatively high credit risk of SMEs, imperfections in the credit market, and SMEs’ lack of collateral (Riding and Haines, 2001 ; Bass and Schrooten, 2006 ; Shim, 2006 ; ADB, 2013). Empirical evidence confirms the theory of credit rationing, suggesting that SMEs not only face higher financing obstacles than larger firms, but the effect of these financing constraints is stronger for SMEs than for larger firms (Beck and Demirguc-Kunt, 2006).

The problem of asymmetric information is particularly relevant in case of SMEs. Especially when a proposed investment involves the use of a new idea or a new technology, banks’ risk perceptions of lending to SMEs are exceptionally high. In addition, transaction costs of lending to SMEs are high relative to lending volumes. Gathering information on SMEs and monitoring their activities is costly and not always economically rational when a loan size is small. In response to asymmetric information and high risk perceptions, banks primarily conduct asset-based lending rather than cash-flow analysis when working with SME borrowers. The credit decisions under asset-based lending are principally based on the quality

Credit Guarantee Schemes in Emerging Market Economies(Tongurai) (727)177

of the available collateral. In developing countries, there is evidence that collateral requirements can exceed 150 percent of loan amount (Beck et al., 2008). Suffering under unequally distributed endowments with regard to collateral and to successful track records and credit history, SMEs usually face disproportionately less access to debt financing compared with large established firms (e.g., Riding and Haines, 2001 ; Beck et al., 2005 a ; Bass and Schrooten, 2006 ; Becket al., 2008 ; ADB, 2013).

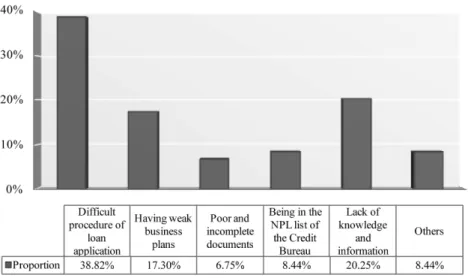

Numerous empirical evidences suggest that SMEs face higher barriers to external financing than large firms. Small and medium-sized firms find it difficult to obtain bank financing, especially long-term loans, for a number of reasons, such as lack of collateral, difficulties in proving creditworthiness, small cash flows, inadequate credit history, high risk premiums, underdeveloped bank-borrower relationships and high transaction costs (e.g., Scholtens, 1999 ; Beck and Demirguc-Kunt, 2006 ; Beck et al., 2008 ; Punyasavatsut, 2011). Ardic, Mylenko and Saltane (2011) estimate the global small and medium enterprise lending volume in 2009 to be 10 trillion US dollar. On average, small and medium enterprise loans constitute 13 percent of GDP in developed countries and 3 percent in developing countries. Punysavatsut (2011) finds that in spite of various measures of government support, only 40 percent of Thai SMEs gain access to

3

credit.

In spite of the SMEs having higher growth potential than the average firms, this potential could be limited by the availability of external sources of financing. At the firm level, financial constraints can limit entrepreneurial activity that adversely affect jobs, innovation and income of SMEs (Beck et al., 2005 b ; Paulson and Townsend, 2004). The economy as a whole may suffer welfare loss as a result of a suboptimal allocation of credit to SMEs. As SMEs play an important role in job creation, economic growth and poverty

4

reduction (e.g., Rajan and Zingales, 1998 ; Hallberg, 2000 ; Riding and Haines, 2001 ; Becket al., 2005 b ; Townsend and Ueda, 2003 ; Wagenvoort, 2003 ; Bass and Schrooten, 2006 ; World Bank, 2008), restrictions on the growth and survival of SMEs are of particular concern to policy makers. During the last two decades credit guarantee schemes have got greater attention as a tool to promote growth of SMEs (Llisteri, 1997 ; Riding and Haines, 2001 ; Beck et al., 2008 ; ADB, 2013). The credit guarantee schemes can help banks overcome information asymmetries by aiding accurate identification of lending risk and improving banks’ ability to make appropriate lending decisions (Levitsky, 1997). The schemes have been widely

────────────

3 It is reported that almost 70 percent of Thai SMEs had problem accessing to credits, compared to only 13 percent of large firms (Poonpatpibul and Limthanmmahisorn, 2005).

4 SMEs in Thailand contributed to 37 percent of the country’s GDP in 2012. The share of SME exports to the total exports of Thailand was 28.8 percent with 3.7 percent year-on-year growth in 2012 (ADB, 2013).

同志社商学 第66巻 第5号(2015年3月)

178(728)

implemented in both developed and developing countries to facilitate the flow of funds to SMEs. It is estimated that there are over 2,250 credit guarantee schemes implemented in almost 100 countries worldwide (Green, 2003).

A credit guarantee scheme is a promise that a guarantor will pay all or part of the loan if the borrower defaults. In essence, the schemes absorb an important share of borrower’s risk and compensate for insufficient collateral. Through a mechanism of risk transfer and diversification, a banks’ risk of lending to SMEs is lowered (i.e., guarantees secure repayment of all or part of the loan in the event of default). Credit guarantee can therefore facilitate access to bank credits for SMEs and, in some cases, improve credit terms for SME borrowers.

By allowing loans to be granted to SMEs, these firms are able to establish a credit reputation (i.e., repayment of loan) that can act as a type of collateral in their future borrowing.

Simultaneously, by extending more loans to SMEs, banks gain experience in managing these types of loans. The use of credit guarantee is expected to result in reduction in information asymmetry in the credit market, more lending to SMEs, and subsequently further development in the SME loan segment of the credit market (Zecchini and Ventura, 2009 ; Honohan, 2010).

Some scholars, however, criticize that credit guarantee may intensify the adverse selection and moral hazard problems of bank lending as only higher risk borrowers that cannot obtain financing without the scheme will be attracted. If adverse selection sets in, and highly risky borrowers enter into the guarantee scheme, the default probability of the scheme may increase and the overall performance of the scheme will deteriorate (Center for Entrepreneurship, SMEs and Local Development, 2013). Credit guarantee may also increase the moral hazard problem as guarantees may discourage financial institutions from closely monitoring their lending (ADB, 2013).

The use of credit guarantees is widespread but the design of guarantee system varies across countries. Credit guarantee schemes can be organized by a public or private credit guarantee institution (Zecchini and Ventura, 2009). Generally, credit guarantee schemes are managed by government-related agencies. However, guarantee services may be provided through the financial system with little government intervention. In some cases, guarantee services are provided by private entities started on public initiative and with majority participation by public entities (Centre for Entrepreneurship, SMEs and Local Development, 2013). Although private institutions can provide credit guarantee services to SMEs, the existence of public credit guarantee institution is necessary, especially in developing countries. A number of factors justify the existence of public credit guarantees : for example, market failure (e.g., incomplete markets, incomplete information), market imperfections (e.g., imperfect

Credit Guarantee Schemes in Emerging Market Economies(Tongurai) (729)179

competition, infant industries operating below their minimum efficient scale), imperfect distribution of endowments (e.g., up-start firms versus large established firms), externalities (e.

g., nonexistence of markets, public goods), policy-dependent investment outcomes (e.g., regulation, public support scheme), and economic downturns (Mostert et al., 2010). Credit guarantees are typically used as a policy tool to increase SME access to finance. Credit guarantee business usually deals with risky segments of enterprises and it is generally hard to maintain sufficient profits for sustainable operations. As a result, credit guarantee business is not attractive to the private sector (ADB, 2013). The public guarantee schemes will help the underserved SME sector to access to bank credits and can be an effective tool for responding to external shocks such as a financial crisis and a natural disaster (ADB, 2013).

Guarantee schemes are generally managed by government related agencies such as public guarantee funds (e.g., Canada Small Business Financing Program (CSBF), the Japanese Credit Guarantee Corporation, and the US Small Business Administration’s (SBA) Loan Program), or by an administrative unit of a ministry. In some cases, the guarantee schemes are operated through agencies with participation by the private sector. Credit guarantee schemes can be directly funded by public authorities, by the private sector or by both parties. Among the 76 credit guarantee schemes surveyed in Beck et al. (2010), 58 percent received funds from the public sector, 49 percent from the private sector and 3 percent from NGOs.

Measured by outstanding guarantee liabilities to GDP, Becket al. (2008) estimate that the median size of credit guarantee schemes in developing countries is 0.30 percent of GDP while the median size of schemes in developed countries is 0.21 percent. The region with the highest use intensity is Asia, where the median size is almost 5 percent of GDP. In 2011, credit guarantees in Korea amounted to 6.2 percent of GDP or almost 10 percent of total outstanding credit in the private sector (Becket al., 2008 ; Center for Entrepreneurship, SMEs and Local Development, 2013). The volume of outstanding guarantees to GDP in 2010 of Taiwan and Japan were 3.6 percent and 7.3 percent of GDP, respectively. In Asia, most of the credit guarantee establishments (e.g., Japan, Korea, Malaysia, Indonesia, Taiwan and Thailand) were initiated by the governments as can be seen in Table 1. Credit guarantee schemes designed to facilitate SME financing are also implemented in other regions. For example, government fund guarantee for small business loans in Germany and the Netherlands.

Organizations external to government, including trade associations, provide loan guarantees in Belgium, Luxembourg, Ireland, France, Portugal, Spain and Greece (Riding and Haines, 2001). Due to importance of SMEs for employment and for the national economy, all OECD countries have publicly backed guarantees to assist new SMEs in getting access to external

同志社商学 第66巻 第5号(2015年3月)

180(730)

financing (Mostert et al., 2010). The government’s Small Business Development Fund (SBDF) guarantees both long-term and short-term loans for SMEs in Slovenia. An agency of Chilean government (i.e., Guarantee Fund for Small Business (FOGAPE)) provides partial credit guarantee to small firms. At a regional level, the EU’s SME Guarantee Facility is managed by the European Investment Fund (EIF) and provides capped guarantees partially covering portfolios of financing to SMEs undertaken by banks, leasing companies, guarantee institutions, mutual guarantee funds.

Theoretically, a credit guarantee scheme is expected to be beneficial to SMEs and the economy. Numerous empirical studies support this theoretical prediction. Examining the Canadian loan guarantee, the study of Riding and Haines (2001) shows that loan guarantee programs can be an effective mean of supporting start-up, growth, and survival of new and risky enterprises. Likewise, Kang and Heshmati (2008) find that credit guarantee schemes of Korea Technology Credit Guarantee Fund (KOTEC) have a positive effect on sales growth and productivity of the Korean firms but failed to stabilize employment in these firms. In general, the credit guarantee enabled guaranteed firms to achieve good performances. Tracking the actual change in employment at 1,166 firms that received 1,515 loan guarantees of the California State Loan Guarantee Program during 1990−1996, Bradshaw (2002) found empirical evidence that employment in firms receiving loan guarantees increased by 40 percent among all firms and 27 percent among non-agricultural firms. The program also increased state tax revenues by 25.5 million US dollar, well in excess of the 13 million US dollar the California state spent on the program. The Japanese credit guarantee sector is said to be among the most important credit guarantees worldwide. In 2010, more than one third of Japanese SMEs are supported by NFCGCs (Centre for Entrepreneurship, SMEs and Local Development, 2013). An investigation of the development of credit allocation among Japanese SMEs reveals that the credit guarantee program implemented by the Japanese government in the late 1990s resulted in the increased availability of funds to SMEs, and to the greater profitability of creditworthy firms (Uesugi, 2008). In addition, the study of ADB (2013) indicates that more than one-third of Japanese SMEs were able to obtain guarantees for loans in 2012, compared to on average 3.7 percent of SMEs in other Asian economies. Regarding loan pricing, the results are rather mixed. While Seidmann (2005) finds that guarantees reduce the spread over LIBOR in the sample loans by 45 basis points, Uesugi (2008) finds no evidence that the credit guarantee program reduces interest rates of loans to Japanese firms.

Credit Guarantee Schemes in Emerging Market Economies(Tongurai) (731)181

Table1Selectedcreditguaranteeschemesinvariouscountries. GuaranteeSchemeCountryEstablished YearMajorshareholdersGuaranteecoverage/coverageratioGuaranteefee (%perannum)Maximum leverageratio SmallBusinessAdministration (SBA)LoanGuaranteeProgramUSA1953GovernmentdepartmentUpto80%ofloansofuptoUS$100,000;upto 75%ofloansaboveUS$100,000;themaximum guaranteeamountofUS$750,000…… SmallBusinessLoansAct(SBLA) GuaranteedLoanCanada1961Federalgovernment85−90%ofloanamounttoamaximumof Canadian$250,0001.75%… DTILoanGuaranteeSchemeUK1981DepartmentofTrade(DTI)85%ofthetotalloan2.50%… NationalFederationofCredit GuaranteeCorporations(NFCGC) (formerCreditGuarantee Corporation(CGC)) Japan

1937 (CGCduring 1937−1961) Publicinstitutionsestablishedunder theCreditGuaranteeCorporationLaw 100%ofloanamounttoamaximumof200 millionyen(individuals/corporations)and400 millionyen(cooperatives)forgeneralguarantee; amaximumof80millionyen(individuals/ corporations)and80millionyen(cooperatives)for guaranteeswithoutcollateral

Avariablefeeratesystem basedoncreditriskof SMEs(0.50−2.2%)35−60times JapanFinanceCorporationfor SmallandMediumEnterprise (JASME)1958UndertheSmallBusinessCredit InsuranceLawin195070−80%oftheloanamount0.87%Nomaximum SpecialCreditGuaranteeProgram forFinancialStabilityOct.1998−Mar. 2001Government-affiliatedinstitution100%coverageoftheprincipalandinterest…… 3,000localcreditguarantee companiesChina1993privatelyowned,fullyorpartlyowned bylocalgovernments……… KoreaCreditGuaranteeFund (KODIT) Korea

1976Public/Private50−85%oftheloanatmost(usually85%)0.50−2.00%(risk-based)20timescapital funds KoreaTechnologyCredit GuaranteeFund(KOTEC)1989Government-affiliatedinstitution85%oftheloanatmost(usually85%)0.50−2.00%(risk-based)20timescapital funds RegionalCreditGuarantee Foundations(RegionalCGF)1996………… KoreaFederationofCredit GuaranteeFoundations(KOREG)2000Government-affiliatedinstitution85−100%oftheloanatmost(usually85%)1.10%15timescapital funds SmallandMediumBusinessCredit GuaranteeFund(SMEG)Taiwan1974non-profitlegalentity(centraland localgovernmentsholda81%share)60−95%oftheloanamount(usually80%)0.75%,1.00%,1.25%, 1.50%(risk-based)20timesnet worth Source:HancockandWilcox(1998),RidingandHaines(2001),Shim(2006),Uesugi(2008),ChungandAhn(2009),NationalFederationofCreditGuaranteeCorporations(2010),ADB(2013).

同志社商学 第66巻 第5号(2015年3月)

182(732)

Table1Selectedcreditguaranteeschemesinvariouscountries.(Cont.) GuaranteeSchemeCountryEstablished YearMajorshareholdersGuaranteecoverage/coverageratioGuaranteefee (%perannum)Maximum leverageratio CreditGuaranteeFundTrustfor MicroandSmallEnterprises (CGTMSE)India2000Government-affiliatedinstitution62.5−85%oftheloanamountApproximately1%… DepositandCreditGuarantee Corporation(DCGC)Nepal1974Government-affiliatedinstitution75%oftheloanamount1.00%… CentralBankofSriLanka(CBSL) (nospecializedinstitutionforCG)SriLanka1950(CG started1967)Government-affiliatedinstitution50−80%oftheloanamount1.00%0.39(contingent liability/capital funds) PTAsuransiKreditIndonesia (Askrindo) Indonesia

1971BankofIndonesia(55%)andMinistry ofFinance(45%)70−80%oftheloanamount1.20−1.50%10timesnetworth PerusahaanUmumJaminanKredit Indonesia(Jamkrindo)1981Government-affiliatedinstitution70−80%oftheloanamount2.28%10timesnetworth PTPenjaminKreditPengusaha Indonesia(PKPI)1995Private75%oftheloanamount1.50%… PerumSaranaPengembangan Usaha(PerumSarana)2000100%government-ownedMaximum75%oftheloanamount0.50−1.50%(risk-based)… CreditGuaranteeCorporation MalaysiaBerhad(CGCMB)Malaysia1972BankNegaraMalaysia(79%)& commercialbanksandfinance companies(21%)30−90%oftheloanamount3.65%6timesreserve SmallBusinessCorporation(SBC)Philippines2001Government-affiliatedinstitution70−80%oftheloanamount…3times ThaiCreditGuaranteeCorporation (TCG)Thailand1991MinistryofFinance(95.49%)& FinancialInstitutions(6.43%)Maximum50%oftheloanamount;the maximumguaranteeamountof40millionbaht1.75%10timesequity Source:HancockandWilcox(1998),RidingandHaines(2001),Shim(2006),Uesugi(2008),ChungandAhn(2009),NationalFederationofCreditGuaranteeCorporations(2010),ADB(2013).

Credit Guarantee Schemes in Emerging Market Economies(Tongurai) (733)183

2.2 Credit Guarantee Schemes in Thailand

Thai Credit Guarantee Corporation (TCG) was established in Thailand under the Small Industry Credit Guarantee Corporation Act B.E. 2534 on December 30,

5

1991. The objective of TCG as stipulated in the Act is to provide credit guarantees to small businesses so as to accelerate the dispersal of credit extension throughout the country for the benefit of the country’s economic and social development (Thai Credit Guarantee Corporation, 2014). TCG also supports the government’s policy in promoting and developing business sectors that are strategically important to the economy. Currently, TCG has 9 offices in Thailand : Bangkok office, Phra Nakorn Si Ayutthaya office, Chiangmai office, Phitsanulok office, Udonthani office, Nakhonratchasima office, Chonburi office, Surat Thani office and Songkhla office. As of December 2014, TCG’s total registered capital is 6,839.95 million

6

baht (about 228 million US dollar at the exchange rate of 30 baht per US dollar), of which 6,702.47 million baht (about 223.42 million US dollar) is paid up. Of this amount, the Ministry of Finance contributes 95.49 percent and contribution from financial institutions accounts for the rest.

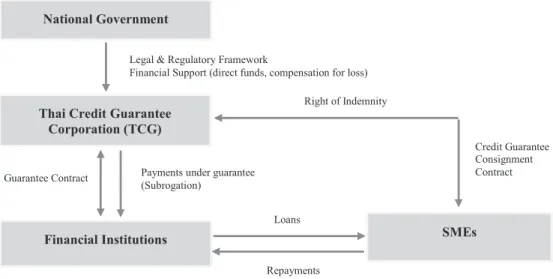

TCG is the only credit guarantee entity in Thailand. It is one of important financial tools for the government in supporting and promoting social and entrepreneur development of the country. The corporation formulates and manages credit guarantee schemes together with its partner financial

7

institutions. Through the network of commercial bank branches, TCG provides guarantee coverage for partly secured as well as unsecured credit facilities. At present, there are four major credit guarantee schemes operated by TCG (see details in Table 2). Normal scheme is a guarantee for unsecured portion of loan that is approved on case-by- case basis. Automatic scheme (MOU) is the pre-approved guarantee that TCG grants to participating financial institutions. Risk participation scheme (RP) is a credit guarantee that lending risk is shared proportionally between TCG and financial institutions. Portfolio guarantee scheme (PGS) is a credit guarantee that TCG sets the limit on Non-Performing Guarantees (NPGs). For portfolio guarantee, the decision to grant a guarantee is not assessed on an individual basis but based on some common characteristics such as loan volume, a minimum level of creditworthiness, the intended use of funds, the geographic location of the

────────────

5 TCG took over all the business and operations of the Small Industry Credit Guarantee Fund, and officially started operations on February 1992 with an initial registered capital of 400 million baht.

6 On July 3, 2000, additional capital of 4 billion baht was approved. The registered capital was increased by another 2 billion baht at the end of 2005. The latest capital increase of 2,137.47 million baht was approved on September 25, 2009.

7 Government Saving Bank, TMB Bank PCL, Bangkok Bank PCL, Krungthai Bank PCL, Kasikorn Bank PCL, Siam Commercial Bank, Thanachart Bank PCL, Financial Institutions Development Fund, Small and Medium Enterprise Development Bank of Thailand (SME Bank), Bank of Ayudhya PCL, United Overseas Bank (Thai) PCL, and Standard Chartered Bank (Thai) PCL.

同志社商学 第66巻 第5号(2015年3月)

184(734)

Table2MajorcreditguaranteeschemesofThaiCreditGuaranteeCorporation. NormalSchemeAutomaticScheme(MOU)RiskParticipationScheme(RP)PortfolioGuaranteeScheme(PGS) DescriptionLoanguaranteeisbasedoncase-by-case analysis;Guaranteeonnon-collateralized portion Pre-approvedguaranteecreditgivento participatingfinancialinstitutionsto shortenlendingapprovalperiod Lendingrisksharedbetweenfinancial institutionsandTCG

ThreeTypes:securedcreditguarantee (Normal),unsecuredcreditguarantee,and guaranteeforNPLwithbusinesspotential Guaranteelimitpercase

Amaximumof100%guaranteeonthe unsecuredportionoftheloanwhichshall notexceed50%ofthetotalloan;the maximumguaranteeof40millionbaht foreachclient Maximumguaranteeamountupto3 millionbaht Aminimumguaranteeamountofnotless thanthedifferencebetweenthetotal principalofthecreditandtheappraisal valueoftheassetswhichshallnotexceed 50%ofthetotalloan;themaximum guaranteeamountof40millionbahtper client

Aminimumguaranteeamountofnotless thanthedifferencebetweenthetotal principalofthecreditandtheappraisal valueoftheassetswhichshallnotexceed 50%ofthetotalloan;themaximum guaranteeamountof20millionbahtper clientforsecuredcreditguaranteeand unsecuredcreditguarantee,and10million bahtperclientforguaranteeforNPL Typesofguaranteeliability

Guaranteeofnormaldebts:TCGis liableaccordingtotheguaranteeliability plusinterestsincethedebtdefaultdate untilthelawsuitfilingdateornot exceedingtheliabilityconditionssetforth intheletterofguarantee. GuaranteeofNPL:TCGisliable accordingtotheguaranteeliabilityplus interestsincethedebtdefaultdateuntil thefinalizationofthelegalcase.

TCGisliableaccordingtotheguarantee liabilityplusinterestsincethedebtdefault dateuntilthelawsuitfilingdateornot exceeding180daysasspecifiedinthe letterofguarantee.

TCGisliableforhalfoftheimpairment loss(impairmentequaltoliability deductedbyvalueofcollateralsold)since thedebtdefaultdateuntilthelawsuit filingdatebutnotexceeding180days.

DependontheproportionofNon- performingcreditguarantee(NPG): NPG!12%,compensation100% 12%<NPG!14%,compensation75% 14%<NPG!18%,compensation50% ClaimpaymentPaiduponlegalproceedingtotheSMEs…PaiduponlegalproceedingtotheSMEsPaidin5installments,startingfromyear 2untiltheendoftheguarantee RecoveryofpaymentTCGwilltakelegalactionagainsttheborrowerand/ortheguarantorafterthereisevidencethattheborrowerand/ortheguarantorarecapableofrepayment.RPschemeisnot applicable. ApprovalperiodAbout22businessdaysfromthedateof receiptsofcompletedocumentsAbout10businessdaysfromthedateof receiptsofcompletedocuments5businessdaysapprovalperiod… Schemelaunchingperiod…April2000May2004March2009 Source:Author’sconstructionbasedondatafromTCG’sAnnualReports.

Credit Guarantee Schemes in Emerging Market Economies(Tongurai) (735)185