Author(s)

Toyokawa, Sayaka

Citation

沖縄大学法経学部紀要 = Okinawa University JOURNAL

OF LAW & ECONOMICS(18): 11-45

Issue Date

2012-12-21

URL

http://hdl.handle.net/20.500.12001/10402

Department of Law and Economics, Okinawa University, 555 Kokuba, Naha, Okinawa, 902-8521 Japan

Abstract

The objective of this paper is to identify and determine potential customers and establish the profile of UK “health food consumers”through their purchasing behaviour, attitudes and motives for functional foods in general and Moromi Vinegar in particular. Moromi Vinegar comes from the island of Okinawa and it has lived up to its own publicity in Japan. Moromi Vinegar is a famous as an over-the-counter supplement to relieve many hyper lipid symptoms.

Whereas the overall food market is relatively stagnant the UK's functional foods and drinks market in contrast, seems have a long-term opportunity for steady growth. Consumer awareness of functional foods is increasingly high in the UK and demand has been strong for a long time. (Toyokawa, 2012)

This paper reviewed secondary data through the descriptive method as well as primary data; qualitative data collected through questionnaires and interviews of the target population.

At the end, this paper suggests a framework that can help rationalize and make more effective the international market strategy process for the Moromi Vinegar company.

Key Words: Functional Food, Vinegar, Okinawa, UK 【Article】

Sayaka TOYOKAWA*

Market Analysis of Japanese Functional Food in the

UK: Case Study of Okinawan Moromi Vinegar

*

l: Introduction 1.1 Background

People are eating more calories than they need. They are eating far too many unhealthy foods and to compound the problem do not take enough exercise. The consequences are dramatically increasing lifestyle related diseases such as obesity and high blood pressure amongst the UK population.

Europe is the third largest functional food market in value behind that of Japan and the U.S. Whereas the overall food market is relatively stagnant the UK's functional foods and drinks market in contrast, seems have a long-term opportunity for steady growth. Consumer awareness of functional foods is increasingly high in the UK and demand has been strong for a long time (Toyokawa, 2012), but the gap between potential and actual demand remains.

Moromi Vinegar has lived up to its own publicity in Japan. It is famous as an over-the-counter supplement to relieve many hyper lipid symptoms. People can take this chance to get rid of their own excessive lipid in their blood circulation. This product helps sufferers to achieve normal levels. Also those people who suffer from different kinds of diabetes are helped as the vinegar helps them to normalize their blood glucose as much as possible. Users of this product have reported significant improvements in their general well being.

The objective of this paper is identify and determine potential customers and establish the profile of UK food “health food consumers” their purchasing behaviour, attitudes and motive for functional foods in general and Moromi Vinegar in particular. Additionally, this paper aim to explore the potential expansion of a small company called Company A. The company produces Moromi Vinegar (health vinegar) and it comes from the island of Okinawa in southern Japan and Company A was awarded a patent from the Japanese government in 2005.

The secret to obtaining good Moromi Vinegar is the rice mash, known as Moromi. Steamed white rice is mixed with black yeast, water and a "seed mash'' or starter (Koji), then left to ferment for about two weeks. The end product is a rich, full flavoured and healthful condiment (Heffeley, 2005).

The rice mash is itself a by-product of Awamori, an Okinawa-originated distilled liquor similar to Sake but quite distinct from it. Moromi does not contain any alcohol. Some of the benefits accorded to Moromi are reduced b1ood sugar levels, lower cholesterol readings, and possibly helping to burn body fat.

According to the Japan Food Analysis Centre study, Moromi contains plenty of amino acid, minerals such as magnesium, calcium, potassium, irons and vitamins B1, B2 and B6. Company A started the production of this Vinegar 11 years ago. They originally blended in pure passion fruit juice to fortify Moromi with more citric acid for a greater synergy effect between health ingredients and flavor.

Constituents to which most researchers attribute its health-enhancing benefits are its high concentrations of citric acid and amino acids. Moromi Vinegar has 43 times the amino acid contents of apple cider vinegar and 16 times the amount found in regular Japanese vinegar. These amino acids provide a valuable nutritional support for healthy skin, muscle strength, mental concentration, and fat metabolism. Citric acid is a great stress-fighting nutrient that helps the body burn fat effectively to increase energy and help maintain a healthy weight. The unique nutritional profile of Moromi Vinegar makes it an outstanding supplement for total body health and vitality(Business Insight, 2004).

In addition, according to Kreb's Cycle (Simpkins & Williams, 1989), citric acid will be efficacious in mainly five different ways.

● Weight loss - When the Citric Acid becomes active, fat will easily change into energy into

energy.

● Diabetes - Citric Acid balances insulin and adrenalin and so can help those suffering from

diabetes.

● Hypertension - Citric Acid promotes the digestion of salt and consequently will help

reduce high blood pressure.

● Constipation and Haemorrhoids-when people take Citric Acid, the intestines become

more active and, will function normally.

● General tiredness - The consumption of this vinegar also helps to remove lactic acid from

muscle this is reducing the symptoms of tiredness such as aching shoulders, stiff joints and fatigue.

New research co-conducted with Nihon Pharmaceutical University proved that an intake of “Moromi vinegar helps lower the total cholesterol level and keep it at a normal level. Also, the lowering of LDL cholesterol has been confirmed” (Takeyama, 2003).

In the UK, there are many people who suffer from the conditions mentioned previously and these people tend to be more open to alternative product of health education and products and more likely to try alternative products like “Moromi Vinegar” in order to maintain good health and an improved immune system. This product can be used as a food supplement as an alterative way of getting rid of trunk obesity and excessive metabolic rates. They can add this product to their own prescribed medication by health/medical authorities and this is particularly helpful to those people who take any form of anti-hyper lipid medication.

1.2 Unique Selling Points

To a certain extent the scientific background and formulation of functional food is its unique selling point (USP). This is what differentiates it from other foods within its

grocery category, and also what adds value. Therefore the unique selling point of Moromi Vinegar is follows;

▲

This product is effect for many illnesses and symptoms as mentioned above.

▲

This Vinegar can be taken as a supplement drink (with medicine) or can be used as an alternative medicine.

1.3 Background Information on Okinawa

Okinawa is located in the southern group of islands between mainland Japan and Taiwan. Okinawa has the highest proportion of centenarians in the world (Takeyama, 2003). In 2001, a book called ‘The Okinawa Program' was published detailing a study of Okinawa longevity by three specialists namely Willcox, Willcox and Suzuki. The authors found that Okinawans elderly people had remarkably low cholesterol, clean arteries and a scarcity of heart disease which were attributed to the consumption of huge quantity of seaweeds and locally grown vegetables (Willcox et al, 2001). The book reached the American best seller lists. In Okinawa, vinegar is also a very important ingredient in the local diet. Food establishments are trying to out do each other by incorporating rice vinegar in as many dishes as imaginable. For example, Okinawa elderly people eat Sashimi with Soy source and vinegar.

The fact that Okinawa is the home to the world's largest population of centenarians has attracted the attention from all over the worlds. Almost 600 of its l.3 million inhabitants have lived into their second century with vivacity (much higher than anywhere else in the world and they look even younger than their actual age (Corliss and Lemonick, 2004). This both creates a good image for Japanese consumers and presents us with a potential plus point vis a vis promoting the production the UK.

1.4 Research and Objectives

The main objective of this project is to analyse and determine the possibility of Moromi Vinegar entering the UK market.

Objectives:

▲

To determine potential customers.

▲

To identify the principal competitors in the UK.

▲

To estimate the potential market size and structure.

▲

To establish the profit of “health food consumer's” through his/her purchase behaviour, attitude and motives for health food.

▲

2: Research Methodology 2.1 Introduction

Methodology can generally be described as “The theory of how research should be undertaken, including the theoretical and philosophical assumptions upon which research is based and the implications of these for the method or method adopted” (Sakaran, 2000). Accordingly, the following section will describe the methodological approach in terms of research design, data collection and method, sample, data analysis and limitations of study for this paper.

In order to find the potential of Moromi Vinegar in the UK market, it is necessary to conduct descriptive research (Churchill, 2002). This paper reviewed secondary data through the descriptive method as well as primary date; qualitative data collected through questionnaires and interviews of the target population.

2.2 Data Collecting Procedure 2.2.1 Primary Research

The primary data collection methods in this research are face-to-face interviews, phone interviews and self-completion (face-to-face and online) questionnaires. The interviews and questionnaire were answered by health food consumers in UK.

Following secondary research on potential market entry strategies, interesting discussions were carried out with two companies. One is a Japanese food retailer near Piccadilly Circus and the other, is an organic food wholesaler that mainly focuses on Japanese foods. A telephone interview was also carried out with one governmental organization called JETRO UK (Japan External Trade Organization) which is engaged in the promotion and facilitation of Japanese business around the world.

2.2.2 Face-to-face interview

Face-to-face interview is the method where the interviewer and the respondent are in direct face-to-face contact. The main advantage of this method is the high quality of the data collected, considering respondents can be encouraged to give a much fuller response in this situation because the interviewer can observe the respondent's behavior and reactions. Personal interviews are generally conducted at a slower pace than other methods, where the respondent will have a time to gather thoughts and thus give more considered responses. 2.2.3 Questionnaires

The research strategy aims at planning how the researcher will answer its research questions. It should contain clear objectives; specify the sources from which data will be collected (Saunders et al, 2007). Concerning the research, the most appropriate research strategy is the survey method because in order to respond objectives, data will be collected

through questionnaires and three interviews.

The questionnaire method took place over a month between 10 a.m. to 6 p.m. in end of November to beginning of December in 2006 in St. John's Wood High Street and in front of St Guys Hospital behind the London Bridge Station. Potential respondents were intercepted by the researcher and asked if they were willing to complete a questionnaire for the research. If the respondent answered positively, the researcher then briefly explained the subject and purpose of the study, informed them that the study was confidential and handed questionnaire to the respondent for them to complete. The researcher was available for any queries the respondent may have regarding the topic. Two different formats had been used for this research:

1. Listed Questions: Listed questions offer the respondent a list of responses, any of which they can choose. Most of the questions is of this type. Such questions are useful when there is a need to be sure that the respondent has considered all possible responses. The response categories used can vary widely and include "Yes" or "No", "Agree" or "Disagree" and "know" or " Do not know". This method is used to ensure that the issue not clouded by intermediate answer (Saunders, Lewis and Thornhill, 2007).

2. Open questions: A few questions are open questions in which the respondent is left free to give any answer in order to obtain more personal points of view and ideas (Hague, 1998). Another questionnaire method used was an on-line survey. Internet mediated questionnaire are usually administered in one of two way: via email or via a website (sited Saunders, Hewson et al, 2003), but this research was only conducted website based

questionnaire.

The author set a questionnaire on the website called “free-online-survey.co.uk” and Japanese social network site called "mixi.co.jp'' The author advertised the website widely using a range of media such as an email pre-survey and a banner advertisement website page that is like to be looked at by the target population, using a hyperlink to the questionnaire and highlighting the closing date. When the respondent completes the questionnaire, these data files are generated and saved automatically on the website.

300 results were collected, 221 surveys were done on the street, then other 79 were collected by online (free-online-survey.co.uk). Both questionnaires used the same question set.

On the other hand, the Mixi questionnaire focused solely on potential Japanese customers. Due to the limited space per person only two questions were allowed. It was necessary to conduct because report needed to know attitude of Japanese. Consequently the volume of responses depended entirely on interest in the topic and questions.

2.2.4 Sampling Design

There are two major sampling techniques, one is probability sampling and another is non-probability sampling(Saunders et a1 2004).

Firstly, selecting a probability sample was not possible because there was no suitable sampling frame, therefore a non-probability sampling has been considered the most appropriate interview technique, in order to identify and question people.

Secondly, the sample size needed to be large enough to provide data which could be analysed and generalizations drawn from. The larger the sample it is the more accurate the data (Hague & Ackson, 1998).

As the objective of the paper is to find attitudes, purchasing motivations and expectations of consumers toward Moromi Vinegar and other health food products it consequently has to be well defined.

2.2.5 Secondary Research

Secondary data refers to data already collected for some other purposes. A review of the literature has been conducted on the UK health food industry in order to obtain a market overview.

This study will also use secondary data sources. Useful sources such as newspapers, commercial data, association website, magazines and academic books have been uncoil in gathering relev ant data. We may use available reports and other information both internal and external sources to study UK health food industry. We also need to review market research publications regarding the health food industry situation in UK. These publications provide sector by sector information regarding market size, trends, consumer expenditure, consumer profiles, industry structure and future prospects.

2.3 Limitation of the Research

This project is a focused research concerning Moromi Vinegar's opportunity in entering the UK market. Mainly due to the limitations of time and manpower, it has been difficult to contact every potential customer or to conduct personal interviews in a wider context Another major limitation of this type of research is the lack of familiarity of the UK market consumers with this category of goods.

3: Literature Review

Recent situation is such that people are eating more calories than they need to. This is because they are eating too much in general, and too much heavily processed food. Further, they do not take enough exercise. The consequences are increasing lifestyle related diseases such as obesity and high blood pressure in the UK population(Mintel, 2005). Consequently, while there is potential for increased sales and consumption of health foods, including

Moromi Vinegar. Previous research (Toyokawa, 2012) showed that the outlook for health food and health products is bright, with favorable demographic changes helping to boost demand. Consumers are becoming increasingly aware of health eating and are also more prepared to take control of their own destiny with healthcare products and remedies. 3.1 Competitor attitudes towards Functional Foods

Business Insights (Summer, 2001) surveyed executives from 100 leading companies in the healthy food industry. They were questioned about the following key factors for their businesses.

When the information revealed in this survey is applied to the retail market, it can be expected that functional organic foods will be launched and marketed at an increasing rate over the coming years.

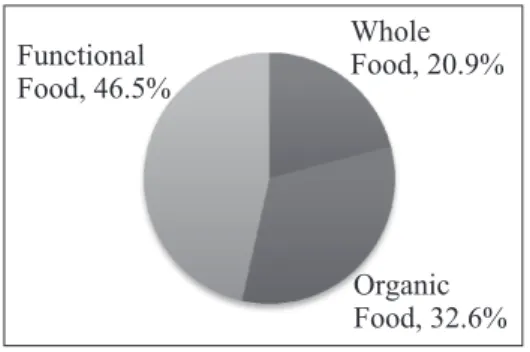

Business insight said (2004), 74% of all respondents said that they are planning to launch a new health product within this 5 years.

46.5% of all new healthy food products due to be launched over the next five years are functional foods. Only fifth of new products will be whole foods, with about a third of all

Whole

Food, 20.9%

Organic

Food, 32.6%

Functional

Food, 46.5%

Figure 1: Do your company plan to launch a health food product?

Figure 2: If your company does plan to launch a new healthy product within the next five years, which of these categories?

new healthy food products being organic.

The last graph indicates the countries in which health food industry most likely to launch new product.

This result also indicated the health food industry in UK will have an opportunity to become more competitive. 79.2% of the company would like to apply mostly in UK and Europe. Less than a third of the 75% of companies launching new healthy food products over the next five years will do so outside of Europe(Business Insight 2004).

All of those result shows that the UK healthy food market is likely to become ever more competitive. The niche markets explored like Company A may well be key areas for companies to explore for less competitive new healthy product sectors.

3.2 Environmental Analysis

External factors are everything in that they are out of the control of the company and among these government regulations, the economic situation, social trends and technological change figure large. These can be summarized in PEST analysis. It is important to build up an understanding of how changes in the macro-environment are likely to affect individual organizations. PEST analysis is useful method to provide the broad date from which the key element of change can be identified (Harberberg & Rieple, 2001).

▲

Political Factors

At the moment, there are no guidelines for functional food. The Health Food Manufacturers' Association in the UK is also concerned with maintaining and raising general standards within the process of being drafted with regard to the independent research needed to support health claims made by manufacturers of functional foods and drinks. However, there will be continued government backing for development of any such products that address common ailments, disease prevention and healthier eating in general.

The Government is particularly concerned about aspects of health in the population, in part in relation to the increasing funds needed to support the NHS (Key Note, 2007).

▲

Economic Factors

Health food and consequently sales revenue is strongly positively correlated with the performance of Gross Domestic Product. Currently, UK has strong environment for example, GDP is growing (2.1% to 3.0% every year), and high employment which is 74.6% in 2004. Additionally, the public has increased disposal income increased 3.2% in 2004.

In team of economic analysis health food can be classified as highly income elastic. This means that health food industry is highly sensitive to upturns and downturns in the economy. So the fortunes of the health food industry will always be subject to the world business cycle and exogenous shocks.

▲

Sociological Factors

Demand for functional food has increased dramatically over the past few years. This has been due to a number of environmental changes including the increasing of awareness of health issues, greater information and education and increases in eating out habits. Population in Britain is increasing about 0.3% every year during 5 years from 2001 (Data Monitor, 2005). Furthermore, by 2031, the percentage of those aged 45 and over is forecast to grow to 47.1%, within a population that will have grown to 67 million.

▲

Technological Factors

Health foods are subject to technological improvement which often involves huge amounts of research and development (R&D).

The whole issue of functional foods essentially relates to ingredients, which provide both nutritional and health benefits of the foods. Because there is an understanding that these ingredients must be obtained or produced from natural sources, there is a substantial level of research activity oriented towards identifying, manufacturing, and demonstrating the efficacy of the new generation of functional ingredients. This research activity can employ biological technologies to produce modified or new ingredients comprising the products(Goldberg and Williams, 1991).

3.3 Legislation

There is no specific legislation to control the composition and labeling of functional foods in UK and the term ‘functional food' is not defined in UK law. This food is subject to the same general controls for labeling and claims as other foods. The UK legislation on claims includes the Food Safety Act 1990 and the Trades Description Act 1968, which prohibit false and misleading claims. In addition, the Food Labeling Regulations 1996 (as

amended) lay down the labeling requirements of food generally and prohibit medical claims i.e. claims that a food will prevent, treat or cure a disease.

To import Moromi Vinegar, Company A has to follow the United Kingdom Food and Agricultural Import Regulations and Standards. It will have to adjust its label to incorporate the requirements of the Food Labeling Regulations of 1996 (Kurz, 2001). The main requirements needed are to include the name of the product as a generic name, the list of ingredients, instruction for use, a statement of minimum durability, storage conditions and the name of the manufacturer, packer of seller established within the EU. Further to this the label will have to be translated into English and re-designed for the UK market. The declaration of minimum durability, in this case a ‘Best before end' statement and storage conditions, were based on the results of the product shelf-life trials (Welch and Joynt, 1987).

When the imported goods arrive at the UK port or airport, the goods must be presented to Customs (Her Majesty's Custom & Excise) by the person who brought them into the UK (Kurz, 2001).

Our product is originally pure vinegar. Food that has to animal content covered by the imported Food Regulations 1997 (IFRs). As this product comes from Japan it does not need health certification under the IFR regulatory system (Ikemoto, 2005).

3.4 Porter's Five Forces Model

Porter's forces analysis is useful to understand how the competitive dynamic within and around an industry are changing (Lynch 2003). For understanding this situation of the health food industry in the UK and considering its factors, a review of five forces industry (the entry of new competitors, the threat of substitutes, the bargaining power of buyers, the bargaining power of suppliers and the rivalry among existing competitors) will be helpful for this study (Porter, 1980). These methods also can help a company to understand new challenges and it may help again when formulating strategy.

▲

Bargaining Power of Suppliers

Supplier ingredient companies focus solely on creating new ingredients and producing already-existing ones as requested by finished-product manufacturers. While they occasionally perform clinical and scientific studies to demonstrate the efficacy of a functional ingredient, mostly that practice is left to the finished-product manufacturers. Supplier ingredient companies typically do not formulate recipes incorporating their functional ingredients into conventional foods or drinks. They provide raw or refined ingredients, powders, and mixtures to finished-product manufacturers of flavor companies who create their own formulations (Key Note, 2005).

from finished-product manufacturers. As such, supplier ingredient companies have become increasingly competitive, often replicating other companies' formulation for a lower price in other to win more business. Product “theft” has acted as a barrier to investment in innovation.

The consolidation process in the health food industry creates a concentration of power. It also may provide some benefit to suppliers in the areas of inventory and delivery of product and distribution process(Barnes, 2002).

▲

Bargaining Power of Buyers

The bargaining power of buyers is considerably low because most of the functional foods and drink consumers accept the premium price. It may be perceived as a guarantee of quality and safety. However, it is important to notice that consumers who do not buy health food products said that price was main reason (Carey, 2002).

▲

Threat of New Entrants

From literature review, nearly 75% of respondents said that they are planning to launch a new health product. If this is the case, the health food market is likely to become increasingly competitive.

Major barriers to entry perceived include capital requirements, lack of knowledge and experience, access to inputs and access to markets, labour intensity and economic of scale. The UK functional foods and drink market is at the growth stage of the industry life cycle. According to Lynch(2003), if the industry is in its growing phase new competitors may be attracted in to the market. However, Lynch also points out that any company that tries to enter incurs high costs for that market share given that they are not the incumbent market leader.

▲

Threat of substitute products

Moromi Vinegar is a new product for this market therefore it does not have a direct substitute.

However, the functional foods and drink sector under consideration includes vitamin and mineral fortification products, cholesterol reduction products, dietary fibre, fortified products, probiotics, probiotics, symbiotic, antioxidants, and photochemicals which in a wider sense can all be act to be substitutes according to economic theory. Therefore all these products can act as substitutes for Moromi Vinegar. The health foods sector consists of organic foods, whole foods, alternative medicine, over the counter medicine will all now be considered as substitutes for our product.

▲

Rivalry among Existing Competitors

According to Lynch (2003), at the moment in market with a dominant company there may be less rivalry because the larger company is often able to quickly stop any entry potentials by smaller competitors. However, the Business Insight survey showed above, the other health food companies and food retailers start interest in launching their products in the functional food which increasing the competitive at the dominant company.

4: Result and Findings

4.1 Summary of Questionnaire Findings (STREETS & ONLINE)

This chapter is based on original research to determine the habits and attitudes of consumers in a number of areas connected with functional foods and Moromi Vinegar. The survey conducted by the author, took place in November 2006 among a sample of 300 adults in London aged 18 and over. The author chose to approach every fourth person walking along the street in order to keep the sample as random as possible.

The questionnaire method took place over a month between 10 a.m. to 6 p.m. in end of November to beginning of December in 2006 in St. John's Wood High Street and in front of St Guy's hospital. Online surveyed, 106 male and 194 female, spread throughout the age range shown below.

Figure 4: Gender Distribution Figure 5: Illustrate Age and Gender Distribution

The demographic distribution (Figure 4) reveals males (35.5%) and females (64.5%), females being proportionally higher than males in the survey. The five classified age groups (Figure 5) were distributed respectively, 18-24 (16.3%), 25-34 (30.7%), 35-44 (23%), 45-54 (20.0%) and 55-64 (9.7%). Figure 6, reveals 111 people as single and 189 people married.

The higher female proportion the greater willingness of women to answer the questionnaire whereas men were far more reticent.

P - Professional

I&JN - Intermediate and Junior Non-manual

SM&NM - Skilled-manual and Own Account Non-professional SSM & PS - Semi-skilled Manual and Personal Services S - Student

E&M - Employers and Managers HW - House Wife

R - Retired

Table 2: Illustration of socio-economic Group Total Male Female Male % Female &

P 92 31 61 29.2% 31.4% I& JN 31 10 21 9.4% 10.8% SN & NM 25 12 13 11.3% 6.7% SSM & PS 32 14 18 13.2% 9.3% S 42 16 26 15.1% 13.4% E&M 46 18 28 17.0% 14.4% HW 27 0 27 0.0% 13.9% R 5 5 0 4.7% 0.0% Total 300 106 194 100% 100%

Questions

1.Do you normally try to eat a healthy diet?

82.8% of the respondents said that they were making an effort to eat more healthily with only 17.8% saying that they did not worry about their diet.

2. Do you normally purchase functional food products?

More than 60% of the respondents declared they purchased functional food products. The graph shows that more than half are frequent or regular functional food customers and that females are predominant. The functional food market has clearly left behind any claims to niche market status. Consumer acceptance of health foods is now more mainstream than say five years ago.

Keynote (2007) also surveyed functional food customers. A lower but still very significant percentage of respondents (53.1%) were interested in buying foods or drinks with health claims, although the survey also identified that 55% of respondents tended not to believe the health claims of functional food and drink manufacturers.

Keynote (2006) noted that 87.3% of respondents felt they obtained all the nourishment they 17.8ɓ 82.8ɓ Yes No 38ɓ 62ɓ Yes No

Figure 7: Healthy Diet?

needed through their normal diet, without consuming functional foods or drinks.

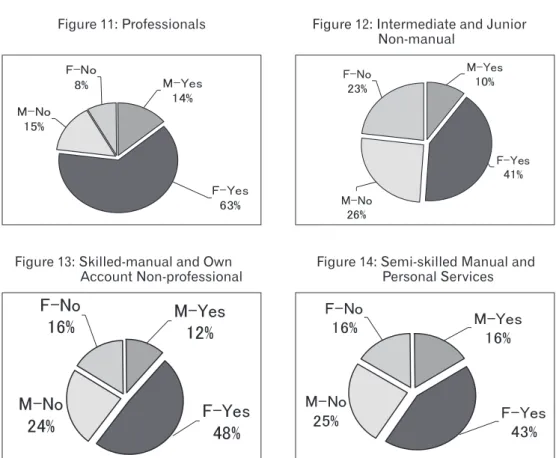

Breakdown by Socio-economic Group

Figure10: Functional Food buyer by Gender and Socio-economic Group

Figure 11: Professionals

Figure 13: Skilled-manual and Own Account Non-professional

Figure 12: Intermediate and Junior Non-manual

Figure 14: Semi-skilled Manual and Personal Services

In general, women have higher purchasing rates in all of the categories except the retired. This is may be because women are more likely buy for a partner, family member as sell as for themselves.

This is despite recent trends where both men and women are more likely to have own jobs and men are helping out around the home and in the shopping to help their busy spouses(Mintel, 2006).

The most heavy functional food users by socio-economic group are clearly the professionals. Indeed 78% of the respondents said they normally buy some type of functional food or drink. Housewives are the second heaviest consumers of functional foods with male students being the least health conscious of all.

The results by socio-economic clearly indicate that women in the professions and housewives are the most health conscious and wield the greatest spending power.

Abstracting the student and retired categories, more than 50% of all the other categories normally buy some functional foods.

Figure 15 : Student

Figure 17: House Wife

Figure 16: Employers and Manager

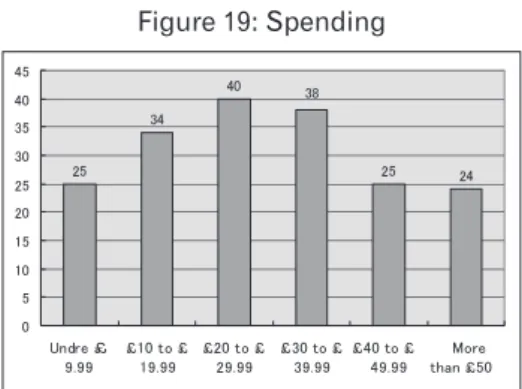

3.How much you do normally spent health food products per month?

Purchasing of health food products varies according by income. Our Figure No.19 is a histogram showing the monthly spending for health food products and indicates a normal distribution. We can assume that middle and higher earners normally spend more on health food products.

Our prior assumption seems correct as the above results reveal purchasing is higher among Employers and Managers as well as Professionals and Housewives. These data sets make it clear that the higher income groups are the main functional food consumers and confirm that they pay more attention to their health and can of course afford to purchase these products.

Retired people are also frequent consumers of FF, although they do not have the purchasing power punch of the other groups. Older people have a huge interest in health matters but having probably suffered various illnesses in their lives such spending may be spread out on other health related products such as medicines, vitamins and minerals.

Figure 19: Spending

4. Would you agree to pay more for health food products?

From the pie chart, 66% of respondents stated they would be more likely to pay more for the healthier option. This seems to confirm the Mintel report that concluded health foods are often more expensive than regular foods. Price is a major limiting factor for the entire healthy foods sector Organic foods are generally about 10-15% higher in price than their conventional counterparts. Functional foods vary from 20-200% higher in price. Whole foods are the only sector of sector of healthy foods that are often cheaper to buy than conventional foods(Mintel 2007).

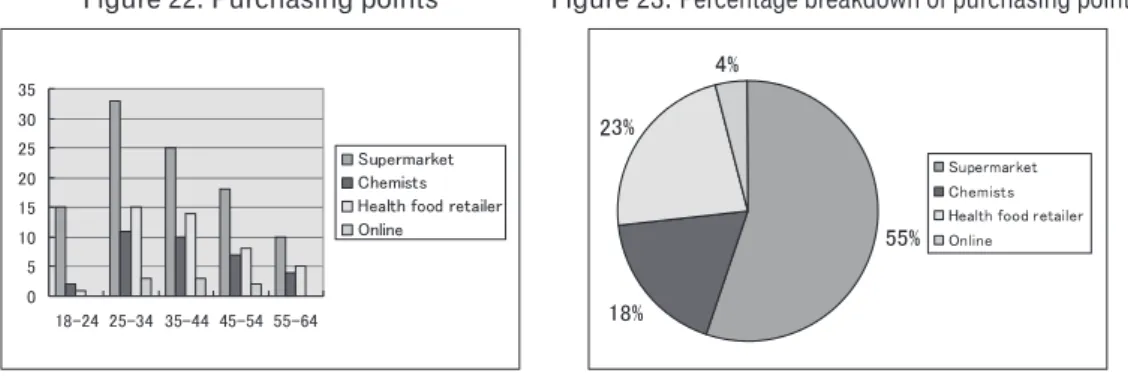

4. Where do you normally purchase health food products?

The graph reveals that most of the sample visit supermarkets, chemists and health food retailers to purchase health foods. However, the supermarkets are now the largest source of health food purchasing, with nearly 50% consumers buying at them.

The health food retailers achieved just under 25% health food retailers probably still cater for the more specialist consumer and offer them a wider choice than the supermarkets

Figure 21

will want to stock. However the health food retailers and the supermarkets between the account for 78% of purchases.

From the age 45 year olds, around half of the respondents preferred the independent retailers. These percentages may mean that younger people or families choose the most convenient place to buy health products, namely supermarkets.

Internet purchasers said they used the online method because they found it easier to purchase more specialised products such as black cohosh, fucoidan and CoQ10. Other internet purchasers just preferred the home delivery aspect.

This result shows that the success of functional food and drinks depends not only on the health benefits, but also on the level of convenience of the selling place that consumers can obtain the benefits.

6. What kind of image or impression do you have about Japanese products?

1.Good Quality 2.Expensive 3.Healthy

4.Reliable/Trustful 5.Good Brand Image 6.Other Comment 7.Missing

The sample shows 21% of the sample believed that Japanese products represent good quality but are expensive. This is a good basis for Company A to work from but clearly the company has to be mindful about its price setting.

7. Were you aware that vinegar was good your health?

Before the next question, the author gave a brief review of the product and its effectiveness. In the online survey, the explanation of the product is on the page.

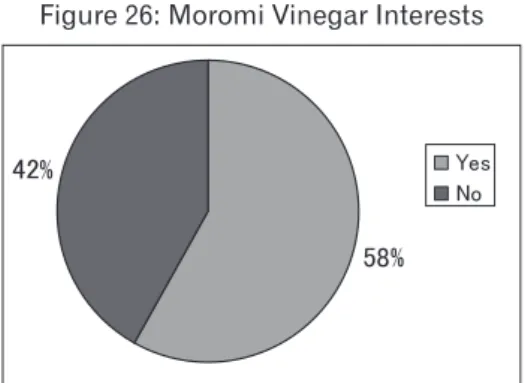

8. Would you be interested in the Japanese product Moromi Vinegar?

Surprisingly a high proportion (58%) of the respondents said they have an interest in Moromi Vinegar

However, more than 40% of respondents said they did not believe the health claims of this product.

Figure 25: Awareness of Drinking Vinegar

The results show a very similar match with figure No.7 (cross tabulation survey with functional food buyer by Socio-economic Group). 58% of respondents were interested in Moromi Vinegar. Women were much more interested than men but this is may be that women were more likely than men to agree with the survey statement. In terms of age, interest in Moromi Vinegar was relatively positive for the 55 to 64 year-old and 45 to 54 year-old categories, followed by those aged 35 to 44. on the other hand, Moromi Vinegar had little interest from the 18-24 age group.

Clearly Moromi Vinegar should be more specifically targeted at the older age groups and in particular women over the age of fifty who are increasingly better informed and health conscious.

9. Do you think £9.99 is value for money for a 720ml bottle (1 month supply) ?

From the result, 38% of the surveyed were happy to buy at the £9.99 price range given that the effectiveness was true. However, 62% were not happy with the price. From the comments it seems likely that these people may need more information concerning Moromi Vinegar before believing that the price is a reasonable one. In Japan and Taiwan there is

Figure 27: Moromi Vinegar interest by

Social-economic group Figure 28: Moromi Vinegar Interest by Age group

a pronounced trend in all stores to let customers sample new products so these comments reflect that experience.

4.2 MIXI‐Japanese Social Network System Survey

Mixi is now the second most visited Japanese website after Yahoo in Japan. It already has 6.5 millions members (Stone, 2006). New users are require an invitation from a friend who already uses the services (McClure, 2006). Over 900,000 online communities exist in the Mixi sharing diverse interests such as “Passion Fruits Crazy”, “University of Tokyo” and “Michel E. Porter”. Communities can be created by any Mixi user, it has a potential to gather more than 50.000 active members (Lewis, 2006). The benefit is these communities can be formed from anything such as company colleagues, former classmate, sports fun and people with shared interests who gather together to share information.

The author set up a questionnaire on this site in the community called “Japanese living in UK” and “Japanese Entrepreneurs in UK”. Due to the limited space per person only two questionnaires were allowed.

Q1. Do you normally purchase any kinds of functional food in the UK?

The chart shows nearly 60% of Japanese respondents living in the UK purchase some form of functional foods. As mentioned before, Japan has been a pioneer in the area of functional foods and has already established a system for approving them, granting such products individual health claims for specific health needs based on approved and sufficient research data. So Japanese expatriates are no strangers to the concept of functional foods whether in Japan or the UK.

Figure 30: Japanese Functional Food buyer

Yes 445

No 286

Q2. Would you purchase Moromi Vinegar if available in the UK and if so, what would you consider a reasonable price for a 720ml bottle (1 month supply)?

According to the chart, 58% of respondents answered they may buy Moromi Vinegar if the company launched it in the UK, but most of the people would prefer to spend less than £10. Give this Company A will have to consider whether it should target the expatriate community as a base to start from or should target both them and UK consumers. Clearly the company will have to consider the £5 to £10 price range very carefully and maybe another survey closer to the possible launch.

4.3 Interviews

4.3.1 Interview with Mr. O, Manager of Japanese Food retailer in London.

Mr. O's experience led him to believe that the majority of Japanese expatriates in the UK today were students. The expatriate community working for Japanese companies in the has been in steady decline since the downturns in the Japanese economy (two in the 1990s and one in the early 2000 period). Consequently the spending power of the Japanese community has been in decline and shifting in nature. The company strategy has consequently moved from selling premium priced products to cheap bulk selling to cater for the student population.

Figure 31 Table 4 Under £5 192 Under £10 92 Under £15 14 Under £20 0 Not buy 215 Total 513

Further Mr. O stated that whereas previously 90% of their customers were Japanese expatriates nowadays 50% of customers were British. He believes that this is the result of Japanese food becoming more popular in the UK and probably the result of Japanese food being perceived as providing a more healthy diet. This was also reflected in the growth in popularity of Japanese restaurants in London which may also reflect the move to eating out rather than eating at home.

While Mr. O felt that Moromi Vinegar was an interesting product, selling it in the current situation would be difficult because:

1. Two giant distribution companies dominate in the UK. One is called JFC Ltd and the other is Tazaki Foods. Their Shop goods are all supplied from these companies.

2. Due to decrease of employed Japanese expatriates, strategy had moved from the premium price range. Until Moromi Vinegar acquired publicity in UK, they would not have enough space or motivation to promote Moromi Vinegar.

Mr. O suggested: 1. Online selling

He agreed to sell our product online if the company would pay a commission.

They would not need to keep the product in stock as the product would be delivered directly from Company A.

2. Collaboration with well known Japanese restaurants - maybe for dressings

To promote this product, it may be a good idea to collaborate with a celebrity Japanese chef or a famous Japanese restaurant in the UK such as Nobu.

He said some British customers come to their shop to buy same ingredients which they used for dressings so maybe Company A could develop new product such as Moromi Vinegar Dressing.

3. Find another Japanese company for a joint export relationship or group exporting. 4.3.2 Interview with Mr. D, CEO of London based Japanese food wholesaler.

This company is a privately owned London-based company established 20 years ago. It is Europe's leading supplier of authentic and organic Japanese foods. It offers the leading range of traditional organic Japanese foods which are available in bulk for the catering trade and as pre-packs for retail shops.

Chairman Mr. D spent 20 years in Japan developing the range of foods made to time-honoured recipes, following the company's food integrity philosophy. Their company respects appropriate traditional technology and the environment.

Findings from this interview

products. When he started his business the majority of people were unaware of Japanese products but recently many retailers were showing an interest in Japanese products.

Mr. D thought that Moromi Vinegar was a very unique product however the stumbling block for UK consumers would be acceptance of the concept of a drinking vinegar as a health product. It might be better to use it as an ingredient in another health related product such as an energy drink or a yoghurt. Many functional food manufacturers are now seeking new ingredients to attract consumers. Company A should consider this food culture difference very carefully.

Mr. D said, “Moromi Vinegar is a difficult concept for UK consumers therefore it will necessarily to use effective packaging and labeling.”

According to Mr. D, Company A should consider changing the packaging to make it more acceptable to UK consumers as food labeling provides essential information for understanding, choice and utilization of the product.

Their company already has some vinegar products such as balsamic and apple cider vinegars however the volume of sales has been weak despite signs of improving. Consequently Mr. D felt it would probably be difficult to launch a new vinegar product. Additionally he thought, Moromi Vinegar may incur significant advertising costs which Company A may find difficult to finance so it may be better to try a joint venture.

4.3.3 Interview with Mr. K, the Food & Agricultural Department Director of JETRO London. JETRO is Japan's official trade promotion association supervised by Ministry of Economy, Trade and Industry.

Established in 1958 and originally set up to promote exports from Japan JETRO activities have stressed both import and export promotions in recent years. JETRO overseas office provides information on overseas markets for Japan's exporters and information to foreign companies interested in business in Japan.

Mr. K stated that although JETRO has been pro-active in promoting exports from small and medium-sized Japanese companies there had been little success for them in the UK and be suggested that he TTPP (Trade Tie-up Promotion Programme) might be more fruitful for a company like Company A.

TTPP is an online database offered by JETRO which enables both foreign and Japanese companies to register their company profile free of charge to promote links with the business matching. The companies just need to register their business model and proposals in both English and Japanese and the site can be regularly updated so enabling the transmission of company and product information. It might be the ideal gateway to contact potential contacts. There are many different categories listed on the site but a product like Moromi Vinegar could be registered under the Beauty and Health section.

4.4 Marketing Mix from Questionnaires and Interviews 4.4.1 Product

Moromi Vinegar is 720ml capacity in bottle. The best recommendation for this supplement is to take it two times in the day, once in the morning and then again in the evening. A measuring cup is included in the package.

Moromi Vinegar is currently on unknown and an unsought product, a consumer good that the consumer either does not know about or knows about but does not normally think of buying. In the UK people do not know about Moromi Vinegar and think about vinegar as a dressing for food but not as a drink for health benefit purposes. By its very nature, an unsought good requires a lot of advertising, personal selling and other market efforts (Kotler et al, 2005).

While the results of this study are largely encouraging to the commercial prospects of Moromi Vinegar, cautionary notes are warranted. No sizeable market for Moromi Vinegar products will evolve without familiarity of the product concept among UK consumers and the approbation of the medical community. An effective product must also be both sophisticated and professional in terms of image and a premium brand image if deemed necessary needs a well thought out label design.

4.4.2 Price

A common pricing method among retailers is mark-up pricing. The market price of this vinegar in Japan is 3200 yen (around £15). However, Moromi Vinegar is a by-product of Awamori production so it is essentially a low cost product which gives some room for price-flexibility on the part of Company A. The Business Insight survey (2003) pointed out almost 95% of companies agreed that the pricing policy of health foods is absolutely vital in respect to the firm's ability to sell the product.

Company A can launch Moromi Vinegar as a premium priced health food product but should seriously consider the advertising and personal selling supports that an unsought good will demand.

4.4.3 Promotion

One obstacle that needs to be dealt with is that section of consumers who are sceptical about the health claims of functional food producers. It will be necessary to gather scientific evidence presented by experts and develop a track record for the product doing what it is supposed to do, “walk the walk as well as talk the talk”.

Recommendations as well as promotional activities will help spread the word. The challenge for Moromi Vinegar is to convey this message to the consumer.

Although there has been considerable research about Moromi Vinegar in Japan, it will be absolutely essential to get other forms of recommendation from different sources in the

form of British organizations, authorities and researchers.

The company needs to offer nutritional support services on their website and on a consumer helpline as the company is already doing in Japan. The customer help line number and web site address are both advertised prominently on the packaging for the brand in Japan and must be replicated in the UK product form.

Direct mail may be useful, research shows that people want to know more about how to manage the diseases they suffer from so potential customers could be encouraged to join a Moromi Vinegar mailing list to find out more about diabetes or other illnesses that Moromi Vinegar could help with.

To promote the product to Japanese customers living in the UK, the company probably can use Japanese community free newspapers. There are 5 different free papers within the Japanese community (Eikoku News Digest, Journey etc).

4.4.4 Place

A channel of distribution is a group of individuals and organization that direct the flow of products from producers to customers. Distribution involves activities that make product available to customers when and where they want to purchase them (Dibb, et al, 2001). Providing customer satisfaction should be the driving force behind all marketing channel activities.

As mentioned before, consumers are most likely to buy functional food in the major supermarkets with health food retailers and chemists following in second and third place. There are more than 7200 health food industry outlets in UK, Holland & Barrett and GNC are the two largest retail chains in the UK and both are owned by the same parent company called NBTY.

Most, but not all, channels of distribution have marketing intermediaries, although there is currently a growth of direct marketing with some suppliers interacting with consumers without the use of intermediaries.

Company A needs the intermediary approach in UK however, this will be difficult until Moromi Vinegar can acquire greater publicity in the UK.

On the other hand, direct mail and telephone selling are part of the direct marketing category which is used to create brand awareness and stimulate product adoption.

Throughout Europe, direct mail is widely used to generate orders, pre-sell prior to a sale call and screen out non-prospects (Palmer et al, 1999). The suppliers of these external lists often undertake the complete direct mail operation for clients, from indemnification of recipients and compilation of list to production of printed material. This is another option that should seriously be considered by Company A as is the world-wide-web option. As more and more households connect to the Internet through increasing numbers of connections world wide, confidence in using this medium for transactions is growing. In UK, a large

number of websites are now selling health related products. Some emerged from the mail order business, while others began as Internet start-up companies.

5: Conclusion 5.1 Introduction

Europe is the third largest functional food market in value behind that of Japan and the US. Whereas the overall food market is relatively stagnant in the UK in contrast, the functional foods and drinks market seems to have a long-term opportunity for steady growth.

People are eating more calories than they need. They are eating far too many unhealthy foods and to compound the problem do not take enough exercise. The consequences are dramatically increasing lifestyle related diseases such as obesity and high blood pressure amongst the UK population.

According to Toyokawa (2012), the outlook for health food and health products is bright, with favourable demographic changes helping to boost demand. Consumers are becoming increasingly aware of healthy eating and are also more prepared to take control of their own destiny with healthcare products and remedies.

However, the major problem for Company A is that Moromi Vinegar is an unknown entity to the UK public. An unsought product which the UK consumer knows nothing about or maybe knows about it but does not normally think of purchasing. In the UK people do not know about Moromi Vinegar and further think of vinegar as a condiment or dressing for food and certainly not as a drink that can improve their health. By its very nature, Moromi Vinegar as an unsought good will require a considerable amount of advertising, personal selling and other forms of market efforts.

5.2 The Cost of the Market Entry

Launching new innovative products is a costly process requiring considerable investment includes promotion and advertising costs. However, there is no guarantee of market success, itself a function of the investment and advertising best suited to UK market conditions.

Moromi Vinegar as a product needs to become a familiar one in the UK market if it is to become successful. Although many smaller specialist companies are operating within the UK market, consumers normally have more confidence in the manufacturer of brand leaders. A well-known, respected name goes a long way in gaining the necessary acceptance of a new product. Consumers are more likely to make an early decision to try something new if they are “familiar” with other products from the same manufacturer, even if the new product is a totally different kind of experience.

manufacturers said that they were planning to launch a new functional food sometime in the future. If this does become the case, then the health food market is likely to become increasingly more competitive and consequently even more difficult to enter.

5.3 Findings

The investigations found that most respondents do purchase health food products. This tends to confirm the increasing maturity of functional food products. The heavy users of functional food products are mainly the 35 - 55 year old females and the 40 - 60 year old males. The higher income groups represent the main health food consumers and this confirms the view that it is the higher income groups that pay more attention to their diet and health and can afford to purchase health food products that normally operate in the premium price range. There is a high degree of probability that a significant percentage of the housewife purchases of functional foods come from families in the higher income groups. Students are also frequent consumers of health foods although they do not have the purchasing power punch necessary to make a significant impact. However it is likely that a significant percentage of students do (and have done so in the past) come from families in the higher income groups although this is a changing variable as more and more young people come into higher education (in line with current government policy). So possibly in the future the student aspect of demand may well not boost the demand for health foods. The Mixi (Japanese social network site) research showed that more than half of the respondents would probably buy Moromi Vinegar in the UK if the price range operated somewhere between five to ten pounds. However, the current composition of Japanese expatriates in the UK are primarily students and not the office workers of the past.

This means that if Company A chose to initially target the Japanese community in the UK as a starting point (for expanding into the wider domestic market) it may have to adopt different strategies for different sections of the market as a whole. Namely adopt a low price (non-premium) version of the product (maybe a mini-bottle) for the Japanese ‘market' while marketing a premium version for the off UK purchasers.

The success of market penetration by Moromi Vinegar will be contingent on both proof of its health effects and a widely received recognition of the product. Even though many health benefits are associated with the use of Moromi Vinegar, the image of vinegar as a health drink at present would not sit easy with the UK population. The implication for promoting and advertising Moromi Vinegar is to bring UK consumers to the point of accepting the idea of a drinking vinegar, maybe along the lines that Yakult is advertising on television at the moment (giving the expert opinion of the inventor, Dr. Shirota, about the health benefits).

Further analysis shows that the success of functional food and drinks depends not only on the health benefits, but also on the level of convenience that consumers can obtain those

benefits. As with the above discussion Company A will have to consider which section of the population it is targeting and convenience could mean changing the product itself by making the health vinegar an ingredient within a new innovative product such as a handy breakfast drink. This may be one strategy to overcome the bias against a drinking vinegar. This product is a “one of a kind product” in the world therefore we do not have a direct competitor in terms of vinegar health drinks. However the product will face an indirect competitive process from health food producers who also supply complementary medicines, health foods and supplements that lay claim to dealing with diabetes and high blood pressure. As economic theory teaches, in principle all goods and services are substitutes for one another. So Company A may well be a monopoly in terms of being the only producer of Moromi Vinegar, the market it operates in is akin to a form of monopolistic competition. According to our questionnaire, innovative new products like Moromi Vinegar are an important stimulus to the market and provide a necessary dynamic to the competitive process. New brands that become established can be extended and represent important capital for the future growth of the functional foods industry and market. Such activity is likely to involve partnerships and alliances to produce the necessary investment funds and resources. It also may require a vigorous advertising campaign to penetrate the market. The implication for Company A as a small company is that it will need to form alliances with other firms in order to generate the necessary investment for whatever form its overall strategy takes. This is particularly true for advertising to put Moromi Vinegar on the UK ‘map'. Increased dependency on ingredient companies due to the growth of functional ingredients is another ‘road' that Company A will have to consider. Scientific claims may not be strong enough to influence sceptical consumers about functional food and drinks, if they do not trust the brand. Consumers are more likely to trust a well-known brand. Full-service providers are a cost efficient method for obtaining functional ingredients.

The other option is to invest in research and development within the company and keep the research in house, although this again is probably only available to the larger manufacturers. However innovation does not necessarily have to be expensive as illustrated by the advent of Moromi Vinegar itself.

6. Recommendations

Consumer awareness of functional foods is increasingly high in the UK and demand has been strong for a long time, but the gap between potential and actual demand remains. To encourage those potential consumers to actually buy Moromi Vinegar it is necessary to make the product more readily available in convenient places of purchase. Consequently Company A needs to find the right partner in the distribution channel or promotion matrix given the expense of our prior costing exercises.

but this would have to be predicated on finding a suitable partner company.

Today, there is both growth and expected future growth in the functional beverages market many companies are consequently planning to launch new health related products. This may help Company A Ltd in finding a suitable partner but on the other hand it may bring the disadvantages of increased competition. Multinational companies such as Nestle are continually extending their range of health food products, aiming to include more varieties and brands. At the same time, the grocery multiples are developing their range of own-label functional products which may attract consumers who do not buy at the specialist retailers. Moromi Vinegar is marketed with specific benefits so tends to be more of a niche product that would feel more at home in the specialist health food retailers. However which type of outlet is used is a problem that needs to be considered after the success or otherwise of forming a partnership deal and to what extent the partner organization is already linked to UK outlets.

Other issues that need to be considered are

● To rethink the design, packaging and possibly the name of the product to make it more

UK market friendly. Moromi Vinegar is only a proposed brand name at present.

● To possibly market the product for different sections of the UK market, namely treat the

Japanese expatriate market differently from UK citizens. This could be taken further by differentiating the product for the higher and lower income groups.

● The prior point will also have implications for the pricing strategy adopted

● Given the previous two points the advertising and which forms it should use should be

carefully considered.

For the reasons outlined previously in our three costing scenarios, at this stage of the business, Company A should not try to enter the UK health food industry. However, the company should keep its eye on the UK market for encouraging developments and in the meantime consider new strategies along the lines outlined previously. For example as a start-up to an advertising campaign Company A should build its own website as the power of the Internet cannot be underestimated given the recent success of pop groups that have initially bypassed the traditional music companies. This would be a good start for the branding process and a lot cheaper than the strategies in the previous chapter.

While keeping its eye on the UK market, Company A should keep attending exhibitions and conferences. Various exhibitions and conferences relating to functional foods in the UK include the Healthy Foods Summit 2013, organized by New Hope Natural Media Europe in London and the Functional Food Summit 2013.

6.2 Limitation and Further Research Investigation

This study suffered from a number of limitations in respect to the interviews and surveys. Time limitation and scale limitation was crucial. Since only two firms and one governmental organization in UK were willing to talk to the author, the information gathered might reflect quite subjective views and possibly personal bias as well. In the interviews, time limitations affected the research producing small and limited perspectives and for more valid research, these limitations will need to be minimized.

Further investigations will require a greater volume and extension of interviews from a much wider variety of organizations (such as UK health food retailers, chemists, distribution channels, exporters) and compare the different opinions to complete a more comprehensive research. A common occurrence in the interview process was that critically important questions about the company were ignored or the answers moved away from the point at issue. While this will inevitably happen in future interviews maybe a wider sample will lower the probability of this event.

While a collective number of 300 (221 on the street and 79 online) people were involved in the different surveys certainly the street survey needs to encompass a larger sample than 221 to get a clearer view of UK consumer attitudes.

In view of the need of Company A to internationalise, and of the difficulties it faces in attempting to expand, there is a need for approaches and models that will improve the company's effectiveness, especially during the crucial first steps of foreign expansion. One of the most important early steps is the selection of an appropriate international market. This report has concluded that at Company A's present levels of know-how and accumulated capital the UK market is far too expensive and complex an entity to try and attempt an entry now. This report suggests a framework that can help rationalize and make more effective the international market strategy process for Company A.

This decision making framework attempts to minimize the weaknesses and to build upon the strengths of the Company A. To do so, it proceeds from the lessons learned from this UK study to the collection of information about a wider range of potential international markets and the gathering and analysis of a broader range of data about them It seems quite logical to assume that some disadvantages of the UK market may not be relevant or turn out to be necessarily crucial disadvantages in other countries.

In other to achieve Company A's internationalization, further study should be undertaken involving a similar but more extensive and intensive form of research in other suitable countries. These might be other Asian countries like Taiwan or South Korea where the concept of ‘drinking vinegar' is an already known concept.

REFERENCES

Business Insight (2004) Branding Health Food, Business Insight Limited, October 2004, [online] available at http://0-www.bi-interactive.com.lispac.lsbu.ac.uk (accessed 19 February 2007)

Business Insight (2005) Innovation in Functional Food and Drink, Business Insight Limited, November 2005, [online] available at http://0-www.bi-interactive.com.lispac.lsbu. ac.uk (accessed 25 February 2007)

Business Insight (2006) Targeting the Healthy Consumer, Business Insight Limited, September 2006, [online] available at http://0-www.bi-interactive.com.lispac.lsbu.ac.uk (accessed 19 February 2007)

Carey, T. (2002) Green Food Slump: Organic ‘not worth it', The Daily Mirror, London 6 September, pp.6-7

Choueke, M. (2006) Soft Drink Indies Fast Flow to Market, Marketing Week, Vol.29, lssue16,

Churchill, G. A. (2002) Marketing Research: methodological foundation, Eighth Edition, Ohio, South-western Thompson Learning

Corliss, R. and Lemonick, M.D. (2004) How to live to be 100, Time, New York, 8 October, Vol. 164 lssue 9, p40-49, 9p, 11c

Goldberg, I. (1994) Functional Foods: Designer Foods, Pharmafoods, Nutraceuticals, New York, Chapman & Hall Inc

Goldberg, I. & Williams, R. (1991) Biotechnology and Food Ingredients, New York, Van Nostrand Reinhold

Haberberg, A. and Rieple, A. (2001) The Strategic Management of Organisations, First Edition, Harlow, Pearson Education Limited

Hague, P. (1998) Questionnaire Design, Third Edition, London, Kogan Page Limited

Hague, P. & Jackson, P. (1998) Do Your Own Market Research, Third Edition, London, Kogan Page Limited

Heffeley, J. (2005) To Your Health, The Austin Chronicle, 3 June 2006, [online] available at http://www.austinchronicle.com/gyrobase/issue(accessed 25 Feb 2007)

Ikemoto, A. (2005) Food labeling Regulations in Japan: the Problems involved in the indication of Manufacturer on Processed Health Food, Food Function, Tokyo, March 2005, Vol.1, p11

Keynote (2006) Healthy Eating, August 2006, [online] available at http://0-www.keynote. co.uk.lispac.lsbu.ac.uk/kn2k1/ (accessed 9 March 2007)

Keynote (2006) Functional Foods, January 2007, [online] available at http://0-www. keynote.co.uk.lispac.lsbu.ac.uk/kn2k1/ (accessed 9 March 2007)