人口・労働・社会保障研究会

The Influence of Unions on Wages in Japan :

Taking into Account Factors Related to Corporate Governance

Hisashi O

KAMOTOTsukasa M

ATSUURAWith long-term employment and seniority-based payment, (enterprise) unions consist of Japanese employment practices. These practices had been highly praised for their efficiency by many academic researchers. However, after the collapse of the bubble economy at the beginning of 1990s, these practices have been severely criticized as the most significant source of the economic downturn. Along with the continuing economic downturn, the Japanese employment practices have been declined and the unionization rate also has been decreased. Many people show the reasons why Japanese unions have been weakened for several decades and most of them seems plausible. In fact, in recent spring offensives, the government has strongly intervened the wage determination process in labor-management negotiations, demonstrating its clout and in contrast to it, unions haven’t have much of a presence. However, even in such situations, unions have no small social significance. For example, when we remember that unions have had a role to enable long-term employment not only to foster human resources but also to build and keep sound labor relations, we will easily find unions in Japan still have an important role.

For the purpose stated above, we examine the influence of unions on wages in Japan taking into account factors related to corporate governance with the use of panel date on the firms listed on the first section of the Tokyo Stock Exchange. In creating variables concerning corporate governance, we focus on four attributes of corporate governance as follows: (1) owner management (2) management tenure, (3) foreign ownership, (4) financial institution ownership. First, we study whether unions as well as these four attributes of corporate governance respectively have influence on wages. Employing OLS with cluster standard errors, FE and RE, we show that unions and, both foreign and financial institution ownership have positive effects on wages. In the second step, we study the hypothesis that the magnitude of the influence of unions on wages varies depending on firm’s governance structure. Introducing interaction terms with unions, we obtain two results. The first one is that interaction terms with foreign ownership and those with financial institution ownership are positive with statistical significance even after controlling for the possibility of endogeneity problems by the use of IV and FE. The second is that interaction terms with owner management and those with management tenure are negative with statistical significance by the use of OLS, but they become statistically insignificant in the panel estimation. This may be because spurious correlations are incurred.

From our obtained results, we confirm that unions still have influence on wages in Japan.

1. Introduction

In Japan, the unionization rate has been declining steadily and collaterally, real wages have been in a declining trend. In order to resolve this situation, Japanese Government has been urging firms’ managers to raise wages blaming the drop in wages for continuing deflation. In contrast to positive attitudes of Japanese Government, unions cannot show their presence. However, it can be said that even in such a situation, unions have no small significance as actors to solve various social problems.

Unions have been a part of Japanese employment practices along with long-term employment and seniority-based payment. Especially in boom in1980s, these practices had been highly praised for their efficiency mainly by academic researchers. They explained that Japanese employment systems allow firms’ managers to build sound relationships with employees based on long-term perspective blessed with institutional complementarity with components of corporate governance such as main-bank system. Aoki (1994) also theoretically argues that features of corporate governance are likely to have some complementarity with employment practices. However, such favorable situations for Japanese economic systems were drastically changed within a short period of time afterward. The collapse of the bubble economy took place at the beginning of 1990s. Since then, Japan’s economic growth rate has continued to be declined (the lost decade).This lead to severe criticism toward the inefficiency of management of Japan’s firms and Japanese employment practices. Even today, their bad reputation remains almost unchanged although long-term employment is strongly supported by quite a few people.

However, it is worth noting that as previously mentioned, there is some complementarity between Japanese employment systems and features of corporate governance. Among three components of Japanese employment practices, there is rich literature on unions’ effects on wages or employment. In contrast to growing literature on unions’ effects (including complementary effects with governance structure) on employment, few studies pay attention to the complimentary effects on wages.

We examine the influence of unions on wages in Japan taking into account factors related to corporate governance using panel date on firms listed on the first section of the Tokyo Stock Exchange. First, we examine whether unions have influence on wages. Next, we examine whether there exist complementary effects between unions and factors related to corporate governance.

This paper has three distinctions. First, we incorporate a perspective of the structure of

corporate governance into the analysis of the influence of unions on wages. As mentioned

before, although there is rich literature in which effects of unions and those of the

structure of corporate governance on wages are examined respectively, few papers deal with interactive effects of these factors. Second, the data used are suitable for our purpose.

We create panel data for firms listed on the first section of the Tokyo Stock Exchange.

Resulting dataset contains almost all the Japan’s leading companies except unlisted ones.

Most of previous studies intended to measure unions’ performance by employing corporate data have drawbacks of small sample on the whole. In addition, although many previous studies deal with unions’ effects on wages, none of them but Noda (1997) employs panel data. Third, in regard to attention to dealing with the possibility of endogeneity, it is insufficient for most of the previous studies on unions’ effects on wages since they just adopt a strategy of introducing 1period lag variables in common.

Additionally, since many studies are conducted with cross sectional data, few methods are left for dealing with potential endogeneity. In our analysis, we deal with potential endogeneity by combining instrumental variables estimation and fixed-effects estimation in terms of exploiting advantages of panel data.

The paper proceeds as follows. We review the existing literature in Section 2. In Section 3, we show hypotheses to be tested, describe the data used for our estimation and explain empirical strategy. In Section 4, we report the estimation results and discuss them. Section 5 concludes the paper.

2. Previous Studies

First of all, we show previous studies concerning the influence of unions on wages and the influence of governance structure such as that of holding stocks on wages. There has been rich literature on the influence of unions on wages as Freeman and Medoff (1984) or Card (1996). Which are regarded as seminal papers. In Japan, many studies have been conducted concerning the influence of unions on wages by the use of both corporate and individual data. Among them, Brunello (1992), Tachibanaki and Noda (2000), and Morikawa (2010) used corporate data. Tsuru and Rebitzer (1995), Noda (1997), Nitta and Shinozaki (2008), and Hara and Kawaguchi (2008) employed individual data. In regard to unions’ effects on wages, roughly speaking, studies conducted using data in the early 2000s as Nitta and Shinozaki (2008), or Hara and Kawaguchi (2008) found a definite union wage premium although, in contrast, those conducted with data in 1990s or before as Tsuru and Rebitzer (1995) or Tachibanaki and Noda (2000) revealed a negligible one

1). Next, we introduce previous works on corporate governance for Japanese firms. As for ownership structure, focusing on family-owned firms, Morikawa (2013) examined

1) Brunello (1992) examined wage differences between unionized firms and nonunionized ones and even found unions’ negative effects on wages.

differences in productivity growth and shows that although family-owned firms are inferior in the percentage of productivity growth to their counterparts, significant differences are not confirmed between them, focusing on listed family-owned firms with non-family-owned firms. Focusing on the influence of foreign shareholders, Kimura and Kiyota (2007) revealed that foreign-owned firms achieve higher productivity than domestically-owned firms. From the similar point of view, Noda (2013) examined the influence of main-bank systems and the influence of the ratio of stocks held by foreigners respectively and revealed that firms closely related to main-bank systems are likely to curb restructuring and those with higher ratio of stocks held by foreigners are likely to promote restructuring. In regard to the influence of corporate governance on Japanese employment systems, Abe and Hoshi (2007) indicated that firms with nontraditional ownership structure characterized by higher ratio of stocks held by foreigners are likely to have nontraditional style of human resource management. Kawaguchi and Nishitani (2011) revealed that firms with strong governance exerted by institutional investors are likely to have female regular employees and supervisory employees.

3. Hypothesis and data

3.1. Hypothesis

As mentioned before, the purpose of this paper is to analyse the effects of unions on wages taking into account factors related to corporate governance. Although a major concern is placed on the examination of whether unions have influence on wages, to study the function of factors related to corporate governance is also important. To analyze the latter, we choose four factors concerning corporate governance as follows; (1) owner management, (2) management tenure, (3) foreign ownership, and (4) financial institution ownership.

As for causal paths from these governance factors to wages and, two patterns seem valid as follows. The first is that governance factors affect wages by way productivity or profitability.

The second is that governance factors affects wages by determining labor share. We focus on the latter, for we control firms’ performance as productivity or profitability using operational profits and operating profits. Then, we put forward several hypotheses to be tested for governance factors mentioned above.

The first one is that owner management, that is, managers whose firms are family- owned or those who have long tenure in the position have influence on wages positively.

This hypothesis highlights the attributes of firms’ managers. Managers whose firms are

family-owned or those who have long tenure in the position are likely to demonstrate

powerful initiative. In regard to the influence on wages, two (opposite) assumptions can be made. The first is that it has positive impacts on wages. Managers with such attributes may seek to establish harmonious labour relationships from a long-term point of view against a backdrop of their managerial initiative. In such a way that they studiously avoid wage cuts in fear of discouraging employees and of losing trusting relationship with them even in poor business conditions, wages are likely to be kept relatively high. The second is that it has negative impacts on wages. In contrast to the first case, managers with the same attributes may be fascinated by building coordinated relationship. In such a case, they may be apt to make such arbitrary decisions as cutting down wages for employees.

This is because they are virtually free from interference from other stakeholders and this results in the absence of adequate monitoring.

The second and the third are on ownership structure, i.e., the influence of foreign and institutional shareholders. The second hypothesis is that higher ratio of shareholdings by foreigners affects wages. As for the relationship between foreign shareholders and employment, Noda (2013) revealed that firms with higher ratio of foreign shareholdings are likely to promote restructuring. If this is because foreign shareholders are demanding for managers seeking for short-term profitability, we conjecture that higher ratio of foreign shareholdings leads to wage cuts. In other words, it affects wages negatively. On the other hand, there also are some studies pointing out that firms with higher ratio of foreign shareholdings are unlikely to adopt Japanese employment systems. In general, employees are supposed to be risk-averse. Therefore, if a firm with less stability in employment, holding others constant, intend to hire an employee, the firm have to offer corresponding amount of risk premium offsetting the inferiority in stability in employment. Considering this, we make additional assumption that higher ratio of foreign shareholdings have positive influence on wages. The third hypothesis is that higher ratio of shareholdings by financial institutions affects wages positively. Financial institutions such as banks, securities and insurance companies are assumed to attach more weight to long-term relationships with their client companies, supporting managers in having long- term, harmonious labor relationships.

The fourth hypothesis is on complementary effects with unions. Since the directions of effects on wages of above-mentioned attributes of firms’ managers and foreign ownership are hard to be uniquely assumed, it is also difficult to make assumptions on the directions of complementary effects of these factors. Therefore, we make one assumption, that is, only on complementary effects of ownership by financial institutions. As mentioned before, higher ratio of shareholdings by financial institutions are expected to raise wages.

If unions exert positive effects on wages, it should amplify these effects. Therefore,

complementarity with ownership by financial institutions are assumed to have positive

influence on wages.

3.2. Data

Our sample consists of the firms listed on the first section of the Tokyo Stock Exchange (excluding those with the Nikkei industry code classifications for banking, insurance, and securities, and other credit companies and holding companies) from fiscal year 2004 to 2013.

As a dependent variable, we use logarithm of mean wage per employee. Descriptions on explanatory variables are show below. At the beginning, in order to examine the influence of unions on wages, we create union dummy (UNION) indicating 1 if a firm has at least one union and 0 if not. Next, we create owner management (OWNER) dummy indicating 1 if a firm is family-owned and 0 if not. We identify family-owned firms in such a way that a firm is regarded as family-owned one only if its representative, generally corresponding to its president or former president, occupies one of the ten largest shareholders of the firm.

Years in operation (DURATION) indicate the length of years from the time of founding to the closing date of the period studied. Management tenure (TENURE) is defined as the time of length from when a manager begins to function as the president to the closing date of the period studied. Foreign ownership (FOREIGN) indicates the rate of

Table 1 Definitions of Variables

Variables Definitions

WAGE The amount of average wages (=total labor cost/the number of employees) UNION Equals 1 if a firm has at least one union and 0 otherwise

REIGN The length of years from when a manager of a firm started his or her career as a president to the latest closing date

OWNER Equals 1 if a manager of a firm is included in the 10 largest shareholders and 0 otherwise

DURATION The length of years from when a firm was found to the latest closing date

FOREIGN The rate of the number of shareholdings by foreign investors to that of total stocks issued

FINANCIAL The rate of the number of shareholdings by financial institutions to that of total stocks issued

ASSET The amount of total assets GSALES The growth rate of sales OPROFITS The amount of operational profits EMPLOYEES The number of employees (in logarithm)

shareholdings by foreigners. And financial institutional ownership (FINANCIAL) indicates the rate of shareholdings by financial institutions. ROA is the rate of current profits to total assets. Table 1 describes definitions of variables. In the estimation conducted below, all the explanatory variables used are 1period lagged for dealing with the possibility of endogeneity.

As for the data source, our sample is mainly collected from the Nikkei Needs-Financial QUEST 2.0 and the Nikkei Telecom 21 provided by Nihon Keizai Shimbun. Table 2 shows descriptive statistics.

Table 2 Descriptive Statistics

Variable Obs Mean S.D.

WAGE 8856 2.083 0.374

UNION 8856 0.706 0.456

FOREIGN 8572 0.126 0.117

FINANCIAL 8588 0.251 0.126

OWNER 8856 0.137 0.344

REIGN 8856 0.072 0.084

ASSET 8856 0.261 0.774

GSALES 8856 0.019 0.248

OPROFITS 8856 0.009 0.038

DURATION 8856 0.584 0.229

EMPLOYEE 8856 6.870 1.201

MANUFACTURE 8856 0.615 0.487

CONSTRUCTION 8856 0.080 0.272

AGRICULTURE 8856 0.002 0.050

MINING 8856 0.003 0.051

MARCHANDISE 8856 0.031 0.173

WHOLESALES 8856 0.007 0.081

ESTATE 8856 0.020 0.141

TRANSPORT 8856 0.057 0.231

TELECOM 8856 0.006 0.075

ENERGY 8856 0.015 0.123

OTHER INDUSTRIES 8856 0.165 0.371

4. Results and Discussion

4.1. Estimation Results without interaction terms

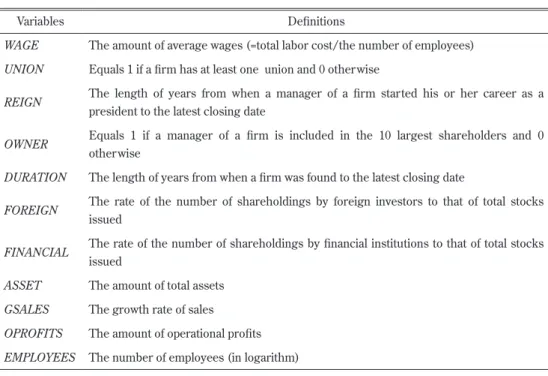

Table 3 lists the regression results without interaction terms. We use three types of estimation methods, pooled OLS with clustered standard errors, fixed-effects estimation

Table 3 Results with OLS, Fixed-effects and Random-effects (without interaction terms) [1]

OLS

[2]

FE

[3]

RE

[4]

OLS

[5]

FE

[6]

RE

UNION 0.107**

[0.0258]

0.0601*

[0.0262]

0.0845**

[0.0194]

0.110**

[0.0257]

0.0673*

[0.0265]

0.104**

[0.0198]

FOREIGN 0.175+

[0.0961]

0.124**

[0.0480]

0.136**

[0.0435]

0.186+

[0.0953]

0.216**

[0.0476]

0.244**

[0.0431]

FINANCIAL 0.309**

[0.0812]

0.247**

[0.0565]

0.280**

[0.0495]

0.337**

[0.0796]

0.271**

[0.0568]

0.403**

[0.0477]

OWNER -0.0636**

[0.0243]

0.00368 [0.00822]

0.000254 [0.00815]

-0.0793**

[0.0220]

-0.0133+

[0.00775]

-0.0212**

[0.00762]

REIGN -0.189+

[0.0995]

-0.0697 [0.0440]

-0.0831+

[0.0424]

-0.176+

[0.0989]

-0.0577 [0.0444]

-0.0678 [0.0427]

ASSET 0.0467**

[0.0174]

-0.0271 [0.0297]

0.0344*

[0.0145]

0.0448**

[0.0170]

-0.00222 [0.0299]

0.0354*

[0.0152]

GSALES -0.0425

[0.0333]

-0.0188*

[0.00833]

-0.0228**

[0.00818]

-0.0277 [0.0257]

0.00324 [0.00798]

-0.00118 [0.00786]

OPROFITS 0.186 [0.155]

0.243**

[0.0582]

0.248**

[0.0583]

0.257 [0.164]

0.293**

[0.0587]

0.322**

[0.0582]

DURATION 0.0336 [0.0523]

-0.644 [7.626]

0.125*

[0.0554]

0.0191 [0.0511]

-0.596**

[0.0869]

-0.123*

[0.0480]

EMPLOYEE -0.0269*

[0.0113]

-0.0121 [0.0129]

-0.0147+

[0.00833]

-0.0282*

[0.0113]

-0.0169 [0.0130]

-0.0228**

[0.00861]

Industry Dummy yes — yes yes — yes

Year Dummy yes yes yes no no no

Hausman 9.16 74.92**

F value 29.78** 29.17**

Observations 8570 8570 8570 8570 8570 8570

R-squared 0.088 0.05 0.081 0.026

(Note) + significant at 10%; * significant at 5%; ** significant at 1%

and random-effects estimation. As a result of Hausman test, the results brought by random-effects estimation are accepted. However, the assumption for random-effects estimation that individual effects are uncorrelated with regressors may be a bit too strong in regard to our sample and even the use of fixed-effects estimation may be inappropriate because union status shows little change. Therefore, we examine the results obtained by the three models with mutual comparison.

All the columns show that UNION is positively significant and indicate that wages in firms with unions are on average 6-11% higher than those in counterparts. This result is consistent with those brought by Freeman and Medoff (1984) and Hara and Kawaguchi (2008) and so on. Especially, the consistency with the results with the control of both personal and corporate attributes obtained in Hara and Kawaguchi (2008) showing 7%

union premium is worth noting. Among variables concerning corporate governance, both

FOREIGN and FINANCIAL are positively significant at the 10% significance level in allthe equations and this shows that the rise in the rate of shareholding by each type of shareholders is likely to raise wages. In particular, as for the influence of shareholding by financial institutions, there is a possibility that their efforts to support the establishment of cooperative labor-management relations based on long-term perspectives raise wages. On the other hand, neither OWNER nor REIGN is significant in fixed-effects estimation though they both are significant in OLS

2). REIGN is negatively significant at the 10%

significant level, but after controlling for year dummy, it becomes insignificant. Taking these into consideration, there can be a possibility that spurious correlation is incurred since time-invariant effects such as corporate culture are assumed to simultaneously affect both wages and these attributes.

4.2. Estimation Results with interaction terms

We have focused on the influence of each explanatory variable using only single terms for estimation so far. From now, we add the examination of complementary relationship between unions and other governance factors by introducing interaction terms

3).Table 4 shows the results with OLS with clustered standard errors. All the columns show that

UNION is positively significant. As for interaction terms, that with FOREIGN and that with FINANCIAL are both positively significant. On the other hand, that with OWNER and thatwith REIGN are both negatively significant.

Table 5 shows the results with fixed-effects estimation dealing with endogeneity by

2) OWNER is negatively significant at the 10% significant level without controlling for year dummy,but its coefficient is rather smaller than that of OLS.

3) The addition of single terms concerning governance factors on equations is not intended because multicollinearity may be incurred when it is done since union status is almost time-invariant.

eliminating time-invariant effects. The results of UNION are almost the same as those shown by Table 3 and Table 4. As for interaction terms, one with OWNER and REIGN are insignificant. As previously mentioned, this may be brought by spurious correlation. On the other hand, that with FOREIGN and FINANCIAL are still positively significant and this result shows that these two factors have robust effects.

Table 4 Results with OLS with cluster standard error (with interaction terms)

[1] [2] [3] [4]

UNION 0.106**

[0.0257]

0.0803*

[0.0329]

0.143**

[0.0262]

0.151**

[0.0276]

UNION×FOREIGN 0.217+

[0.118]

UNION×FINANCIAL 0.221**

[0.0829]

UNION×OWNER -0.0942*

[0.0394]

UNION×REIGN -0.291*

[0.122]

ASSET 0.0432*

[0.0176]

0.0472**

[0.0182]

0.0454*

[0.0180]

0.0451*

[0.0180]

GSALES -0.043

[0.0342]

-0.043 [0.0342]

-0.065 [0.0395]

-0.0648+

[0.0393]

OPROFITS 0.238

[0.165]

0.268 [0.173]

0.272 [0.169]

0.277 [0.169]

DURATION 0.112*

[0.0498]

0.0865+

[0.0511]

0.123*

[0.0513]

0.130*

[0.0511]

EMPLOYEE -0.015

[0.0112]

-0.012 [0.0105]

-0.009 [0.0110]

-0.009 [0.0111]

Industry Dummy yes yes yes yes

Year Dummy yes yes yes yes

Observations 8572 8588 8856 8856

R-squared 0.115 0.116 0.112 0.112

(Note) + significant at 10%; * significant at 5%; ** significant at 1%

4.3. Estimation Results by IV methods

The results obtained in the previous analysis imply the difficulty in dealing with endogeneity. This corresponds to the way of dealing with union status in this study. As mentioned before, union status is almost time-invariant. Therefore, it is hardly possible to create “variable” because of zero deviation from the mean concerning many firms.

Moreover, even if the deviation can be measured, there remains a possibility of measurement error. Angrist and Pischke (2009) recommended the use of instrumental

Table 5 Results with fixed-effects estimation (with interaction terms)

[1] [2] [3] [4]

UNION 0.0566*

[0.0268]

0.024 [0.0284]

0.0558*

[0.0264]

0.0599*

[0.0265]

UNION×FOREIGN 0.0984+

[0.0548]

UNION×FINANCIAL 0.246**

[0.0654]

UNION×OWNER -0.011

[0.0132]

UNION×REIGN -0.098

[0.0618]

ASSET -0.026

[0.0297]

-0.022 [0.0297]

-0.038 [0.0307]

-0.038 [0.0307]

GSALES -0.0194*

[0.00833]

-0.0190*

[0.00832]

-0.0273**

[0.00848]

-0.0274**

[0.00848]

OPROFITS 0.251**

[0.0583]

0.248**

[0.0582]

0.258**

[0.0608]

0.257**

[0.0608]

DURATION -0.165

[7.635]

-1.364 [7.630]

-0.284 [7.913]

-0.040 [7.912]

EMPLOYEE -0.012

[0.0129]

-0.012 [0.0128]

0.009 [0.0122]

0.009 [0.0122]

Industry Dummy yes yes yes yes

Year Dummy yes yes yes yes

Observations 8572 8588 8856 8856

R-squared 0.047 0.048 0.039 0.039

(Note) + significant at 10%; * significant at 5%; ** significant at 1%

variables estimation for this kind of problem

4). In order to deal with the possibility of endogeneity, we introduce IV estimation and compare the results with those obtained by fixed-effects estimation. Considering the results of over identifying restrictions test and weakly identified test, we pay attention to the potential biases brought by the use of IV. We use the following variables as instruments of UNION and FOREIGN; 2periods lags

4) However, as Himmelberg et al. (1999) pointed out, as for governance variables, it is difficult to find proper instrumental variables which are correlated with structure of holding stocks and are uncorrelated with firms’ performance.

Table 6 Results with IV (with interaction terms) [1]

2SLS

[2]

2SLS

[3]

2SLS

[4]

2SLS

[5]

FE2SLS [6]

FE2SLS [7]

FE2SLS [8]

FE2SLS

UNION 0.516**

[0.141]

0.393*

[0.171]

0.399**

[0.115]

0.147 [0.176]

0.208*

[0.104]

0.212*

[0.105]

0.208*

[0.104]

0.195 [0.120]

FOREIGN 1.343*

[0.571]

-0.0459 [0.110]

UNION×FOREIGN 1.797*

[0.164]

-0.0685 [0.164]

FINANCIAL 1.042*

[0.405]

0.0409 [0.165]

UNION×FINANCIAL 1.577*

[0.649]

0.0813 [0.251]

ASSET 0.0349*

[0.0166]

0.022 [0.0195]

0.0549**

[0.0182]

0.0559**

[0.0177]

-0.0145 [0.0348]

-0.0141 [0.0349]

-0.0147 [0.0348]

-0.0139 [0.0350]

GSALES -0.0186

[0.0275]

-0.0133 [0.0275]

-0.00822 [0.0247]

-0.0107 [0.0254]

-0.0061 [0.0172]

-0.00608 [0.0172]

-0.00596 [0.0171]

-0.00588 [0.0171]

OPROFITS -0.175 [0.268]

-0.0812 [0.241]

0.193 [0.185]

0.192 [0.196]

0.272+

[0.139]

0.273+

[0.140]

0.269+

[0.138]

0.268+

[0.138]

DURATION -0.163 [0.115]

-0.240*

[0.113]

-0.284*

[0.113]

-0.365**

[0.139]

-12.47 [17.92]

-12.27 [17.94]

-12.64 [17.84]

-12.95 [17.80]

EMPLOYEE -0.0880**

[0.0242]

-0.0936**

[0.0288]

-0.0575**

[0.0162]

-0.0663**

[0.0196]

0.0264 [0.0428]

0.0265 [0.0428]

0.0257 [0.0427]

0.0256 [0.0427]

Industry Dummy yes yes yes yes - - - -

Year Dummy yes yes yes yes yes yes yes yes

Kleibergen-Paap

Wald rk F statistic 8.24 6.822 13.221 6.844 40.777 24.445 85.931 29.862

Sargan p staistic 0.8812 0.7502 0.2509 0.2445 0.8126 0.818 0.766 0.772

Observations 7315 7315 7307 7307 7280 7280 7283 7283

(Note) + significant at 10%; * significant at 5%; ** significant at 1%

variables of OWNER, REIGN, FINANCIAL and use the following variables as instruments of UNION and FINANCIAL: 2 periods lagged variables of OWNER, REIGN, FOREIGN. In addition, we use fixed-effects estimation to cope with two types of reverse causality, time- variant and time-invariant. For this purpose, in regard to instruments, we add 2 periods lagged endogenous variables to those above-mentioned.

The results are shown in Table 6. The results of weakly identified test for UNION,

FOREIGN and FINANCIAL show they are not weak instruments5).In addition, the results of Sargan over identification test show the null hypothesis that there is no over identification is not rejected.

Column [1] shows that UNION and FOREIGN are positively significant. Column [2]

shows that interaction term between these two variables is also positively significant.

These results are similar to those brought by fixed-effects estimation previously conducted. Putting these together reveals that firms with unions and higher rate of shareholdings by foreigners raise wages regardless of whether we try to eliminate time- variant endogeneity with fixed-effects estimation or time-invariant endogeneity with IV estimation. In addition, Column [3] and column [4] show that the similar tendency holds for higher rate of shareholdings by financial institutions.

Lastly, we explain the results of IV estimation with fixed-effects. According the results of two tests for instruments above mentioned, our way of choosing instruments are valid.

All the columns ([5]-[8]) show substantial effects of unions on wage raise. However, in contrast to the results obtained so far, no interaction term with governance variables is significant.

5. Concluding Remarks

In this paper, we examine the influence of unions on wages and complementary effects between unions and several attributes of corporate governance. First, unions’ robust effects of raising wages are confirmed. This is consistent with most of the previous studies. In relation to the use of the data on the first section of the Tokyo Stock Exchange, it can be said that large unionized companies in Japan have tried to held back wage cut. As for governance attributes, the structure of holding stocks has effects on wages.

Specifically, complementary effects of higher rate of shareholding by foreigners and that

by financial institutions with unions are likely to raise wages. As for the complementary

effects concerning share holdings by financial institutions, several previous studies point

out that financial institutions respect long-term interest. There is a possibility that financial

5) However, the null hypothesis is rejected in column[3]-[4], so some reservation should be needed.institutions help client firms avoid wage cut as much as possible for the sake of fostering a long-term relationship with employees. On the other hand, the complementary effects concerning higher rate of shareholding by foreigners may be a little different from common understanding such as their attitudes toward seeking for short-term profitability even by taking advantage of labor adjustment. As for the reason, we conjecture as follows.

As Abe and Hoshi (2007) revealed, firms with higher share holdings by foreigners are unlikely to have Japanese employment practices. These practices are expected to assure employees the stability of wages and employment. In other words, higher shareholding by foreigners leads to lower stability of wage and employment. Under conditions where there exists considerable instability in wages and employment, firms have to pay higher wages including the amount of risk premium. And the amount of risk premium should be larger for unionized firms.

References

Abe, M. and T. Hoshi (2007) “Corporate Finance and Human Resource Management in Japan” in Aoki, H., Jackson, G., and Miyajima, H. (Eds.) Corporate Governance in Japan. Oxford University Press Angrist, J.D. and J.-S. Pischke (2009) “Mostly Harmless Econometrics”, Princeton Press

Aoki, M. (1994)“The Contingent Governance of Team: Analysis of Institutional Complementarity,”

International Economic Review Vol. 35, pp. 657-676

Brunello, G. (1992) “The Effect of Unions on Firm Performance in Japanese Manufacturing,” Industrial and Labor Relations Review, 45 (3), pp. 471-487

Card, D. (1996) “The Effect of Unions on Structure of Wages: A Longitudinal Analysis”, Econometrica 64 (4), pp. 957-979

Freeman, R.B. and J. Medoff (1984) “What Do Unions Do?”, Basic Books

Hara, H., and D. Kawaguchi. (2008) “The Union Wage Effect in Japan,” Industrial Relations, Vol. 47, No. 4, pp. 569-590

Himmelberg, C.P., R.G. Hubbard. and D. Palia (1999) “Understanding the determinants of managerial ownership and the link between ownership and performance” Journal of Financial Economics 53, pp.

353-384

Kawaguchi, A. and K. Nishitani (2011) “Corporate Governance to Jyosei no Katsuyaku.” [Corporate Governance and Women’s Success at Work], JCER Economic Journal, Vol. 65, pp. 65-93

Kimura, F. and K. Kiyota (2007) “Foreign-owned versus Domestically-owned Firms: Economic Performance in Japan,” Review of Development Economics 11 (1), pp. 31-48

Morikawa, M. (2010) “Labor Unions and Productivity: An Empirical Analysis Using Japanese Firm-Level Data,” Labour Economics, Vol. 17 No. 6, pp. 1030-1037

Morikawa, M. (2013) “Productivity and Survival of Family Firms in Japan,” Journal of Economics and Business, Vol.70, pp. 111-125

Nitta, M. and T. Shinozaki (2008) “Roudou Kumiai no Chingin Kouka.”[Union Wage Effect.], in Tanioka, I., Nitta, M., and Iwai, N. (Eds.), Nihon Jin no Ishiki to Koudou [The Mind and Behavior of Japanese People], Tokyo: Keiso-syobo, pp. 71-84

Noda, T. (1997) “Chingin Kouzou To Kigyounai Roudou Kumiai.” [Wage Structure and Enterprise Unions.

], JCER Economic Journal, Vol. 35, pp. 26-44

Noda, T. (2013) “Determinants of the Timing of Downsizing among Large Japanese Firms: Long-Term Employment Practices and Corporate Governance,” Japanese Economic Review, 64 (3), pp. 363-398

Tachibanaki, T. and T. Noda (2000) “The Economic Effects of Trade Unions in Japan”, Palgrave Macmillan Press

Tsuru, T. and J.B. Rebitzer (1995) “The Limits of Enterprise Unionism: Prospects for Continuing Union Decline in Japan,” British Journal of Industrial Relations, 33 (3), pp. 459-492

![Table 3 Results with OLS, Fixed-effects and Random-effects (without interaction terms) [1] OLS [2]FE [3]RE [4] OLS [5] FE [6]RE UNION 0.107** [0.0258] 0.0601* [0.0262] 0.0845**[0.0194] 0.110** [0.0257] 0.0673* [0.0265] 0.104** [0.0198] FOREIGN 0.175+ [0](https://thumb-ap.123doks.com/thumbv2/123deta/6363223.2130342/8.773.136.646.359.967/table-results-fixed-effects-random-effects-interaction-foreign.webp)

![Table 6 Results with IV (with interaction terms) [1] 2SLS [2] 2SLS [3] 2SLS [4] 2SLS [5] FE2SLS [6] FE2SLS [7] FE2SLS [8] FE2SLS UNION 0.516** [0.141] 0.393* [0.171] 0.399**[0.115] 0.147 [0.176] 0.208* [0.104] 0.212* [0.105] 0.208* [0.104] 0.195 [0.120]](https://thumb-ap.123doks.com/thumbv2/123deta/6363223.2130342/12.773.115.659.184.744/table-results-interaction-terms-sls-sls-sls-union.webp)