第 54 卷 第 5 期

2019 年 10 月

JOURNAL OF SOUTHWEST JIAOTONG UNIVERSITY

Vol. 54 No. 5 Oct. 2019 ISSN -0258-2724 DOI:10.35741/issn.0258-2724.54.5.36 Research Article

Accounting Information System

T

HEE

FFECT OFA

CCOUNTINGI

NFORMATIONS

YSTEMS(AIS)

ONE

NTERPRISER

ESOURCEP

LANNING(ERP)

会计信息系统(航空情报服务)对企业资源计划(企业资源计

划)的影响

Hisham Noori Hussain Al-Hashimy *, Aliaa Saad Al Jubair, Eman Talib Jasim

Computer Information System Department, University of Basrah Al-Ashar–Corniche St., Basrah, Iraq, [email protected]

Abstract

The purpose of this study is to know the impact of accounting and administrative information systems on the performance of institutions. It also aims at finding the relationship between the variables of the accounting information system and the performance variables of the institutions. The study data were collected from 60 employees and faculty members within the College of Computer Science and Information Technology at the University of Basra in Iraq. The project management process was carried out through the PMP program and analysis of the project was conducted through the SPSS program. The study showed the importance of management and planning followed by constraints on efficiency and procedures related to the performance of institutions. The study achieved its objectives and determined the relationship between variables. The use of accounting and management information systems is very important within the organization in the context of technological development in the world.

Keywords:Accounting Information System, Enterprise Resource Planning, MS Project, SPSS

摘要 这项研究的目的是了解会计和行政信息系统对机构绩效的影响。 它还旨在寻找会计信息系 统变量与机构绩效变量之间的关系。 研究数据来自伊拉克巴士拉大学计算机科学与信息技术学院 的 60 名员工和教职员工。 项目管理过程是通过 PMP 程序进行的,而项目分析是通过 SPSS 程序进 行的。 研究表明管理和计划的重要性,其次是效率和与机构绩效有关的程序受到限制。 该研究 实现了其目标并确定了变量之间的关系。 在全球技术发展的背景下,会计和管理信息系统的使用 在组织内部非常重要。 关键词: 会计信息系统,企业资源计划,女士项目,SPSS

I. I

NTRODUCTIONThis study focuses on the role of Accounting Information Systems (AIS) and Internet of things (IOT) in the successful

implementation of an organization within the ERP System). This study was conducted in the Information Systems Department in Iraq and discussed the impact of the evolution of

accounting and management information systems in the College of Information Systems if project management planning is used. In this study, we examined ERP technology, especially its application across all departments of the Administrative College, using real data collected through a random survey in Basra, Iraq. We distributed questionnaires among 60 respondents from the teaching staff in Computer Science. The data were analyzed using SPSS version 0.23 and MS project [2], [3].

Accounting Information Systems is a new variable in Iraq that has gained research interest [1]. One of the most important aspects of Accounting Information Systems is that it concerns the relation to Enterprise Resource Planning (ERP) [4], [22], [24], [26], [31]. At the end of the study, we identified factors that could affect the use of project management planning: project planning, Business case, control, business operating, System development and operating [5], [6], [30], [32].

II. L

ITERATURER

EVIEWIn this section of the research we will provide the Literature review table of this research to be able to specify the related hypotheses. We also provide definitions for all the variables that have effect on the use of the IOT, AIS and ERP [7].

A. Research Variables 1) Control

Control is the engine for most control engineering applications. Linear control theory is not always the best for bias with high nonlinear systems. Accordingly, the increasing control theories of computing are applicable to complex systems relatively easily [8]. It has been also mentioned elsewhere that control manages, directs and regulates the performance of systems or devices [13]. There are two types of control: logical control, linear control, and another type of control that uses some intelligent systems. Besides, from another perspective, control is one of the managerial functions like planning, organizing, staffing and directing [9].

2) Communication Accounting and Auditing

Communication accounting and auditing is executing an audit, by a person or a firm appointed by a company to act as an auditor a person should be certified by the regulatory authority of accounting and auditing or possess certain specified qualifications [10]. Generally, to act as an external auditor of the company, a person should have a certificate of practice from the regulatory authority. In any case, from another worldwide point of view, it is characterized as an orderly and free assessment of the Organization's books, accounts, legitimate records, archives and vouchers to guarantee that budget reports and non-money related exposures give a genuine and reasonable view. It additionally attempts to guarantee that the books of record are appropriately kept up by consideration as legally necessary. Communication accounting and auditing has also been defined as a measurement, processing, and communication of financial information about economic entities such as businesses and corporations. In fact, auditing has become such a ubiquitous phenomenon in the corporate and the public sector that academics started identifying an "Audit Society" [11]. Another world said that Accounting exchange is the procedure to ensure the objectives of the association in the adequacy and effectiveness of operation, the preparation of reliable financial reports and compliance with laws, regulations and policies. It is an offshore concept and includes everything that controls the risks to the organization [29]. From another scientific perspective, accounting and auditing is the process of summarizing, analyzing and reporting business-related financial transactions and audits of financial statements prepared using the cash basis or some other basis of appropriate accounting for the organization [12].

3) System Development

Framework advancement is a term utilized in frameworks, data frameworks and programming building to depict the arranging, creation, testing and sending of a data framework. The idea of frameworks improvement applies to a scope of equipment and programming setups. A framework can comprise equipment just, programming just,

or a mix of both. Be that as it may, from another worldwide viewpoint, it is characterized as the way toward imagining, distinguishing, planning, programming, reporting, testing, and fixing mistakes including the creation and support of uses, structures or other framework segments, or a different universe characterized as framework improvement and procedure, a procedure including new research, advancement or Prototypes. Alteration, reuse, reengineering, upkeep or different exercises prompting the results of the framework, which may incorporate the inner improvement of custom systems [13]. Fulton, Mayo et al. [21] said that system development process includes a set of procedures and methods for the system development identified and implemented in all relevant projects and systems. The framework advancement intends to detail the methodology and techniques used to oversee and control crafted by the framework improvement group. The approach may incorporate explicit expectations that are made and finished by a task group to create or keep up an application [14].

4) Management Decision Making

The executive's basic leadership can be viewed as a critical thinking movement yielding an answer considered to be ideal, or if nothing else good [15]. It is subsequently a procedure which can be pretty much discerning or nonsensical and can be founded on unequivocal or inferred learning and convictions [16]. It is subsequently a procedure which can be pretty much discerning or nonsensical and can be founded on unequivocal or inferred learning and convictions. But from another scientist perspective it is defined as an "emerging important discipline, due to an increasing need to automate high-volume decisions across the enterprise and to impart precision, consistency, and agility in the decision-making process". Decision management is implemented "via the use of rule-based systems and analytic models for enabling high-volume, automated decision making", another scientist defined as a business process (with a decision being the result of that process) that allocates goods and values

in a system (such as one's own time and assets, family or organizational wherewithal, or community and national resources) [19]. In a business context, the system is the business organization as the decision unit, with the manager or executive the decision maker [19]. Wiesner-Hanks [28] said that management decision making is process that directly translate the explosion of much data into improved and effective decision and it is an integral part of modern management Rational or sound decision making is taken as primary function of management and management decision making Is Process that include several level first is to define the problem then diagnose its causes next design possible solution and finally decide which is best, and of course implement the choice [17].

5) Business Operating

Business operating refers to a standard, enterprise-wide collection of business processes used in many diversified industrial companies. The definition has also been extended to include the common structure, principles and practices necessary to drive the organization. Fultz, Billinge et al. [21] defined how organizations are approaching business process management, direction setting and managerial processes and applicability of techniques and concepts from operations management, and the fundamental enabler rule in creating and maintaining a flexible business network, using framework that breaks IT-enabled business into several level. Fylan, Marques et al. [23] said the business operations holds promise as a unifying unit of analysis that can facilitate theory development in entrepreneurship [18]. It is concerned with converting materials and labor into goods and services as efficiently as possible to maximize the profit of an organization, and from another scientist perspective business Operations is the task of managing the activities of BUSINESS or the transformation and interaction of organizational “static substance knowledge” and “dynamic process knowledge” for “products, services, and practical process innovation” and, at the same time, “creating new or justifying existing organizational systematic knowledge [19].

Communication is the activity of conveying information through the exchange of thoughts, messages, or information as by speech, visuals, signals, writing, or behavior. Schaffer and Reithinger [19] defined as the act of conveying meanings from one entity or group to another through the use of mutually understood signs symbols, and semiotic rules. Weinert and Artelt [27] characterized as the way toward trading data and thoughts, both verbal and non-verbal, inside an association. An association may comprise of representatives from various pieces of the general public. These may have various societies and foundations, and can be utilized to various standards. Furthermore, is a deliberate movement of trading data and importance crosswise over reality utilizing different specialized or common methods whichever is accessible or liked. Correspondence requires a sender, a message, a medium and beneficiary, in spite of the fact that the recipient does not need to be available or mindful of the sender's aim to convey at the hour of correspondence [25]. Correspondence is includes composed, oral, visual and advanced correspondence inside a working environment setting, mixes together, innovation, programming and learning hypothesis convey correspondence in an assortment of settings going from specialized composition to ease of use and computerized media configuration to all the more successfully impart in the business world [20].

B. The Questionnaire

The literature review table shows the Questionnaire Parts dependent variables as given in Table 1.

Table 1.

Questionnaire parts

Sections Constructs Number of items

Section A Background 5 information Section B Accounting information systems 4

Section C Internet of things 2

Section E Enterprise

resource planning 2

III. D

ATA ANDA

NALYSISThis sections presents the findings of this study. Descriptive analysis is employed to generate the descriptive information of the respondents such as their gender, age, educational level, and year of experience and some other questions. Further, the descriptive analysis is employed as well to find the descriptive information on the variables. Furthermore, the chapter presents the reliability test and measures the internal consistency between the items. Finally, the chapter presents correlation analysis as well as the result of hypotheses testing using regression analysis.

A. Descriptive Information of the Respondents

This section shows the demographic information about the respondents. Figures are used to illustrate this information. The data include age, gender, education level, specialization, years of experience and other questions related to variables and their components.

1) Gender of Respondents

Figure 1 and Table 2 show the gender of the respondents. Table 2 shows that a total of 33 (50%) of the respondents are males and 27 (40.9%) are females. The gender of the respondents is graphically presented in Figure 1. It can be seen that the proportion of males is higher than that of females. The high percentage of males can be due to the fact that the numbers of male among faculty members are higher than those of females.

Figure 1. Gender of respondents Table 2.

Gender of respondents

Gender Label Frequency Percent

Valid Male 33 50.0

Female 27 40.9

Total 60 100.0

2) Age of Respondents

Figure 2 and Table 3 depict the information about the age of the respondents. Table 3 shows that 13 (19.7%) are in the age group less than 30 followed by 15 (22.7%) in the age group of 30 and 40 years old,

followed by 18 (27.3%) in the age group of 40 and less than 50 years, then followed by 10 (15.2%) in the age group of 50 and less than 60 years. A minority of 4 (6.1%) of the respondents are less than 30 years old.

Figure 2. Age of respondents Table 3.

Age of respondents

Age Frequency Percent

Valid Less than 30 13 19.7

30 and less than 40 years 15 22.7

50 and less than 60 years 10 15.2

60 years and mores 4 6.1

Total 60 100.0

3) Educational Level

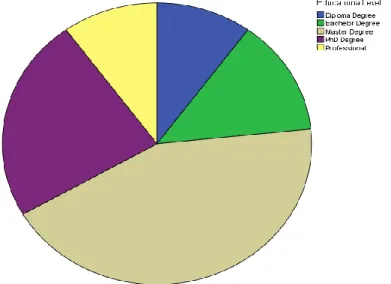

Educational level of the respondents is presented in Figure 3 and Table 4. Table 4 shows that 6 (9.1%) of the respondents have Bachelor degree followed by 6 (9.1%) with Master degree, followed by 8 (12.1%) with Diploma Degree, which followed by 26

(39.4%) with PhD Degree, and followed by 14 (21.2%), who are Professionals. The grades of the teaching staff of the college are overlooked, but the highest ratio of Professionals (21.2%) is dominant.

Figure 3. Educational level of respondents Table 4.

Educational level of respondents

Education Frequency Percent

Valid Bachelor Degree 6 9.1

Master Degree 6 9.1 Diploma Degree 8 12.1 PhD Degree 26 39.4 Professional 14 21.2 Total 6 9.1 4) Experience

Experience of the respondents is presented in Table 5. It shows that 6 (9.1%) of the respondents have less than 5 years of experiences and 9 (13.6%) of the respondents have experience between 5 and 10 years followed by 12 (18.2%) of the respondents have experience of more than 10 years and less than 15 years. A total of 15 (22.7%) of the respondents have experience between 15 and less than 20 years followed by 14 (21.2%) of the respondents have experience of 20 years and more.

Table 5.

Experience of the respondents

Experience Frequency Percent

Valid Less than 5 years 6 9.1

5 and less than 10

years 9 13.6

10 and less than

15 years 12 18.2

15 and less than

20 years 15 22.7

20 years and

more 14 21.2

Total 10 15.2

5) Specialists

Specialists among the respondents are presented in Figure 4 and Table 6. The table shows that 12 (18.2.8%) of the respondents are in Database followed by 8 (12.1%) are in Programming and 4 (6.1%) in Analysis and Web Developing and network, followed by 3 (4.5%) of teaching staff in Computer Science

and Interfacing and Information System and total of 7 (10.0%) in Security and finally 1 (1.5%) in Photoshop.

Figure 4 shows the Specialists among the respondents. As shown in the diagram, we

note that the College of Computer Science and Information Technology contain many specialties taught by a numerous teaching staff.

Figure 4. Specialists Table 6.

Specialists

Specialist Frequency Percent

Valid Database 12 18.2 Analysis 4 6.1 Computer science 3 4.5 Web developer 4 6.1 Network 4 6.1 Interfacing 3 4.5 Information system 3 4.5 Database storage 4 6.1 Programming 8 12.1 Photoshop 1 1.5 Security 7 10.6 Total 60 100.0

B. Descriptive Information of the Variables The average mean value of the study variables is presented in Table 7. This is to show the relationship between the variable and its component whether it is direct or opposite or there is no relationship between them.

Table 7.

The average mean value of the study variables

Question Mean score Relationship P2-Q1 2.57 No relationship P2-Q2 2.50 No relationship P2-Q3 1.0 Positive relationship P2-Q4 2.57 No relationship P3-Q1 1.0 Positive relationship P3-Q2 1.0 Positive relationship P4-Q1 2.57 No relationship P4-Q2 2.30 No relationship

IV. C

ONCLUSION ANDF

UTUREW

ORK In the questionnaire methodology we followed Systems (AIS) and Internet of things (IOT) in the Successful Implementation of Organization of the ERP System. We distributed the survey including questions about this research among 60respondents from the teaching staff in Computer Science and Information Technology college. As a result, the data obtained during the study enable us to work on the reasons for the lack of using ERP system at a computer science and information technology college.

R

EFERENCES[1] AL-DMOUR, A.H. and AL-DMOUR, R.H. (2018) Applying Multiple Linear Regression and Neural Network to Predict Business Performance Using the Reliability of Accounting Information System.

International Journal of Corporate Finance and Accounting, 5(2), pp. 12-26.

[2] AL-HASHIMY, H. (2017) Factor Influencing Salaries and Wage Order: Empirical Study at Basra University. IOSR

Journal of Business and Management, 19(1),

pp. 30-36.

[3] AL-HASHIMY, H.N.H., HAMOUD, A.K., and HUSSAIN, F.A. (2019) The Effect of Not Using Internet of Things in Critical life Situations in the Health Field and the Effect on Iraqi Profitability: Empirical Study in Basra. Journal of Southwest Jiaotong

University, 54(4).

[4] AL-HILA, A.A., ALHELOU, E.M.S., AL SHOBAKI, M.J., and NASER, S.S.A. (2017) The Impact of Applying the Dimensions of IT Governance in Improving E-Training - Case Study of the Ministry of Telecommunications and Information Technology in Gaza Governorates.

International Journal of Engineering and Information Systems, 1(8), pp. 194-219.

[5] ALAVOSIUS, M.P., HOUMANFAR, R.A., ANBRO, S.J., BURLEIGH, K., and HEBEIN, C. (2017) Leadership and Crew Resource Management in High-Reliability Organizations: A Competency Framework for Measuring Behaviors. Journal of Organizational Behavior Management, 37,

pp. 142-170.

[6] HILKEVICS, S. and SEMAKINA, V. (2019) The classification and comparison of business ratios analysis methods. Insights

into Regional Development, 1(1), pp. 48-57.

[7] ANSARI, F., SCHENKELBERG, K., SEIDENBERG, U., and FATHI, M. (2017)

Problem Solving in the Digital World: Synoptic Formalism, Incrementalism and Heuristics. In: LAPLANTE, P. (ed.)

Encyclopedia of Computer Science and Technology. Boca Raton, Florida: CRC

Press, pp. 1-9.

[8] ARUMUGAM, V., HUSSEIN, H.N., and NAJMULDEEN, C. (2015) A Review and Model Development of the Factors that Affect Mobile Marketing Acceptance by Customers. International Journal of Science

and Research, 4(10), pp. 1475-1478.

[9] CHUA, M.E., SEE, M.C., ESMEŇA, E.B., BALINGIT, J.C., and MORALES, M.L. (2018) Efficacy and safety of gabapentin in comparison to solifenacin succinate in adult overactive bladder treatment. Lower Urinary Tract Symptoms, 10(2), pp. 135-142.

[10] COVIN, J.G. and SLEVIN, D.P. (1991) A conceptual model of entrepreneurship as firm behavior. Entrepreneurship Theory and

Practice, 16(1), pp. 7-26.

[11] FUI-HOON NAH, F., LEE‐ SHANG LAU, J., and KUANG, J. (2001) Critical factors for successful implementation of enterprise systems. Business Process Management Journal, 7(3), pp. 285-296.

[12] HAYES, A.F. (2017) Introduction to

Mediation, Moderation, and Conditional

Process Analysis: A Regression-Based

Approach. New York: Guilford Publications.

[13] HUSSAIN, H. (2017) Introduction to

Management Skills Must Be Available to Accountants in Iraq. International Institute

for Science, Technology and Education. [15] HUSSEIN, H., KASIM, N., and ARUMUGAM, V. (2015) A review of creative accounting practices and its area, technique and ways of prevention.

International Journal of Science and

Research, 4(10), pp. 1377-1381.

[16] IBRAHIM, S.K. and JEBUR, Z.T. (2019) Impact of Information Communication Technology on Business Firms. International Journal of Science and

Engineering Applications, 8(2), pp. 53-56.

[17] LEWIS, W.E. (2017) Software Testing

and Continuous Quality Improvement. Boca

[18] LOVEJOY, A. (2017) The Great Chain

of Being: A Study of the History of an Idea.

Abingdon: Routledge.

[19] QUINTANILLA, K.M. and WAHL, S.T. (2018) Business and Professional

Communication: Keys for Workplace

Excellence. Thousand Oaks, California: Sage

Publications.

[20] SCHROEDER, R.G., CLARK, M.W., and CATHEY, J.M. (2019) Financial

Accounting Theory and Analysis: Text and Cases. Hoboken, New Jersey: John Wiley &

Sons.

[21] FULTON, J.S., MAYO, A., WALKER, J., and URDEN, L.D. (2019) Description of work processes used by clinical nurse specialists to improve patient outcomes. Nursing Outlook, 67(5), pp. 511-522.

[22] PRODANI, R., BUSHATI, J., and ANDERSONS, A. (2019) An assessment of impact of information and communication technology in enterprızes of Korça region. Insights into Regional Development, 1(4), pp. 333-342.

[23] FYLAN, B., MARQUES, I., ISMAIL, H., BREEN, L., GARDNER, P., ARMITAGE, G., and BLENKINSOPP, A. (2019) Gaps, traps, bridges and props: a mixed-methods study of resilience in the medicines management system for patients with heart failure at hospital discharge. BMJ Open, 9(2), e023440.

[24] SUBAČIENĖ, R., ALVER, L., BRŪNA, I., HLADIKA, M., MOKOŠOVÁ, D., and MOLÍN, J. (2018) Evaluation of accounting regulation evolution in selected countries. Entrepreneurship and Sustainability Issues, 6(1), pp. 139-175. [25] NAJEMY, J.M. (2019) Between Friends: Discourses of Power and Desire in the Machiavelli-Vettori Letters of 1513-1515. Princeton, New Jersey: Princeton University Press.

[26] VEGERA, S., MALEI, A., SAPEHA, I., and SUSHKO, V. (2018) Information support of the circular economy: the objects of accounting at recycling technological cycle stages of industrial waste. Entrepreneurship and Sustainability Issues, 6(1), pp. 190-210.

[27] WEINERT, S. and ARTELT, C. (2019) Measurement of skills and achievement: a

critical assessment of theoretical and methodological concepts. In: BECKER, R. (ed.) Research Handbook on the Sociology of Education. Cheltenham: Edward Elgar Publishing, pp. 106-132.

[28] WIESNER-HANKS, M.E. (2019) Women and Gender in Early Modern Europe. Cambridge: Cambridge University Press. [29] BALYNSKAYA, N.R. and KOPTYAKOVA, S.V. (2015) Specifics of Information Risks in the Municipal Administration System of Modern Russia.

Journal of Advanced Research in Law and Economics, 6(2(12)), pp. 284-290.

[30] AKHMETSHIN, E.M., VASILEV, V.L., MIRONOV, D.S., ZATSARINNAYA, Е.I., ROMANOVA, M.V., and YUMASHEV, A.V. (2018) Internal control system in enterprise management: Analysis and interaction matrices. European Research

Studies Journal, 21(2), pp. 728-740.

[31] STRICHKO, E. (2013) Costs of Accounting Information Support. Journal of

Contemporary Economics Issues, 4.

Available from

https://doi.org/10.24194/41313.

[32] CHERKAS, V. (2013) The Theoretical Aspects of Management Reporting. Journal

of Contemporary Economics Issues, 1.

Available from https://doi.org/10.24194/11323.

参考文:

[1] AL-DMOUR,A.H. 和 AL-DMOUR, R.H.(2018)应用多元线性回归和神经网 络通过会计信息系统的可靠性预测业务绩 效。国际公司财务与会计杂志,5(2), 第 12-26 页。 [2] AL-HASHIMY,H.(2017)影响工资 和工资秩序的因素:巴士拉大学的实证研 究。 IOSR 商业与管理杂志,19(1),第 30-36 页。 [3] AL-HASHIMY,H.N.H.,HAMOUD, A.K. 和 HUSSAIN,F.A.(2019)在卫生 领域关键生活状况中不使用物联网的影响 及其对伊拉克获利能力的影响:巴士拉的 实证研究。西南交通大学学报,54(4) 。[4] A.AL. AL-HILA, E.M.S。ALHELOU ,M.J。AL SHOBAKI 和 S.S.A. NASER。

(2017)在改进电子培训中应用技术情报治 理维度的影响-加沙省电信和信息技术部 的案例研究。国际工程与信息系统杂志, 1(8),第 194-219 页。 [5] ALAVOSIUS , M.P. , HOUMANFAR ,R.A.,ANBRO,S.J.,BURLEIGH,K. 和 HEBEIN,C.(2017)高可靠性组织中 的领导力和船员资源管理:衡量行为的能 力框架。组织行为管理杂志,37,第 142-170 页。 [6] HILKEVICS,S. 和 SEMAKINA,V.( 2019)业务比率分析方法的分类和比较。 《洞察区域发展》,1(1),第 48-57 页 。 [7] ANSARI,F.,SCHENKELBERG,K. ,SEIDENBERG,U。和 FATHI,M。( 2017 年),《数字世界中的问题解决:对 映形式主义,增量主义和启发式》。在: LAPLANTE,P.(编辑)《计算机科学与 技术百科全书》中。佛罗里达州博卡拉顿 :CRC 出版社,第 1-9 页。 [8] ARUMUGAM,V.,HUSSEIN,H.N. 和 NAJMULDEEN,C.(2015)对影响移 动营销接受度的因素的回顾和模型开发。 国际科学与研究杂志,4(10),第 1475-1478 页。

[9] M.E. CHUA , M.C 。 SEE , ESMEEEA.E.B 。 , J.C 。 BALINGIT 和 M.L. MORALES。 (2018)在成人膀胱过 度活动症治疗中,加巴喷丁与琥珀酸索非 那新的疗效和安全性比较。下尿路症状, 10(2),第 135-142 页。 [10] COVIN,J.G。和 SLEVIN,D.P. ( 1991)作为企业行为的企业家精神的概念 模型。创业理论与实践,16(1),第 7-26 页。 [11] FUI-HOON NAH,F.,LEU-SHANG LAU,J. 和 KUANG,J.(2001)成功实 施企业系统的关键因素。 《业务流程管理 杂志》,7(3),第 285-296 页。 [12] HAYES,A.F.(2017)中介,调节和 条件过程分析导论:基于回归的方法。纽 约:吉尔福德出版社。 [13] HUSSAIN,H.(2017)伊拉克会计师 必须掌握管理技能简介。国际科学,技术 和教育学院。 [15] HUSSEIN , H. , KASIM , N. 和 ARUMUGAM,V.(2015)对创新会计实 践及其领域,技术和预防方法的评论。国 际科学与研究杂志,4(10),第 1377-1381 页。 [16] IBRAHIM,S.K。以及 JEBUR,Z.T. (2019)信息通信技术对商业公司的影响 。国际科学与工程应用杂志,8(2),第 53-56 页。 [17] 刘易斯(W.E.) (2017)软件测试和 持续质量改进。佛罗里达州博卡拉顿:奥 尔巴赫出版社。 [18] LOVEJOY,A.(2017)生命的大链 :思想史研究。阿宾登:劳特利奇。 [19] 昆塔尼拉(KIN)和 S.T. WAHL ( 2018)商业和专业沟通:卓越工作场所的 关键。加利福尼亚州千橡市:智者出版物 。 [20] SCHROEDER,R.G.,CLARK,M.W 。和 CATHEY,J.M。(2019 年),《财 务会计理论与分析:文本与案例》。新泽 西州霍博肯:约翰·威利父子公司。 [21] J.S. FULTON , A 。 MAYO , J 。 WALKER 和 L.D. URDEN。(2019)说明 临床护士专家用来改善患者预后的工作流 程。 《护理展望》,67(5),第 511-522 页。 [22] PRODANI , R. , BUSHATI , J 。 和 ANDERSONS,A。(2019 年),对信息 和通信技术对科尔萨地区企业的影响的评 估。 《洞察区域发展》,1(4),第 333-342 页。 [23] B.FYLAN,MARQUES,I.SMAIL, H. , BREEN , L. , GARDNER , P. , ARMITAGE,G。和 BLENKINSOPP,A 。(2019 年),缺口,陷阱,桥梁和道具 :出院时心力衰竭患者药物管理系统中复 原力的混合方法研究。英国医学杂志公开 赛,9(2),e023440。 [24] SUBAČIENĖ , R. , ALVER , L. , BRŪNA , I. , HLADIKA , M. , MOKOŠOVÁ,D. 和 MOLÍN,J.(2018)

对选定国家会计准则演变的评估。创业与 可持续性问题》,6(1),第 139-175 页 。 [25] NAJEMY,J.M.(2019)《朋友之间 :权力与欲望的话语》,刊登于 1513 年 至 1515 年的马基雅维利-维托里书信中。 新泽西州普林斯顿:普林斯顿大学出版社 。 [26] VEGERA , S. , MALEI , A. , SAPEHA,I. 和 SUSHKO,V.(2018)循 环经济的信息支持:工业废物循环技术循 环阶段的核算对象。 《创业与可持续性问 题》,6(1),第 190-210 页。 [27] WEINERT , S. 和 ARTELT , C. ( 2019)技能和成就的衡量:对理论和方法 论概念的批判性评估。在:BECKER,R 。(编辑)《教育社会学研究手册》中。 切尔滕纳姆:爱德华·埃尔加出版社,第 106-132 页。 [28] WIESNER-HANKS , 硕士 (2019 年 ),《近代早期欧洲的妇女与性别》。剑 桥:剑桥大学出版社。 [29] BALYNSKAYA , N.R 。 和 KOPTYAKOVA,S.V. (2015)现代俄罗 斯市政管理系统中的信息风险细节。法律 与经济高级研究杂志,6(2(12)),第 284-290 页。 [30] 阿克梅特欣( E.M. ), 瓦西里夫 ( VASILEV),弗洛里(V.L.),米罗诺夫 ( D.S. ) , 扎 特 萨 那 那 亚 ( ZATSARINNAYA), 埃米 尔 ( I. ), 罗 曼诺夫(ROMANOVA)和马萨诸塞州尤 马谢夫(YUMASHEV)。 (2018)企业 管理中的内部控制系统:分析和交互矩阵 。欧洲研究杂志, 21(2),第 728-740 页。 [31] STRICHKO,E。(2013)会计信息 支持成本。当代经济学问题杂志,4。可 从 https://doi.org/10.24194/41313 获得。 [32] CHERKAS,V.(2013)管理报告的 理论方面。当代经济学问题杂志,1。可 从 https://doi.org/10.24194/11323 获得。