NII-Electronic Library Service

Performance Measurement

in the French Public Services :

New Public Management

and Republican Centralism

Nathalie Halgand*

Abstract

The article analyses the structural and technical aspects of Performance Measurement as partofNew PublicManagement intheFrench context, atbothcentral and localIevels.[[Ehecentralist influenceisanalysed through concrete featuresof the

system. Some biasesare highlightedinthecontrol structure. The accounbing system is

describedas focusedon limitedpoliticalpur[posesbothebenefitoftheExecutive,and the

recent organisational decentralisationrevival incentral state publicsewtces provesto beduetoa strong toppoliticalsupport. An in-depthview of theimpedimentstoperfor-

mance measurement developmenbstihenshows tihatcentralism isdeeplyrooted incul- tJuralTepublican values, which shape tihefoundabionsof both thepublicservice system

and thepoliticalone, theformerbeinginfluencedbythelatter,thnugh tiheconcentra-

tionofmanagerial and politiealpowers inthehandsof a smal1 eliteclan.Fina]ly,some emerging reflections are reported, which proposeguidelinestoreform thewhole system.

Key Words

Perfbrmance Measurement, New PublicManagement, PublicAccounting, Public

Control

SubmittedJuly1996.

Accepted March1997.

* SeniorLecturerinManagement Seience(Accounting),CREGO (CentredeRecherehe en Gestiondes Organisations ;Research Centre forManagement), University ofMontpellier II,Place E.Bataillon, 34095 Montpelliercedex 5,FRANCE -fax:+33-4-67 144242-E-mail:halgand@iae,univ-montp2.fr

29

NII-Electronic Mbrary

Performanee Measurement inthe French PublieServices

1. Introduction

The New PublicManagement (NPM) has been characterized by Hood [8]by first,a

reduced diffbrencebetween the publicand the private sectors, and second a greater

emphasis placed on result oriented management. Performance measurement ishence

a central concept inthiscontext, and accounting isheldas a key element ofNPM.

This article aims at firstdescribing and analyzing the performance measurement system Ge.structures and techniques)of the French publicservice and second exam- iningthe impediments towards thisprocess development,ina context which isstrong-

lyinfluenced by republican centralism. Afteran overview of the French context and

the politico-administrativeframework (2.),the structures ofthe performance measure-

ment system (3.)and techniques (4.)are examined. The accountability patterns and

the cultural values are then analyzed as obstacles toperformance measurement devel-

opments (5.),and a means ofrestructuring thepublicservice ispresented (6.).

2.Context and Politieo-administrative.Structures :

The institutionalcontext isstrongly infiuencedby a tradition of written law.

According to Hofstede'smodel [7],the French cultural values include a small power distance,which ishighlighted by the people'sattachment tothe republican value of

equality, and results ina highdegreeofuniformity interms of accounting system fea- tures (Gray& Radebaugh [6]).Centralism and secrecy are also prevalent features of the politico-administrativesystem. The republican central state isentrusted with

safeguarding the general interestand the publicservices are considered as the opera-

tionalmeans of shaping action on French society, includingbothsocial and economic aspects.

2.1 PoliticalStructuresandtheRoleofCentralState

The politicalstructure issemicentralized, with a powerfu1 center and a three level periphery,which has become independent since the early eighties, through the decen-

tralization laws.The three localauthorities includethe municipalities' (about36,OOO),

the departments(i.e.general councils) and the regions (i.e.regional eouncils). They

are responsible forspecific publicservice missions, which have been transferredfrom the central level,and which bordertheircompetence scope. Hence,thereisno hierar-

chieal relationship betweenthe threeterritorialauthority types.

At bothlevels(i.e.Iocaland central), the power pattern isstrongly rooted incentral-

ism tothe benefitof the executive body. At the central level,the fifthrepublic consti-

m u/1 heoppositionrights,andhasaimedatprovidingthe

1 `municipality' isusedinthepapertotranslatetheFrenchword `commune' .

NII-Electronic Library Service executive with politicalstability. The weakness ofthe Parliament stems from the elec-

toral systern, which was originally designed in order to guarantee the government a legislativesupport through an over-represented majority. On another hand,some pro-

cedures (e.g.the decree)enable the Executive tomake decisionswithout requiring the

support of the two chambers (i.e.the Parliamentand the Senate).On financialmat-

ters,the control of Parliament iswidely denounced and similarly ineffbctive(Muzellec [14]).At the locallevel,inorder toresist against the centralist pressures,the decen- tralizationlaws have entrusted the territorialauthority executives with huge powers, placed in the hands of a notable class, at the expense of the opposition rights. As a result, the power pattern isstrongly personalized,as though the government model had been imitated at the locallevel,with a similar reluctance towards transparency (M6ny [11]).

2.2Overview of the ]FV,ench PecbticServiee System

PoliticalAuthoritiesExainples of

Public ServiceMissions

- rail transport

-defense,justice -electricityf energy

Examples of

Management Patterns

-public body -directsupervision

-mixed third body (nationalpublicfirrm)

-secondary school building

and ruming (from15to18) -regional archives

-directsupervision

-directsupervision

-secondary school building

and running (from11to15) -pupil transport

-direetsupervision

-publiof privatel third body

-primaryschools {from3 te 11) -waterdistibution

-planningpermissions

-direct supervision

-publiofprivatel thirdbody -directsupervision

Figure 1.Description of the French politico-administrative system

Every state authority, which iselected by the people and hence represents the will of the people (i.e.the nation), either at the central or locallevel,isentrusted with a

specific range of publicservice missions. For many of them, itisempowered to choose

theirmanagement pattern.Itcan run them directly,in which case itconcentrates

both politicaland managerial powers. An alternative solution would involvedelegat- ingthe management to a thirdparty,which can beeither public (e.g.a publicestab-

31

Performance Measurernent intheFrench PublicServices

lishment likea university), private or mixed (i.e.a firm with mixed privatefpublic

shares). The deeentralizationIaws have widened the Iocalauthority scope, inducing

the rise of the delegatedmanagement model tothe benefitof the privatesector, espe-

cially at the municipal level.

3. Stntctures ofthe Performance Measurement System

The structures of the system do not prevent centralist pressures,which induce bias-

es inthe control and controller capture situations.

3.1.Ilheinternal Control Structure

The basicprinciple in public accounting (introducedin 1822) consists of sharing the

managerial power between two persons :the firstone isthe decisionmaker (e.g.the

minister, at the central level,or the elected chiefexecutive ofthe territorialauthority, at the locallevel>,the second one isa publicaccountant (i.e.a civil servant), who exe-

cutes the order (Labie[9]).This dissociationintothe administrative and accounting

phases stems from the need to contrel frauds (Muzellec[14]).Hence, the public

accountant, playing the role of a cashier, isincharge of the day-to-daycontrol of the

regularity of the order (i.e.procedure control) that isgiventohim, and isresponsible on his personal funds(i.e.he has to reimburse a payment that he has donewithout havingcontrolled itslegality)forthe payment operations thathe executes.

The public accountant is hierarchically depending upon the `General Payer Treasurer',at the departmental level,and can be controlled by the `Finance General Inspection',which isthe internalauditing body of the Ministerof Finance.On the

other side, the order giver(e.g.a Secretary)iscontrolled and advised by a financial

controller, nominated bythe Ministerof Finance.

The case of public national firms(e.g.SNCF forrailways) isspecific. They are man-

aged along the privatesector rules, butare controlled by the central state through the tutelagesystem. The technicaltutelageisunder the responsibility of the relevant min-

ister,while the financialone isin charge of one state controller.

3.2.The StateAccountAaditing

Public service auditing distinguishesbetween two situations. When the public ser-

vice mission isunder the central state scope, the auditing bodyisthe AccountCourt.

Symmetrically,the AccountRegionalChambers are incharge of the auditing task,at the locallevel.This apparatus guarantees that the entire publicseetor, includingthe publicfirms,isexternally controlled by an independent body. The structure and mis- sions of the localand central sub-systems are basicallysimilar, since the regional

NII-Electronic Library Service chambers havebeencreated in1982,as partofthe decentralizationprocess,by central

-- .

Imltatlon.

At the central level,theAccount Court aims at controlling the account conformity to the Law of Finance, which isthe annual financialexpression of the intended govern-

ment action. An annual auditing program isdefined in order to control each public

service every fburth or fifthyear, on average. The ohject of the auditing process has gone beyond the regularity control of the public fund use (i.e.comparing itwith the Law of Finance), to assess managerial perfbrmance of public units, embracing the

order giversand publicaccountants' actions. But the task divisionbetween regional and central bodieshas shown some limitationswhen faced with globalobject assess-

ment. For example, investigations concerning the decentralizationprocess conse-

quences have required the cooperation of both levels.Moreover, the effbcts of thiscon- trolhave highlighted some weaknesses and meant reducing itto an information tool.

Forexample, theproblems identifiedina minister bythe Courtresult inmailing a let- tertothe concerned secretary, but cannot leadtoany sanction. The Court can audit an

institution(i.e.a public firm) at the government request. It also enlightens the Parliament control through a feed-backcontrol report on the executive action, and

contributes to detecting financial scandals. The weaknesses of the Court control

resources, facedby the huge amount of operations tobe controlled isalso worth noting

(Muzellec[14]).Inany case, the AccountCourtpower islimitedtoa moral judgment

and has no compulsory means ofimposing itsrecommendations.

At the locallevel,the Account RegionalChambers audit the territorialauthorities

(i,e.municipalities, departments and regions) and the institutionsincluded in their

scope. To the account auditing have beenadded some management control recommen- dations.Althoughthe decentralizationlawshavetriedtoprovidethe Chambers with a

comprehensive control power over the public fund utilization, the 1982 text was

refined in 1988 under the pressure of localelected people,and the utilization review was restricted toa `regular use of funds'(Labie[9]).Once again, the Chamber has not been empowered to impose itsmanagement recommendations. Italso stresses that thisinstitutionhas no jurisdictionalpower on the localorder giver,by contrast with

the public accountant. Furthermore, some analysts stress the weakness of an ex-post control which can only state the critical situations, insteadof preventing them. Some

attempts to improve the financialinformation provision have resulted in the 1992 laws,setting first,that the prefectcan request Regional Chamber audit of any finan-

cial commitment of the localauthority, and second, that the prefector the decentral- izedauthority can order an investigationon any private institutionwhich benefits from public funds. Nevertheless mueh remains to do in terms of preventive control

(Mignot[13]).Moreover, the Regional Chambers are not allowed to get access tothe relevant real time information,ifno claim has been referred to them (Froment- Meurice & al. [5]),which tends to demonstratethe need foran external systematic

33

NII-Electronic

Performance Measurement in the French Public Services

audit of the territorialauthorities' accounts (Ohnet[15]).

3.3.Elystemic Level:pragrain andpoliay evaluation

Recognizing thatthe regularity control had priorityover management control (Vidal

inMuzellec[14]),a publicpolicyevaluation system was introducedin 1990,as part of the state modernization process.[IIhepurpose of the reform was toprovide the state action with an efTective performance measurement tool,which took into account the

specificity of the public activities (i.e.global).Because of theirwide scope, the public policiesand the public programs (thelatterbeingused to implement the former)

require a systemic approach. The evaluation system has a two body structure. The Evaluation Inter-ministerial Committee has fbcused on public policiesand the EvaluationScientificCommittee (ESC)has aimed at assessing publicprograms. While

the formerbelongstothe Executive itselfand can hencebeconsidered as partof a self

controlling process,the latterhas been defined as an independent body. The evalua- tion object, displayedas policies,are actually restricted to methodological aspects of public programs. In 1994, an independent audit (TECNED International),ordered by the committee, highlightedthe .procedure biasesresulting inthe progressivetransfor-

mation of the role of the ESC into a projectdesignadviser (ConseilScientifiquede

1'Evaluation[3]).First,the evaluation process ispartialand never systematic, since

the committee only works at the projectauthors' request. Second,the evaluation sys-

tem structure hasbeenput intoquestionby theabsence of any superior authority (e.g.

a high court) regulating controversies between the requester (i.e.the executive) and

the committee, and guaranteeing the independence of the latter.Furthermore,the

committee power islimitedtothe issuingof advisory conclusions. Finally,the opacity of the projectssubmitted by the executive has ledthe consultants toanalyze iteither as purposefu1,the authors keeping some eore detailsforthem, or as a proof of their inabilitytoproperly definea project.

4.Performance Measurement Techniques

The performance measurement techniques are examined in terms of their account-

ing and managerial aspects.

4L1 PublieAccounting at bothCentral and Local Levels

The double entry bookkeeping principle was introduced in 1808 inthe state account-

ing system and has fosteredthe identificationof the publicaccountants' frauds,con- sisting of theirappropriation of some of the tax revenues, that they were incharge of recovering (Berthier[1]).

-Budgetary and FinancialAccounting Systems

NII-Electronic Library Service

The French publicfinance distinguishesbetween two parts :`budgetary accounting' which isspecific tothe publicservices and `financial accounting' ,which isclose tothe privateFrench accounting system. These two parts can either buildseparate systems, which are articulated (i.e.at the central state level),or constitute an integratedsys-

tem (i.e.at the localauthority level).They pursue diffbrentgoalsand are ruled by spe-

cific procedures.The budgetarysystem firstprovides the order giversand the public

accountants with a basisofthe execution of the Budget, which results from theannual

Law of Financevoted bythe Parliament, and second, constitutes the reporting system used to review the public fund utilization. The Law of Financehas a special impor- tance,since ita priorirestricts the publicfund allocation to the government fora

givenyear, and isthe main means in the hands of the Parliament and the Account Court to control the action of the Executive, a posteriori.By contrast, `financial

accounting' isthe usual bookkeeping system, the principlesofwhich evolve towards an accrual basis,although this has not been reached yet.Indeed,the tangible assets

acquired in the year are no longer considered as charges, but the tangible assets

boughtbefbre 1981 are not included in the balance sheet account. Furthermore, the inventoriesare not described,since the constitutional yearly bndgeting principledoes-

n't allow tofbrecastexpenses over the year.Thismeans that the goods boughtduring

the year should be consumed at the end of the same year.No allowance fordoubtfu1

accounts iseither recorded, because itwould imply that the state isnot able toimpose thepayment of taxes on individuals.

Exec

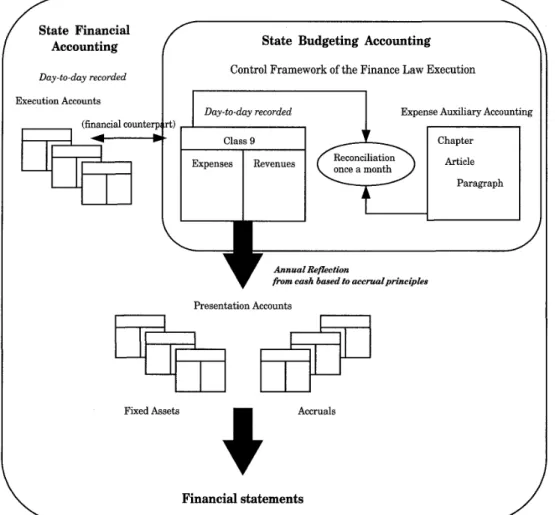

,

Figure 2.The Articulation between Budgeting and 1ffnancial Accounting Systems

35

Performance Measurement inthe French PublicServices

At the central level,the two systems have remained distinct.This can firstbe

explained by the strong emphasis placed upon the budgetary accounting system deal- ingwith democratic stakes, while the other part isassociated with managerial purpos-

es, considered as much lessimportant. Furthermore the changing nature of the bud-

geted expense nomenclature can hardlycope with the stability of the `General Chart of

Accounts' used fbrfinancialaccounting. Finally,the articulation of the two systems is done through data processing,which isnot laborintensive.Then, while `budgetary

accounting' isruled by the simple entry bookkeeping principle,an annual reflection procedure enables itsarticulation with financialaccounting, inorder toproduce annu-

al financialstatements. Thisprocedure also aims at making the budgetaryaccounting outputs, ruled on a cash basis,consistent with the financialaccounting principles.

Duringthe year,the budgetaccount class (i.e.class 9)isused torecord the execution

of the expenses and the revenues, that havebeen fbrmerlyauthorized inthe Law of

Finance,with a financialeounterpart in a cash financial account. An auxiliary expense accounting system isset inparallel,inorder tomatch the highlydetailedcod-

ificationrequired by the Law of Finance. A reconciliation between theexpense part of

class 9 and the auxiliary system isdone every month. Recording an operation in the

class 9 includesthe computing of a code which identifiesthe associated account inthe financialchart, used at the end ofthe year.

The budgetaryexpense nomenclature isdominatedby a resource oriented logic.This

means that the credits are apportioned firstbetween ministers and second by type of

resources (e.g.personnel,traveling expenditures). An alternative solution could be to

allocate publicfunds on a functionalbasis,namely on operational goalsand projeets.

Thisisonly effective forinvestmentflows,theneed forwhich enables a clear identifi-

cation of the expected fundutilization. As a result, the vote of the Law of Finance is done blindly(Berthier[1]),and itsfinancialrgporting system (i.e.budgetaryaccount-

ing)cannot provide a real management accounting tool.

The financialstate chart of account, issued in 1988 has been inspired by the so-

called `General ChartefAccounts'used bythe privatesector since 1982.Nevertheless, the formerhas stillnot reached the fu11accrual basisof the latter:itsevolution stage can be translated intoEnglish by `stated rights accounting (`comptabilit6 de droits

constates' ).For example, a charge that has been incurred by the order giver,but

which has still not entered the accounting phase, isnet recorded. On another hand,

the descriptionof the assets remains uncompleted on several points.First,neither inventoriesnor bad debts are described.The fixedasset accounting has been improved, since the annual investment flow (e.g.buildings)are accounted in a fixed

asset class, while they were considered as a charge until 1988.Nevertheless,the exist-

ingfixedassets, thathaveentered the state patrimony before1981 are not recognized

in the accounts, and hence not depreciated (Berthier[1]).The amortization question,

as forinventory,has suffbred fromthe strong infiuenceof the budgetaryaccounting