Intergenerational Conflict Over Fiscal Consolidation: Theory and Evidence from

Japan

∗Real Arai† Ryosuke Okazawa‡ Katsuya Takii§ Last Revised: February 2, 2018

Abstract

This paper analyzes the determinants of voter preferences on fiscal consolidation policies using an opinion survey of Japanese citizens. We address the following ques- tions: (i) Is there a huge intergenerational conflict of interest surrounding fiscal con- solidation policies? (ii) Can standard political economic theory explain the observed differences in political preferences among generations? Contrary to the prevailing view, we find that older voters aremore likely to support fiscal consolidation policies. We build a simple political economic model and provide several hypotheses that explain the observed fact. We find that financial asset holdings and political knowledge are sig- nificantly related with citizen’s preferences for fiscal consolidation. Moreover, we find that nearly half of intergenerational conflict surrounding consumption tax policy can be explained by the differences in these factors.

∗We are grateful to Nobuo Akai, Yu Awaya, Shunichiro Bessho, Takero Doi, Makoto Hasegawa, Masayuki Kudamatsu, Kazuki Onji, Shinpei Sano, Kimiko Terai, and the participants of the seminar in Osaka Uni- versity, Kochi University of Technology, Tokyo Metropolitan University, GRIPS, Kansai Public Economics workshops. Of course, we alone are responsible for both the content and any errors.

†Department of Management, Kochi University of Technology.

‡Graduate School of Economics, Osaka City University. Email: [email protected]

§Osaka School of International Public Policy (OSIPP), Osaka University.

1 Introduction

Since the outbreak of financial crisis, many developed countries, are suffering from enormous government debt. Figure 1 illustrates the recent amounts of general government liabilities per GDP in selected OECD countries. It shows that many countries have experienced govern- ment liabilities per GDP after financial crisis. Although fiscal consolidation is one of urgent macroeconomic issues for most developed countries, the processes of fiscal consolidation do not seem to continue well in many countries1. Why is fiscal consolidation so difficult?

[Figure 1 here]

The political process is often considered a cause of persistent government deficit. In the classical work, Buchanan and Wagner (1977) argue that fiscal consolidation policies, such as tax increases or cuts in government spending, tend to be postponed in democratic societies because they burden the current electorate although they are beneficial for future genera- tions. Since future generations do not have political influence on current policy decisions, fiscal policy often causes enormous accumulation of government debt.2 Figure 2 shows that the median age of voters consistently increases in advanced countries in periods when gov- ernment debt expansion is observed. The changes in the age distribution of the electorate in recent years suggests that the intergenerational conflict might be one explanation for recent government debt expansion.3

[Figure 2 here]

This paper analyzes the determinants of voter preferences for fiscal consolidation policies using an opinion survey conducted among Japanese citizens. We examine how the age of voters influences the preferences for fiscal consolidation policies. Because, as Figure 1 and 2 show, Japan experiences a rapid increase in the median age of voters as well as that in government debt per GDP, Japan is an ideal country for our research purpose. A popular view on a cause of a huge government debt can be summarized by Ihori (2016): “As the difference in preference by age increases, the current beneficiary tends to hope for an increase in benefit payments but is reluctant to bear their costs, and the reforms tend to be postponed.

As a result, the fiscal burden is imposed on the future beneficiary. If the policy is determined by “silver democracy,” it causes the accumulation of fiscal deficits and an increase in social security benefits.” Using an opinion survey conducted in Japan, this paper examines whether the growing political power of older generations threatens fiscal sustainability.

1Alesina et al. (2015) analyze the features of fiscal consolidation policies and examines their consequence on the economy in the period 2010-2013.

2There is also substantial literature that analyzes the debt management policies of the government from a positive perspective (e.g., Alesina and Passalacqua (2016)). Intergenerational conflict over fiscal policies is often noted in the literature.

3Since aging populations typically place a financial burden on the government through an increase in medical spending or pension benefit payments, the role of intergenerational political conflict is reflected only by the observed co-movement of an aging population and the accumulation of government debt. However, it seems natural that politicians in democratic countries should heed the interests of older voters as the median age of the voters increases.

The first and most important contribution of this paper is to provide robust evidence that the older voter ismorelikely to support fiscal consolidation policies. As Figure 3 shows, the share of those who support a consumption tax hike monotonically increases with age.

A similar pattern is observed in opinions concerning trade-off between fiscal stimulation and consolidation policies. The differences in preferences across generations are statistically significant even if we control for differences in education, income, and family structure.

Moreover, we show that it is difficult to explain the observed differences in policy preference by the altruism of older citizens toward future generations. These findings are contrary to the prevailing view that older voters hinder the implementation of fiscal consolidation policies.

[Figure 3 here]

Our second contribution is to provide several hypotheses that explain the reasons why older voters are likely to support fiscal consolidation policies. We build a simple political economic model where the consumption tax rate and level of government debt are deter- mined by the political process. Our model captures the basic insights of the common view of intergenerational conflict over fiscal consolidation policy. In the benchmark model, the electorate is only interested in how the tax burden is allocated intergenerationally. Since the older voter does not have incentive to approve an increase in the current tax level, the benchmark model cannot explain the observed fact.

To explain the fact, we reconsider the underlying assumptions of a benchmark model.

We propose three possible explanations. First, we consider the case where the tax rate and the amount of government spending are jointly determined by the political process. In this case, the older citizen has an incentive to increase the tax rate if it increases public good provision. If older citizens receive greater benefit from government spending, older citizens might be more likely to accept a tax increase to finance additional government spending.

Second, we consider the possibility that the government can raise a tax on domestic savings returns of older citizens after saving decision is made. Government can implement this policy not only by a default on sovereign debt, but also more implicitly by an inflation tax with an assist of central bank.4 In this case, the older voter faces a trade-off between a tax on consumption and a tax on current saving. Since this ex post tax on saving implies redistribution from older citizens who hold more domestic assets compared to younger citi- zens, the older voter might accept a consumption tax increase to prevent heavy taxation on saving.

Third, we relaxes the assumption of perfect knowledge by the voter. Although our model assumes that the voter has perfect knowledge concerning the current fiscal situation and their impact on future policies, the voter might have only limited information in reality. If the lack of political and economic knowledge causes citizens to underestimate the problem of fiscal sustainability, citizens’ knowledge would be correlated with their support for fiscal consolidation policies. According to this argument, the older voter might be more likely to

4In facts, there are some opinions that the main purpose of a monetary easing in Japan since Abe Cabinet started in 2012 might be monetization.

support consolidation policies if the older voter has more political concerns and takes the current fiscal situation more seriously than the younger voter.

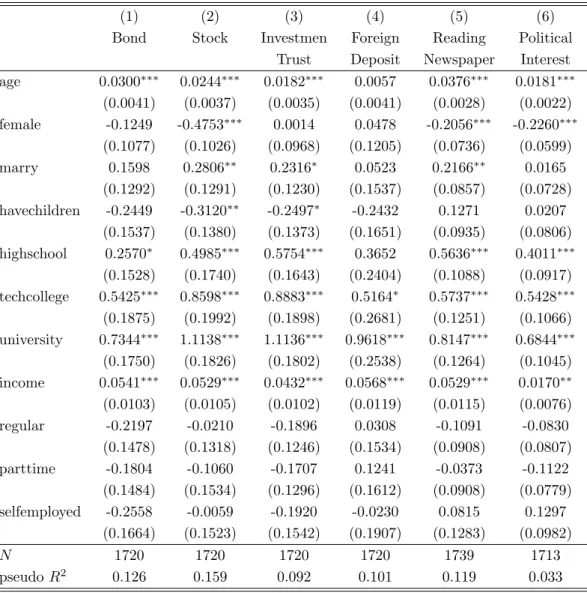

In the latter part of the paper, we test the validity of these hypotheses using policy preference data, asset holdings, and citizens’ knowledge. We show that the coefficients of ages on the preferences for the rise in consumption tax does not change even after controlling several proxies for the preference for the amount of government spending. On the other hand, we find that the citizen who holds bonds and reads newspapers more frequently is likely to support a consumption tax increase. Interestingly, holding foreign stock does not have any significant effect on the preference on the consumption tax increase. Moreover, when we control the effect of asset holdings and the frequency of reading newspapers, the correlation between age and support for a consumption tax hike becomes weaker. Although we cannot derive a definite conclusion on the channel through which age influences policy preferences from this evidence, older citizens’ concern for their assets’ value or their political knowledge are likely to explain the parts of reasons why an old supports fiscal consolidation in Japan.

This study is related to several studies that analyze the determinants of fiscal policy preference using survey data. Many studies analyze the determinants of preference on redis- tributive policy (e.g., Corneo and Gruner 2002, Alesina and La Ferrara 2005, Alesina and Fuchs-Sch¨undeln 2007, Alesina and Giliano 2011, Giuliano and Spilimbergo 2013).5

On the other hand, a few studies analyze preferences for fiscal consolidation policies.

But, an existing few studies suggest that Japan is not only country that old support fiscal consolidation more. Blinder and Krueger (2004) investigate the process of public opinion formation using a telephone survey of a sample of the US population. Although they do not address fiscal consolidation policies directly, the authors show that older respondents are more likely to consider the fiscal deficit a serious problem while they are less likely to consider raising tax an appropriate way to reduce the deficit. Heinemann and Hennighausen (2012) and Hayo and Neumeier (2017) also find that older citizens are more likely to demand public debt reduction using German Survey data. Walter et al. (forthcoming) also find that older voters tend to agree with austerity programs rather than young people using the original survey data in Greece. Although these authors find similar evidence as we find in Japan, they do not analyze the reason why older citizens prefer debt reduction because the intergenerational conflict over consolidation policy is not the main focus of their analysis. 6 This paper goes further ahead. We try to investigate the reason why older citizens prefer consolidation using a simple political economic model and Japanese data. In particular, to

5While several studies analyze fiscal policy preferences(e.g., Ohtake and Tomioka 2004, Hayo and Ono 2010, Yamamura 2012, 2014) using survey data from Japanese citizens, there is no empirical research that analyzes Japanese citizens’ preferences for fiscal consolidation.

6The intergenerational conflict over policy preference is studied more substantially in research that an- alyzes demand for government spending. Much research examines the differences in opinion between gen- erations over public education spending. The empirical research using survey data typically confirms that the older voter is less likely to support spending on public education, which is consistent with the standard economic theory since government spending on public education is considered redistribution from older to younger generations (e.g., Bruner and Baldson 2004, Cattaneo and Wolter 2009, Rattsøand Sørensen 2010, Sørensen 2013, Bruner and Johnson 2016).

the best of our knowledge, no previous study analyzes the relationship between financial asset holding and fiscal policy preferences.

Our explanation on the reason why older citizens prefer debt reduction can provide an important lesson for other countries because the arguments that the aging electorate causes political bias toward the interests of the older electorate are commonly observed in many advanced countries. In countries where the accumulation of sovereign debt is outstanding, such as Italy and Greece, loose financial administration is often attributed to political rule by the older generation. For instance, in an article in the Financial Times, the common view of the young Italian is described as follows “(young people) feel stifled by Silvio Berlusconi’s older generation of political leaders who drove Italian public debt to crippling levels and kept the top jobs to themselves for decades.”7Our results suggest that there is a mechanism that an old rather prefers a reduction of debt to save their assets.

Our finding is also related to the recent discussion on political reforms in aging societies.

In developed countries where there is a tendency for the political power of older citizens to increase, some people insist on election system reform to ensure equality between generations.

Giving suffrage to the youth is a standard reform plan, which has been introduced in some regions and countries in recent years. For instance, the voting rights in the parliamentary election in the United Kingdom was extended to 16 and 17-year-old citizens in 2016. In Japan, the voting age has recently been lowered to 18. The Demeny voting system, which gives political influence to children by allowing parents to vote on behalf of their children, is being discussed as an alternative reform plan in several countries such as France, Germany, Hungary, and Japan. 8 Although there are additional aims of such electoral reform plans, the concern for fiscal sustainability is included in the reform plan objectives. However, our result casts doubt on the argument that such electoral reforms will enhance fiscal sustainability.

The remainder of the paper is organized as follows. In Section 2, we explain the back- ground of the recent fiscal policy in Japan. In Section 3, we explain the characteristics of our data. Section 4 provides the basic empirical results. In Section 5, we build a simple political economic model for government debt to consider the implications of our findings theoretically. We propose several hypotheses that explain our empirical findings. We test the validity of these hypotheses using data in Section 6. Finally, we provide some discussion and conclusions in Section 7.

7“Italy’s Generation X hopes to loosen grip of gerontocracy”Financial Times, December 2, 2016 https://www.ft.com/content/e1075190-b7d6-11e6-961e-a1acd97f622d?mhq5j=e5

8In Japan, several other electoral reform plans are being discussed. For instance, Doi and Ihori (1998) propose electoral reform that reallocates representatives’ seats to each generational group. By assigning a fixed number of seats to each generation, it solves the problem whereby the aging population causes political bias toward the older voter through an increase in the age of the median voter. See also Kato and Kobayashi (2017).

2 Background

In this section, we briefly explain the recent history of consumption tax and public finance in Japan. The amount of public debt in Japan has been ballooning for some decades. While the government began issuing government bonds in 1966, the gross liability of Japan’s general government has grown since 1966 and reached over 220% in 20169.

Faced with accumulating public debt, the sustainability of the fiscal system in Japan has been doubted since the mid 1990s. In response to the severe fiscal situation, the government has attempted to enact fiscal consolidation. In 2001, the government developed the basic plan for economic fiscal policy (Basic Policies for Economic and Fiscal Policy Management and Structural Reform) and set the following policies to restore fiscal sustainability: (i) The government restricts the issue of new government bonds to a maximum of 30 trillion yen.

(ii) The government will transform the primary balance of the budget into a surplus.

Although the fiscal balance gradually improved in the mid-2000s toward a surplus by the early 2010s, the primary balance again deteriorated due to the financial crisis in 2008.

After the change in government on September 9, 2009, the administration of the Democratic Party of Japan formulated the Basic Frame for Fiscal Consolidation: Medium-term Fiscal Plan in 2010 and emphasized the aim of improving the primary balance and persistently reducing the amount of government debt to GDP ratio. In the plan, the government aimed to reduce the primary deficit of national and local governments to GDP ratio by half from 2010 to 2015 and bring the primary balance of the budget into surplus by 2020. The coalition government composed of the LDP (Liberal Democratic Party) and Komeito decided to take over the target of fiscal consolidations after the change of government on December in 2012.

However, it will be difficult to achieve a primary surplus for national and local governments by 2020 even if increases in the consumption tax to 10% can be implemented. In 2017, Prime Minister Shinzo Abe recognized that the fiscal situation is such that the goal will be difficult to attain.

The comprehensive reform of social security and tax systems have played a key role in the fiscal consolidation plans of the government since 2011. The reform proposal in 2011 stated that the consumption tax rate would be raised gradually to 10% by the middle of 2010.10 Consumption taxation is considered an important channel for increasing primary revenues and attaining fiscal consolidation. 11 Additionally, in the Basic Frame of Fiscal Consolidation, the government plans to increase the consumption tax rate taking economic conditions and other factors into account.

The consideration of economic conditions allows discretion and make the implementation

9Data source: OECD Economic Outlook 2017 (June).

10The consumption tax was introduced in Japan in 1988. Then, the tax rate was 3%. In 1998, the consumption tax rate was raised from 3% to 5%.

11For instance, the IMF (2011) reported that Japan faces a severe situation regarding fiscal sustainability and should raise the consumption tax rate as a main revenue source to avoid a fiscal crisis. Many academic studies also investigate sustainable fiscal policy and show a similar result that implies that Japan must adjust its fiscal policy and fiscal sustainability system (e.g., Ihori et al., 2005; Imrohoroglu and Sudo, 2011; Arai and Ueda, 2013; Hansen and Imrohoroglu, 2016; Imrohoroglu et al; 2016).

of fiscal consolidation politically difficult. In 2014, the consumption tax rate was raised from 5% to 8% as planned. However, in 2014, a further increase in the consumption tax rate from 8% to 10%, which was scheduled in October 2015, was postponed to April 2017 by the political decision of the prime minister Abe. Moreover, it was postponed again to October 2019 in June 2016 because of economic stagnation and sluggish domestic demand.

Political consideration underlies delays in fiscal consolidation. The consumption tax is unpopular with voters and, hence, it is necessary to avoid tax increases to win the election.

The opposition to tax increases remains strong at present, and there are concerns of a further delay in fiscal reform.

3 Data

In this section, we discuss our investigation of intergenerational differences in attitude toward consolidation policies. We describe our data and the measurement of preferences for the consumption tax rate from the data.

We use survey data from the Japanese General Social Survey (JGSS) and opinion poll data from the University of Tokyo/Asahi Shimbum Survey (UTAS). The JGSS is a Japanese version of the General Social Survey and collects data including demographic characteristics such as age, sex, family structure, education, and income. The JGSS also collects opinions, preferences, and data on the sense of values of a wide range of respondents. 12 While the survey has been conducted periodically since 2001, and most of the survey data are available, we use the data from 2010 (JGSS2010) and 2012 (JGSS2012) because these surveys investi- gate opinions on the desirable consumption tax rate in the context where public discussion on the consumption tax increase attracts much attention at the time when the two surveys were conducted. The government decided on the consumption tax increase in 2013, and the tax rate was increased from 5% to 8% in 2014. 13 Our data contain citizens’ opinions on the desirable level of consumption tax at the time before the government eventually decided on the consumption tax increase.

While the JGSS contains cross-sectional data, and respondents are not the same in the 2010 and 2012 surveys, these two surveys use the same method and contain many overlapping question items. Therefore, we pool the data from the two surveys and analyze preferences for fiscal consolidation using the pooled data.

As secondary data source, we use data from the University of Tokyo/Asahi Shimbum Survey (UTAS), which has jointly conducted public opinion polls since the 46th Lower House

12The JGSS is designed and conducted by the JGSS Research Center at Osaka University of Commerce (Joint Usage/Research Center for Japanese General Social Surveys accredited by the Ministry of Education, Culture, Sports, Science and Technology) in collaboration with the Institute of Social Science at the Uni- versity of Tokyo. The JGSS adopts both interview and detention methods using a questionnaire to collect survey data. The questions on subjects that would relate to social justice or morals are posed using the detention method. The survey population is composed of men and women from 20 years old to 89 years old.

The survey subjects are selected using a stratified two-stage sampling method.

13Although a further tax increase from 8% to 10% was supposed to take place in 2017, the Japanese government decided to delay it until 2019.

general election in 2012. 14 The prominent characteristic of this data are that it includes data on the political preferences of candidates running for the Diet, although we use only the opinion data of citizens. The survey was conducted nationwide and questionnaires were sent to 3,000 voters; responses were received from 1,900 voters, and data on the attitudes toward various policy dimensions including diplomatic issues, political reform, trade policies, and fiscal policies were obtained. The advantage of the UTAS data is that the data reflect respondents’ opinions on tax policies and on the desirable amount of government spending.

On the other hand, we find more demographic variables, such as the income of respondents, in the JGSS. Therefore, we use the UTAS to back up our findings obtained in the JGSS.

3.1 Preferences for the Consumption Tax Rate

Let us first discuss how to measure the preferences for fiscal consolidation using the JGSS survey data. We measure preferences for fiscal consolidation using the following question on the consumption tax rate: “At what level do you think the consumption tax rate should be?” This question was posed to 2,507 respondents in the JGSS 2010 and 4,667 in the JGSS 2012. 15 The respondents were asked to choose their answers from six alternatives, which are composed of two categories with the tax rate less than 5 %, one with a tax rate of exactly 5%, and three with tax rates higher than 5%. 16 We focus on whether the respondents choose a tax rate higher than 5%, which is the actual consumption tax rate at the time of each survey, and construct a binary variable that takes a value of 1 if the respondents choose alternatives that indicate tax rates higher than 5% and 0 otherwise. In the following analysis, we regard those who choose tax rates higher than 5% as supporters of the consumption tax increase and empirically analyze the determinants.

In the UTAS, citizens are asked for their opinions on tax policies and fiscal stimulants.

Concerning fiscal consolidation, the following statement is presented: “For the time being, the government should increase spending to stimulate economic activities rather than cut spending for fiscal consolidation.” The respondents are required to choose their answers from five alternatives: agree, somewhat agree, cannot say (between agree and disagree), somewhat disagree, and disagree. The respondents are also asked to provide their opinion of the consumption tax increase using the following statement: “In the long run, it is inevitable that the consumption tax rate will be higher than 10%.” The respondents choose their answers from five alternatives, which are the same as those above. We use each respondent’s response to these questions as their preference for fiscal consolidation and the consumption tax increase.

14The UTAS is conducted by Masaki Taniguchi at the University of Tokyo and the Asahi Shimbun.

15Approximately half of the respondents in the JGSS 2010 are not asked their opinion on the consumption tax.

16Although the questions were the same for the JGSS 2010 and 2012, there was a slight difference in their alternatives. While the six alternatives were (1) 0%, (2) 1 to 4%, (3) 5%, (4) 6 to 7%, (5) 8 to 9%, and (6) more than 10% in the JGSS 2010, The alternatives in 2012 were (1) 0%, (2) 1 to 4%, (3) 5%, (4) 6 to 9%, (5) 10 to 14%, and (6) more than 15%. To control any possible influence caused by the differences in the answer categories between the JGSS 2010 and 2012, we include a survey year dummy in the following analysis.

3.2 Independent Variables

Following the literature, we include some control variables such as sex, marital status, number of children, education, employment status, and annual household income in our analysis.

These variables are designed to control for economic and demographic characteristics among citizens that might influence their preference for fiscal consolidation.

We classify respondents into the following four categories according to their terminal ed- ucation record: elementary and junior high school, high school, some college, and university.

17 Employment status is classified into four categories in the JGSS data: regular employment (seiki-koyo), part-time employment (hiseiki-koyo), self-employment, and not working. 18 In the UTAS data, we created two different categories, public servant and student, in addition to the four categories. For household income, only JGSS asks for pre-tax household income that includes wages and pension benefits, yields on shares, and income from real estate. The respondents are asked to choose their answers from among several income categories. We record the median value of the category that the respondent chooses as household income.

19

We also include additional controls in some specifications. (1) Whether a respondent lives in a city with a population over 250,000. (2) A subjective evaluation of their health status (five grades). (3) Whether the respondent has their own house20(4) Whether the respondent trusts members of Congress2122(5) Whether the respondent donated during the past year.

(6) Whether the respondent will participate in volunteer activities23The last two variables are included in the JGSS 2012, which was conducted in the year following the Great East Japan Earthquake. We use these two variables as a proxy for respondent altruism.

[Table 1, 2 here]

17Both the JGSS and UTAS ask respondents for their terminal education record. The “some college”

category includes colleges of technology and junior colleges. Graduate school is included in the university category.

18Managers and directors are included in regular employment while part-time and temporary workers are included in non-regular employment. We provide a more rigorous explanation of the variables in the appendix.

19We assign 350 thousand yen for the respondent who chooses the lowest category, less than 700 thousand yen for the next lowest category, and 25 million yen for the respondent who chooses the highest category of more than 23 million yen.

20Stadelmann and Eichenberger (2012, 2014) show that public debts capitalize into prices of property.

House ownership might affect policy preference through the capitalization effect of public debt.

21Stix (2013) shows that the credibility of fiscal consolidation matters with regard to attitudes toward fiscal consolidation policies.

22In the JGSS, there are questions concerning trust in members of Congress as follows: “How much do you trust members of Congress?” We regard those who respond with “trust a lot” or “trust a little” as having trust in politicians, and we examine the impact. Since half of the respondents in the JGSS 2012 are not asked about trust toward members of Congress, the sample size substantially decreases when we include trust in politicians in our analysis.

23JGSS 2012 asked respondents, “Would you like to participate in volunteer activities if there is an oppor- tunity to from now on?” We regard those who respond with “I’d like to participate” or “I’d like to participate if I could” as having the will to participate in volunteer activity.

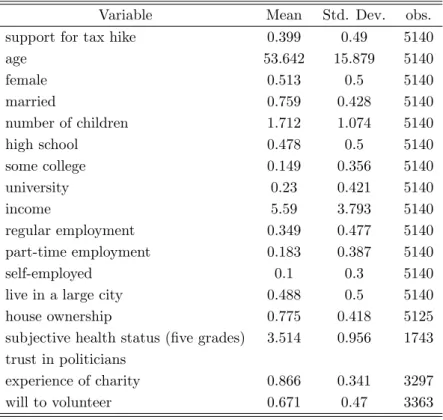

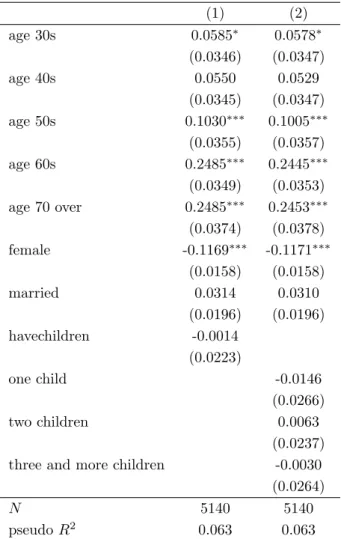

Table 1 and 2 provide the summary statistics for the variables used in our analysis. 24 Table 1 shows that 39% of respondents of the JGSS support a consumption tax hike.

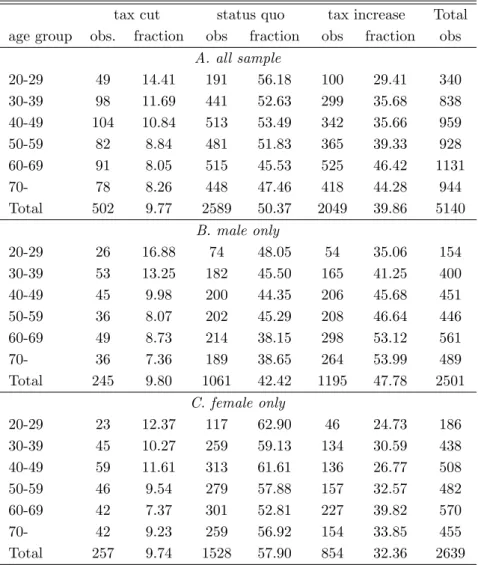

Table 3 shows how consumption tax preferences vary among different demographic groups.

Approximately half of all respondents choose the status quo for the consumption tax rate.

While 46% of those aged in their 60s support a consumption tax increase, only 29% of those aged in their 20s support a consumption tax increase. Few people hope for a reduction in the consumption tax rate, which is natural when we consider the current fiscal situation in Japan. However, there is a tendency among younger respondents to hope for a reduction in consumption taxes compared to older individuals.

Panels B and C in Table 3 compare the gender differences. The results show that female respondents are less likely to support a consumption tax increase. The tendency that the fraction of tax hike supporters increases with age is observed both in the male and female sample, although it is less obvious in the latter. These findings contradict the standard argument that the older generation would postpone the implementation of consolidation policies and impose greater fiscal burden on future generations.

[Table 3 here]

4 Empirical Results

This section shows our empirical results. We first show the results from the JGSS.

4.1 Japanese General Social Survey

Following the literature on fiscal policy preferences, we control several demographic variables to isolate the impact of age on support for a consumption tax increase, which cannot be explained by the correlation between age and other demographic variables. We use the following regression model to clarify how tax policy preferences are related to age and other variables,

Yit=β0+β1Ageit+β2Xit+δt+ϵit (1) whereYitrefers to support for the tax increase. In the benchmark specification,Yitrefers to whether the respondentisupports the consumption tax increase, and we estimate (1) using probit regression. 25 The subscripttrefers to the survey year.

In Model (1), our main concern is whether the coefficient of age,β1, is positive or negative.

The other basic control variablesXitinclude the demographics of the respondent isuch as sex, marital status, number of children, education, employment status, and annual household

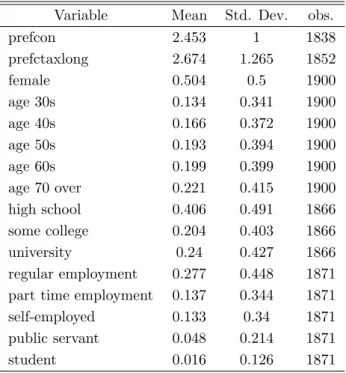

24There is no information on marital status and family structure in the UTAS data.

25Even if we measure preferences for a tax increase more precisely by dividing the respondents into (i) those who choose a tax rate less than 5%, (ii) those who choose a tax rate equal to 5%, and (iii) those who choose more than 5%, our qualitative result does not change. In this case,Yit is the ordered variable that refers to the degree of preference for the consumption tax increase, and we estimate (1) using an ordered probit. The result is available upon request.

income. We always include the survey year fixed effectδt, which captures any differences between the survey years.

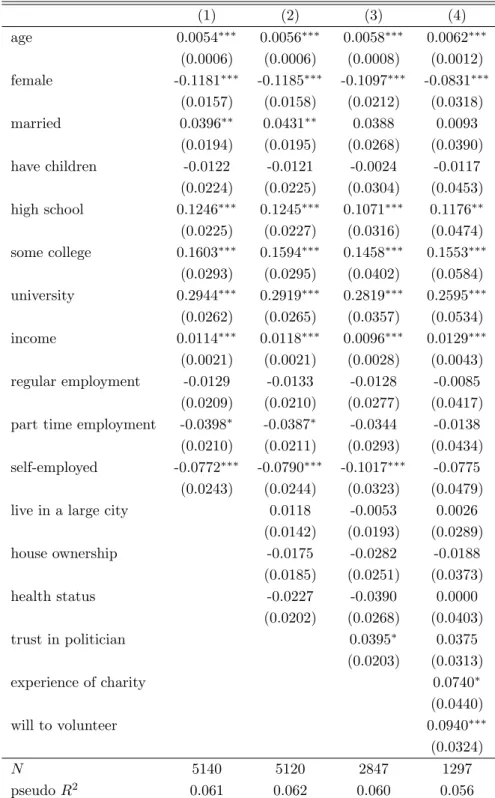

Table 4 provides the estimation results from our basic specification. The explained vari- able is whether the respondent supports a consumption tax increase, and Table 4 reports the marginal effect on such support. The important finding is that older individuals are significantly more likely to support a consumption tax increase even if we control the demo- graphic variables. In all specifications, the impact of age is significantly positive, and the estimated marginal effect is approximately 0.5 to 6%. Therefore, aging 20 years increases the probability that the respondent will support a consumption tax increase by approximately 10%, indicating that the intergenerational difference in preference for the consumption tax should not be negligible.

[Table 4 here]

The results in Table 4 do not depend on the assumption of a linear relationship between age and preference for a tax increase. To allow a non-monotone relationship between age and policy preference, we estimate a model that includes the cohort dummies of respondents instead of their age. Table 5 provides the results, which show that there is no clear pattern that strongly denies the monotone relationship between age and preference. The number of supporters of the consumption tax increases consistently with age although individuals in their 60s are more likely to support the tax increase than individuals over 70. Notably, support for the tax increase is significantly large among those in their 60s, which is when Japanese workers typically retire and start to receive pension benefits.

[Table 5 here]

Table 4 also shows that females are significantly less likely to approve of a consumption tax increase. The large estimated impact indicates that gender is one of the most important factors explaining the differences in attitudes toward a tax increase. Moreover, family struc- ture has an impact on preferences for a consumption tax increase. Compared with single individuals, those who are married are more likely to support a consumption tax increase although the estimated impacts are not significant in all specifications. The existence of children, however, has no significant impact on preferences for a consumption tax increase, which is contrary to the results in the previous literature. This result is robust when we allow the nonmonotone relationship between number of children and policy preference as Table 5 shows. Therefore, there would be no tendency whereby individuals with children are more likely to consider the welfare of future generations and, thus, approve fiscal consolidation policies.

The relationship between education and preference for the consumption tax increase is roughly consistent with that of previous research. There is a tendency that more educated individuals are more favorable toward a consumption tax increase. Additionally, household income is a key determinant of preference for a consumption tax increase; rich individuals are significantly more likely to support a consumption tax increase, which might be because of the regressivity of the consumption tax.

Column (2) in Table 4 shows that the positive relationship between age and support for a consumption tax increase is robust even when we include the additional control variables of residential area, house ownership, and health status. Whether the respondent lives in a city with a population of more than 200,000, house ownership and the subjective health status are not related to support for a consumption tax increase. More importantly, the esti- mated impact of age barely changes even if we control these variables. Therefore, we cannot attribute the intergenerational differences in preferences for a consumption tax increase to differences in residual area, house ownership, and health status.

Distrust in the political process might be an obstacle preventing support of fiscal con- solidation policies, as Stix (2013) argues. To test the validity of this argument, we include trust in politicians as an explanatory variable. Column (3) in Table 4 shows that support for a tax increase is not significantly related to trust in politicians, and the intergenerational difference in preferences for a consumption tax increase do not disappear even if we control trust in politicians.

The finding that older individuals tend to prefer a consumption tax increase seems to be robust but not consistent with the standard view that older individuals would place fiscal burden on future generations. Is this because older individuals are altruistic toward future generations? If older individuals value the welfare of society including that of future generations, they would prefer fiscal consolidation policies not for their own interest, but for the public’s interest. 26 To examine whether such a preference exists and can explain the observed intergenerational differences in preferences for fiscal policies, we run the regression model that includes the proxies of altruism as additional control variables. For the proxies of altruism, we use the experience of donation during the past year and volition to volunteer.

Column (4) reports the results. Altruism seems to have a significantly positive impact on support for the consumption tax increase. 27 There is a tendency for individuals who have experience with donating or volunteering to be more likely to approve of a consumption tax increase, which would be beneficial for future generations. However, the marginal effect of age barely changes even if we control the degree of altruism. This is because there is no strong relationship between age and the proxies of altruism. Therefore, altruism cannot explain the observed intergenerational differences in political preferences.

While we find that older Japanese individuals tend to support fiscal consolidation poli- cies, is there a general tendency that they are more likely to support policies for future generations? We provide evidence against this claim from different points of view. We focus on the educational policy of the government, which attracts attention when there is active

26In the model in Section 5, we assume that each agent thinks only of their self-interests. If older individuals focus on the welfare of their offspring as if it were their own, the so-called Ricardian equivalence should hold. That is, any difference in government finance policies does not affect the welfare of citizens given the sequence of public spending. Therefore, in such a case, there would be no intergenerational conflict over fiscal consolidation policies. However, it is difficult to explain our finding based only on the altruism of older individuals because the Ricardian equivalence cannot explain the fact that older individuals aremorelikely to support a consumption tax increase than younger individuals.

27The sample size decreases considerably compared with the benchmark specification because the questions regarding donation and volunteering are contained only in the JGSS 2012.

debate on tax reforms. The Democratic Party, which came to power in 2009, enacted a bill that provides free high school tuition to extend educational opportunity. Since government spending on education is a type of intergenerational transfer from older to younger gener- ations, older individuals care for future generations if there is a tendency that the older generations are more likely to support such educational policy.

Fortunately, the JGSS 2010 investigates respondents’ attitudes toward educational poli- cies as follows: “Are you in favor of policies to make the tuition of public or private school free? ” The respondents are asked to choose an answer from the alternatives, which are agree, somewhat agree, somewhat disagree, disagree, and do not know. Using the JGSS 2010, we estimated the determinants of a positive attitude toward public educational policies using ordered probit estimation.28

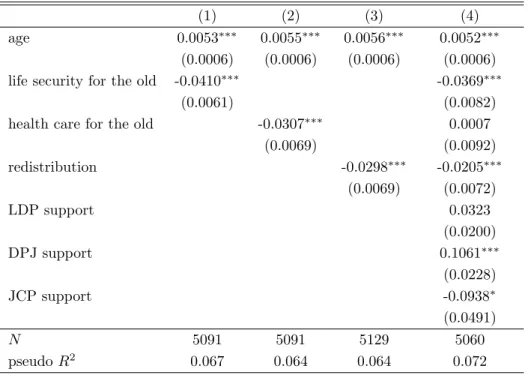

Table 6 provides the results and shows that the coefficient of age is significantly negative.

Therefore, older individuals are significantly less likely to agree with the public subsidy for education, which is consistent with previous research (e.g., Brunner and Balsdon 2004, Cattaneo and Wolter 2009, Brunner and Johnson 2016). Contrary to the case in support of the consumption tax increase, the existence of children has a significant impact on support for educational spending; however, marital status does not. While it seems natural that older individuals are less likely to support an educational subsidy, this result casts doubt on the argument that these individuals care significantly for future generations.

[Table 6 here]

4.2 Opinion Poll by the University of Tokyo and Asahi Shimbum Survey

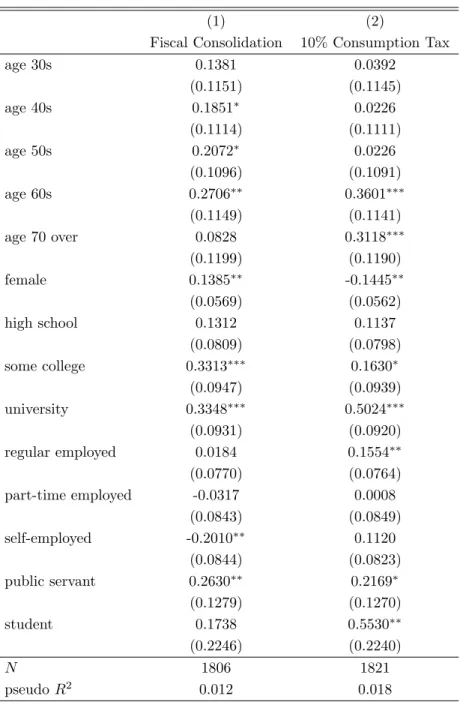

To confirm the robustness of our findings, we reexamine the relationship between age and preference for fiscal consolidation policies using the UTAS data, which have the advantage of more directly investigating respondents’ preferences for fiscal consolidation policies. When we analyze the UTAS data, the dependent variable is the attitude toward fiscal stimulant policies or a consumption tax increase. These are ordered variables, and a higher number corresponds to stronger support for fiscal consolidation or the consumption tax increase.

Therefore, we estimate using ordered probit models.

[Table 7 here]

Table 7 shows that older individuals are significantly likely to prefer fiscal consolidation to stimulate policies and to approve of the consumption tax increase in the long run compared to younger individuals. More precisely, those in their 60s are most likely to support fiscal consolidation policies. While females tend to disagree with a tax increase, which is consistent

28We define the attitude toward subsidy for education by the ordered variable, which takes 4 if the respon- dent chooses agree as the answer to the above question, 3 if they choose somewhat agree, 2 if they choose somewhat disagree, and 1 if they choose disagree. We drop the sample of respondents who choose do not know.

with the result in the JGSS, they are also more likely to support fiscal stimulants. Therefore, it would not be true that females do not support fiscal consolidation policies, but they would prefer spending cuts rather than a tax increase. Additionally, we observe the tendency that more educated individuals support fiscal consolidation policies. Moreover, publicly employed voters and students are likely to approve of a consumption tax increase. Overall, we find no evidence that refutes our findings using the JGSS.

5 Why Do Older Generations Support a Tax Increase?

In the previous section, we find that older voters tend to support a consumption tax increase.

This finding is not consistent with the prevailing view on intergenerational conflict with fiscal consolidation policy. In this section, we build a political economic model for consumption tax and consider the theoretical implications of our findings in the previous section.

5.1 The Benchmark Model

There are some theoretical studies in the literature that analyze the politics of intergener- ational conflict over government debt policy (Tabellini 1991, Song et al. 2012). Following Song et al. (2012), we provide a simple political economic model that captures the inter- generational conflict over consumption tax policy. We consider a small open overlapping generations economy. In every period, one unit of individual is born and lives for two pe- riods. In each period, there is a young individual and an old individual. We assume that there is no production. Each individual is given a certain unit of endowment to allocate to consumption and saving. The government provides public good revenue from a consumption tax or by issuing government debt.

The lifetime utility of an individual born in periodt is given by

Ut= logcyt +θloggt+β(logcyt+1+θλloggt+1). (2) wherecyt is private consumption in youth, cot+1 is consumption in old age, andgtand gt+1

are public good provision in periodtandt+ 1, respectively. The parameterβ is the discount factor, andθ represents the degree of an individual’s preference for public good. Following Song et al. (2012), we assume that there is a difference in preferences for public good between the old and the young. The relative strength ofold’s preference for public good is captured by parameter λ > 0. For instance, if λ > 1 holds, the older individual receives higher marginal utility from public good than the young.

Th individual faces the following budget constraints,

(1 +τt)cyt +st=e, (3)

(1 +τt+1)cot+1=Rst. (4)

Equation (3) is the budget constraint when the individual is young where τt is the con- sumption tax rate,stis private saving, and eis the endowment that the individual receives

at birth. The saving is invested in an open financial market with a constant return, R.

Therefore, the consumption in old age is given by (4).

Given a fiscal policy sequence{gs, τs}∞s=t, each individual chooses the amount of private consumption{cyt, cot+1}and savingstto maximize their utility, equation (2), subject to their budget constraints (3) and (4). Solving the utility maximization problem, we obtain

cyt = e

(1 +β)(1 +τt), (5)

cot+1= β 1 +β

eR

1 +τt+1, (6)

st= β

1 +βe. (7)

We assume that fiscal policy is determined through the political process in each period.

In other words, we suppose that the government cannot commit to future fiscal policies.

Hence the policy in period t must be determined in period t. Therefore, current citizens cannot choose the sequence of future policies directly. However, the current fiscal policy has influence on future fiscal policy because the current policy affects the future fiscal situation.

For instance, the accumulation of government debt approved by current citizens would place an enormous burden on the government budget in the future, which would affect fiscal policies in the future. Since future policy depends on the state of the economy at that time, the current citizens can influence future policy indirectly through the impact of the current policy on the state of the economy in the future. 29

Fiscal policy must satisfy the government budget constraint,

Rbt+gt=τt(cyt+cot) +bt+1, (8) where bt is the amount of public debt at the beginning of period t. Moreover, we assume that the government cannot throw away the repayment of public debt. That is, we do not consider sovereign default.30 This implies that the government can issue public debt only up to the amount that equals the sum of the present value of future primary surplus. Therefore, the government faces the natural debt limit

bt+1≤¯b, (9)

where ¯bis the maximum amount of public debt.

We analyze the intergenerational conflict in fiscal policy by comparing the policy pref- erences of the young and the old agent. We assume that the public good provision of the government is exogenously given in the benchmark model. By fixing the spending size of public finance, we clarify the difference in preference toward the allocation of fiscal burden among generations. Given the amount of public good provisiongt=g, the consumption tax

29We assume that the citizens can choose fiscal policies depending on the state of the economy but not on the entire past history. This is a standard assumption in the dynamic political economic model that analyzes strategic interactions across generations, such as Hassler et al. (2003, 2005, 2007) and Song et al. (2012).

30In the following section, we explicitly introduce wealth taxation to our model. The wealth tax can be interpreted as partial default of public debt or inflation tax.

rate,τt, and the amount of public debt at the beginning of periodt+ 1,bt+1, are determined in periodt by the political process.

The policy that each agent prefers must maximize the following indirect utility function V(a)31

max

τ≥0,b′≤¯b

V(a) =−log (1 +τ)−β(1−a) log (1 +T(b′)), (10) s.t. b′=Rb+g− τ

1 +τ

(1 +βR)

1 +β . (11)

wherea ∈ {0,1} indicates the age of the agent. It holds that a= 0 if the agent is young, whereas it holds thata= 1 if the agent is old.

We drop the time subscripttin (10) and (11) because our model has a recursive structure.

The variables τ andb are the consumption tax rate and the amount of public debt in the current period, whereasb′ is the amount of public debt at the beginning of the next period.

The functionT(b′) represents the consumption tax rate in the next period, which depends on the amount of public debt at the beginning of the next period. As (10) shows, the welfare of the young agent depends on the consumption tax rate in the next period,T(b′). 32 Given the amount of the government debt b, the agent chooses the current fiscal policy, (τ, b′), taking their influence on the consumption tax rate in the next period into account.

We assume that the function T(b′) is differentiable. Then, we can derive the change in welfare caused by the marginal increase of the current consumption tax rate as follows

dV(a)

dτ =− 1

1 +τ + 1 (1 +τ)2

(1 +βR)e

1 +β × β(1−a) 1 +T(b′)

dT

db′. (12)

The first term on the right side of the equation (12) is the utility loss due to a decrease in the current consumption by an increase in the consumption tax rate in the current period.

As (5) and (6) show, the current consumption necessarily decreases when the consumption tax rate increases, which is the marginal cost of the consumption tax increase for the agent.

Moreover, the change in the tax rate in the current period affects the amount of public debt at the beginning of the next period through the government budget constraint and, thereby, influences the consumption tax rate at the next period. The second term on the right side of the equation (12) captures the welfare effect of this channel.

Equation (12) shows the intergenerational differences in policy preference. Since the utility of the old agent (a = 1) does not depend on the consumption tax rate at the next period, an increase in the consumption tax rate at the current period always decreases the

31In this case, the upper bound of public debt ¯bcan be represented as

¯b=Q−g R−1, whereQ=(1+βR)e1+β .

32Since we assume that the citizens can choose fiscal policies depending on the state of the economy, the consumption tax rate in the next period depends on the amount of public debt at the head of the next period. While we take functionT(b′) as exogenously given, we can derive it by analyzing the Markov perfect political equilibrium. We provide the policy function in political equilibrium in the appendix.

utility of the old agent:

dV(1)

dτ =− 1

1 +τ <0 (13)

Therefore, the old agent would like the consumption tax rate to be as low as possible.

On the other hand, there would be a benefit to the consumption tax increase for the young agent (a= 0) if it holds that dbdT′ >0. This is because the government can reduce the current issuance of public debt if it increases the current consumption tax rate. If the decrease in the government debt yields a decrease in the consumption tax rate in the next period, the young agent can increase consumption in the next period. Therefore, if less issuance of government debt in the current period implies a lower consumption tax rate in the next period, the young individual can receive benefit from the fiscal consolidation policy.

In such circumstances, it necessarily holds that dVdτ(0) >dVdτ(1). Hence, the older individual would not prefer a higher consumption tax rate than the younger individual if dbdT′ >0.

Proposition 1. Suppose that the amount of public good provision is exogeneously given, gt=g. Moreover, we assume that the consumption tax rate in the next period increases the amount of government debt at the beginning of the next period, dTdb′ >0. Then, older citizens do not prefer a higher consumption tax rate than the young.

Proposition 1 captures the basic insights of the prevailing argument for the intergenera- tional conflict over fiscal consolidation policy. If the political interest is only focused on how to share the cost of public good provision among generations, there is no reason for older citizens to support an increase in the consumption tax rate. On the other hand, there is some benefit to a consumption tax increase for younger citizens if the future consumption tax rate increases as government debt accumulates. The assumption that the future consumption tax rate is increasing in the future amount of public debt, dbdT′ >0, seems natural because the large accumulation of government debt eventually makes a tax increase unavoidable.

33 Therefore, the standard theory predicts that the older citizen generally prefers a lower consumption tax rate than the younger citizen.

While we provide a simple political economic model, and its prediction is consistent with the prevailing argument, our findings in section 4 do not support such a prediction.

Therefore, we must consider why the benchmark model cannot explain the empirical findings.

34 In the following, we examine how the role of three assumptions underlies the benchmark model, that is, exogeneous public good provision, the perfect commitment of the government to the repayment of public debt, and perfect knowledge of agents. By reconsidering these assumptions, we propose some hypotheses that can potentially explain our empirical findings.

33In the appendix, we derive the policy functionT(b′) endogenously through the voting process. We show that the policy functionT(b′) is monotonically increasing inb′ in a politico-economic equilibrium.

34If we introduce the altruism of the old agent into the model, intergenerational differences in policy preferences would be reduced, but we cannot explain the fact that the older individual does prefer a higher consumption tax rate than the younger individual by the altruism of the older agent.