Doctoral Dissertation

(Ph.D. in Public Management)

PERFORMANCE MANAGEMENT SYSTEM UNDER THE PROGRESS OF DECENTRALIZATION

A COMPARATIVE STUDY ON

THE ROLE OF PERFORMANCE AND ACCRUAL BASED INFORMATION IN THE DEVELOPMENT OF

NEW PUBLIC GOVERNANCE

July 2010

The Okuma School of Public Management Waseda University

TJUNG Mei Ling

TABLE OF CONTENTS

ACKNOWLEDGEMENT ... v

INTRODUCTION ... 1

PART I. THEORETICAL FRAMEWORK DEVELOPMENT OF PERFORMANCE MANAGEMENT IN NEW PUBLIC GOVERNANCE ... 3

CHAPTER 1. BACKGROUND, OBJECTIVES AND RATIONALE OF THE STUDY ... 4

SECTION 1. DECENTRALIZATION:THE TRANSFORMATION FROM HIERARCHICAL GOVERNANCE TO DISTRIBUTED GOVERNANCE ... 4

1.1. Functional segregation and redefinition of business processes of central governments and service delivery partners ... 7

1.2. The relation between the central government, service delivery partners and stakeholders in distributed governance ... 9

SECTION 2. DISTRIBUTED GOVERNANCE AS ONE FORM OF NEW PUBLIC GOVERNANCE ...11

SECTION 3. PERFORMANCE MANAGEMENT UNDER THE PROGRESS OF DECENTRALIZATION:THE CHANGE IN THE ROLE OF PERFORMANCE AND ACCRUAL (COST) INFORMATION ... 13

SECTION 4. THE SCOPE OF THE STUDY ... 17

CHAPTER 2. LITERATURE REVIEW ... 20

SECTION 1. LIMITATIONS OF PREVIOUS RESEARCH REGARDING PERFORMANCE MANAGEMENT ... 20

SECTION 2. THEORETICAL APPROACHES TO PERFORMANCE MANAGEMENT ... 23

2.1. Contingency Theory ... 25

2.2. Complex Adaptive System ... 27

CHAPTER 3. THE DEVELOPMENT OF A PERFORMANCE MANAGEMENT MODEL UNDER THE NEW PUBLIC GOVERNANCE... 32

SECTION 1. THE DEVELOPMENT OF A PERFORMANCE MANAGEMENT MODEL: INTEGRATING PERFORMANCE MEASUREMENT AND ACCOUNTING PRINCIPLES INTO PERFORMANCE MANAGEMENT TO REGULATE THE RELATIONSHIP BETWEEN ACTORS AND STAKEHOLDERS ... 32

SECTION 2. DEVELOPMENT OF HYPOTHESES ... 47

2.1. A performance management system accommodates the transformation from hierarchical to quasi-contractual accountability ... 49

2.2. A performance management system accommodates the transformation from line item expenditures to costs under a strategic perspective ... 51 2.3. A performance management system accommodates the transformation from an annual to a strategic

perspective by linking the accountability purpose to the managerial purpose (PDCA cycle) ... 53

SECTION 3. DATA AND METHODOLOGY ... 55

CHAPTER 4. PERFORMANCE MANAGEMENT SYSTEMS IN OECD COUNTRIES ... 64

SECTION 1. PERFORMANCE MANAGEMENT REFORM IN OECD COUNTRIES: REFORM IN DECENTRALIZATION, PERFORMANCE MEASUREMENT AND ACCOUNTING SYSTEM TOWARD THE UTILIZATION OF PERFORMANCE AND ACCRUAL (COST) INFORMATION IN THE PDCA CYCLE ... 64

SECTION 2. PERFORMANCE MANAGEMENT SYSTEMS IN OECD COUNTRIES:VARIABLE DESCRIPTION ... 69

SECTION 3. HYPOTHESIS TESTING AND MODELING RELATIONAL AND CAUSAL LINKAGES ... 83

PART II CASE STUDIES ON THE DEVELOPMENT OF PERFORMANCE MANAGEMENT SYSTEMS UNDER THE TRANSFORMATION FROM NEW PUBLIC MANAGEMENT TO NEW PUBLIC GOVERNANCE ... 114

CHAPTER 5. A PERFORMANCE MANAGEMENT SYSTEM UNDER THE FRAMEWORK OF SPENDING REVIEWS, PUBLIC SERVICE AGREEMENTS, RESOURCE ACCOUNTING AND BUDGETING IN THE UNITED KINGDOM ... 115

SECTION 1. PERFORMANCE MANAGEMENT SYSTEM UNDER THE PROGRESS OF DECENTRALIZATION IN THE UNITED KINGDOM ...115

SECTION 2. ANALYSIS OF THE PERFORMANCE MANAGEMENT FRAMEWORK IN THE UNITED KINGDOM ... 120

2.1. Performance measurement system ... 120

2.2. Strategic perspective of the performance management framework ... 121

2.3. The development of the accrual (cost) concept under the reconciliation between cash and accrual-based information under the strategic perspective ... 122

2.4. Distributed governance: The quasi-contractual relation and stakeholder management/involvement in the United Kingdom (UK) ... 124

2.5. Utilization of performance and accrual (cost) information in decision making ... 126

2.6. Development of the performance management model in the United Kingdom ... 127

CHAPTER 6. A COMPARATIVE CASE STUDY ON PERFORMANCE MANAGEMENT SYSTEMS UNDER THE PROGRESS OF DECENTRALIZATION IN JAPAN AND INDONESIA ... 129

SECTION 1. THE PROGRESS OF ADMINISTRATIVE DECENTRALIZATION IN JAPAN AND INDONESIA TOWARD THE DEVELOPMENT OF NEW PUBLIC GOVERNANCE ... 129

SECTION 2. THE REFORM OF PERFORMANCE MEASUREMENT AND ACCOUNTING SYSTEMS IN THE CENTRAL GOVERNMENT OF JAPAN AND INDONESIA ... 141

SECTION 3. THE DEVELOPMENT OF A PERFORMANCE MANAGEMENT MODEL UNDER THE PROGRESS OF DECENTRALIZATION IN JAPAN AND INDONESIA:HYPOTHESIS TESTING AND MODELING RELATIONAL AND CAUSAL LINKAGES……. ... 150

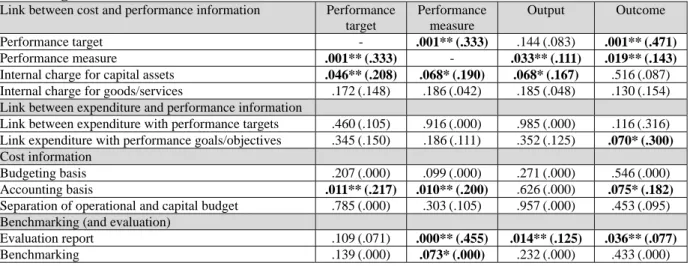

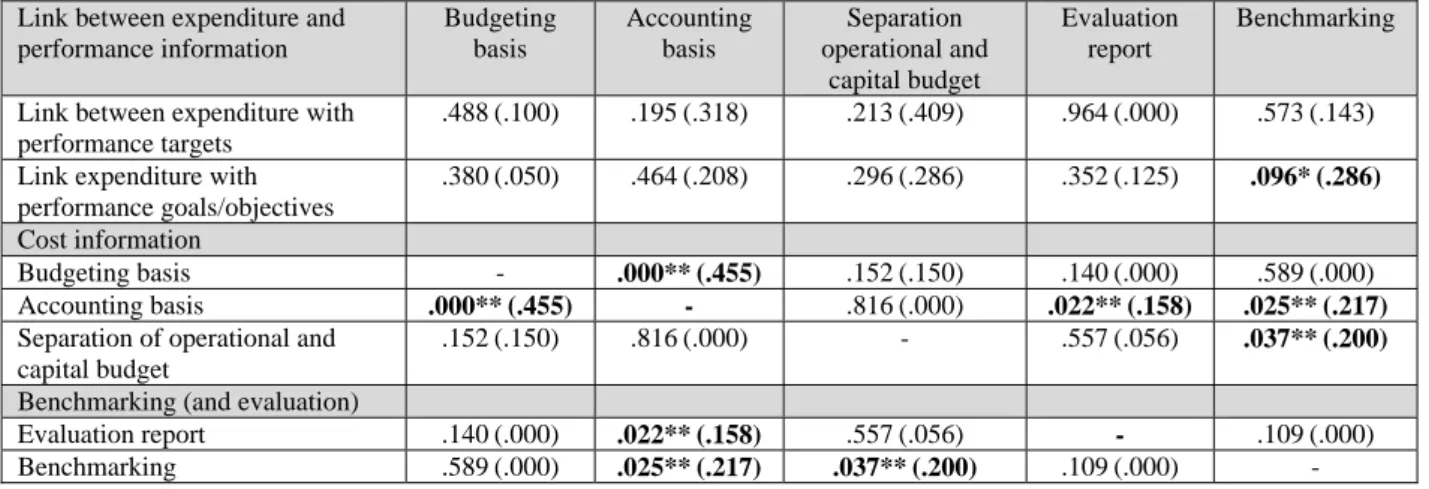

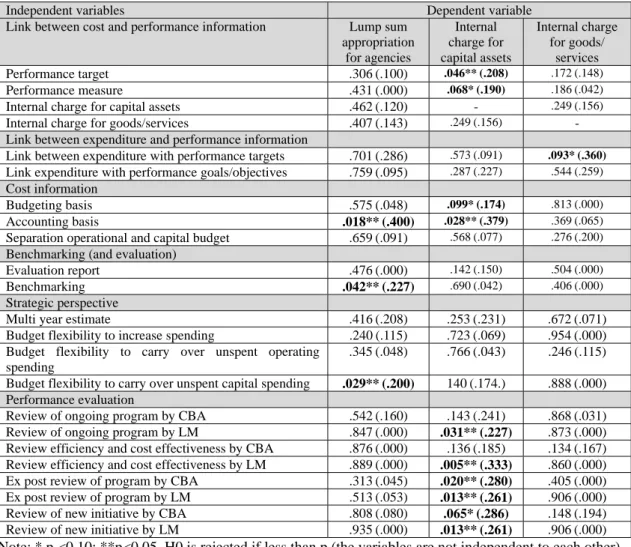

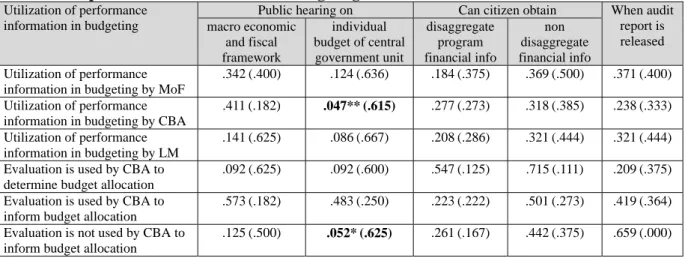

3.1. The variables and contingency factors for the utilization of performance and accounting information

... 151

3.2. Independent variables: Performance measurement system, accrual accounting system, and the link between cost and performance information ... 154

3.3. Dependent variables ... 156

3.4. Chi-square test: Elaboration on the relational linkages between the central government, service delivery partners and stakeholders with the businesslike level as the control variable ... 166

3.5. Multiple regression analysis: Modeling the causal linkage on the utilization of performance and accrual-based information ... 173

3.6. Performance management model ... 181

PART III CONCLUSION AND FUTURE ISSUES ... 187

CHAPTER 7. THE ROLE OF PERFORMANCE MANAGEMENT SYSTEM IN THE DEVELOPMENT OF NEW PUBLIC GOVERNANCE ... 188

SECTION 1. PERFORMANCE MANAGEMENT SYSTEM IN DISTRIBUTED GOVERNANCE ... 188

SECTION 2. DYSFUNCTION OF THE PERFORMANCE MANAGEMENT SYSTEM IN A CENTRAL GOVERNMENT (GAP BETWEEN IDEAL AND REALITY) ... 192

2.1. Accrual (cost) concept and the link between performance and cost information ... 193

2.2. Stakeholder management and involvement ... 193

2.3. Strategic perspective ... 195

2.4. Performance evaluation and accountability ... 195

SECTION 3. IMPLICATIONS OF PERFORMANCE MANAGEMENT SYSTEM IN INDONESIAN CENTRAL GOVERNMENT…… ... 196

CHAPTER 8. CONCLUSION AND FUTURE ISSUES ... 201

SECTION 1. CONCLUSION ... 201

SECTION 2. FUTURE ISSUES ... 202

BIBLIOGRAPHY ... 203

APPENDIX…. ... 212 Questionnaire on the utilization of performance and accrual-based information in semi autonomous agencies in Japan and Indonesia

ACKNOWLEDGEMENT

First of all, I thank God, for nothing happens without His permission.

I am deeply grateful to my advisor Prof. Kobayashi Mari, for her continuous support throughout the Ph.D. program. She was always there to meet me to talk about my ideas and to mark up my papers and chapters. She has guided me with a great deal of patience and continuous support in many ways. She showed me different ways to approach research problems and demonstrated the need for persistence in order to accomplish any goal. She is primarily responsible for helping me to complete this dissertation as well as the challenging research that lies behind it.

I also thank my co-advisors. Prof. Kishimoto Tetsuya provided insightful comments and reviewed my work on very short notice. He brought out the good ideas in me. Prof. Fukushima Yoshihiko asked me good questions to help me think through my problems. Without their encouragement and constant guidance, I could not have finished this dissertation. Besides my advisors, I would like to thank the rest of my dissertation committee, Prof. Tsukamoto Hisao and Prof. Tsuda Hiroki for their insightful knowledge and comments.

I am also thankful to my supervisors and colleagues in the Ministry of Finance of the Republic of Indonesia for their support in many ways. I would like to dedicate my gratitude to Hekinus Manao, Inspector General of the Ministry of Finance, who has kindly shared his precious knowledge and experience. I am grateful to Sonny Loho, Director for Accounting and Reporting of the Directorate General of Treasury, who has been a great mentor to me throughout my academic and working years. I am indebted to Sumijati for providing me with insightful information.

I have also benefited tremendously from the opportunity provided by MEXT Japan to pursue this educational experience. Learning in Japan has not only enhanced my academic knowledge but also enriched my life. During the course of this work, I was supported in part by research grants from The Fuji Xerox Setsutaro Kobayashi Memorial Fund and the Matsushita International Foundation

Last, but not least, I thank my wonderful parents, my loving brothers and sisters for their unconditional support, prayers, and enthusiastic encouragement to pursue my interests, even when those interests went beyond boundaries of language, field and geography. I dedicate this dissertation to them. Finally, I would like to thank all my friends in Japan for the unforgettable memories we shared. Hopefully the readers may gain useful knowledge from this dissertation.

Any remaining errors are my own liability.

Tjung Mei Ling

INTRODUCTION

Reforms in performance measurement and accrual accounting systems tend to emerge only to fade gradually into routine paper work. Despite the theoretical conviction that performance and accounting information could facilitate decision making and problem solving, answering performance challenges in the public sector, previous research findings have shown that there have been different and disappointing outcomes resulting from the same approach to adopting performance and accrual accounting reform. The performance and accrual information appears to be not widely utilized to its full potential in decision making (Dooren, 2005; Vakkuri and Meklin, 2006; Schick, 2007; Jansen, 2008, Julnes, 2009).

The discussion regarding the utilization of performance and accrual (cost) information in the plan-do-check-action (PDCA) cycle in order to improve government performance originates from the perspective of New Public Management (NPM). A critique of NPM is that it attempts to replace poor public management with private sector management techniques (Bevir et al. 2003), marking an attempt to reduce costs (with implications for services) without considering that public service delivery has different mechanisms from those in the private sector. Although it has been argued that the applicability of NPM concepts to the public sector has deteriorated (Dunleavy et. Al, 2006), it is possible to argue that NPM is one manifestation of new forms of public governance (Osborne, 2010) through the separation of policy making and service delivery, and involving the implementation of performance measurement and accrual accounting systems.

The transformation from the NPM to the New Public Governance (NPG) perspective has been accompanied by a transformation in governance structure. As public sector governance had been steered by the central government, reform has been undertaken from the perspective of the internal organization of the central government, so the performance management system of the public sector had revolved around the concept of government’s plan-do-check-action (PDCA) cycle. As a result, the utilization of performance and accounting information has been considered to be the conversion of knowledge into action, which means using this information in the PDCA cycle and for the purpose of accountability.

Decentralization, particularly the separation between policy making and implementation, has led to a new governance structure of distributed and networked governance. Decentralization has changed the relationship between actors and stakeholders and shaped the business process of central government. Each actor and stakeholder is able to steer the network through their functions. It has further changed the decision-making process in the PDCA cycle.

Decentralization has redefined the performance regime in the NPM concept from an intra organizational focus to the relational and network focus of NPG. A performance management

system has to be adjusted to decentralized government and distributed governance to allow the effective utilization of performance and accounting information in the decision-making process.

This emphasizes the significance of a well-developed and integrated performance management system. The inability of performance management systems to accommodate decentralized government will lead to an ambiguity of performance information (March 1994), which is indicated by a lack of utilization of the information in decision making.

This dissertation constitutes theoretical and practical considerations that guide and inform research in performance management systems. It is expected to contribute to the development of a theoretical framework for an effective performance management system. This dissertation considers the active role of performance and accounting information in regulating the relationship between actors and stakeholders. The decision to utilize the information is not from the actor or stakeholder alone, instead, it is enforced by the relationship with other actors and stakeholders. Decision making should be considered under the relationship between actors and stakeholders, as the decision made by each actor and stakeholder influences the other actors and stakeholders. Consequently, information becomes the rules and routines that regulate the actors and stakeholders toward the negotiated and agreed-upon performance.

This dissertation is based on empirical research into how decentralization, in terms of policy making and implementation, transformed the role of performance measurement and accounting systems in a performance management system in NPG. It is expected to provide an explanation of the development of a performance management system under the integration of a process-based PDCA cycle and relational-based governance structure. It will provide an explanation of how the inability of performance management system to accommodate decentralized government leads to ambiguity of performance information in decision making and causes different and disappointing outcomes resulting from the same approach to adopting performance and (accrual) accounting reform.

It is expected to provide insights to the public sector, particularly to central governments, on how a performance management system should be adapted to reflect the unique characteristics of public sector organizations. Systematic study in this area will help public sector organizations, especially in developing countries, to re-evaluate themselves and to develop appropriate and rigorous methodologies to implement performance management systems. It is expected to provide empirical evidence on the significance of accrual information, particularly cost, not only for accountability purposes, but also for regulating the relationship between actors and stakeholders for the purposes of decision making. It also emphasizes the significance of the customization of performance and cost information to the needs of each actor and stakeholder in the decision-making processes according to their function within the governance structure.

PART I. THEORETICAL FRAMEWORK DEVELOPMENT OF PERFORMANCE MANAGEMENT IN NEW PUBLIC GOVERNANCE

This part explains the theoretical framework development of performance management in New Public Governance. Chapter 1 provides an explanation of the background, objective and rationale of the study. It reviews how decentralization transformed the governance structure of the public sector, which further transformed the roles of performance measurement and accounting systems in performance management systems. Chapter 2 explains the limitations of previous research studies regarding performance management and emphasizes the significance of new theoretical approaches to performance management. Based on the literature review, the performance management model and hypotheses are developed in Chapter 3. Chapter 4 explains the performance management system in Organization for Economic Cooperation and Development (OECD) countries, based on the hypothesis testing.

This dissertation will investigate performance management as a concept, conceptual model and system. A performance management system consists of performance measurement and accounting systems, which generate performance and accounting information.

CHAPTER 1. BACKGROUND, OBJECTIVES AND RATIONALE OF THE STUDY

The wave of public sector reform, which started in Anglo Saxon countries during the late 1970s, has spread throughout the world. It has become an evolving phenomenon, as each region and nation develops its own model and pattern (Hood, 1995; Olson, 1998; Groot and Budding, 2008).

Despite the fact that such reform has been adapted to fit the political and administrative structure of each nation, the reform has articulated similar concepts of decentralization, performance improvement and accountability for performance (Groot and Budding, 2008).

Public sector reforms marked by the transformation of public sectors using private sector performance criteria have been widely and internationally codified as New Public Management (NPM). It has been adopted based on the fact that governments have faith in its deployment to make the public sector more businesslike. The remarkably resilient feature of many public sector reforms under the NPM movement initiated over the past two decades is the pre-occupation with organizational performance (Brunsson, 1989; Hood, 1995; Olson et al., 1998; Bowerman et al., 2002; Williams, 2003; Johnsen, 2005; and Helden, 2005) with a focus on performance measurement (Pollitt and Bouckaert, 2004) and accounting systems (Carlin, 2005). The idea of performance measurement in NPM is to formulate an envisaged performance of an entity, and to indicate how this performance can be defined and measured. It implies a perspective of performance measurement that is broader than financial indicators.

As mounting research studies argue that NPM fails to capture the complex reality of the design, delivery and management of public service delivery (Hood and Jackson, 1992; Lapsley, 2008;

Osborne, 2010), there is a pressing need for a more comprehensive and integrated approach to analyze how the development of governance concepts in policymaking and public service delivery transforms the concept of performance management.

Section 1. Decentralization: The transformation from hierarchical governance to distributed governance

A hierarchy facilitates the command and control mechanism in central government and is considered as the precondition for political accountability. It is argued that only through the existence of an unbroken hierarchy does it make sense to hold the executive accountable for the decisions made within the administration. Still, even if hierarchy is the dominant organizational form within the public sector, public sector organizations rarely stand alone. The size of the service area of public sector organizations, the complexity of their tasks and stakeholders, and

the limitation in financial capacity imply that the operation of public administration relies on extensive decentralization through and outside the hierarchy.

The term decentralization has a broader meaning than just the transfer of authority from a central to a local government. There are various typologies of decentralization, but this dissertation will utilize the categorization of political, administrative, fiscal and market decentralization (World Bank, 2000), particularly administrative and market decentralization, as they relate to the separation between policy making and implementation, which is the main focus of this dissertation. Administrative decentralization seeks to redistribute authority, responsibility and financial resources to provide public services among different levels of government. It consists of three major forms of decentralization: deconcentration, delegation, and devolution.

Deconcentration refers to the redistribution of decision-making authority, financial and management responsibility (for specified functions generally on some spatial basis) to lower levels within the central government or to local authorities who are upwardly accountable to the central government (Ribot, 2002). There is no real transfer of authority between levels of government. Delegation refers to a situation in which the central government transfers responsibility for decision making and the administration of service delivery to local governments or to semi-autonomous organizations (agencification) that are not wholly controlled by the central government, but are ultimately accountable to it (Rondinelli, 1981 and 1989). Devolution refers to a situation in which the central government transfers authority for decision making, finance and management of service delivery to local governments that elect their leaders, raise their own revenues, and have independent authority to make investment decisions (Rondinelli, 1981 and 1989).

Privatization and Public Private Partnership are included in the category of market decentralization because they shift the responsibility of service delivery to the private sector.

Privatization refers to a situation in which the central government transfers ownership of a business, enterprise, agency or public service to the private sector. In a broader sense, privatization refers to the transfer of any government function, particularly in service delivery, to the private sector. It involves different financing mechanisms, as the service beneficiaries are generally charged for the delivered service. Public Private Partnership (PPP) refers to a situation in which the central government transfers responsibility for decision making and the administration of service delivery to a non-governmental, private or voluntary organization through a contract-based partnership, in which the private party assumes substantial financial, technical and operational risk. In the broadest sense, PPPs can cover all types of collaboration across the interface between the public and private sectors to deliver policies, services and infrastructure (HM Treasury).

Figure 1.1 Decentralization from central government

Source: Developed by author (based on Cheema, Rodinelli and Nellis, 1983, as cited in UNDP, 1998, p.1).

Based on the above explanation, it is possible to conclude that decentralization (Figure 1.1.) includes the transfer of responsibility for planning, management and resources from the central government to service delivery partners, such as: (a) filed units of central government ministries or agencies; (b) subordinate units or levels of government; (c) semi-autonomous public authorities or corporations; (d) area-wide, regional or functional authorities; or (e) non-governmental, private or voluntary organizations (Cheema, Rodinelli and Nellis, 1983, as cited in UNDP, 1998, p.1). This links the term decentralization to the notion of participation and sharing of responsibility through the active involvement of civil society. Based on the definition, although widely used distinctions of decentralization that change the mobilization of public resources and stakeholders are delegation and devolution (Rondinelli, 1981 and 1989), it consists of all types of authority and responsibility transfer, including privatization and partnership with private sector organizations. The main difference between the decentralization categories is in the control level by the central government and the discretion level in decision making.

Decentralization does not necessarily imply less central government control; it may only mean spreading central control across organizations, thereby, in fact, strengthening the outreach of supervisory power of the central authorities.

This dissertation contemplates the decentralization concept from functional and relational approaches, instead of the structural instrumental approach. The main premise of decentralization emphasizes the separation between policy making and implementation, which transfers most service delivery functions to service delivery partners. The functional segregation of policymaking and implementation drives both the structural segregation of policy implementation from central governments and the functional integration of the function as service delivery partners. It shapes the business process of central governments by redefining the roles of central governments from a direct role to a more indirect role in the provision of public service (Batley and Larbi, 2004). As a result, it has developed a performance regime model

Central government

(b) local governments and semi-autonomous agencies, which are not wholly controlled but ultimately accountable to central government

(a) subordinate units or levels of government that are accountable to central government

(c) area-wide, regional or functional authorities that have independent authority to elect leaders, raise revenue and make investment

(d) non-governmental, private or voluntary organization Privatization,

Public Private Partnership Devolution to local

authorities Delegation (including agencification) Deconcentration

(Talbot et. al, 2005): ‘strategic centralization’ and ‘operational decentralization’, which outline fundamental concepts in the relationship between the central government and service delivery partners. Decentralization puts central governments (cabinet level) in charge of setting government objectives, policy making and regulation, which are translated into implementation.

Service delivery partners are in charge of policy implementation and service delivery. The extent to which a central government has to translate programs and outcome targets for service delivery partners depends on the decentralization level.

1.1. Functional segregation and redefinition of business processes of central governments and service delivery partners

A government has three main functions in policy making, regulation and service delivery, which are delivered through a combination of businesslike and non-businesslike processes, and of job-order type and process-type business processes.

Table 1.1 Businesslike and non-businesslike organizations C1 Businesslike Non-Businesslike

Profit Oriented Private companies, state-owned

enterprises

Non-Profit Type A Non-budget-dependent semi-autonomous agencies

Non-Profit Type B Budget-dependent semi-autonomous agencies

Non-Profit Type C Bureaucratic units

C2 Businesslike Quasi-businesslike Non-businesslike

Adapted from Anthony, R. (1978), Financial Accounting in Nonbusiness Organizations: An Exploratory Study of Conceptual Issues, p.162, with modifications by the author.

Notes:

1. Non-Profit Type A: a non-profit organization whose financial resources are obtained, entirely, or almost entirely, from revenue from the sale of goods and services. Based on the profit/non-profit category (C1), type A is non-businesslike. Based on the source of resources (C2), type A is businesslike (Anthony, 1978). This type of agency provides financially measurable outputs in terms of revenue (Christiaens and Rommel, 2008).

2. Non-Profit Type B: a non-profit organization that obtains some amount of financial resources from the sale of goods and services, but still receives subsidies from the state budget. The product/service of semi-autonomous agencies is exclusively provided by charging some of the cost to the beneficiaries (financially measurable product/service, but non-profit oriented), and its production cost is more variable than those of public goods (Van Thiel, 2001). In addition to the private goods provided by the private sector, the government provides similar quasi-public goods due to the needs of implementing government policy.

3. Non-Profit Type C: a non-profit organization that obtains a significant amount of financial resources from sources other than the sale of goods and services (Anthony, 1978), mostly from the state budget.

Decentralization in the separation of policy making and implementation has further separated government business processes that are based on the businesslike level and process continuity. It is possible to discuss the definition of the term businesslike from the financial resource (Anthony, 1978) and business area/economic characteristics of products and services (Batley and Larbi, 2004). The businesslike level of an entity determines the influence level of the central government and of stakeholders toward an entity, which further determines the rule in resource

allocation. The more businesslike an entity is, the more likely it is to be influenced by stakeholders and regulated by market rules. On the other hand, the less businesslike an entity is, the more likely it is to be influenced by the central government and regulated by budgeting rules.

Based on process continuity, there are two types of business processes that influence the performance evaluation process: job order type and process type. A Job order type business process consists of specific and customized processes, and accumulates cost per job. Policies and programs are likely to be considered as job order type, as the process is case-specific for a certain period of time and is accustomed to the national policy-making interest during that period.

It might emerge in one period and disappear during the next period. Process type business processes tend to be stable from year to year, as they repeat the same processes to deliver homogeneous products and services.

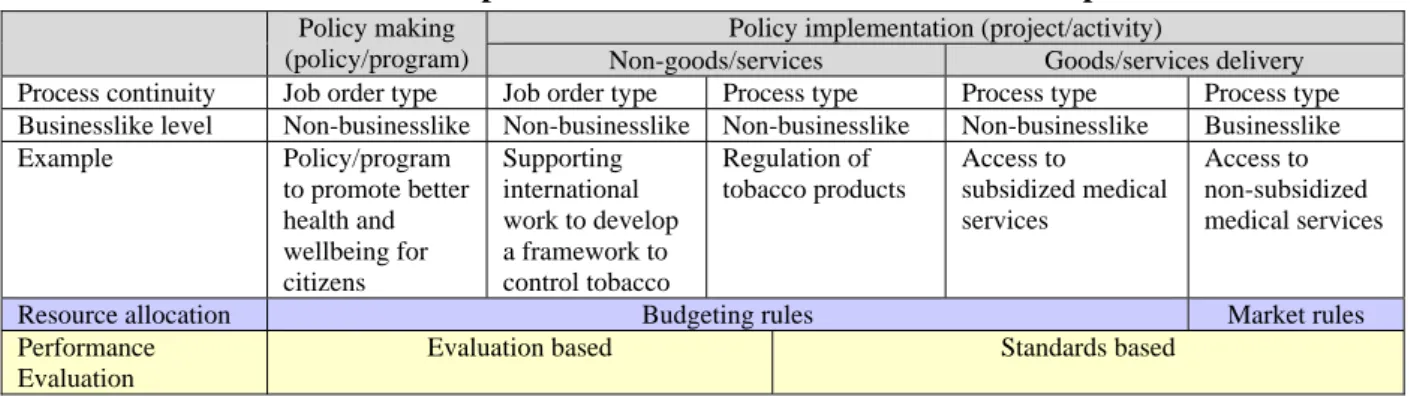

Table 1.2 Resource allocation and performance evaluation based on business processes

Policy making (policy/program)

Policy implementation (project/activity)

Non-goods/services Goods/services delivery Process continuity Job order type Job order type Process type Process type Process type Businesslike level Non-businesslike Non-businesslike Non-businesslike Non-businesslike Businesslike Example Policy/program

to promote better health and wellbeing for citizens

Supporting international work to develop a framework to control tobacco

Regulation of tobacco products

Access to

subsidized medical services

Access to non-subsidized medical services

Resource allocation Budgeting rules Market rules

Performance Evaluation

Evaluation based Standards based

The categorization influences the resource allocation processes as they regulate the cost calculation and evaluation. Job order type businesses process will allocate resources based on estimated costs. Due to this process’s specification of each policy/program, it relies on performance evaluations conducted by beneficiaries. Resource allocation and performance evaluation in process type business processes are conducted based on standard costs. Variance analysis is applicable for both types of business processes to analyze actual and planned performance for the purpose of performance improvement. It is possible to argue that it is easier for the process type business process to measure and benchmark its performance due to the availability of standards. It contributes to the information timeliness, as it would be easier to measure and manage performance if the business process is relatively stable and continuous from period to period. The characteristic of a job order business process highlights the needs to reach for its stakeholders. As there is a lack of standards and comparable performance information, decision makers would have to rely on a relatively subjective performance evaluation by actors and stakeholders, rather than on benchmarking or analysis of variance.

As decentralization redefines the decision-making process, particularly in resource allocation

and performance evaluation through the functional and business process segregation between the central government and service delivery partners, it further redefines the relationship between actors and stakeholders, and it transforms the governance structure from hierarchical and process-based governance into relational and rules-based governance.

1.2. The relation between the central government, service delivery partners and stakeholders in distributed governance

Decentralization has transformed the backbone of public sector governance from hierarchical to distributed governance, as the functional segregation creates structural separation based on functions. Decentralization underlines the concept of distributed governance (OECD, 2002), by not only decentralizing the organization structure and business process but also delegating stakeholder management to the relevant service delivery partners according to their functions. It redefines the mechanisms, processes and institutions at all levels, through which policy makers, service delivery partners and stakeholders participate to articulate their interests, exercise their rights, meet their obligations and mediate their differences toward transparency, efficiency, effectiveness and accountability. In general, decentralizations aim at more horizontal interactions between a central government, service delivery partners and stakeholders, and they are regarded as a way to decrease the perceived gap between the government and stakeholders, to enrich the policy proposals and to increase the likelihood of policy implementation.

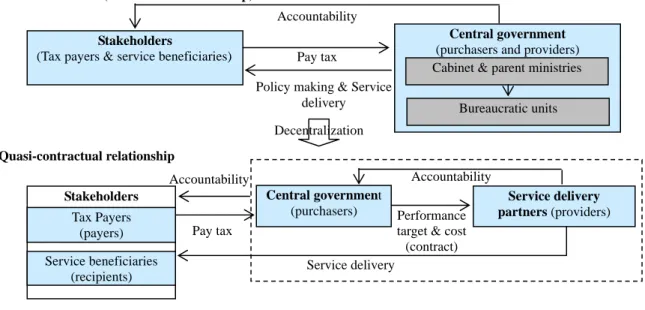

Distributed governance is developed on the concept of a quasi-contractual relationship and stakeholder management and involvement. A quasi-contractual relationship implies that the relation between the central government and service delivery partners is not purely contractual, as the performance evaluation is not only restricted to the conditions of the contract, but it also considers other factors, such as stakeholders’ involvement in performance evaluation based on their experiences and perceived benefits.

1.2.1 The quasi-contractual relationship between the central government, service delivery partners and stakeholders

The public sector has a unique mechanism for the distribution of goods and services that do not follow the market model (see English and Guthrie, 1997). The payers are not always the purchasers or service recipients, as the flow of money is not always concurrent with the flow of service. As a result, transaction intermediaries are needed in the mechanism to regulate and oversee the flow of transaction between payers, purchasers, providers and beneficiaries. In a centralized government, there is no clear identification between the payers/service recipients and purchasers/service providers. The decentralization has further endorsed the use of economic

contestability in the provision of services (Barton, 2001; English & Guthrie, 2001). It underlines the contractual relation between the central government and service delivery partners, which in turn emphasizes the performance and cost concept as a form of performance contracts that develop the performance management system across the new governance structure.

Decentralization enables central governments to better monitor their partners who are in the frontline of service delivery (Fritzen and Ong, 2006). As service delivery partners usually have a great deal of discretion in decision making, the main design issue is to ensure the service delivery partners act as closely as possible in accordance with the government’s objectives through performance contract, performance evaluation and accountability. Service delivery partners implement policies and deliver goods and services to service beneficiaries, and they directly accountable to the central government, while the central government is accountable to stakeholders for the whole process of policy making and implementation.

Figure 1.2 The mechanism for the distribution of goods and services in the public sector

1.2.2. The significance of stakeholder management and involvement

The unique characteristic of the public sector also highlights the significance of stakeholder management and involvement to negotiate and evaluate performance. Decentralization demands a reassessment of the role of the central government and its relationship with the formal and informal public sector organizations, and with its stakeholders in ensuring the accountability of the government (Mishra, 1994). Decentralization changes the focus in the relationship between the government and stakeholders from accountability to more broadly stakeholder management.

It shapes stakeholder management in the central government by bringing performance management closer to stakeholders through the disclosure of performance and accounting

Bureaucratic unit (hierarchical relationship)

Stakeholders Tax Payers

(payers)

Service delivery partners (providers) Central government

(purchasers) Performance target & cost (contract) Service delivery

Accountability

Service beneficiaries (recipients)

Pay tax Stakeholders (Tax payers & service beneficiaries)

Central government (purchasers and providers) Policy making & Service

delivery Accountability

Accountability

Decentralization

Bureaucratic units Cabinet & parent ministries Pay tax

Quasi-contractual relationship

information.

Furthermore, a decentralized government expands the opportunity for stakeholder involvement on a systematic and inclusive basis in the decision-making process and in accountability for performance. This is necessary in order for decisions to be made in an informed and representative manner on the basis of sufficient knowledge of stakeholders’ range of views. In principle, decentralization brings decision-making closer to stakeholders by minimizing institutional obstacles, thereby potentially giving them greater opportunities to participate. By bringing policymakers and implementers closer to the public, decentralization makes it easier for stakeholders to participate and to monitor government performance.

There are different approaches to stakeholder involvement that could be realized under the performance management framework, such as providing reliable and accessible information on services and performance, stakeholder consultation about services and policies, direct stakeholder involvement in designing, delivering or assessing a service, and responsibility devolvement for the delivery of a service. Previous research has found that decentralization improves citizens’ participation and the performance of government services (Crook and Manor, 1995).

Figure 1.3 Quasi-contractual relationships and stakeholder management and involvement

Section 2. Distributed governance as one form of new public governance

Governance consists of a wide variety of mechanisms, processes, institutions and relationships through which individuals, groups and organizations can express their interests, exercise their rights and responsibilities, and mediate their differences (Nelson and Zadek, 2000). It is increasingly about balancing the roles, responsibilities, accountabilities and capabilities of different actors and stakeholders in society (Osborne, 2010).

One of the most widely cited definitions of governance is governance as self-organizing inter-organizational networks (Rhodes, 1996, p.653). Networks are argued to be a means for coordinating and allocating resources – a governing structure – in the same way as markets and bureaucracies (Hughes, 2010). Networks are made up of organizations that need to exchange

Central government

Service delivery partners Stakeholders

Contractual relationship Stakeholder

management by policy making

Stakeholder management by service delivery

resources to achieve their objectives, to maximize their influence over outcomes, and to avoid becoming dependent on other players (Rhodes, 1996). It has developed the concept of NPG, which offers a conceptual model to understand, evaluate and clarify the core challenges of the reality of policy implementation and service delivery (Osborne, 2010). NPG focuses on the institutional and external environmental pressures that both enable and constrain policy implementation and service delivery. It is suggested that the fundamental unit of analysis is the interrelationship between a number of interdependent elements of the performance management system, such as actors and stakeholders, and the wider institutional and environmental contingencies of public service delivery.

Table 1.3 Markets, Hierarchies and Networks

Markets Hierarchies Networks

Basis of relationship Contracts and property rights

Employment relationship

Resource exchange Degree of dependence Independent Dependent Interdependent

Medium of exchange Prices Authority Trust

Means of conflict resolution and co-ordination

Haggling and the courts Rules and commands Diplomacy

Culture Competition Subordination Reciprocity

Source: Bevir, Mark and Rhodes, R. A. W. (2003), Interpreting British Governance, pp. 55, London:

Routledge.

It is argued that the rise of such networks means that the state must be concerned with managing and steering the networks, rather than with direct action (Rhodes, 1996). Although Bevir and Rhodes argue in favor of the reduced privilege, sovereignty, and ability of the central government to steer network governance (2003:53), this dissertation holds that network governance does not mean any necessary decline in the power of a central government at all, but rather, an increased realization of the separation between policy making and implementation, which replaces the formal and bureaucratic model. This dissertation will approach the concept of NPG from decentralization, particularly in the separation between policy making and implementation and how this separation transforms the hierarchical structure to distributed governance. Decentralization has transformed public governance structure toward the development of new public governance, as it changed the relation between actors and stakeholders and shaped the business processes of central government. It has further changed the decision-making process in the PDCA cycle. Distributed governance is developed based on a network based relationship between the central government, service delivery partners and stakeholders, in which all actors and stakeholders are able to steer the network through their functions. As a result, the performance measurement and accounting systems, which are responsible for providing relevant information for the decision-making process, have to be adapted to the decentralized government and distributed governance.

Section 3. Performance management under the progress of decentralization: The change in the role of performance and accrual (cost) information

As decentralization has changed the governance structure and business process, it creates new challenges regarding how to produce similar clear lines of political and performance accountability for distributed governance. It would be challenging to take into account all actors and stakeholders, as this could produce a multitude of performance measures (Wisniewski and Stewart, 2004). In addition, it would be difficult to set targets or to make decisions based on the measurement results, because of conflicting objectives. The conflicting needs of the central government, service delivery partners and stakeholders must somehow be reconciled in the performance management system.

The separation of function between the central government and service delivery partners is expected to resolve the conflict of interest between policy making and service delivery and to deliver the service more efficiently. The separation between policy making and implementation influences the coordination between levels of government and service delivery partners in policy translation and implementation. In their pursuit of effectiveness, governments, regardless of their degree of decentralization or type of constitutional arrangement, need to think about how to manage interdependencies in policies between actors at different levels and functions. Such interdependencies can affect policy initiatives with national implications. Thus, policy plans become ineffective, unless the commitments assumed by the central government can be properly translated and implemented by service delivery partners.

As a result, managing relations between a central government and service delivery partners is a necessity in a decentralized government. The relationship is characterized by mutual dependence, because it is impossible to have a complete separation of responsibilities and outcomes among actors. The coordination between levels and organizations becomes more complicated, as decentralization has changed public sector governance into the “joined-up government” concept (Ling, 2002), which highlights the partnership between actors within a tier of government, different tiers of government, and government and other sectors (e.g. private, NPO, and community). It is a complex and networked relationship – simultaneously vertical across different levels of government, and horizontal within the same level of government.

In order to encourage the policy translation process, governments must first try to bridge a series of gaps with service delivery partners. Each country may experience difference levels of gap, according to the level of mutual dependence and the network-like dynamic in distributed governance and bridging them is one of the primary challenges in distributed governance. The gaps may lead to fragmentation in policy, implementation and service delivery, as each actor

might have different aims and interests.

Policies and programs can be more efficiently and effectively implemented when resources are pooled and information is shared. Performance management can become a tool to help bridge the gaps that exist between the central government and service delivery partners. However, it is a considerable challenge to coordinate performance management undertaken by the central government, as performance outcomes reflect the interaction and coordination of policies between various and networked actors.

Figure 1.4 Gaps in distributed governance

Source: OECD, 2009 (with modification by author).

The NPM has redefined the compliance regime (budget compliance) to suit the performance regime. However, it is decentralization, particularly the separation between policy making and implementation, which has developed a new governance structure of distributed and networked governance. Decentralization has redefined the performance regime in the NPM concept from an intra-organizational focus to the relational and network focus of NPG.

The performance management system must be adapted to the decentralized government and to distributed governance in order to effectively utilize performance and accounting information in decision-making processes. As public governance is categorized into three types, according to the regimes in the public sector (Bevir and Rhodes, 2003; Osborne, 2010), the role of the performance management also changes according to the regimes:

a. Performance management as a hierarchical accountability tool in administrative governance, which is concerned with the effective application of public administration and its repositioning to encompass the complexities that are vertically integrated policy making and implementation, as a closed system within the hierarchical structure of government (Salamon, 2002; Lynn et al., 2001, Milward and Provan, 2003).

b. Performance management as a management tool in contract governance, which is concerned with the governance of contractual relationships in the delivery of public services under the New Public Management regime (Kettl, 1993, p.207; Kettl, 2000).

Information gaps

Capacity

gaps Fiscal gaps Administration

gaps Policy gaps

Central Gov

Service delivery partners Performance Management

Performance measurement and accounting systems

Multi-year budgets

Legal mechanism and standard setting (integration mechanism, inter-sectoral collaboration)

Grant, co-funding arrangement based on performance contracts

Performance information is essential in NPM to set targets in management contracts and to focus on efficiency by comparing the targets and actual performance. This suggests that NPM adopts a perspective on performance that differs from the traditional public sector approach. The focus of NPM on efficiency implies a more explicit internal perspective of performance than in traditional public management, and the focus on outputs and results implies a customer perspective of performance. The adoption of NPM implies that the traditional and primarily financial perspective of the performance of governmental organizations has to be broadened (Jansen, 2008).

c. Performance management as rules and routines in the distributed and networked governance, which is concerned with how to regulate self-organizing inter-organizational networks to implement public policies and to deliver public services both with and without the government (Rhodes, 1997; Kickert, 1993; Denters and Rose, 2005; Entwisle and Martin, 2005). The performance management system should accommodate the quasi-contractual relationship and stakeholder management by providing verifiable performance target and cost information. The performance management system should accommodate the link between the policy-making level and the policy-implementation level. The performance regime model requires the government to strike the right balance between coordination and subordination between the central government and service delivery partners on the one hand and between autonomy and performance accountability on the other hand (OECD, 2002).

Table 1.4 Comparison of three regimes in the public sector

Paradigm/

Key elements

Theoretical roots

Nature of the state

Focus Emphasis Resource allocation mechanism

Nature of the service

system

Value bases

Public Administration

Political science and public policy

Unitary The political system

Policy creation and

implementation

Hierarchy Closed Public sector ethos New Public

Management

Rational/public choice theory and management studies

Regulatory The organization

Management of organization resources and performance

The market and classical or neo classical contracts

Open rational

Efficacy of competition and the market place New Public

Governance

Institutional and network theory

Plural and pluralist

The organization in its environment

Negotiation of values, meaning and relationship

Network and relational contracts

Open closed Dispersed and contested Source: Osborne, S. P. (2010), The New Public Governance: Emerging Perspective on the Theory and Practice of public governance, Routledge.

The NPG has changed the two key issues of performance management: accountability and performance evaluation. Accountability and performance evaluation, where services are evaluated against standards and objectives, are legacies of NPM. NPG has changed the context of accountability by linking formal hierarchy accountability to relationship accountability between service delivery, which requires an accounting system that goes beyond traditional formal accounting approaches and focus (Gray, 2002). NPG has changed the focus of

performance evaluation to evaluating the performance of the collaborative network of multi-organizations. As the reality of public service regimes has evolved, performance management has not evolved, but remained stagnant within the open rational system of NPM, as will be shown by the case studies presented in this dissertation.

Table 1.5 An explanatory model of the interaction between public policy implementation, service delivery regimes and managerial practices

Policy and service regime

Focus on managerial action

Policy Organization Environment

Public Administration Street-level bureaucracy Professional practice Political management New Public Management Cost of democracy Organizational performance Competitive market behavior New Public Governance Stakeholder management Boundary spanning and

boundary maintenance

Sustainable public policy and services

Source: Osborne, S. P. (2010), The New Public Governance: Emerging Perspective on the Theory and Practice of public governance, Routledge.

The inability of performance management to accommodate the decentralized government leads to ambiguity in performance information (March, 1994), which is a situation where performance information loses its validity and relevance in decision making. Consequently, performance and accounting information is prepared only to comply with the regulation requirements and reporting purposes. It is not used with the intensity as implied by many studies. As a result, defining and compiling performance and accounting information is not only the first step, but the last one as well (Schick, 2007). Reform in performance measurement and accounting systems – particularly, the implementation of accrual accounting – tends to emerge and gradually fade into routine paperwork, as demonstrated in this dissertation’s case studies. Furthermore, ambiguity of performance information will pose problems in a result-oriented organization, as the planning and control processes are performance driven. It will arise in the interpretation of performance indicators and their variances, thus presenting the risk of misleading decision-making processes or providing opportunities to manipulate results. It will influence decision makers to behave not in the rationalist manner, as implied in the NPM model (i.e. Christensen and Yoshimi, 2001 and Lapsley and Pallott, 2000), as the performance and accounting information loses its relevance in decision making.

Despite the theoretical conviction that performance and accounting information could facilitate decision making and problem solving to answer the government’s performance challenges, previous studies’ findings show different and disappointing outcomes resulting from the same approach in adopting performance and (accrual) accounting reform measures. Many countries have approached performance ambiguity with the introduction of a more sophisticated performance measurement and accrual accounting system. However, it does not necessarily ensure the managerial use, as the weight given to performance and accounting information in the decision-making process will depend on the quality (relevance) of the information, which emphasizes the significance of a well-developed and integrated performance management

system. Given this longstanding debate, this dissertation will explore the potential of New Public Governance as a theoretical framework to investigate how performance measurement and accounting systems may become more firmly embedded at a conceptual level to facilitate policy making and service delivery.

Section 4. The scope of the study

Democracies, either parliamentary or presidential systems, have been conceptualized as chains of delegation of authority from citizens to elected politicians and from elected politicians to bureaucracies. In the last two decades, OECD, transitional economies and developing countries have developed a trend of delegation from politicians to agencies, which separate bureaucracies from agencies. These agencies have important implications for the roles and authority of ministers and the capacity of governments to enforce policy. Countries that create agencies are not merely importing new administrative structures, but they are also making significant changes in government operations. Decentralization within the hierarchy of a central government to agencies has shaped the role of the central government in policy making. Although there are still agencies involved in policy making in some countries, this dissertation will focus on agencies in policy implementation and service delivery, and consider agencies that are involved in policy making as part of the central government.

Decentralization to agencies is different from the other type of decentralization. It does not involve political decentralization, as in the case of decentralization to a local government. It is also distinct from privatization and PPP, as it does not introduce the concept of the full market mechanism. Decentralization to agencies will shape the performance management of the central government through the quasi-contractual relationship, stakeholder management and involvement, and the dichotomy of business processes within the hierarchy, as semi-autonomous agencies share the performance management system with the central government. Agencification is considered to be the last piece of the puzzle needed to transform the role of the central government as the policy maker, given that the agencies are established to implement policies or to provide goods and services that the government does not have to provide, but that are likely to be neglected by the private sectors. The establishment of agencies enables the central government to concentrate on policy making.

The quasi-contractual relationship and stakeholder management have their greatest challenges in the decentralization to departmental units (deconcentration) and to semi-autonomous agencies (agencification). The agencies are included within the hierarchy of the central government, but considered as arm length partners in service delivery. Unlike the other service delivery partners in the private sector, the central government – as the only purchaser of goods or services, similar

to monopsony1 – may dictate terms to agencies in the same manner that a monopolist controls the market for its buyers. The strong influence of the central government has weakened the bargaining power of agencies in the quasi-contractual relationship, running the risk of a return to non-contractual hierarchical relationships, unless performance targets and cost information are enforced in the quasi-contractual relationship and stakeholder management.

Discussions about the adoption of performance measurement and accrual (cost) accounting techniques by the public sector have been so widespread, that questions as to how to utilize the performance and accounting information in the decision-making process or how to integrate the performance measurement and accounting system into the government’s PDCA cycle have penetrated every layer of the public sector over the past decade (Pallot, 1994; Shand, 1995;

English et al., 2000 and Carlin, 2005). These issues are also still pondered by interested parties in jurisdictions ranging from those that have adopted comprehensive sector-wide performance management systems such as the United Kingdom (Likierman, 2000), those that are in the stage of early implementation of performance management systems, such as Japan, to those announcing future moves to performance management systems such as Indonesia.

After decades of advocacy for accrual accounting in the public sector, there are some growing questions about the impact of accrual accounting on the management and performance of government organizations, as it is reported that there have been few successful stories in terms of the implementation of the accrual concept. Only a few OECD member countries – Australia, New Zealand, Iceland, and the United Kingdom – have implemented the accrual concept in their financial systems. Others have incorporated the accrual concept only to some degree into their financial management systems (US GAO, 2000). Furthermore, an increasing body of literature has expressed skepticism and criticized the adoption of accrual accounting by public organizations on both theoretical grounds (Carnegie and Wolnizer, 1995; Christiaens, 1999;

Ellwood, 1999; Guthrie and Johnson, 1994; Guthrie, 1998; Lewis, 1995; Ma and Matthews, 1993; McRae and Aiken, 1994; Oettle, 1990; Monsen, 2002; Montesinos et al., 1995; and Stanton and Stanton, 1998) and practical considerations (Carlin and Guthrie, 2001; Guthrie, 1998; Hodges and Mellett, 2003; Newberry, 2002; and Stanton and Stanton, 1998).

Among the OECD member countries, Japan is considered to be lagged behind (Hood, 1995;

Kokubu, 1998; and Yamamoto, 2004) in the area of public sector reform, particularly in the implementation of performance measurement and accrual-based accounting. Japan and Indonesia started their public sector reforms at almost at the same time and share similar patterns.

The Japanese and Indonesian governments faced the same problem when they introduced

1 A market form in which only one buyer faces many sellers.

performance measurement and evaluation system as the system designed to be completed internally without stakeholder involvement (see Kudo, 2003). Japanese central government prepared its first balance sheet for the fiscal year of 2000 and consolidated government-wide accrual based financial statements for the fiscal year of 2003. Nevertheless, adding to the growing number of less satisfactory results in the implementation of accrual-based accounting, a 2007 survey conducted by Japan’s Ministry of Finance showed that there were rarely positive opinions about the implementation of accrual-based accounting in the central government.

Meanwhile, Indonesia’s central government published its first balance sheet for the fiscal year of 2004, but it is still struggling to improve the quality of its modified accrual financial statements as the Supreme Audit Board renders disclaimer opinion for four consecutive fiscal years.

Despite the slow implementation progress of performance measurement and accounting systems in the central government, the establishment of semi-autonomous agencies in both countries as pioneers in the implementation of performance measurement and accrual accounting systems has contributed to the implementation progress of both systems, as well as to the utilization level of performance and accrual (cost) information in decision making. This dissertation will elaborate on how the decentralization to semi-autonomous agencies, particularly in emerging countries’

public sector reforms such as in Japan and Indonesia, influences reforms in performance measurement and accounting systems and changes their roles in the performance management system of the new governance structure.

CHAPTER 2. LITERATURE REVIEW

Section 1. Limitations of previous research regarding performance management

NPM has made some attempts to introduce businesslike practices to the public sector. As NPM concepts are likely to be applicable (if the concept is directly translated) to the businesslike part of government (Christiaens and Rommel, 2008), it is particularly important to carefully and selectively reconsider the implementation of these concepts. Metcalfe (Pallot, 1998 and 1999) highlights the need to move beyond the imitation of business management to innovations that are more suited to the government sector. Ittner and Larcker (1998, p. 233) also argued that:

“Perhaps the most fundamental question is whether private sector notions of performance measurement and accountability are applicable in the public sector”. This further highlights the necessity to apply the same consideration into the plan to adopt the accrual concept in the public sector. There is a call for the ‘new cameralistic accounting’, a new concept that combines budgeting accounting with accrual information in an integrated way or separately (Lüder and Jones, 2003, Groot and Budding, 2008; Christiaens and Rommel, 2008).

Hybrid business processes, combined with a mechanism for the distribution of goods and services in the public sector that does not follow the market model appearing in the private sector (Guthrie and English, 1997), have provided possible explanations for why simply translating the language of the private sector with minor modifications is unlikely to accurately or appropriately represent the interests and needs of the actors and multiple complex stakeholders in the public sector (Bendheim and Graves, 1998). The issue of multiple actors and stakeholders in the public sector, in comparison to the focus of the private sector on customers, presents difficulties that must be addressed when attempting to adapt private sector approaches to the public sector, also it will become the foundation for building any performance management system in the public sector, differentiating it from that of the private sector.

Bendheim and Graves (1998) suggest that all of the factors involved in performance measurement and management systems are influenced by the overarching effect of multiple actors and stakeholders.

The unique mechanism for the distribution of goods and services in the public sector has shaped the role and the significance of stakeholders in strategic performance management of the public sector, which is different from those of the private sector, because the “success” of public organizations depends on satisfying key stakeholders according to their definitions of what is valuable (Bryson, 1995). Consequently, the performance management system should emphasize the reciprocal relationship between actors and stakeholders, not only from the perspective of

quasi-contractual relationships, as suggested by the NPM principle, but also from the perspective of stakeholder management and involvement, as suggested by the NPG.

Some research endeavors study the role of stakeholders in performance measurement systems and their utilization of performance information (Mc Adam, Hazlett, Casey, 2005; Rantanen, Kulmala, Lönnqvist, Kujansivu, 2007). However, these studies mainly discuss the significance of stakeholder-driven performance management without linking it to the impact of decentralization toward the distributed and networked governance structure. As NPM emphasized that the outcome of effective and strategic performance management will be reached only by integrating the performance measurement and accrual concept into the government PDCA cycle, new public governance further recognizes the role of performance measurement and accrual accounting to regulate the interaction between actors and stakeholders in the PDCA cycle.

Discussions about the adoption and utilization of performance measurement and accrual accounting techniques in the decision-making process have penetrated every layer of the public sector over the past decade (Pallot, 1994; Shand, 1995; Hatry, 1999; English et al., 2000 and Carlin, 2005). However, these discussions focus on the technical changes of performance measurement and accounting systems from the NPM perspective, rather than considering the change from a broader perspective of governance and business processes. Research regarding the accrual concept has focused on widespread debate on whether the accrual concept is appropriate for and should be adopted by the public sector, including public sectors in developing countries (Oettle, 1990; Ma and Matthews, 1993; Guthrie and Johnson, 1994; McRae and Aiken, 1994;

Carnegie and Wolnizer, 1995; Lewis, 1995; Montesinos et al., 1995; Guthrie, 1998; Stanton and Stanton, 1998; Christiaens, 1999; Ellwood, 1999; Monsen, 2002; Newberry, 2002; Carlin and Guthrie, 2003; Hodges and Mellett, 2003; Athukorala, 2003). Despite the debate, almost all scholars agree that governmental accounting reform needs an adequate, well-developed conceptual performance management framework, which prescribes the perspective, aim, users and consequences of the PDCA cycle. Once these specifications are known, one can create and implement the framework in terms of more explicit rules and regulations. The academic field of public administration, however, is lagging behind in terms of the attention paid to building the conceptual framework of performance management, particularly in emerging decentralized central governments: how the decentralization process changes the way to integrate and utilize performance and accounting information in the government PDCA cycle through changes in governance and business processes.

Decentralization helps to clearly identify the central government, service delivery partners and stakeholders, and this in turn helps to redefine the unique mechanism for the distribution of