320

LEMONS, AUCTIONS, AND

INFORMATION AGGREGATION

I

n this chapter, I present some examples of how incomplete information af fects trade and the aggregation of information between two or more eco nomic agents. Each of the settings is modeled as a static game.MARKETS AND LEMONS

You may have had the experience of buying or selling a used automobile. If so, you know something about markets with incomplete information. In the used car market, sellers generally have more information about their cars than do prospective buyers. A typical seller knows whether his car has a shrouded en gine problem-something that the buyer might not notice but that would likely require a costly repair before long. The seller knows whether the car tends to overheat in the summer months. The seller knows the myriad idiosyncracies that the car has developed since he acquired it. Prospective buyers may know only what they can gather from a cursory inspection of the vehicle. Thus, buy ers are at an informational disadvantage. You would expect that, as a result, the buyers would not fare well in the market. Nonetheless, sellers might lose if the market failed owing to justiiably cautious buyers. I

To illustrate, suppose Jerry is in the market for a used car. One day he meets a shifty looking man named Freddie, who offers an attractive ifteen year-old sedan for sale. Jerry likes the car's appearance. He imagines himself at the wheel, cruising up and down Broadway, taking in the flirtatious glances of many a woman through his sunglasses. Then he imagines the engine explod ing, followed by an embarrassing scene in which he watches from the curb as a irefirhter dowses his vehicle with water. Jerry says to Freddie, "The car looks b rood but how do I know it isn't a lemon?" Freddie rejoins, "You have my

�

ord'; this car is a peach; it's in great shape!" Jerry insists, "Galimatias! Let's put aside the hep-talk. Since I will not likely see you again, your word meansI The trading example that I present here is inspired by G. Akerlof, "The Market for Lemons: Qualitative Uncertainty and Ihe Market Mechanism." QI/arterly lOl/mal oj Ecollomics 84( 1970):488-500. For hIs work, George Akerlof was awarded the 2001 Nobel Prize in Economics, with corecipients A. Michael Spence and Joseph Stiglitz.

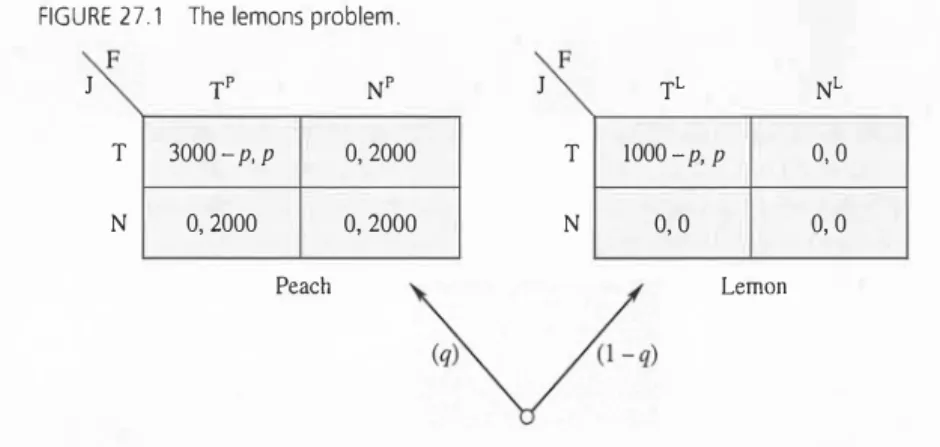

FIGURE 27.1 The lemons problem.

J F TP NP

T 3000-p, p 0,2000

N 0,2000 0,2000

Peach

J F

T N

TL 1000-p, p

0,0

Markets and lemons 321

NL 0,0

0,0 Lemon

nothing to me. I know game theory and, as Professor Watson clearly explains, you have no way of, or interest in, establishing a reputation with someone you will never see again." Freddie nods and says, "Okay, let's talk turkey. The

Blue

Book

tells us the market price for this car.2 You can look the car over as you please. In the end, you will have to decide whether you are willing to pay theBlue Book

price for the car, as I must decide whether to ofer the car at this price."Interaction between Je'y and Freddie may be quite elaborate, but I would like to abstract from this complexity and simply focus on the bottom line. Suppose there is some ixed market price for fifteen-year-old sedans of the . type that Freddie is selling. Call this exogenously given price p. Assume that Jerry and Freddie play the game depicted in Figure

27.1.

Nature first chooses whether the car is a peach or a lemon. If the car is a peach, then it is worth$3000

to Jerry and$2000

to Freddie. If the car is a lemon, then it is worth$1000

to Jerry and$0

to Freddie. Note that, in both cases, Jerry values the car more than does Freddie, so eficiency requires that the car be traded and the surplus (in each case$1000)

be divided between them. But there is incomplete information; Freddie observes nature's choice, whereas Jerry knows only that the car is a peach with probability q. Then the players simultaneously and independently decide whether to trade (T) or not (N) at the market price p. If both elect to trade, then the trade takes place. Otherwise, Freddie keeps the car.Two kinds of equilibria are possible in this game. In the first kind, only the lemon is traded. Let us check whether there are values of p for which only the lemon is traded in equilibrium. That is, Jerry selects T and Freddie plays the

2The Kelley Bille Book is a publication in the United States that establishes price guidelines for used automobiles.

322 27: lemons, Auctions, and Information Aggregation

strateuy NPTL (no trade if peach; trade if lemon). In order for Freddie's strategy to be

�

ptimal, it must be that0 :: p

andp :: 2000

(otherwise Freddie would either not want to trade a lemon or want to trade a peach). In order for Jerry's strategy to be optimal, it must be that Jerry is willing to trade,conditional on

knowing that Freddie only ofers the lemon for sale.

Jerry obtains an expected payoff ofq . 0

+(1 - q) (1000

-p)

if he chooses T,0

if he chooses N. Jerry is willing to trade if and only if(1

-q)(1000

-p) :: 0,

which simpliies to

p :: 1000.

Putting the incentive conditions together, we see that, ifp

E(0, 1000),

then there is an equilibrium in which only the lemon is t.·aded. Intuitively, if the market price is below$1000,

Freddie would want to bring only the lemon to market. Anticipating that only a lemon will be for sale, Jerry is willing to pay no more than$1000.

The second kind of equilibrium features t·ade of both the lemon and the peach. That is, Jerry selects T and Freddie plays the strategy TPTL. In order for this equilibrium to exist, the market price must be high enough so that Freddie is willing to sell the peach; speciically,

p :: 2000.

In addition, Jerry's expected value of owning the car must be at least as great as the price. That is, it must be that3000q

+1000(1 - q) :: p,

which simpliies to

1000

+2000q ::

p. Thus, there is an equilibrium in which both types of car are traded as long as1000

+2000q :: p :: 2000.

Note that there is a price

p

that works if and only if1000

+2000q :: 2000,

which simplifies to

q :: 1/2.

In words, unless the probability of a peach is sufficiently high (there are not too many lemons in the world), there is no equilibrium in which the peach is traded.If

q

<1/2,

then only lemons are traded in equilibrium. Recall thatthis outcome is

ineicient,

because trading the peach creates value. Thus, the model demonstrates that asymmetric information sometimes causes markets to malfunction.AUCTIONS

Auctions 323

In the lemons example, the seller has private information about his and the buyers' valuations of the good to be traded. Other markets have diferent in formation structures. In many instances, prospective

buyers

have private infor mation about their valuations for the good. Furthermore, diferent prospective buyers have different tastes, needs, and abilities, leading to variations in peo ple's willingness to pay for things such as houses, artwork, and productive inputs.The seller of a good naturally wants to trade at the highest price that she can obtain. When the seller has one object to sell and there are multiple poten tial buyers, the seller would like to ind the buyer with the highest willingness to pay for the object and then consummate a deal with this buyer at a price close to the buyer's valuation of the good. Unfortunately for the seller, she may not know the prospective buyers' valuations. One way for the seller to encourage competition between prospective buyers and to identify the highest valuation is to hold an auction.

Auctions are quite common in reality. All sorts of merchandise is sold at formal and informal auction houses, often over the Internet. Many diferent auction formats are in use as well. There are sealed-bid auctions, where bidders simultaneously and independently submit offers; sealed bids are often used in home sales and for government procurement. There are dynamic oral auctions, where an auctioneer suggests prices in a sequence and the prospective buyers signal or call out their bids. Several versions of these auction forms are in prominent use.

To give you a taste of auction theory and its elemental intuition, I shall present an analysis of two examples of sealed-bid auctions. Imagine that a person-the seller-has a painting that is worth nothing to her personally. She hopes to make some money by selling the art. There are two potential buyers, whom I call bidders