Evidence from Japanese Scanner Data Publications Tsutomu Watanabe

全文

図

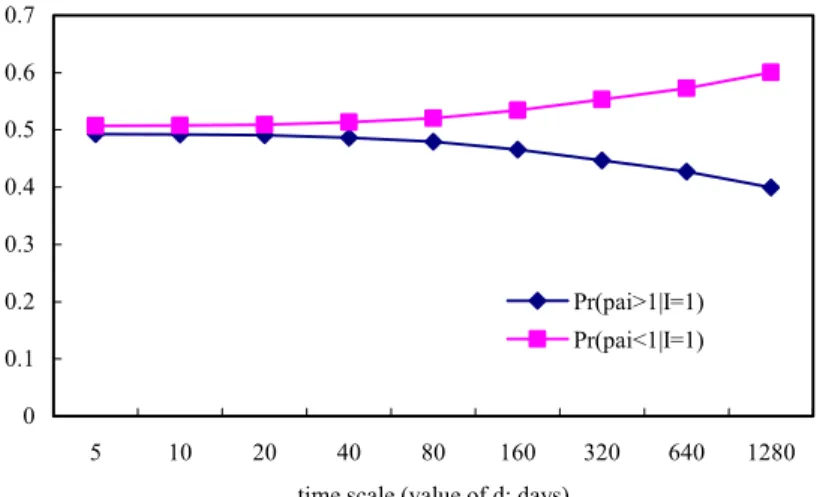

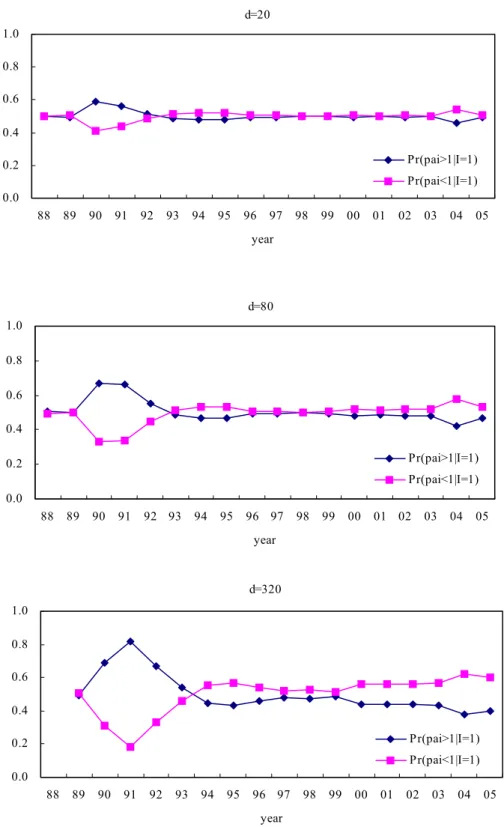

![Table 5: Prediction Errors by Price Duration Predicted minus actual values for log Pr[Π d t < 0.93 | I t−dd = · · · = I t−ndd = 0, I t−(n+1)dd = 1] Duration [days] G0 G1 G2 G3 G4 10 0.043 0.061 0.069 0.066 0.029 15 0.046 0.064 0.071 0.075 0.039 20 0.047](https://thumb-ap.123doks.com/thumbv2/123deta/5651019.6490/26.892.250.668.285.604/table-prediction-errors-duration-predicted-actual-values-duration.webp)

関連したドキュメント

Throughout our present work we study the Heston model of pricing for European call options on stocks with stochastic volatility (Heston [27]) by abstract analytic methods coming

We present European call option pricing formulas in the case of ergodic, double-averaged, and merged diffusion geometric Markov renewal processes.. Motivated by the geometric

In the previous section, we revisited the problem of the American put close to expiry and used an asymptotic expansion of the Black-Scholes-Merton PDE to find expressions for

By using the averaging theory of the first and second orders, we show that under any small cubic homogeneous perturbation, at most two limit cycles bifurcate from the period annulus

In [6], Chen and Saloff-Coste compare the total variation cutoffs between the continuous time chains and lazy discrete time chains, while the next proposition also provides a

(4) The basin of attraction for each exponential attractor is the entire phase space, and in demonstrating this result we see that the semigroup of solution operators also admits

“Breuil-M´ezard conjecture and modularity lifting for potentially semistable deformations after

Then it follows immediately from a suitable version of “Hensel’s Lemma” [cf., e.g., the argument of [4], Lemma 2.1] that S may be obtained, as the notation suggests, as the m A